For most Singaporeans, buying an HDB flat means taking on a home loan that will last decades. One of the first decisions buyers face is whether to finance their flat with an HDB concessionary loan or a bank loan.

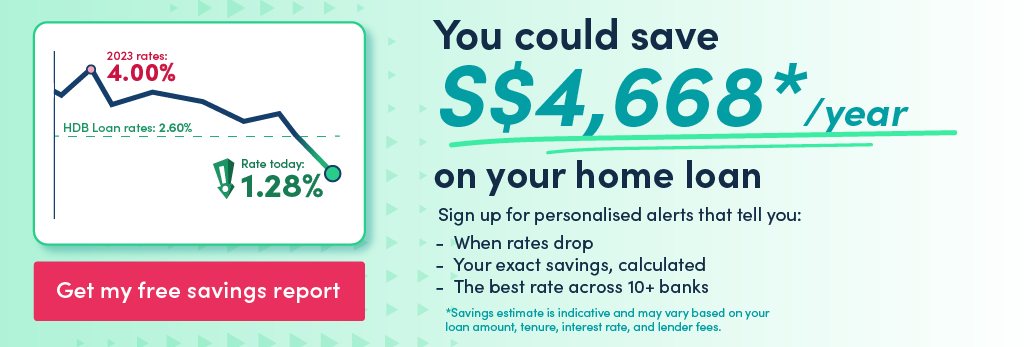

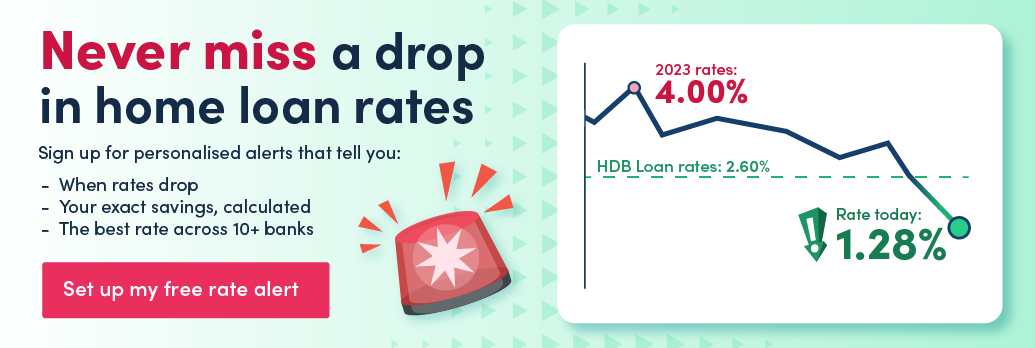

In 2025 and early 2026, Singapore bank home loan interest rates eased from the higher levels seen in previous years. Fixed-rate mortgage packages that were commonly quoted in the low 3% range in early 2025 have since been offered closer to the 1.4%–1.8% range in late 2025 into 2026, as benchmark rates softened and banks became more competitive.

This shift has prompted more buyers—including HDB buyers—to re-examine whether a bank loan could be worth considering alongside the historically stable HDB concessionary loan.

For starters, both options can be used to buy the same HDB flat, but they work very differently. Interest rates are structured differently. Upfront costs differ. So do eligibility rules, repayment flexibility, and how much you can comfortably borrow.

This guide breaks down how HDB loans and bank loans work in 2026, so you can understand the trade-offs clearly before deciding which path makes sense for you.

In summary

|

[ms-toc title="HDB loan vs bank loan: Key things to know in 2026"]

1. Why this choice matters for today’s HDB buyers

A home loan isn’t just about the interest rate you start with. It affects:

- how much cash or CPF you need upfront

- how predictable your monthly repayments are

- how flexible you are if your finances change

- whether you can switch loans later without penalties

In recent years, interest rates have moved more than many buyers were used to. At the same time, HDB affordability rules and loan limits have continued to shape how much buyers can borrow. That’s why understanding how each loan option works—beyond headline rates—matters more than ever.

2. The 2 main home loan options for HDB flats

What is an HDB concessionary loan?

An HDB concessionary loan is provided directly by the Housing & Development Board. It is available only to buyers who meet HDB’s eligibility criteria, including citizenship, income ceilings, and property ownership rules.

