If you think that fixed deposits are only for conservative cash-rich aunties and uncles, think again.

A fixed deposit (also known as a time deposit) account is a type of bank account that pays account holders a fixed amount of interest in exchange for depositing a certain sum of money for a certain period of time.

Although fixed deposit rates have been falling, there's a good number of rates that are still very decent and worth giving a shot if you have some money lying around. You don’t even need a large stash of cash—these days, banks are offering fixed deposits starting from as low as $500!

Here’s our round-up of the best fixed deposit rates in Singapore in July 2026 for banks like UOB, DBS, OCBC, and more.

[ms-toc title="Summary: Best fixed deposit rates in Singapore" headings="h2,h3"]

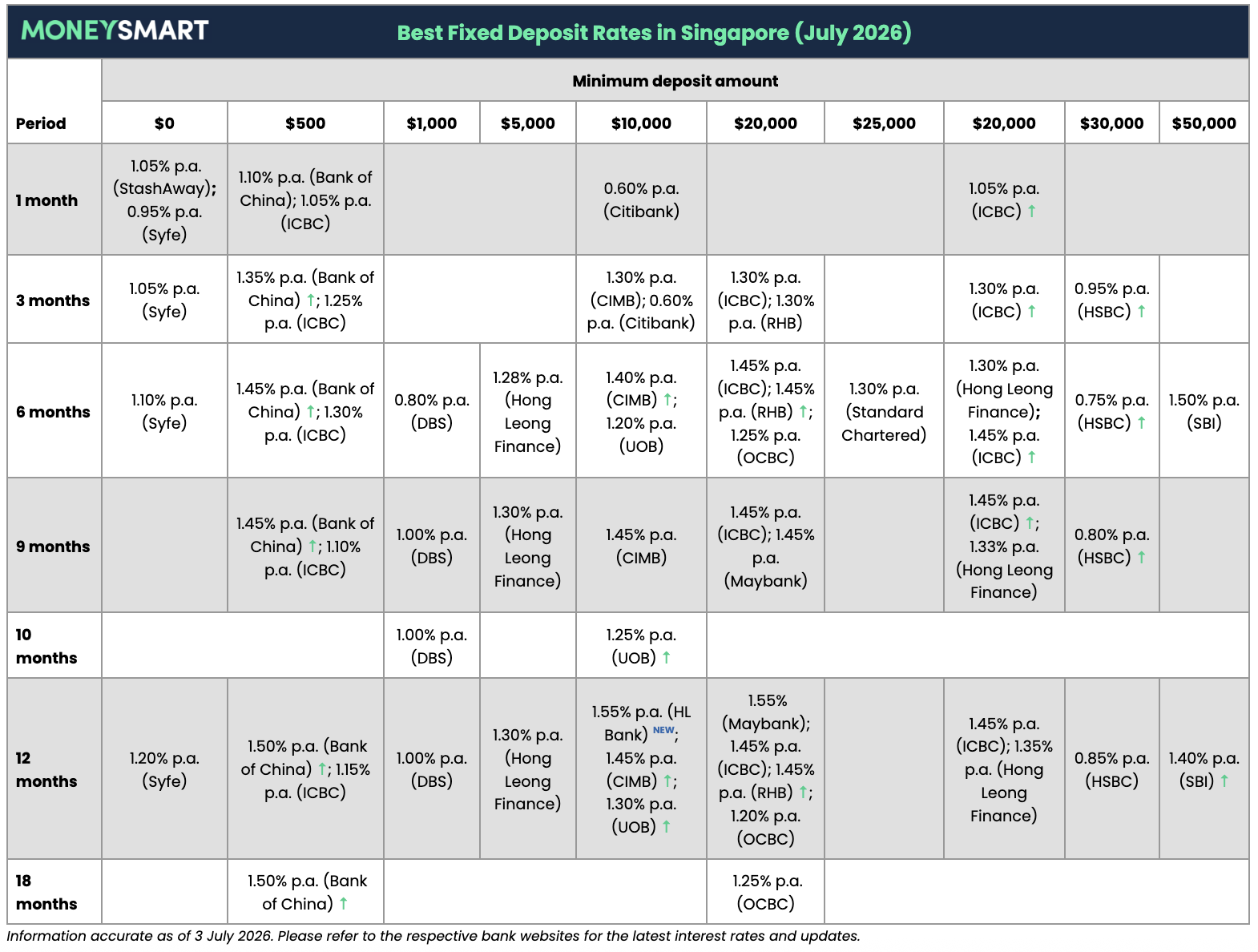

Overview of Singapore fixed deposit rates (July 2026)

Which bank in Singapore has the best fixed deposit rate? These are the best fixed deposit rates in Singapore this month for various deposit amounts and commitment periods.

