In 2026, HDB is set to launch 19,600 Build-to-Order (BTO) flats. That includes some 4,000 units (about a fifth) with waiting times of under 3 years! It's going to be an exciting year ahead for prospective homeowners.

But if this is your first BTO application, excitement might quickly give way to intimidation and confusion when you find out how long the process can be. And don't even get us started on the acronyms that can make you want to tear your hair out.

Regardless of where you are in your home ownership journey, don’t fret—you’re not alone. In our comprehensive guide, we will delve into the various steps involved in purchasing an HDB BTO flat in Singapore, covering everything from determining your eligibility to the application process to your considering your financing options.

By the end of this guide, you should have a clear understanding of what it takes to navigate the HDB BTO flat-buying process and make an informed decision that suits your needs and preferences.

Check out our review of the latest HDB BTO sales launch: HDB BTO Feb 2026 Review—Locations, Application Rates, Prices, and More

We're also expecting a June 2026 BTO launch soon—look out for our review of the projects.

[ms-toc title="A step-by-step guide to buying an HDB BTO flat in Singapore (2026)"]

Watch: Buying an HDB BTO in Singapore—from Flat Application to Key Collection

1. Timeline and steps to buying an HDB BTO flat in Singapore

So, what steps need to happen to get a BTO flat? And how long does each stage of the HDB BTO process takes? The timeline below shows every key step, so you know exactly what to expect from eligibility checks to key collection. Use it for a quick snapshot before you dive into the details.

Step | What to do | When to do it | Documents required |

Check eligibility | Apply for an HDB Flat Eligibility (HFE) letter. This letter not only lets you apply for a flat, but also tells you if you’re eligible to buy one, apply for grants, and take up a loan. | Apply by the 15th, at least 2 months before the BTO launch month. For example, if the BTO launch is in Jun 2026, apply for your HFE letter by 15 Apr 2026. | Apply via Singpass. |

Apply online | Apply for a flat on the HDB Flat Portal. It costs $10 per application. | During the sales launch. The window will be open for 1 week. | You must have a valid HFE letter to apply for a BTO flat. |

Get ballot results | Look out for an email from HDB—it’ll tell you your ballot results. | Up to 2 months after applications close. | – |

Book a flat | Book a flat based on your queue position at HDB Hub. You’ll need to pay the option fee: | – BTO and SBF: From 4 weeks after ballot results. |

|

Sign agreement for lease | Pay downpayment. Ensure you have a valid Letter of Offer if taking a bank loan. | Within 9 months after booking a flat. |

|

Collect keys | Pay the balance purchase price and collect your keys. |

|

|

2. Are you eligible for HDB BTO?

To buy an HDB BTO flat, you’ve got to first check if you're eligible. Otherwise, the government is going to slam the door in your face.

You must be at least 21 years old and satisfy one of the following in order to purchase a BTO flat:

- Fiancé and fiancée: At least 1 of you is a Singapore Citizen, and the other is a Singapore Citizen or PR. Be prepared to register your marriage before taking possession of your flat if applying for additional or Enhanced CPF Housing Grant or within 3 months of taking possession of flat.

- Married couples and/ or parent(s) with child(ren): You are a Singapore Citizen, applying with at least 1 other Singapore Citizen or PR as a family nucleus. This means you are applying with:

- Spouse and kids (if any); OR

- Parents and siblings (if any), and if you're unmarried/ widowed/ divorced, at least one of your parents is a Singapore Citizen/PR; OR

- Your child(ren) under your legal custody (only for widowed/divorced applicants).

- Multi-generation families: You are a Singapore Citizen, and are applying with your spouse and parents. Aside from you, at least 1 other applicant must be a Singapore Citizen or PR. This sounds like the "married couple with parents" eligibility condition above, but the difference is that under this scheme you'll be eligible for a 3Gen flat.

- Orphaned siblings: You and your siblings are orphans and single (unmarried, divorced, or widowed) and at least 1 of your deceased parents was a Singapore Citizen or PR.

- Families with non-residents: You are a Singapore Citizen applying with your non-resident spouse who holds a valid Visit Pass or Work Pass that can have any validity period. If you apply with your non-resident parents or child(ren), you'll only be eligible to buy a resale flat and not a new flat like a BTO.