The interest rate for an HDB loan follows a fixed formula: it is pegged to the CPF Ordinary Account (OA) interest rate plus a small margin. Because CPF OA rates are relatively stable, HDB loan repayments tend to be predictable over time.

What is a bank home loan?

Bank home loans are offered by private financial institutions such as DBS, OCBC and UOB, among others. These loans are typically pegged to market benchmarks such as SORA (Singapore Overnight Rate Average), or offered at a fixed rate for an initial period before switching to a floating rate.

Bank loans give borrowers more exposure to market movements. When rates fall, repayments may become cheaper. When rates rise, repayments can increase. This variability is an important difference compared to HDB loans.

3. HDB loan vs bank loan—Key differences at a glance

Feature | HDB loan | Bank loan |

Interest rate type | Pegged to CPF OA + margin | Market-linked (fixed or floating) |

Loan-to-value (LTV) limit | Up to 75% | Up to 75% |

Downpayment | 25% (CPF and/or cash) | 25% (at least 5% cash) |

Maximum tenure | Typically up to 25 years | Often up to 30 years |

CPF usage | Full use of CPF OA allowed | CPF OA allowed, with limits |

Lock-in period | None | Common (varies by bank) |

This table isn’t about deciding which loan is “better”. It’s about understanding how the structure of each loan affects your finances.

Next, we’ll dive deeper into 4 differences between the 2 types of loans and explain how you should factor them in.

4. Key difference #1: Loan-to-value limits in 2026—how much can you borrow?

Flat Value20%CashCPF/Housing Grants/CashHDB LoanDownpaymentFor HDB concessionary loans, the downpayment is 25% of the valuation.All 25% of the downpayment can come from CPF or housing grants.Flat Value25%CPF/Housing Grants/CashAmountFinancedof flat75%Bank LoanDownpaymentFor banks, the downpayment is 25% of the valuation.20% of this downpayment can come from CPF or housing grants. The last 5% must be paid in cash.AmountFinancedof flat75%25%5%

Both HDB loans and bank loans generally allow buyers to borrow up to 75% of the flat’s purchase price or valuation, whichever is lower. CPF OA can usually be used to cover the monthly instalments

That means buyers must fund the remaining 25% upfront using a combination of CPF OA savings and cash.

With an HDB loan, many buyers can cover most or all of this 25% using CPF OA, depending on how much they have accumulated. Cash is only required if CPF OA is insufficient

With a bank loan, buyers are required to pay at least 5% in cash, with the remaining portion of the downpayment funded by CPF OA or additional cash.

However, the 75% borrow limit is only one part of the equation.

Income-based limits: MSR and TDSR

Beyond the property-based cap, how much you can borrow is also constrained by affordability rules.

For HDB flats, the Mortgage Servicing Ratio (MSR) limits how much of your gross monthly income can go towards your home loan instalment.

For bank loans, lenders also assess the Total Debt Servicing Ratio (TDSR), which looks at all your debt obligations combined—including car loans, credit cards and other commitments—not just your mortgage.

In practical terms, this means:

- You may not qualify for the full 75% loan amount even if the property value allows it.

- A bank loan might look cheaper on paper, but your existing debts could reduce how much you’re allowed to borrow.

For some buyers, the LTV is the binding constraint. For others, it’s the income-based rules that determine their actual loan amount.

ALSO READ: Buying a House? Here are 8 Terms You Need to Know Before You Meet Your Realtor

5. Key difference #2: Interest rates and monthly repayments

How HDB loan interest rates work

HDB loan interest rates are pegged to the CPF Ordinary Account (OA) interest rate, plus a fixed margin. In practice, this means the HDB concessionary rate is set at CPF OA + 0.1%, which works out to 2.6% per year as of 2026, based on the current CPF OA rate.

This rate does not move in line with market benchmarks such as SORA—ensuring repayment stability. Monthly instalments remain relatively predictable, which can be reassuring for buyers who prefer certainty and long-term budgeting clarity.