Overall highest fixed deposit rates in Singapore (July 2026)

Looking for the absolute highest fixed deposit rates across all deposit amounts and commitment periods? If your deposit amount and period are flexible, these are the best fixed deposit rates you can get in Singapore this month:

- HL Bank (1.55% p.a.—$10,000 for 12 months)

- Maybank (1.55% p.a.—min. $20,000 for 6 months)

- Bank of China (1.50% p.a.—min. $500 for 12, 18, and 24 months)

- State Bank of India (1.50% p.a.—min. $50,000 for 6 months)

- CIMB (1.45% p.a.—min. $10,000 for 9 or 12 months)

- Hong Leong Finance (1.45% p.a.—min. $10,000 for 5 or 6 months)

- ICBC (1.45% p.a.—$20,000 for 6, 9 or 12 months)

- RHB (1.45% p.a.—min. $20,000 for 6 or 12 months)

- Standard Chartered (1.30% p.a.—min. $25,000 for 6 months)

- UOB (1.30% p.a.—min. $10,000 for 12 months)

- OCBC (1.25% p.a.—min. $20,000 for 6 or 18 months)

- Syfe (1.20% p.a.—12 months with no minimum amount)

- StashAway Simple Fixed (1.05% p.a.—1 month with no minimum amount)

- DBS (1.00% p.a.—min. $1,000 for 9, 10, or 12 months)

- HSBC (0.95% p.a.—min. $30,000 for 3 months)

- Citibank (0.70% p.a.—$10,000 for 12 months)

To view fixed deposit rates by commitment period or deposit amount, navigate our summary to jump to the section that best matches your needs.

ALSO READ: Fixed Deposit Alternatives in Singapore—5 Easy, Low-Risk Investments

Fixed deposit rates by commitment period

When it comes to fixed deposits, do you have a time frame in mind? Whether you want to stash your cash for 3, 6 or 12 months, we’ve worked out the best fixed deposit rates for you.

Best fixed deposit rates for a 3-month commitment periods or shorter

Looking for a short fixed deposit period? Here are the best fixed deposit rates in Singapore for a 3-month commitment period.

- Bank of China (1.35% p.a.—min. $500 for 3 months)

- RHB (1.30% p.a.—min. $20,000 for 3 months)

- ICBC (1.30% p.a.—$20,000 for 3 months)

- CIMB (1.30% p.a.—min. $10,000 for 3 months)

- Syfe (1.05% p.a.—3 months with no minimum amount)

- StashAway Simple Fixed (1.05% p.a.—1 month with no minimum amount)

Syfe Cash+ Guaranteed

Period | Syfe Cash+ Guaranteed rate (no min. or max deposit amount) |

1 month | 0.95% p.a. |

3 months | 1.05% p.a. |

6 months | 1.10% p.a. |

12 months | 1.20% p.a. |

Rates accurate as of 3 July 2026. Do check the Syfe Cash+ Guaranteed page for the latest rates.

If you're looking for a fuss-free, guaranteed way to grow your money, you might want to look beyond our traditional banks.

Syfe Cash+ Guaranteed isn't technically a fixed deposit, but invests your funds into fixed deposits by with banks that are regulated by MAS. Their rates are generally higher than traditional banks, and there's also no minimum or maximum amount.

At the time of writing, Syfe Cash+ Guaranteed is offering up to 1.20% p.a. with a 12-month tenure. That's a slight increase of 0.05% p.a. from the month before.

MoneySmart Take

- What we like: Higher rates than traditional banks, no minimum or maximum deposit amount.

- What we don't like: No liquidity. You cannot withdraw the funds prematurely even if you're willing to pay a penalty. With traditional banks, you can prematurely withdraw your fixed deposit funds by paying an early withdrawal fee.

StashAway Simple Fixed rate (formerly Simple Guaranteed)

Period | StashAway Simple Fixed rate (no min. or max. deposit amount) |

1 month | 1.05% p.a. |

Rates accurate as of 3 July 2026. Do check StashAway's Simple Fixed page for the latest rates.

StashAway offers a cash management solution called Simple Fixed, which evolved from Simple Guaranteed. Like its predecessor, the advertised rate is guaranteed. StashAway Simple Fix invests your money in money market funds managed by licensed financial institutions. While the return on these does have minor fluctuations, StashAway will top up the difference if the returns fall short of the rate they promised you.

At the time of writing, the StashAway Simple Fixed interest is 1.05% p.a. for a 1-month period, with no minimum or maximum deposit amounts.

MoneySmart Take

- What we like: Relatively high rates compared to traditional fixed deposits. Plus, no minimum or maximum deposit amount.

- What we don't like: Like Syfe's Cash+ Guaranteed, there's no way for you to withdraw your funds early, penalty fee or not. Once locked in, your cash is locked in tight.

