It’s 2025, and I still get people giving me a blank expression when I mention that I recently got a flat through the SBF exercise.

I get it. BTOs are more commonly sought after, but I think it’s important to note that that’s not your only option when you’re looking to get a flat of your own.

The SOP for buying an HDB BTO flat has definitely been well-documented. Buying a flat via HDB’s Sale of Balance Flats (HDB SBF) or the new open booking system is a little less talked about.

Here’s a quick summary:

- HDB SBF: The flats here are unsold units from previous BTO launches. These launches typically happen twice a year and in February 2025, we had the largest SBF exercise to date with over 5,590 SBF units offered.

- HDB Open Booking of Flats: This is where any remaining unsold units after SBF will be available. These units can open for booking any time during the year.

In this article, you’ll discover everything you need to know about SBF flats and Open Booking options. We’ll guide you through the application process, including how to navigate the application portal and what loan procedures you’ll probably end up encountering.

Plus, I’ll also throw in a couple of tips (including a little bit about my own experience with certain things) on how to prepare for this important step in securing your new flat. Sounds like a lot, but fret not—I’m here to help.

A Guide to HDB Sale of Balance Flats (SBF) and Open Booking of Flats (2024)

- What is a Sale of Balance (SBF) flat?

- Sale of Balance Flat (SBF) vs Built to Order (BTO)

- How and when can I view SBF flats?

- How do I apply for Sale of Balance (SBF) flats?

- How do I apply for HDB Open Booking flats?

- I don't have enough money for my BTO or SBF

- HDB Loan or Bank Loan?

1. What is a Sale of Balance (SBF) flat?

Sale of Balance (SBF) flats are leftover or “balance” flats that weren't sold during previous BTO sales launches, repurchased flats, and more.

In the past, SBF exercises were held multiple times a year. However, the government has recently reduced them to just once a year to consolidate the limited supply of SBF flats. This change aims to offer a larger selection during each launch, increasing applicants' chances of securing a flat.

Just take a look at the recent launchfor an idea of the number of units and flat mix. The Feb 2025 exercise saw the largest ever SBF exercise with over 5,590 balance flats available, of which around a whopping 40% were already completed.

The main advantage of buying an SBF flat is the chance to jump the BTO queue. After all, the standard HDB BTO route does have some factors to it that people might not find ideal.

Some feel BTO projects offer limited location choices, while others find the long wait—sometimes up to 6-7 years—frustrating. To be clear, I’m not against getting a BTO, but it’s worth highlighting the advantages of choosing an SBF flat instead.

On that note, here are some of the pluses and minuses when you go the SBF route:

Advantages | Disadvantages |

More locations to choose from | Slim chancesBecause the supply is much smaller than HDB BTOs, the chances of a successful application can be slim. |

Shorter wait | Lesser choice for unit selection |

Easier to gauge chances | Might be pricier |

Fortunately, each SBF launch is about a week long, so you and your partner/family can take your time (sorta) to carefully review the information available and make an informed decision on which route to go.

Remember—you aren’t allowed to apply for both BTO or SBF options during the same round of applications.

2. Sale of Balance Flats (SBF) vs Open Booking of Flats

So, HDB Sale of Balance Flats (SBF), as we discussed briefly, comprises flats left over from previous HDB BTO launches. These either did not get selected by the BTO ballot winners, or were selected but later given up (e.g. if the applicants decided to break up or go for condo).

So, what if there are any leftover, leftover flats? Well, they'll be offered under HDB's Open Booking of Flats.

Here are the differences:

| HDB Sales of Balance Flats | HDB Open Booking of Flats |

When it’s available | Twice a year (the first in 2024 was in Feb 2024) | All the time |

Application period | 1 week (during sales launch) | Generally open throughout the year |

What flats are available | Leftover flats from previous HDB BTO launch, repurchased flats, etc | Leftover flats from previous HDB SBF launches |

How many units | Over 1,000 (Feb 2025 exercise had 5,500) | Depends, but typically less than 100 |

Unit mix | Most unit types available | Limited unit sizes |

Locations | Mature & non-mature estates | Mature & non-mature estates, but only a few in each |

Ethnic quota | Fairly spread out among races | Very few units for Chinese buyers |

Open Booking flats are the leftovers of SBF flats—best for those who need housing quickly and aren’t picky about location. If that’s you, this option is worth considering! The biggest advantage? A much shorter wait time. If successful, you could be invited to select your flat as soon as the next working day.