- Seniors: You are a Singapore citizen aged 55 and above. You can also apply with your fiancé/ fiancée or spouse, parent(s) or child(ren), siblings who are orphans and single, your non-resident spouse, or unrelated single citizens. With the exception of your non-resident spouse, the others you apply with must be a Singapore Citizen/PR. Under this scheme, you can buy a short-lease 2-room Flexi flat or Community Care Apartment.

- Singles: You are a single Singapore Citizen aged 35 and older applying alone OR with up to 3 other singles, of which at least 1 must be a Singapore Citizen/PR. Note that you'll only be eligible for 2-room flats, but they can be in any location.

Read more about HDB's eligibility requirements when you apply as a couple or family, senior, or as a single.

ALSO READ: Can Singles Buy an HDB Flat in Singapore? Here’s What You Need to Know

In addition, you’ll have to ensure you’re not making too much money to qualify for the flat you’re eyeing. Here are the income ceilings for the various types of flats:

- 2-room Flexi flat: $7,000; or $14,000 for short-lease flats (max 45-year lease)

- 3-room flat: $7,000; or $14,000 depending on which project you’re balloting for. Check the sales launch to know the exact income ceiling.

- 4-room flat or bigger: $14,000; or $21,000 if you’re purchasing the flat as an extended or multi-generation family.

Note that your children included as co-applicants or occupiers also contribute to the total household income if they're earning an income. Include their salaries when you're adding things up to make sure you don't bust that income ceiling as an extended family.

ALSO READ: What Counts as Income When You’re Buying a Flat in Singapore?

You (and anyone else in your BTO application) must also not own any other property, HDB or private, locally or overseas.

- If you currently own private property, you’ll need to sell off your property at least 30 months before you apply for the HFE letter, which you in turn should apply for before you apply for your BTO.

- If you currently own an HDB flat, you must dispose of the flat within 6 months of the completion of your BTO flat.

3. Apply for an HDB Flat Eligibility (HFE) letter

Even before you start searching the web for new launches, HDB requires you to first apply for an HDB Flat Eligibility (HFE) letter through the HDB Flat Portal. You will need your Singpass to sign in.

This letter will set out whether you are eligible to buy a flat, apply for the Enhanced CPF Housing Grant and take up an HDB or bank loan. In other words, it will mine your data and tell you most of what you need to know.

You cannot escape applying for the HFE Letter even if you already have all the necessary information. Without it, you cannot even apply for a flat.

It will take about 1 month for the HFE Letter to be issued after receipt of your application and supporting documents. It may be longer during peak periods, so applying earlier is safer. Once you get your hands on it, the HFE Letter is valid for 9 months from the date of issue.

Bottom line: Once you (and your fiancé/family, if applicable) decide you want to try for a flat, you should apply for the HFE Letter as soon as you can. It's better to have it ready rather than wait until a launch you are interested in rolls around.

PSA: If you plan to apply for a BTO flat during the Jun 2026 sales exercise, HDB actually recommended you apply by 15 Apr 2026. That's how early you should apply for it! If you don't have a valid HFE, you can apply for your HFE letter now in time for the next sales exercise instead. |

The HFE Letter is not to be confused with the now-defunct HDB Loan Eligibility (HLE) Letter, which was meant solely for those taking out an HDB Housing Loan. The HLE Letter was meant to be applied for AFTER balloting for a flat, and only those taking out an HDB loan had to apply.

The HFE Letter now replaces the HLE Letter. But do note that every single applicant, regardless of loan, needs to apply for the HFE Letter BEFORE balloting.

4. Look out for sales launches

First, you’ll have to check the HDB website regularly for news of upcoming sales launches. To make life easier, sign up for HDB’s eAlert Service so you can be notified of upcoming launches.

HDB typically announces upcoming BTO projects at least 3 months prior to their launch. This should give you ample time to plan for the location you want.

Although HDB does announce information like the locations, number of projects and flat types in upcoming launches months early, details like their prices, flat classification (Standard, Plus, Prime), and subsidy clawbacks will only be confirmed when applications open (i.e. when the launch, well, launches).

That said, we can make good guesses on how much certain projects would cost and what classification they would fall under. We do this by looking at their locations and referencing past launches. That's exactly what we did for our Feb 2026 BTO review—check it out.