ICBC fixed deposit rates

Deposit amount | |||

Period | $20,000 to <$200,000 (over the counter) | $500 to <$200,000 (via e-banking) | $20,000 to <$200,000 (via e-banking) |

1 month | 1.05% p.a. | 1.05% p.a. | 1.10% p.a. |

3 months | 1.25% p.a. | 1.25% p.a. | 1.30% p.a. |

6 months | 1.40% p.a. | 1.30% p.a. | 1.45% p.a. |

9 months | 1.40% p.a. | 1.10% p.a. | 1.45% p.a. |

12 months | 1.40% p.a. | 1.15% p.a. | 1.45% p.a. |

Rates accurate as of 3 July 2026. The rates above are promotional rates subject to change at any time by ICBC. Do check ICBC’s website for the latest rates.

There are a few fixed deposits which have pretty low barriers to entry on this list, but Chinese bank ICBC takes the cake. If you set up your fixed deposit via e-banking, their minimum deposit is just $500—nope, we didn’t miss a zero there!

Even if you only have $500 to invest, you can still get a rate of 1.30% p.a. with a commitment period of 6 months. You have to do this via e-banking to get this rate.

If you've got at least $20,000 to spare, you're looking at higher rates: up to 1.45% p.a. with a tenure of 6, 9 or 12 months. You can also get 1.30% p.a. with $20,000 for a commitment period of 3 months.

Beyond interest rates, there is another plus point for ICBC's fixed deposit—there's no penalty for early withdrawal. That means your fixed deposit isn't as fixed as you might think.

MoneySmart Take

- What we like: Ultra low minimum deposit amount of just $500 via e-banking and a low commitment period of anywhere between a month to a year, making ICBC very accessible. ICBC also doesn't penalise you for early withdrawals.

- What we don't like: Rates are only slightly above average. And for older folk who want to open a fixed deposit account in person, their minimum deposit amount shoots up to $20,000 while the fixed deposit rates drop slightly.

Citibank fixed deposit rates

Tenure | Interest rate (p.a.) for deposits $10,000 to $3,000,000 (Board rates) |

|---|---|

1 week | 0.20% |

2 weeks | 0.20% |

1 month | 0.60% |

2 months | 0.60% |

3 months | 0.60% |

6 months | 0.60% |

12 months | 0.70% |

24 months | 0.10% |

36 months | 0.10% |

The best Citibank fixed deposit board rate you can currently get is 0.70% p.a. for a minimum deposit amount of $10,000 and a commitment period of 3 months.

If you are a Citigold or Citigold Private Client customer, you can enjoy the following fixed deposit promotions from Citibank:

Tier | Customer type | 3 months (p.a.) | 6 months (p.a.) |

Citigold | Eligible customer | 1.35% | 1.40% |

Citigold | Eligible Accredited Investor (AI) customer | 1.40% | 1.45% |

Citigold Private Client | Eligible customer | 1.45% | 1.50% |

Citigold Private Client | Eligible Accredited Investor (AI) Customer | 1.50% | 1.55% |

Citigold Private Client | Eligible customer with AUM ≥ S$6,500,000* | 1.60% | 1.60% |

All tiers above apply to New Funds Deposit Amount of $10,000 to < $10,000,000. View Citigold Time Deposit Promotion Terms and Conditions and Citigold Private Client Time Deposit Promotion Terms and Conditions for full eligibility conditions.

Note: The rates above are accurate as of 3 July 2026. Do check Citibank's fixed deposit promotion page for the latest rates in the event Citibank makes changes.

If you're new to Citibank and have at least $350,000 you're looking to place in a fixed deposit, you can enjoy up to 1.30% p.a. over a 3-month tenure. Have even more cash to stash? New Citibank customers with $1.5 million can unlock the highest rate of 1.50% p.a. with a 3-month tenure.

New funds deposit amount (for new-to-bank customers) | 3 months (p.a.) | 6 months (p.a.) |

$350,000 to < $1,500,000 | 1.45% | 1.40% |

$1,500,000 to $5,000,000 | 1.65% | 1.60% |

Note: The rates above are accurate as of 3 July 2026. Do check Citibank's fixed deposit promotion page for the latest rates; Citibank may make changes at any time at their discretion.

- Base Interest Rate p.a.

- 0.01%

- Max. Interest Rate p.a.

- 7.51%

- Total Relationship Balance

- S$350,000

Get S$1,500 Cash or 19,050 SmartPoints (enough to redeem an Apple iPhone 17 Pro Max)

- Sign up as an Accredited Investor

- Deposit S$500,000 AUM in fresh funds within 3 calendar months

OR

- Sign up as an Non-Accredited Investor

- Deposit S$500,000 AUM in fresh funds within 3 calendar months

- Make a new qualified investment of min. S$100,000 within 3 calendar months

Get S$1,200 Cash or 15,970 SmartPoints (enough to redeem an Apple 13-inch MacBook Air)

- Sign up as an Accredited Investor

- Deposit S$350,000 AUM in fresh funds within 3 calendar months

Get S$900 Cash

- Sign up as an Non-Accredited Investor

- Deposit S$350,000 AUM in fresh funds within 3 calendar months

PLUS get an additional S$200 Cash Bonus on top of your gifts if you fund the fresh funds within 2 months! T&Cs apply.