From my personal experience, there are some pretty great units at HDB SBF launches. Many couples default on their super hyped $400k or $500k high floor units after realising that they can't pay up for the hefty down payments, can't get sufficient mortgage to cover their flat's price, or umm... broke up.

My fiancee and I took a shot last year, and got approved for an SBF flat in a pretty good area, up on the 9th floor—so I am essentially living proof that SBF flats aren’t undesirable leftovers from BTO launches.

3. How and when can I view SBF flats?

SBF flat exercises used to happen around twice a year (in May and November mostly). But in the last 2 years, HDB has bucked the trend by holding only 1.

Yeah, that’s right—so if you missed the SBF launch last month, I’m sorry to say you’re probably going to have to either go the BTO route with the 2 remaining launches this year or wait for next year’s SBF exercise.

Why? HDB has explained that due to the limited number of flats available in each SBF launch, consolidating them into a single annual exercise allows for a larger pool of units. This increases the chances of applicants successfully securing a flat.

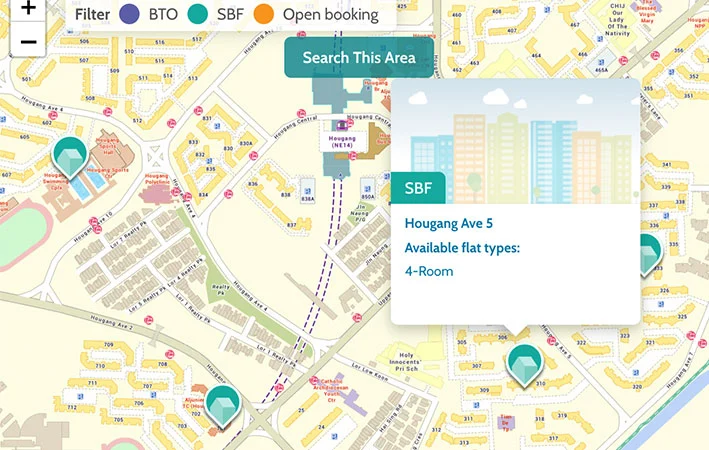

SBF applications typically open for about a week. During the SBF periods, you can view the SBF flats available by going to the HDB website, clicking onto SBF, and going to the "Finding a Flat" webpage. You will be shown a map, and individual estates' details will show up. Go to the estate you're interested in to view available units there.

Here's an example from a previous SBF exercise. If I'm looking for a SBF unit near Hougang MRT station, this is what I will see on the map:

Image: HDB

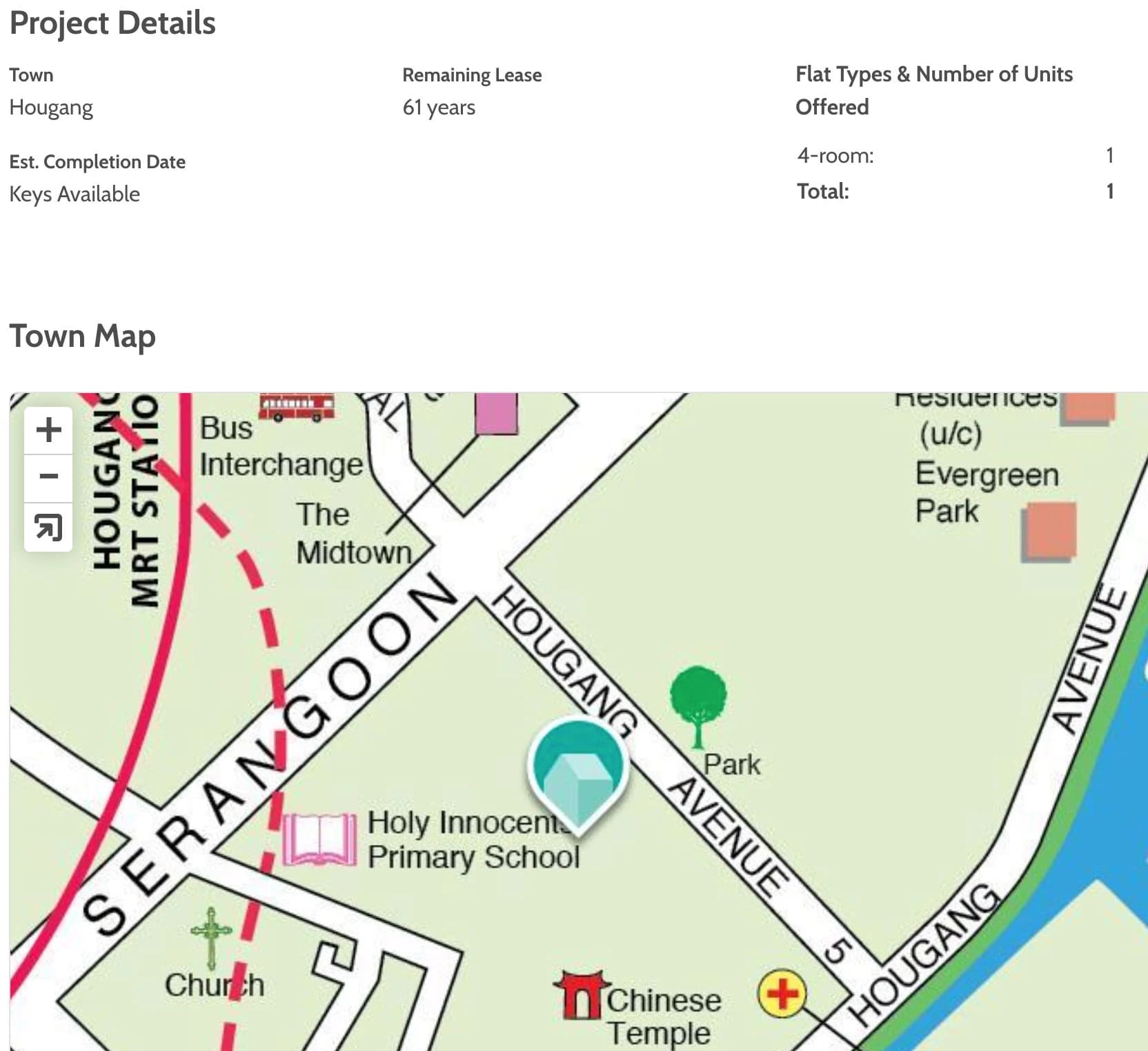

If you were to click into the SBF Hougang Ave 5 bubble, a dedicated webpage will pop-up to show you more details of the available SBF units in this estate:

Image: HDB

At this stage, you'll be able to view key details such as the estimated completion date, remaining lease duration, and the number of available units. This information can help you decide whether to apply for a 4-room or 5-room flat based on availability.

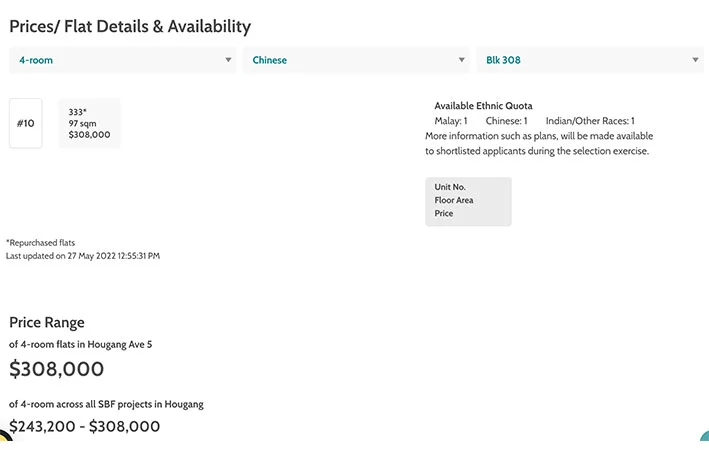

When you click on individual flats, you'll also see the Available Ethnic Quota data, which indicates the allocation of units for each ethnic group within a block. Since quotas vary across different flats, don’t be discouraged if the ratio isn’t in your favor for a particular block—check other available flats within the same project, and you might have better luck.

