If your home loan is currently charging you more than 2.4% interest, you might be paying more than you need to, and should definitely consider refinancing.

Refinancing your home loan in Singapore means reducing your monthly repayment amount by switching to a lower interest rate.

This could mean switching to a new loan package within your current bank, or switching bank altogether. Here’s what you should know about refinancing in Singapore:

Contents

- What is refinancing?

- How much can you save when you refinance?

- When should you refinance your home loan?

- What is the cost of refinancing?

- Repricing vs refinancing - what's the difference?

- Bottom line: Should you refinance or not?

1. What is refinancing?

Refinancing a home loan is an opportunity for homeowners to switch their home loan to another bank for a lower interest rate. This can help you save money in the long run.

Refinancing is usually done when you hit the 4th year of your home loan or after. That's because typical home loan packages raise their interest rates after 3 years, after which the interest rate is likely to rise. So this is the best time to see if another bank can offer you a lower interest rate.

Another reason homeowners in Singapore consider refinancing their current home loans is due to changes in SIBOR and SOR rates (which determine the interest rates on some home loans).

SIBOR and SOR could be on their way up due to global economic changes, so if an increase is predicted, you’ll want to switch to a lower interest rate loan too.

The Monetary Authority of Singapore (MAS) and The Association of Banks Singapore (ABS) monitor these SIBOR and SOR rates and make adjustments to inter bank lending rates daily.

2. How much can you save by refinancing home loans?

Here’s an example to illustrate how you can save on monthly repayments when you refinance home loans:

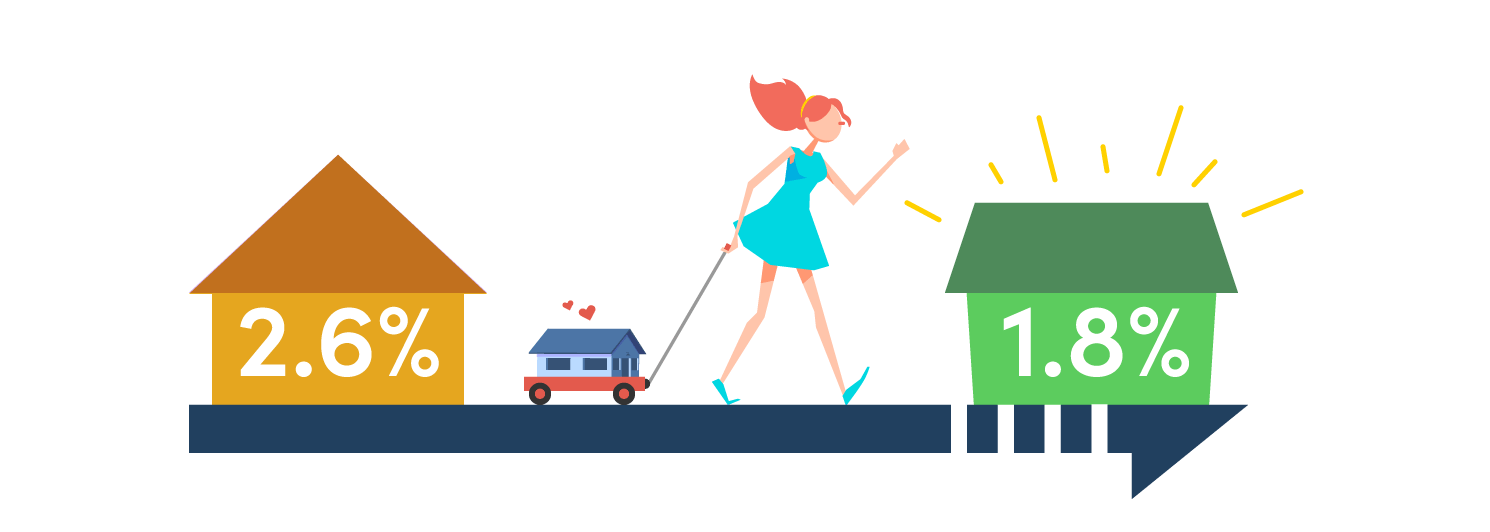

Ms Liana has an outstanding home loan of $300,000 with about 20 years left. Her current interest rate is 2.6%. That means she’s paying about $1,604.36 a month.