MoneySmart Take

- What we like: Short commitment period of just 3 months. For those with a lot of money to park in a fixed deposit account, there's also a high upper limit of $3 million.

- What we don't like: High minimum deposit amount. Not everyone has $50,000 just lying around.

HSBC fixed deposit rates

Deposit period | Personal Banking customers | Premier customers without wealth holdings | Premier customers with wealth holdings or Premier FX Engaged customers | Premier Elite customers |

3 month | 0.95% p.a. | 1.00% p.a. | 1.25% p.a. | 1.30% p.a. |

6 months | 0.75% p.a. | 0.80% p.a. | 1.10% p.a. | 1.15% p.a. |

9 months | 0.80% p.a. | 0.85% p.a. | 1.15% p.a. | 1.20% p.a. |

12 months | 0.85% p.a. | 0.90% p.a. | 1.20% p.a. | 1.25% p.a. |

Promotional rates valid until 31 July 2026. Do check HSBC’s website for the latest rates.

HSBC is offering anything from 0.75% to 1.30% p.a., depending on your banking relationship with them. For the bulk of us who are regular banking customers, the highest fixed deposit rate you can get with HSBC this month is just 0.95% p.a.

The best case scenario is if you are a Premier Elite customer with HSBC. If you fit the bill, HSBC will give you 1.30% p.a. for a deposit period of 3 months.

No matter your banking relationship with HSBC, the minimum sum you have to put in is $30,000.

MoneySmart Take

- What we like: Short commitment period of just 1 or 3 months available.

- What we don't like: High minimum sum. You're going to need at least $30,000 to place a fixed deposit with HSBC.

Bank of China fixed deposit rates

Period | Fixed deposit interest rates (mobile banking, minimum $500 unless otherwise stated) |

1 month | 1.10% p.a. |

3 months | 1.35% p.a. |

6 months | 1.45% p.a. |

9 months | 1.45% p.a. |

12 months | 1.50% p.a. |

18 months | 1.50% p.a. |

24 months | 1.50% p.a. |

The rates above were set on 29 Jun 2026 and are valid till 5 July 2026. Check the Bank of China website for the latest rates.

The best part about the Bank of China’s fixed deposit rates is the low minimum deposit and tenor period. They are currently offering 1.50% p.a. for a placement of $500 for a period of 12, 18 or 24 months—these are longer tenors, but a relatively accessible minimum deposit amount.

Do note that you need to make your deposits via mobile banking to enjoy the rates above.

MoneySmart Take

- What we like: Short commitment period of 3 months available, and very low minimum deposit amount of $500.

- What we don't like: The highest rates are unlocked only with long commitment periods, which may not be feasible for those who need their funds in a shorter time frame.

Best fixed deposit rates for a 6-month and 12-month commitment periods

Looking to stash your cash in a fixed deposit account for 6 months or 1 year? Here’s a summary of the best fixed deposit rates in Singapore in 2026 for 6-month and 12-month commitment periods:

Best fixed deposit rates in Singapore for 6 and 12 months (July 2026) | ||

Min. deposit amount | 6 months | 12 months |

No minimum | 1.05% p.a. (Syfe) | 1.20% p.a. (Syfe) |

$500 | 1.45% p.a. (Bank of China); 1.30% p.a (ICBC) | 1.15% p.a. (ICBC); 1.50% p.a. (Bank of China) |

$1,000 | 0.80% p.a (DBS) | 1.00% p.a (DBS) |

$10,000 | 1.45% p.a. (Hong Leong Finance); 1.40–1.45% p.a. (CIMB); 1.20% p.a. (UOB) | 1.45–1.50% p.a. (CIMB); 1.30% p.a. (UOB) |

$20,000 | 1.30% p.a. (Maybank); 1.45–1.55% p.a. (RHB); 1.25% p.a. (OCBC) | 1.30% p.a. (Maybank); 1.20% p.a. (OCBC); 1.45–1.55% p.a. (RHB) |

$25,000 | 1.30%–1.60% p.a. (Standard Chartered) | – |

$50,000 | 1.50% p.a. (State Bank of India) | 1.40% p.a. (State Bank of India) |

CIMB fixed deposit rates

Deposit amount: $10,000 and above | ||

Period | Personal Banking (For regular CIMB customers) | Preferred Banking |

3 months | 1.30% p.a. | 1.35% p.a. |

6 months | 1.40% p.a. | 1.45% p.a. |

9 months | 1.45% p.a. | 1.50% p.a. |

12 months | 1.45% p.a. | 1.50% p.a. |

Promotional rates valid from 1 July 2026, subject to change anytime by CIMB. Do check CIMB’s website for the latest rates.

Malaysian bank CIMB is offering relatively good fixed deposit rates in Singapore this month, at up to 1.45% p.a. for regular CIMB customers and 1.50% p.a. if you're a CIMB Preferred Banking customer. These aren't high in absolute terms, but they are some of the highest this month compared to rates offered by other banks.