Image: HDB

Additionally, this is where you can find details on the unit’s square footage and total price, helping you make a more informed decision.

4. How do I apply for Sale of Balance Flats (SBF)?

We’ve talked about how the time frame for HDB SBF is the same as that of BTOs—and guess what? It turns out that the application procedure is similar as well.

Step 1: Check eligibility. The eligibility criteria, income ceiling, and housing schemes that apply to BTOs also apply to Sale of Balance Flats. For a recap of the criteria, see our step-by-step guide to applying for a BTO or HDB’s official eligibility page.

Step 2: Apply for your HDB Flat Eligibility letter (HFE). You’re not going to be able to participate in any launch if you don’t have your HDB Flat Eligibility (HFE) Letter. This requires time to process (about a month) so ensure you’ve got it ready well before any launches come up. It’s just a simple online application on the sales launch page, so just follow all instructions carefully and you should secure it with ease.

The HFE will tell you all about the different loans and grants available to you based on your financial standing. This should allow you to make a more informed decision about the flat you select when the SBF exercise opens up.

Step 3: Apply for your SBF. Well, this is the time you enter the BTO/SBF exercise portal and apply for your flat. As mentioned, you have about a week to submit your application before the window slams shut.

Step 4: Wait for results. After application closes, prepare to spend the next few weeks in an insomniac state as HDB conducts the balloting process. This is basically a lottery, but HDB has set it up in such a way that your chances are better if you are a first-time applicant, applying as a couple or family. Your chances are even greater If eligible for one of the HDB priority schemes (e.g. for living near your parents), you can improve your chances.

Personally, my partner and I actually used the Married Child Personal (MCPS) scheme because lucky for us, the project we wanted was within 4km of her parent’s flat.

Step 4: Hear from HDB. At the end of about 3 weeks, you’ll get a letter from HDB with your ballot queue number. If it’s something ridiculous like #1,735 then GG, better luck next time. But if your queue number is reasonably small, you get an appointment with HDB for the event of the year: Your SBF flat selection. *pops champagne*

For example, the flat my fiancee and I applied for had a total of 13 units available. And guess the number of people that applied for it? 180. Yeap, so we were incredibly lucky to get a ballot number of 11, which was within the number of available units which meant we were definitely going to secure at least one available unit.

Don’t be discouraged if you get a ballot number that exceeds the number of units available by a little. It is a common situation where people who have ballot numbers before you choose not to opt for a flat which moves you up the queue. So keep checking (and praying). On the flip side, if you do get a ballot number and choose to not choose a flat in that exercise, do note that you’ll lose your first timer status the next time you apply—which lowers your chances of securing a flat by a fair bit.

Step 5: Go to HDB and book your flat. At HDB Hub, you’ll be shown what’s available to you, and, if you like what you see, you can book it on the spot (must pay an option fee of $500, $1,000 or $2,000, depending on the size of your flat). Once you have your finances in order, you can come back and sign the official lease agreement and make the downpayment of 20% (HDB loan) or 25% (bank loan) of the flat price.

Step 6:Key collection. Assuming all goes well, the next time you’ll hear from HDB is when your key is ready. Hurray! Depending on how far along your flat is in the construction process, key collection day can be as early as within 3 months (if it’s already complete) to 2+ years (if it’s a previously-unsold BTO).

5. How do I apply for HDB Open Booking flats?

HDB Open Booking was designed to be available all year round, so there isno need to wait till HDB launches a BTO to apply for one or go through the whole balloting process. To be alerted of any open booking flats, you can sign up for the HDB eAlert Service.

It was meant to be first come, first served. You could do it anytime, provided you can find one that you qualify for and suits you.

If you qualify, you’ll be very pleased to know that the HDB open booking is short and simple.

Step 1: Check your eligibility. As with all flats bought directly from HDB, you need to meet certain age/family/income requirements, so check your eligibility here before applying.