5. Ballot for your BTO

When you see a launch in an area that interests you, pay a non-refundable $10 application fee to ballot for it during the BTO application window.

If you thought striking Toto was hard, try balloting for an HDB flat. How many tries it takes you to get a flat depends on your luck. While some people get it on the first or second try, we’ve heard of cases where couples tried more than 10 times to no avail.

Expect to wait a maximum of 2 months to know if you are successful or not.

See HDB's website for more details on the HDB BTO application timeline and process.

6. Get an HDB Loan…or AIP if you’re taking out a bank loan

Finally! The heavens smile upon you and you receive a decent queue number. After buying 4D on your lucky day, what’s next?

Before you progress to the next stage and sign your life away, it’s worthwhile to plan your finances using this helpful HDB tool.

A crucial part of the financing process is to decide on whom to get your home loan from. You have a choice between taking out an HDB loan vs bank loan.

First-timers typically go for an HDB loan since the downpayment amount that HDB requires is less. But if you’re savvy and have enough savings, you can usually opt for a bank loan to get lower interest rates—we say "usually" because interest rates for housing loans are currently higher than HDB loans.

Here's a pro tip the HDB staff told me when I was booking my own BTO: Choose an HDB loan first if you're unsure. You can later switch from an HDB loan to a bank loan, but cannot switch from a bank loan to an HDB loan.

Either way, you’ll need to get some kind of loan approval in principal BEFORE you chope the flat. You’ll need to have all your loan documents in order to sign the lease agreement.

- HDB loan: You would already have obtained your HFE Letter before you applied for the flat, so there’s no further action needed here. The letter will tell you how much money HDB is willing to loan you.

- Bank loan: You would have concurrently applied for in-principle approval (AIP) from the bank with your HFE letter application.

With the new HFE letter, applicants should have worked out their financing options ahead of time—even before you applied for your BTO. So you would know what your options are.

7. Book your BTO flat and pay option fee

You’ll get called in to select a unit from 4 weeks after the release of the ballot results.

Your queue number will determine your priority in choosing a unit. The number of people allotted queue numbers will exceed the number of units, so if your queue number is way out there, chances are you won’t be able to get your hands on a unit and will have to ballot again.

When it comes time to show up at HDB Hub to book your flat, don’t forget to bring along your IC for identity verification. You may also need the following documents:

Scenario | Document required |

You are married | Marriage certificate |

You are divorced | Divorce certificate |

Your spouse is deceased | Death certificate of spouse |

You are buying a flat under the Family Care Scheme (FCS) (Joint Balloting) or FCS (Proximity) | Your birth certificate and your parents' marriage certificate |

You have applied for a flat under the Family and Parenthood Priority Scheme (FPPS) | A doctor's certification of pregnancy or your child's birth certificate |