This promo is for deposits of at least $10,000. To enjoy the highest rates, you need to lock up your money for 6 or 12 months and must apply and deposit your money online.

If you’re looking to deposit smaller amounts of your savings into a fixed deposit account, CIMB's board rates apply from deposits of $1,000 and up. However, they are a measly 0.2% to 0.3% p.a. or so. In this instance, you would be better off placing your money almost anywhere else. ICBC (1.30% p.a. with a minimum deposit of $500 for 6 months) and the Bank of China (1.50% p.a. with a minimum of $500 for 12 months) are good options for small deposit amounts and small time frames. You could also look at a less traditional fixed deposit option, Syfe Cash+ Guaranteed, for up to 1.20% p.a. (no minimum amount, 12-month period) this month.

MoneySmart Take

- What we like: Relatively short commitment periods of 3 and 6 months.

- What we don't like: CIMB's best rates are reserved for their Preferred Banking customers—these are 0.05% p.a. higher than the rates for regular Personal Banking customers. So if they advertise their rates as up to a certain rate, know that those rates may not apply to you.

RHB fixed deposit rates

Deposit amount: $20,000 and above | ||

Period | Personal banking | Premier banking |

3 months | 1.30% p.a. | 1.40% p.a. |

6 months | 1.45% p.a. | 1.55% p.a. |

12 months | 1.45% p.a. | 1.55% p.a. |

Note: The rates above are correct as of 3 July 2026. They are promotional rates subject to change at any time by RHB. Do check RHB’s website for the latest rates.

The easiest way to place your fixed deposit with RHB is on your phone via the RHB Mobile SG App. However, if that isn't possible for you, RHB's fixed deposit rates are the same whether you use mobile banking or head down to one of their branches.

The highest rate personal banking customers can get is 1.45% p.a. with a minimum deposit requirement of $20,000—pretty high right now relative to other banks. Currently, this rate applies to 2 of the 3 available tenors: 6 and 12 months. If you are a Premier Banking customer, you can get a rate of 1.55% p.a. for the same periods.

A big advantage to RHB's fixed deposit is that they don't charge you any penalty fee for early withdrawal. That means you can take your cash out early with no penalty in the event of an emergency.

MoneySmart Take

- What we like: No premature penalty fee if you want to withdraw your funds early!

- What we don't like: RHB's minimum deposit amount of $20,000 is higher than that for other banks.

HL Bank fixed deposit rates

Fixed deposit tenure | Promotional interest rate (p.a.) for fixed deposit | Savings account interest earned (p.a.) | Overall effective interest rate (EIR) |

|---|---|---|---|

12-month | 1.55% (min $10,000 per placement) | 0.10% ($1,000 earmarked for every $10,000 of fixed deposit) | 1.42% |

Rates accurate as of 3 July 2026. Do check HL Bank's latest fixed deposit rates; HL Bank may revise rates at their discretion.

A member of the Hong Leong group, HL Bank has one ongoing fixed deposit promotion at the time of writing. They're rewarding you for pairing a fixed deposit with a savings account—but it's only available via FAST transfer.

Place a minimum of $10,000 in a 12-month fixed deposit and earn a promotional rate of 1.55% p.a. At the same time, earmark $1,000 in your savings account for every $10,000 placed in the fixed deposit, and that savings amount earns 0.10% p.a. Combined, this works out to an overall effective interest rate of 1.42% p.a.

To qualify, simply make a one-time FAST transfer into your savings account with the comment "FDSA". Do note that both the fixed deposit and the earmarked savings amount cannot be withdrawn for the full 12-month tenure.

MoneySmart Take

- What we like: Low tenors available, from just 1 month. No interest charged if you make a withdrawal prematurely.

- What we don't like: If you visit a branch, high minimum deposit amount required at $100,000.

Maybank fixed deposit rates

Period | Promotional rate | Effective rate |

|---|---|---|

9 months (Branches and online) | 1.45% p.a. | 1.32% p.a. |

12 months (Branches and online) | 1.55% p.a. | 1.41% p.a. |

Note: The rates above are promotional rates subject to change at any time by Maybank. Check the Maybank fixed deposit rate page for the latest rates.

Maybank is among one of the higher fixed deposit rates this month with up to 1.55% p.a. (EIR: 1.41% p.a.) over 6 months under a fixed deposit promotion. Here's how this promotion works:

- You deposit at least $2,000 into a Maybank account (in sets of $1,000)

- For every $1,000 you deposited in step #1, you can deposit $10,000 into a Maybank fixed deposit (minimum $20,000)

- You'll get up to 1.55% p.a. on your fixed deposit.

However, since the money in the savings account will only earn 0.05% p.a., the effective interest rate you earn is actually 1.32% p.a. That's still a good rate compared to other banks this month.