Let’s assume a bank is willing to offer her a home loan package of 1.8% for the first 3 years. If she takes it up, she will only need to pay about $1,489.40 a month. That’s a difference of about $115 a month, $1,380 a year and $4,140 after 3 years!

Current loan package | New loan package | Savings | |

Outstanding loan amount | $300,000 | $300,000 | - |

Interest rate | 2.6% | 1.8% | 2.6% - 1.8% = 0.8% |

Estimated monthly repayment | $1,604.36 | $1,489.40 | $1,489.40 - $1,604.36 = $115 |

Of course, this is a simplified illustration. In reality, you also need to consider other factors like the lock-in period into the real cost of refinancing. (More on that in the next section.)

You'll also need to pay legal charges and valuation fees when you refinance. This can set you back by $2,000 to $3,000 depending on your property type.

So, while you do save money in the long run, the amount you save may not be as significant as it first appears. In this article we'll cover all the costs that go into a refinancing package so you can understand them better.

3. When should you start looking to refinance your loan?

While you can technically refinance at any time, you should always wait until your lock-in period is over before you jump ship. If you try to do it during the lock-in period, you'll usually be charged a penalty fee, typically about 1.5% of your outstanding loan amount.

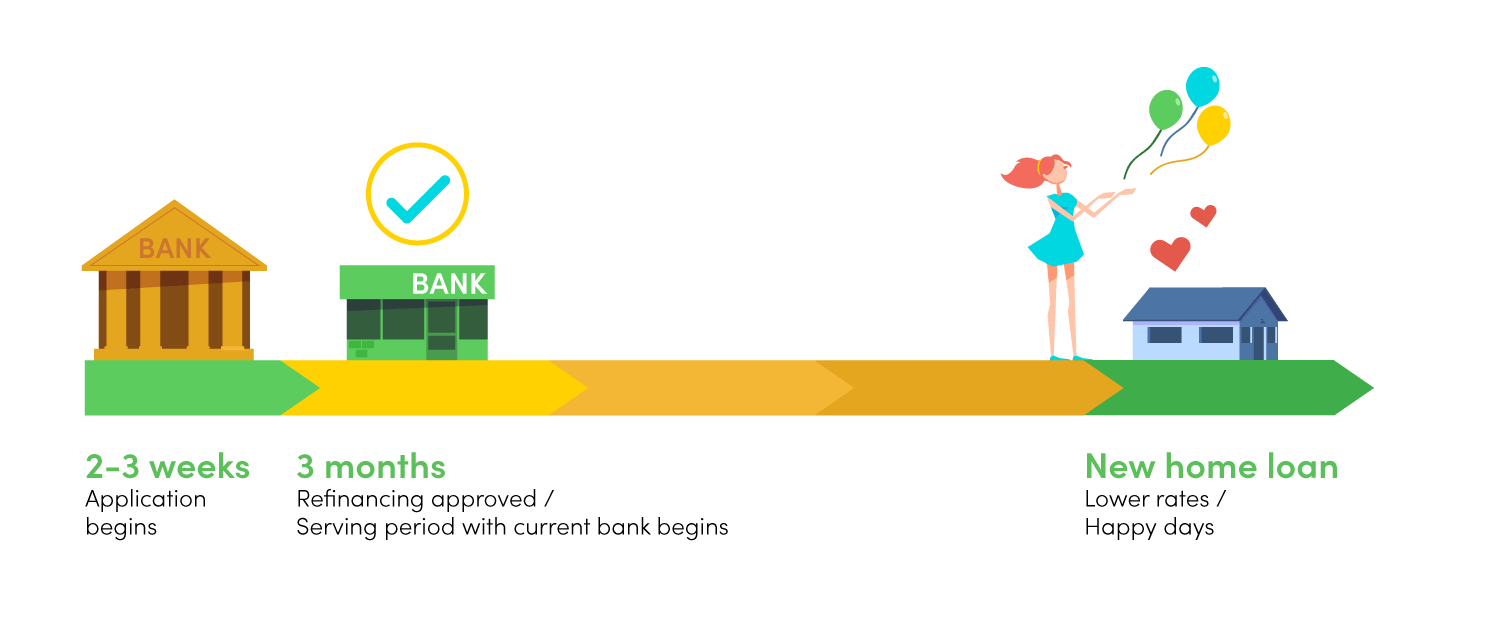

There’s no need to wait until the lock-in period is over before you begin the process of refinancing, though.