How bank loan rates work in 2026

Bank home loans are typically structured around fixed rates, floating rates, or a combination of both. Many bank loans start with a fixed interest rate for an initial period, commonly two to five years, before switching to a floating rate thereafter. This allows borrowers to lock in predictable repayments for a period of time, after which the loan becomes market-linked.

Floating-rate bank loans are usually pegged to market benchmarks, plus a bank-determined spread. As market rates move, the interest charged on these loans can rise or fall, which means monthly repayments can change over time.

Because bank loan rates are tied to market conditions, they offer potential savings when rates fall—but also introduce variability. This exposure to rate movements is one of the key differences between bank loans and the more stable HDB concessionary loan.

6. Key difference #3: Eligibility rules and loan assessments

Who qualifies for an HDB loan

HDB loans are subject to specific eligibility rules, including:

- At least one buyer must be a Singapore citizen

- Buyers' monthly income must not exceed $14,000 (or $21,000 for extended families)

- Buyers must not own any private residence (in Singapore or overseas)

- Buyers must not have taken more than two previous HDB loans

- Buyers have not disposed of private residential property within 30 months before the loan application

- Buyer's monthly income must not exceed $7,000 for singles buying a 5-room or smaller resale flat, or 2-room new flat in a non-mature estate under the Single Singapore Citizen (SSC) Scheme

Not all buyers qualify, even if they are financially able to service a loan.

How bank loans are assessed

Banks assess borrowers based on income stability, existing debt, credit history, and overall financial health. There is no income ceiling, but approval depends on meeting affordability rules and bank-specific criteria.

For specific requirements, you could speak directly with our financial advisory team, or get in touch with your preferred bank directly.

7. Key difference #4: Flexibility over the loan period

Early repayment and refinancing

HDB loans generally do not come with lock-in periods. Borrowers can make partial repayments or redeem the loan early without penalty, subject to HDB’s rules.

Bank loans, however, often include lock-in periods, commonly between one and three years. Refinancing or redeeming the loan during this period may incur fees, depending on the bank package.

To make this more concrete, here are two scenarios buyers often ask about.

Scenario 1: Taking an HDB loan first, then refinancing to a bank loan later

Some buyers start with an HDB loan because of its stable, CPF-pegged interest rate and predictable repayment structure.

For example:

- Loan amount: $400,000

- HDB interest rate: 2.6% per year

- Monthly repayments remain relatively steady over time

If bank loan rates become more competitive a few years later, the buyer may decide to refinance from HDB to a bank loan.

Because HDB loans do not have lock-in periods, this switch is generally possible. However, refinancing still comes with practical considerations, such as:

- Legal and administrative fees

- Property valuation costs

- New bank package terms (including lock-in periods)

The key takeaway is that starting with an HDB loan keeps the option open to move to a bank loan later, if circumstances change.

Scenario 2: Taking a bank loan first (and why switching back to HDB is not straightforward)

Other buyers may start with a bank loan, especially when banks are offering attractive fixed-rate packages.

For example:

- Loan amount: $400,000

- Bank fixed rate (first 2–3 years): around 1.5%–2.0%

- After the fixed period, the loan may revert to a floating rate pegged to SORA

One important point is that bank loans generally cannot be switched back into an HDB loan later.

HDB concessionary loans are typically granted at the point of purchase, subject to eligibility conditions. So buyers who begin with a bank loan should treat it as a longer-term commitment to staying within the bank loan system, even if they refinance between banks.

Bank loans may also involve:

- Lock-in periods

- Early repayment penalties during lock-in

- Greater variability in monthly repayments over time

8. A simple way to think about the trade-offs

HDB loan | Bank loan |

– Stability | – Potential cost savings |

Neither option is universally better. The right choice depends on how you weigh certainty, flexibility, cash flow, and long-term comfort.

Choosing between an HDB loan and a bank loan is a long-term decision. Rather than focusing only on headline interest rates, it helps to understand how each loan works—how repayments behave, how much flexibility you have, and how the loan fits into your broader financial picture.

Before deciding, check the latest information from official sources such as HDB, CPF Board, and banks directly. What matters most is choosing a structure you can live with comfortably over the long run.

Found this article useful? Share it with your family and friends!

Related Articles