If you don't want to make use of the bundle promotion, Maybank also has an option for "à la carte" fixed deposits:

Tenor | Maybank fixed deposit promotional rates |

|---|---|

6 months | 1.30% p.a. |

9 months | 1.30% p.a. |

12 months | 1.40% p.a. |

The highest rate of 1.40% p.a. is less than what you'd get with the bundle promotion, but is still decent compared to other banks this month.

MoneySmart Take

- What we like: We like that both online placements and placements in branch enjoy the same rates—those who can't access one or the other for whatever reason aren't disadvantaged. Their deposit bundle promotions also work well if you already have or intend to get a Maybank savings account.

- What we don't like: Low rates, longer commitment periods, and quite a large deposit amount relative to other banks on this list.

OCBC fixed deposit rates

Period | Deposit amount of $20,000 and above |

6 months | 1.20% p.a. (placement in branch) / 1.25% p.a. (online banking) |

12 months | 1.15% p.a. (placement in branch) / 1.20% p.a. (online banking) |

18 months | 1.20% p.a. (placement in branch) / 1.25% p.a. (online banking) |

Note: The rates above are promotional rates subject to change at any time by OCBC. See OCBC’s fixed deposit rates for the latest.

OCBC's highest fixed deposit rate this month is 1.25% p.a. for a 6- or 18-month deposit period. That's if you use internet banking. Going down to an OCBC branch to set up your fixed deposit account is going to yield an even lower rate of 1.20% p.a. Ouch.

While these rates may not appear very high, other banks have slashed their rates too. OCBC's is low, but so is everyone else's.

MoneySmart Take

- What we like: Convenient application via OCBC app.

- What we don't like: Relatively high minimum deposit amount of $30,000. OCBC also has a pretty significant disparity in its in-branch rates versus online banking rates, which makes me think older folks who only can only access banking services in person are disadvantaged.

Fixed deposit rates by minimum deposit amount

Is cash your limiting factor? Good news—the minimum amount for a fixed deposit account starts from as low as $500! Here are the best fixed deposit rates for deposits of the following amounts:

Best fixed deposit rates for deposits $10,000 and under

These are the best fixed deposit rates in Singapore 2026 for deposits $10,000 and under:

- DBS (1.00% p.a.—min. $1,000 for 8 – 60 months)

- Bank of China (1.50% p.a.—min. $500 for 12 months)

- CIMB (1.45% p.a.—min. $10,000 for 9 or 12 months)

- ICBC (1.30% p.a.—$500 for 6 months)

- UOB (1.30% p.a.—min. $10,000 for 12 months)

DBS fixed deposit rates

Deposit amount | ||

Period | $1,000 – $19,999 | $20,000 – $999,999 |

1 month | 0.05% p.a. | 0.05% p.a. |

3 months | 0.15% p.a. | |

6 months | 0.80% p.a. | |

9 months | 1.00% p.a. | |

12 months | 1.00% p.a. | |

Currently, the best DBS fixed deposit rate is 1.00% p.a. for those who put $1,000 to $19,999 into a fixed deposit for 8 to 12 months. This is low compared to other promotional fixed deposit rates this month from other banks (but still a little better than having your cash parked in a regular savings account—check out these high-yield savings account for other options).

Rates aside, one thing I have always liked about the DBS fixed deposit rates is their low minimum deposit amount of $1,000. They’re also pretty flexible with the deposit period. If you can only afford to lock in your cash for less than 12 months, DBS will let you choose any deposit period at 1-month intervals, from 1 – 12 months. Most other banks limit this to 3-month intervals.

However, if you’re looking to put $20,000 or more into a fixed deposit, the current DBS rates are a flat, unimpressive 0.05% p.a. for all lock-in periods. You’d be better off investing your money almost anywhere else.

MoneySmart Take

- What we like: Low minimum amount of just $1,000. We also like that you get so much flexibility in terms of how long you want to leave it in for—DBS offers deposit periods in 1-month intervals from 1 -12 months.

- What we don't like: DBS doesn't have very high fixed deposit rates (and rarely change them too). Their rates only become worth looking at from deposit periods of 12 months onwards, and even then are only relatively attractive if other banks drop their rates. Also, DBS is a poor option for investing larger sums. If you want to put in $20,000 or more, DBS fixed deposit rates plummet to just 0.05% p.a.

UOB fixed deposit rates

UOB fixed deposit rates (minimum deposit amount: $10,000) | |

Period | Base interest rate / Promotional interest rate for customers with Wealth Products* |

6 months | 1.20% p.a. / 1.25% p.a. |

10 months | 1.25% p.a. / 1.30% p.a. |

12 months | 1.30% p.a. / 1.35% p.a. |

Promotion valid until: 31 July 2026, subject to change by UOB. Do check UOB's website for the latest rates.

*Eligible Wealth products include: Unit Trusts, Maxi Yield, Bonds, Structured Products, Regular Premium insurance and Single Premium insurance. Placements must be made via Relationship Managers or Client Advisors.