Step 2: Settle your loan. At the same time, you should also obtain an HDB Flat Eligibility (HFE) letter and Approval in Principal letter from your bank. Things can move at lightning speed with open booking, so you should prepare all the necessary information before applying.

Step 3: Apply for your flat. No need to wait around for an auspicious date, because balance units are first come, first served. This means that if you see anything you like and have fulfilled all the eligibility requirements, you should apply online immediately. The usual $10 admin fee applies.

Step 4: Get an appointment with HDB. Immediately after application, you’ll receive a queue number and an appointment to book your flat. This can be as early as the same day of your application (if you book before noon on a weekday—otherwise, it’s the next working day). So it’s best to clear your schedule on application day!

Step 5: Book your flat. During your appointment with HDB, you can go ahead and book the flat by paying a $500, $1,000 or $2,000 option fee (depending on flat size).

Step 6: Sign lease agreement. The next HDB appointment is to sign the official agreement. You will want to make sure you have enough cash/CPF on this day, because it’s also when you’ll be making the downpayment (20% or 25% of your flat), plus legal and stamp fees (1% to 3% of the flat).

Step 7: Key collection. If the flat you booked is already complete, you can collect your keys on the same day as signing the lease agreement. Otherwise, you will need to wait till the block is constructed and then collect your key.

6. I don't have enough money for my BTO or SBF.

With an HDB BTO, you have what seems like all the time in the world to save up for your downpayment and sort out your finances.

But due to the chop-chop nature of HDB SBF, some applicants may run into cashflow issues. To help with that, HDB has a few concessions.

Deferment of income assessment

If you and your partner are fresh out of school or NS (within 12 months), you can defer your income assessment until 3 months before key collection for an uncompleted flat or at the time of flat booking for a completed one. HDB will notify you to submit your income documents then. You may also be eligible for a 2.5% initial downpayment—read more about what help young couples can get from HDB when buying their first home.