Newly-signed refinancing contracts are valid for 6 months, so in a rising interest rate environment, you’ll want to obtain a good home loan package as early as possible. You would also need to give at least 3 months’ notice before you can refinance.

Here’s how early you should be refinancing in order to make sure you don’t pay a higher interest rate:

Typically, bank loans have a lock-in period of 2 or 3 years. You will want to take note of the date on which your current bank will increase your home loan interest rates, and work backwards from there.

Based on the timeline above, starting your process of refinancing applications should begin about 4 months or so before the date of the increase. This factors in the 3 month notice period you need to serve with the current bank and also application time with the new bank you wish to move to.

Lock-in periods are the norm, but if you're really lucky, you might be one of those people who signed up for a home loan package with no lock-in. This can happen if you signed your home loan during a price war between the banks.

4. What is the cost of refinancing?

We have already mentioned the various costs of refinancing – legal fees, valuation fees, prepayment penalties during the lock-in period.

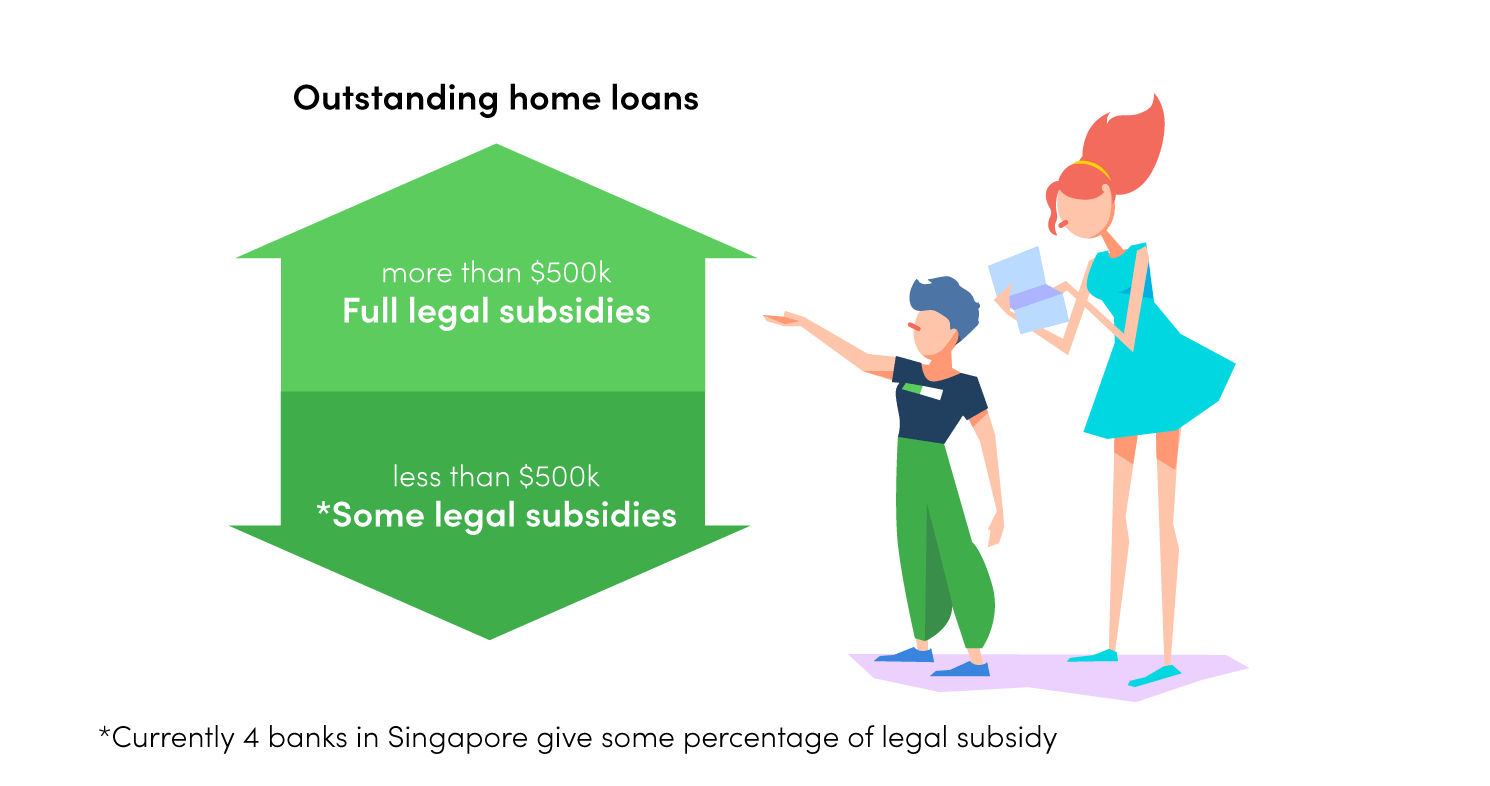

However, some of these costs can be subsidised by the bank under some circumstances. For example, if your loan amount is big enough, banks will be willing to defray the legal fees with subsidies. They usually do this for outstanding loan amounts above $500,000.

While everyone loves a good freebie, do think carefully about taking on such legal subsidies as they will often come with terms and conditions. Mostly, these stipulate a certain duration known as the "clawback period", which is the time you need to stay with the bank before you can refinance to another bank without a penalty fee.

In other words, this is a new lock-in period for your new home loan. If you don't stick with this bank for the duration of it, the bank will claw back the freebies they gave you.

Another cost of refinancing is known as the cancellation fee. This is incurred if you refinance a home loan package when the property is still uncompleted. For buildings under construction, the home loan amount is disbursed in stages. The cancellation fee amount is around 1.5% of the loan amount that hasn’t been disbursed yet.