For regular UOB customers, UOB’s highest fixed deposit rate of 1.30% p.a. currently applies to 1 tiers—for a deposit period of 12 months. This rate applies as long as you deposit a minimum of $10,000.

If you also have wealth products with UOB, you can unlock a higher rate of 1.35% p.a. for the same commitment period.

While for regular banking customers, the highest rate of 1.30% p.a. doesn't sound high, it is fairly average this month in relative terms. If you want higher rates, consider an option like the Bank of China (1.50% p.a. for $500 over 12 months), ICBC (1.45% p.a. for $20,000 over 6 months), or RHB (1.45% p.a. for $20,000 over 12 months).

MoneySmart Take

- What we like: Commitment periods start from a relatively short 6 months.

- What we don't like: UOB's current rate is below average. As aforementioned, you'd do better at other banks for the same deposit amount and period.

Best fixed deposit rates for deposits $20,000–$49,999

If you have over $20,000 you want to stash away, here are your best fixed deposit rates in Singapore this month:

- Maybank (1.45% p.a.—min. $20,000 for 9 or 12 months)

- Bank of China (1.50% p.a.—min. $500 for 12 months)

- Hong Leong Finance (1.45% p.a.—min. $10,000 for 5 or 6 months)

- ICBC (1.45% p.a.—$20,000 for 6, 9 or 12 months)

- CIMB (1.45% p.a.—min. $10,000 for 9 or 12 months)

- RHB (1.45% p.a.—min. $20,000 for 6 or 12 months)

- OCBC (1.25% p.a.—min. $20,000 for 6 or 18 months)

- Standard Chartered (1.30% p.a.—min. $25,000 for 6 months)

Standard Chartered fixed deposit rates

Deposit amount: $25,000 and above | |||

Period | Personal Banking customers | Priority Banking customers | Priority Private Banking customers |

6 months | 1.30% p.a. | 1.40% p.a. | 1.60% p.a. |

Promotional rates valid until: 3 July 2026, subject to change by Standard Chartered. Do check Standard Chartered's fixed deposit rates for the latest figures.

With interest rates from 1.30% p.a. to 1.60% p.a., Standard Chartered’s fixed deposit rates are high compared to rates from other banks this month. However, do note that you only unlock the highest rates if you're a priority private banking customer, i.e. with a certain high net worth. If you’re a regular customer, you’ll only be able to get a rate of 1.30% p.a. with a 6-month tenor at their current promotional rates.

This month, you could get a better rate at banks like ICBC or the Bank of China, which also come with a smaller minimum sum. ICBC is offering 1.30% p.a. for a minimum sum of $500 and a deposit period of just 6 months, or 1.35% p.a. if you can stash $20,000 away for 12 months. For the Bank of China, deposit $500 or more to lock in 1.50% p.a. over 12 months.

MoneySmart Take

- What we like: Relatively short commitment period.

- What we don't like: Standard Chartered doesn't have very high rates for the average Joe—you only get a decent one if you're a priority private banking customer.

Best fixed deposit rates for deposits $50,000 and above

Have a fairly sizeable sum of money? If you have $50,000 or more that you want to put into a fixed deposit account, you’ve got a few good options. Here are the best fixed deposit rates in Singapore 2026 for deposits $50,000 and above:

- State Bank of India (1.50% p.a.—min. $50,000 for 6 months)

- Bank of China (1.50% p.a.—min. $500 for 12 months)

- ICBC (1.45% p.a.—$20,000 for 6, 9 or 12 months)

- RHB (1.45% p.a.—min. $20,000 for 6 or 12 months)

- CIMB (1.45% p.a.—min. $10,000 for 9 or 12 months)

- Hong Leong Finance (1.45% p.a.—min. $10,000 for 5 or 6 months)

- Citibank (0.70% p.a.—$10,000 for 12 months)

State Bank of India Singapore fixed deposit rates

SBI Singapore promotional fixed deposit rates | |

Period | Minimum deposit amount: $50,000 |

6 months | 1.50% p.a. |

12 months | 1.40% p.a. |

Rates accurate as of 3 July 2026. Do check SBI's fixed deposit promotion page for their latest promotional rates.

The State Bank of India is currently offering 2 tiers of promotional fixed deposit rates for a minimum deposit of $50,000: 1.50% p.a. for a tenor of 6 months and 1.40% p.a. for a tenor of 12 months. While $50,000 isn't exactly a small sum of money, the interest rate they're offering is high relative to other banks this month.

If you don't have $50,000 lying around, you're left with their board rates:

SBI Singapore board rates | |

Period | Deposit amount: $5,000 to $1,000,000 |

1 month | 0.35% p.a. |

3 months | 0.70% p.a. |

6 months | 0.80% p.a. |

12 months | 0.70% p.a. |

24 months | 0.25% p.a. |

The highest board rate you’ll get to enjoy is 0.80% p.a., which is not worth your time. For example, with $500, you can get 1.30% p.a. (6 months) with ICBC or 1.50% p.a. (12 months) with the Bank of China.