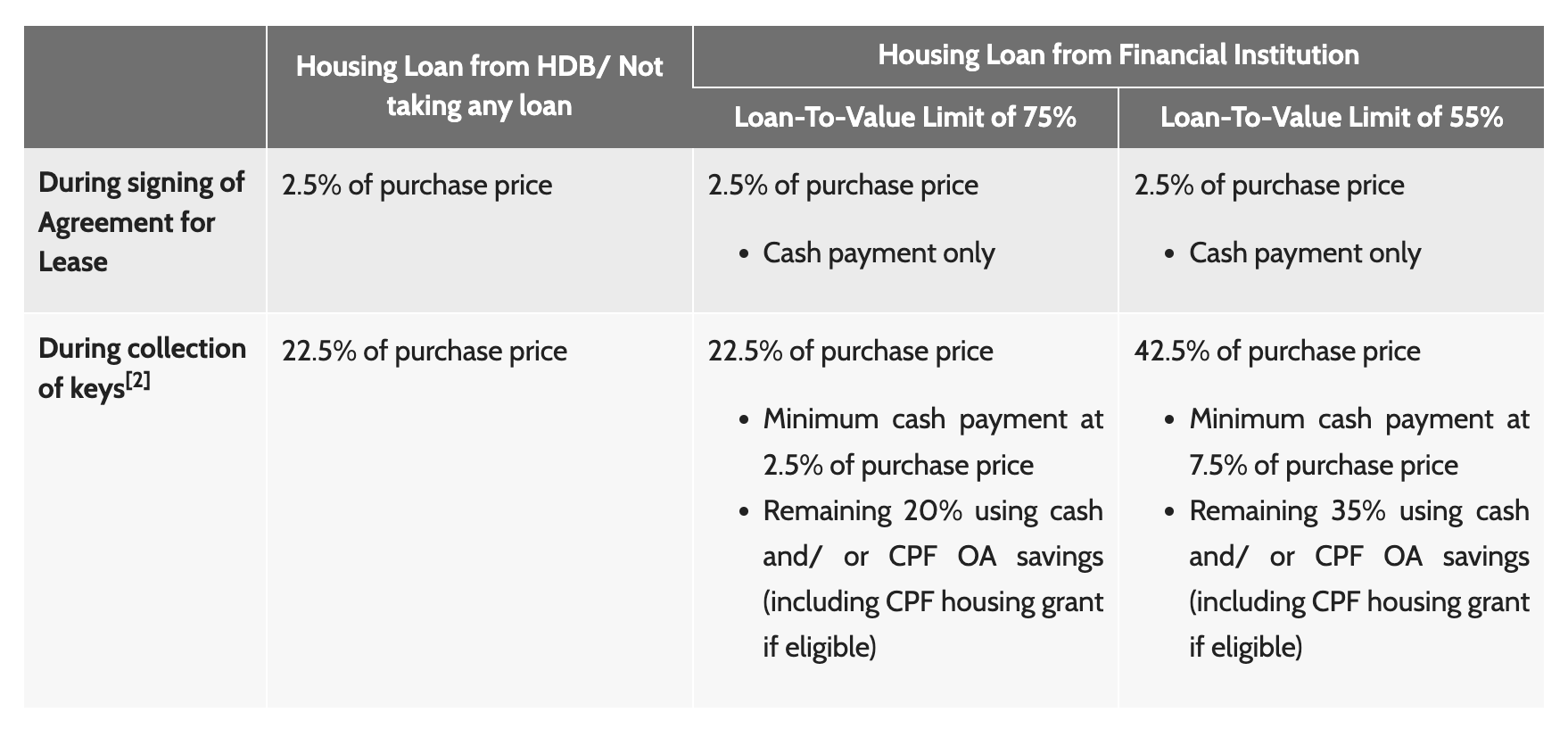

Staggered Downpayment Scheme

First-timer couple applicants under 30 years old, or current homeowners looking to downsize to a smaller flat, can request for the downpayment to be paid in 2 parts. Assuming you go for an HDB loan, this means you only need to pay 2.5% when you sign the lease agreement, and the other 22.5% at key collection.

Image: HDB

Deferred Downpayment Scheme

For elderly (age 55 and up) homeowners looking to downsize their current flat to a new, smaller home (3-room or smaller), your downpayment due date will be automatically extended until the key collection date. When signing the lease agreement, you will only need to pay the stamp duty and legal fees (1% to 3% of flat).

These are the eligibility requirements to qualify:

- Aged 55 and above at the time of their HFE letter application.

- Have not sold or completed the sale of their existing flat at the time of their HFE letter application.

- Have booked an uncompleted 3-room or smaller flat in any HDB sales exercise.

Temporary Loan Scheme (TLS)

If you’re in the midst of selling your current flat and want to use the proceeds to pay for your new flat, this scheme allows you to get a short-term loan from HDB to help with the cashflow while you wait for the sale proceeds to come in.

To qualify, you must have:

- Booked a flat and received an invitation to collect the keys.

- Applied to sell your existing flat.

- Fully redeemed your housing loan for your existing flat if the loan was provided by a financial institution (FI).

Do note that you’ll also need to be:

Able to pay the full purchase price of the flat using:

- CPF Ordinary Account balance.

- CPF refund and cash proceeds from the sale of your existing flat.

If funds are insufficient, you must top up the shortfall by the deadline set by HDB before they consider your request for the TLS. You may request for the TLS when you apply to sell your existing flat.

7. HDB Loan or Bank Loan for my BTO or SBF?

No matter how long you put off financing your HDB flat, you'll have to deal with the painful money bit of buying your flat at some point.

Like every other home buyer, you'll need to decide on who you get your home loan from—HDB or a bank.

Requiring no cash downpayment, the HDB loan is the default choice for many new homeowners. However, if you have enough cash for the downpayment, bank loans typically have lower interest rates. Typically! You should always compare the current bank loan interest rates with the HDB loan interest rate.

Currently, HDB loan interest rates (2.60% p.a.) are generally lower than other home loan interest rates. Banks don't readily publish these rates online though, so you might want to get a home loan quote from MoneySmart. We'll do the hard work for you!

Know someone applying for a flat? Share this article with them!

Related Articles