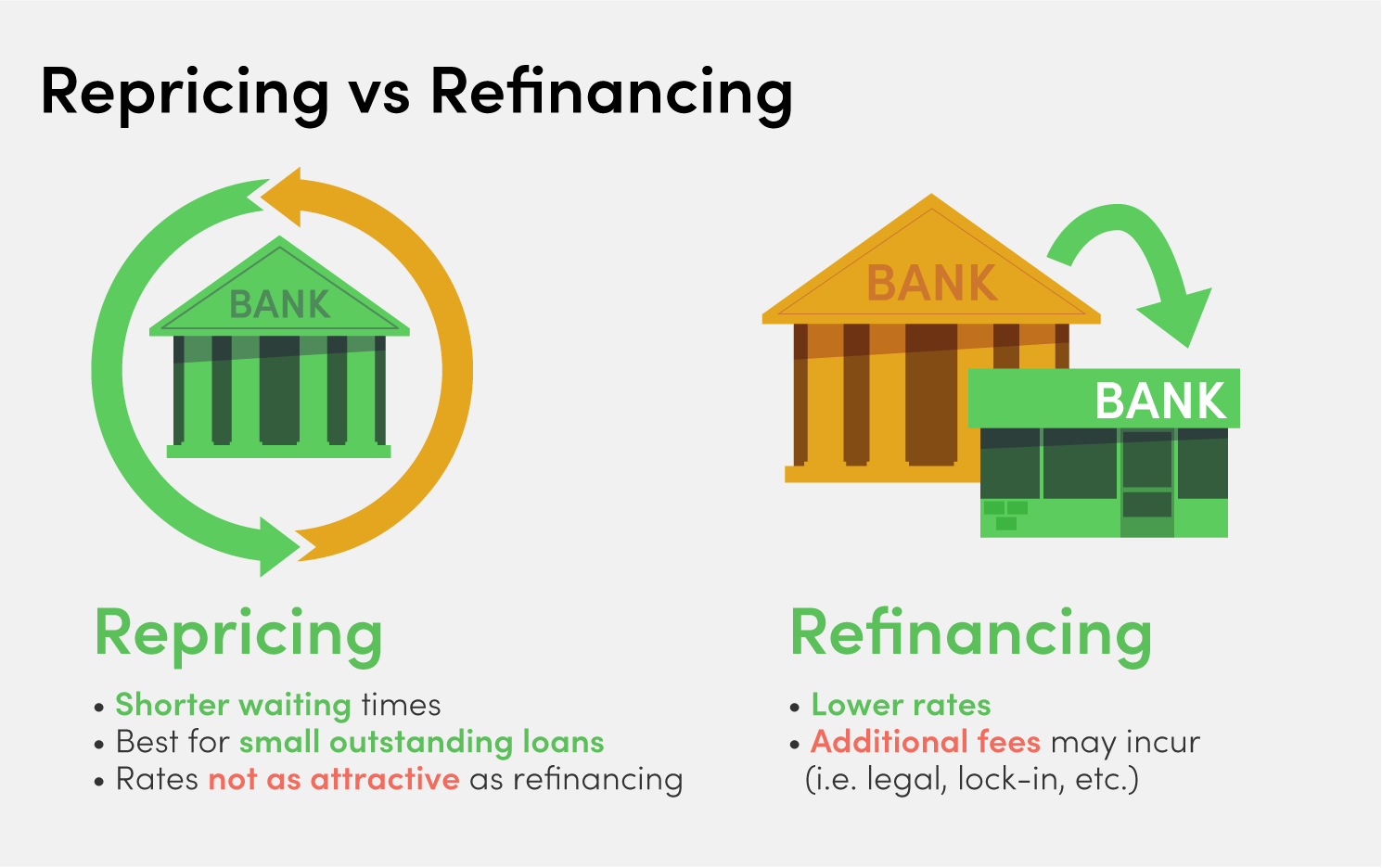

5. Repricing vs refinancing - what's the difference?

If you're not happy about your current home loan's increasing interest rates, you do have another option apart from refinancing - repricing. Repricing a home loan is similar to refinancing except that you stay with the same bank and switch to a new loan package that they offer you.

The time it takes to reprice is shorter compared to refinancing, which means you can switch to a lower interest rate package sooner.

Repricing does not require legal fees and a new valuation of the property does not need to be conducted. However, it is not necessarily cheaper than refinancing, especially when you sign up for loans that come with legal fee subsidies.

Cost of refinancing | Cost of repricing | |

Legal & valuation fees | $300 to $500 (or none, if it’s subsidised by the bank) | - |

Administrative fees | - | $500 to $800 |

Total cost | $300 to $500 | $500 to $800 |

The sad fact is that banks always try harder to get new customers than retain existing customers. You are more likely to find a more competitive interest rate when you refinance than when you reprice.

A savvy homeowner will want to find out what the refinancing options are in the market, and then check back with their bank if they can offer a competitive repricing package.

Ultimately, there is only one factor you should consider when choosing whether to refinance or reprice – cost.

In most cases, repricing is usually ideal only for homeowners who have a small outstanding loan amount of $200,000 or less, since the cost of refinancing will probably be significant compared to the amount you save.

Bottom line: To refinance or not to refinance?

If your outstanding loan amount is above $500,000, then you should seriously consider refinancing. It's easier for you to refinance for cheap as most banks will absorb the legal fees.

And due to the low interest rate environment, you can snag a low interest mortgage very easily at the moment. We're talking about interest rates as low as 1.29% p.a. — much, much lower than HDB's 2.6%.

If your outstanding loan is below $500,000, you can still refinance, but you have fewer options as only a handful of banks will subsidise your legal fees.

In this case, you should check out both refinancing packages with legal fee subsidies AND also the repricing options offered by your bank.

Either way, you can cut out the legwork by refinancing through MoneySmart. Our mortgage specialists will round up the best home loan packages for you so you don't have to trawl through all the banks' websites.

We'll also help you work out the costs of each options and give you unbiased advice on what you should do next. Best of all, this service is completely free so you don't waste a cent if you decide not to refinance after all.

Assessing whether you should or should not apply for refinancing of your home loan in Singapore comes with several factors to consider. Contacting a Mortgage Specialist at MoneySmart for a free consultation can also help you make sense of it all.