MoneySmart Take

- What we like: Relatively short commitment periods available, with decent interest rates.

- What we don't like: SBI asks for a high minimum deposit sum.

Hong Leong Finance fixed deposit rates

Deposit amount | 6-month | 9-month | 12-month |

$5,000 to < $20,000 | 1.28% | 1.30% | 1.30% |

$20,000 and above | 1.30% | 1.33% | 1.35% |

The rates above are given p.a. and were published on 3 July 2026. They are subject to change any time at the discretion of Hong Leong Finance. See Hong Leong Finance's fixed deposit rates for the latest.

Besides putting your money with banks, it’s also worthwhile looking into other financial institutions which also offer competitive fixed deposit rates. Hong Leong Finance is one such institution. Don’t get it confused with HL Bank, though. While the 2 share the same name, they offer entirely different fixed deposit rates.

With a lock-in period of 6 to 12 months, Hong Leong Finance is currently offering a fixed deposit rate of up to 1.35% p.a. for a $10,000 minimum deposit over 12 months. This is high compared to other fixed deposit interest rates this month. Apply online via HLF Digital to enjoy this rate.

MoneySmart Take

- What we like: Short tenor periods for which you have to stash your cash with them. They also offer a minimum deposit option of $5,000, which is more beginner-friendly.

- What we don't like: Hong Leong Finance isn't coming out super strong in terms of their fixed deposit rates—average at best.

Now that we’ve had a look at the interest rates banks have to offer, here’s a quick and easy summary of what you need to know about fixed deposits.

Fixed deposit vs savings account—what’s the difference?

Anyone looking for a better alternative to their basic savings account will be faced with the same decision: fixed deposit or high-interest savings account? Both options beat the measly 0.05% p.a. interest on a regular savings account, but looking at interest rate alone isn’t enough to compare the two.

Here are the differences between fixed deposits and savings accounts at a glance:

Fixed deposit | Savings account | |

Tenure | As low as 1 month, but go for at least 6 months for better rates | None |

Interest rate | Usually, the longer the tenure, the better the interest rate | Usually the same regardless of tenure |

Deposit amount | Fixed amount, usually at least $5,000, but promotional offers can go as low as $500 with ICBC and the Bank of China | Smaller initial deposit and minimum monthly balance ($500 to $3,000) |

Currency | SGD by default, but some banks offer higher interest rates for foreign currency | SGD by default. There are a few multi-currency accounts, but no difference in interest rate |

Can you withdraw? | Contrary to popular belief, yes, you can withdraw prematurely. However, you lose the interest and may have to pay a penalty. | Yes, no impact on interest, but don’t fall below the minimum balance |

Interest payments | Quarterly or annually | Monthly |

Risk level | Virtually risk-free, insured up to $100,000 by Singapore Deposit Insurance Corporation (SDIC) | |

Compare fixed deposit vs Singapore Savings Bonds (SSB) vs T-bills

If you’re looking for a virtually risk-free investment vehicle, you’re bound to have come across fixed deposits, Singapore Savings Bonds (SSB) and Treasury bills (T-bills). Which is the right one for you? Here are some key differences you should consider.

Fixed deposit | SSB | T-bills | |

Tenure | As low as 1 month, but go for at least 6 months for better rates | 10 years | 6 months / 1 year |

Current interest rate | Up to 3.35% p.a. | 2.11% p.a. (Jun 2026 SSB’s 10-year average return) | 1.48% p.a. (cut-off yield for 4 Jun 6-month T-bill) |

Deposit amount | Usually at least $5,000, but promotional offers can go as low as $500 with ICBC and the Bank of China | $500-$200,000 | $1,000, with a cap of $1 million in non-competitive bids at each auction. |

Currency | SGD by default, but some banks offer higher interest rates for foreign currency | SGD | SGD |

Can you withdraw? | Contrary to popular belief, yes—you can withdraw prematurely. However, you lose the interest and may have to pay a penalty. | Yes, with no penalty. However, you must pay a $2 transaction fee each time you buy/redeem a bond. | No, you cannot redeem T-bills early. Instead, you can try to sell it on the secondary market. |

Interest payments | Quarterly or annually | Every 6 months | Upon maturity, full value of T-Bill refunded following initial sale at a discount |

Risk level | Virtually risk-free, insured up to $100,000 by Singapore Deposit Insurance Corporation (SDIC) | Virtually risk-free, backed by the Singapore government | Virtually risk-free, backed by the Singapore government |

Find out more about the best easy and low-risk investments, including T-bills, SSBs and more.

You can also explore fixed deposits in other currencies. For starters, we also compare fixed deposit in Hong Kong! Check out our guide to HKD fixed deposit rates.

Know anyone who'd like guaranteed returns from their cash? Share this article with them!

Related Articles