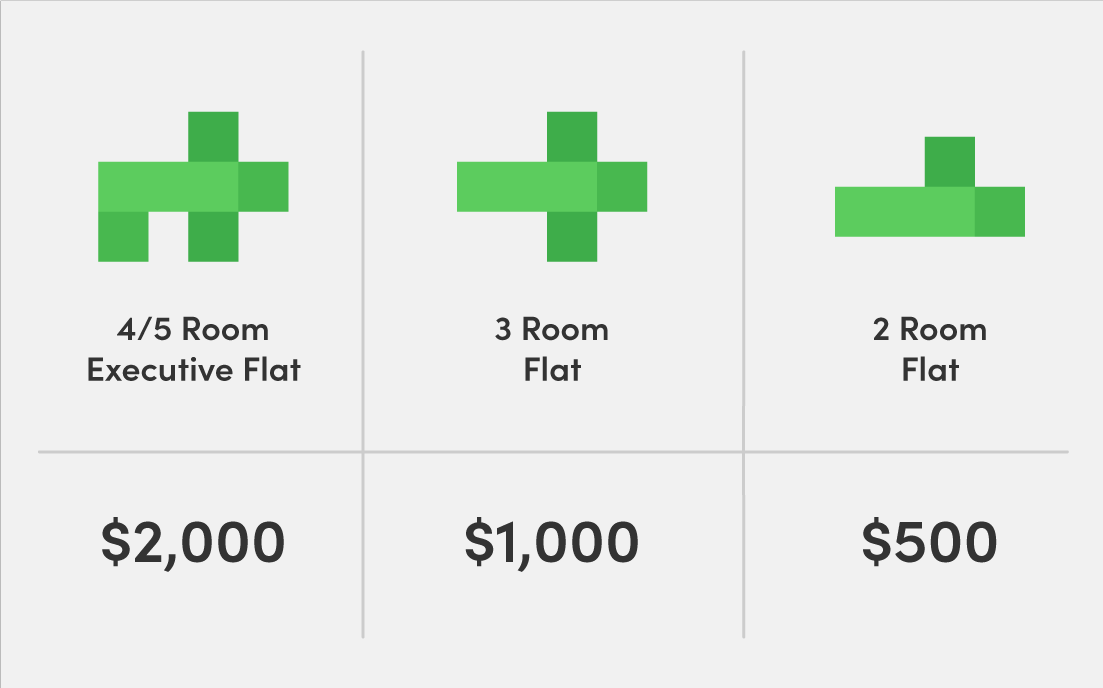

Once you’ve selected your unit, start the purchase process by paying the option fee on the spot. By securing the Option to Purchase (OTP), you get the right to purchase your flat.

The amount which you have to pay depends on your flat type. Note that payment can only be made via NETS.

- $500 for 2-room flexi flats

- $1,000 for 3-room flats

- $2,000 for 4 room or larger flats

ALSO READ: HDB Grants Guide: What’s the Max CPF Housing Grant You Can Get?

8. Sign BTO lease agreement, pay downpayment

In the past, you’d have to make a trip back to HDB Hub to sign the lease agreement within 4 months of booking a flat. But now, the wait between flat booking and signing the lease agreement can be up to 9 months.

Make sure you’ve gotten your HDB loan or bank loan arrangements in order by that time.

On the day you sign the lease agreement, you’ll have to fork out the downpayment, as well as stamp duties and legal fees.

Downpayment at the signing of Agreement for Lease

You must make a portion of your downpayment on the day you sign the lease at HDB Hub. You'll pay the rest of your downpayment during key collection.

How much your downpayment at the signing of your lease agreement will be depends on whether you’re taking out an HDB or a bank loan.

- Buyers taking out HDB loan or no loan—10% of the purchase price (Cash and/or CPF).

- Or 5% under the Staggered Downpayment Scheme (we'll elaborate below)

- Or 2.5% under deferred income assessment for students and NSFs (we'll also elaborate below)

- Buyers taking out bank loan—20% (minimum 5% in cash, remaining 15% using CPF savings and/or cash)

For those taking out a bank loan, the above scenario is based on a Loan To Value (LTV) limit of 75%. The LTV determines how much you are able to borrow from the bank in order to finance your home purchase.

Legal fees and stamp duties

Your legal fees and stamp duty can be paid using a mixture of cash and CPF. The stamp duty rates are as follows:

- First $180,000: 1%

- Next $180,000: 2%

- Next $640,000: 3%

- Next $500,000: 4%

- Next $1,500,000: 5%

- Remaining amount: 6%

Use our handy stamp duty calculator to figure out how much you'll need to pay.

Staggered Downpayment Scheme

If you’re a couple applying for a BTO for the first time before the younger applicant’s 30th birthday or an existing flat owner downgrading to a 3-room or smaller flat in a non-mature estate, you can apply for the Staggered Downpayment Scheme.

As the name implies, this allows you to split the downpayment into two payments:

- First payment when signing the lease agreement

- Second payment when you sign the Terms of Agreement and collect your keys

If you’re wondering how this differs from the regular downpayment scheme, it lets you push a larger percentage of your downpayment to the day you collect your keys.

For those taking out a bank loan, the following is the breakdown of payment:

- Downpayment at signing of agreement for lease: 5% in cash + 5% using CPF OA savings or cash

- Payment during collection of keys: 15% using CPF OA savings or cash

However, if you’re taking out an HDB loan, the following applies:

- Downpayment at signing of agreement for lease: 5% using CPF OA savings or cash

- Payment during collection of keys: 15% using CPF OA savings or cash

Now, all you can do is wait for your BTO flat to be completed. This stage typically takes a few years—I mean, it's called "build-to-order" for a reason.

Staggered Downpayment Scheme (for young couples)

If you and your boo are NSFs or fresh graduates, you're eligible for deferred income assessment. That means your initial downpayment at the lease agreement signing stage is even lower:

- Downpayment at signing of agreement for lease: 2.5% using CPF OA savings or cash

- Payment during collection of keys: 17.5% using CPF OA savings or cash

That gives you guys more time to pool your savings and get together enough moolah for the remaining 17.5% you need to fork out during key collection. Read more about HDB housing schemes to help young couples.

Deferred Downpayment Scheme (for seniors)

The DDS is for seniors aged 55 years and above who are downsizing their flats. They should still own their existing flat at the time of application and have booked an uncompleted 3-room or smaller flat in an HDB sales exercise.

Buyers who successfully apply for the DDS will only have to pay stamp duty and legal fees when they sign the Agreement for Lease. They only need to pay the purchase price of the flat upon collection of the keys.

9. BTO key collection day!

At some point, HDB will notify you to say that you can pick up the keys to your unit. Hooray!

Payment during the collection of keys

The day you collect your keys, years later, you’ll have to pay the following:

- Buyers taking out HDB loan or no loan: 15% (CPF savings or cash)

- Buyers taking out bank loan: 5% (CPF savings or cash)

For those taking out a bank loan, the following example is based on an LTV limit of 75%.

Selling your old flat and buying a new one

If you already own an existing HDB flat, you must dispose of it within 6 months from your BTO flat completion. To help you out, HDB lets you take out a Contra Payment Facility that will enable you to save a bit of money while coordinating the sale of your first flat and the purchase of the new one.

If you do not intend to take out a loan, you can opt for the Temporary Loan Scheme which will enable you to use the nett proceeds from the sale of your existing flat to pay for your new flat without having to take out a housing loan.

As a second-time flat buyer, you’ll need to pay a resale levy when you sell your existing flat to buy a new one. The resale levy will be automatically deducted by the HDB from your sale proceeds. If there is any shortfall, this must be settled in cash.

Other things to pay upon key collection

When you collect the keys, you’ll also be charged the following:

- Survey fees—You will need to pay $164 to $409, depending on flat type, for a surveyor to inspect the condition and value of your flat. This can be paid using CPF savings if you wish.

Flat Type | Survey Fee (inclusive of GST) |

|---|---|

2-room Flexi/ Community Care Apartment | $163.50 |

3-room | $231.60 |

4-room | $299.75 |

5-room | $354.25 |

Executive | $408.75 |

- Registration fees—You will have to pay a $38.30 registration fee if you are using HDB’s lawyers.

- Stamp duty for Deed of Assignment—This must be paid for anyone taking out a housing loan, and costs 0.40% of the loan amount up to a maximum of $500.

- Home Protection Scheme (HPS)—This mortgage-reducing insurance offered by the CPF Board is compulsory for those using CPF savings to repay their home loan. Premiums are to be paid using CPF savings and/or cash. Use HDB's HPS calculator to find out how much you'd need to pay per year.

- Fire Insurance—Fire insurance is compulsory for those taking out HDB loan. You must produce your Certificate of Insurance from HDB's appointed insurer, Etiqa, on the day you collect your keys. The premiums range from $1.11 for coverage of $37,900 for a 1-room Community Care Apartment to $6.68 for coverage of $176,700 for an Executive or Multi-Generation flat.

Flat type | Fire insurance premium for 5-year term (includes GST) | Sum insured |

1-Room/Community Care Apartment | $1.11 | $37,900 |

2-Room/2-Room Flexi/ Studio Apartment | $1.99 | $57,000 |

3-Room | $3.27 | $83,300 |

4-Room/S1 | $4.59 | $117,000 |

5-Room/S2/3Gen | $5.43 | $144,800 |

Executive/Multi-Generation | $6.68 | $176,700 |

10. What happens if you can’t sign the Agreement of Lease or collect your keys personally?

You can sign an HDB Power of Attorney (POA) appointing another person to act on your behalf in specified matters.

For instance, you might appoint someone to help you sign certain documents such as the Agreement to Lease. This might be necessary if you are not in Singapore on certain dates.

You need to submit all your POA documents to HDB at least 2 weeks before your appointment, so plan ahead. There's also a good 8 documents (including photocopies) to submit, so get prepared early—read more about the POA on HDB's website.

Found this article useful? Share this with fellow homeowners-to-be!

Related Articles