If you could earn more than your CPF interest, would you actually be better off?

That’s the question behind the CPF Investment Scheme (CPFIS). On the surface, it sounds straightforward: take some of your CPF savings, invest it, and aim for higher returns than what your Ordinary Account or Special Account provides. But once you factor in risks, fees, and the discipline required to invest well, the answer becomes far less obvious.

And it doesn’t help that your CPF isn’t the only benchmark. With options like fixed deposit accounts offering relatively stable returns, the bar for “beating CPF” is higher than it first appears.

Before you commit your CPF savings, here’s a clearer look at how CPFIS really stacks up, and what you need to get right for it to be worth it.

What am I currently earning on my CPF savings?

Before we think about investing our CPF savings, we need to see what we’re currently earning (since we need to beat this rate).

Here are the current interest rates on CPF accounts:

Account type | Annual interest rate | Bonus interest |

Ordinary Account (OA) | 2.5% | +1% on first $60,000 for members below 55 years old (capped at $20,000 for OA) |

Special Account (SA) | 4% | |

Medisave Account | 4% | |

Retirement Account | 4% |

(Since CPFIS directly relates to OA and SA, we’ll talk a little more about these 2 accounts.)

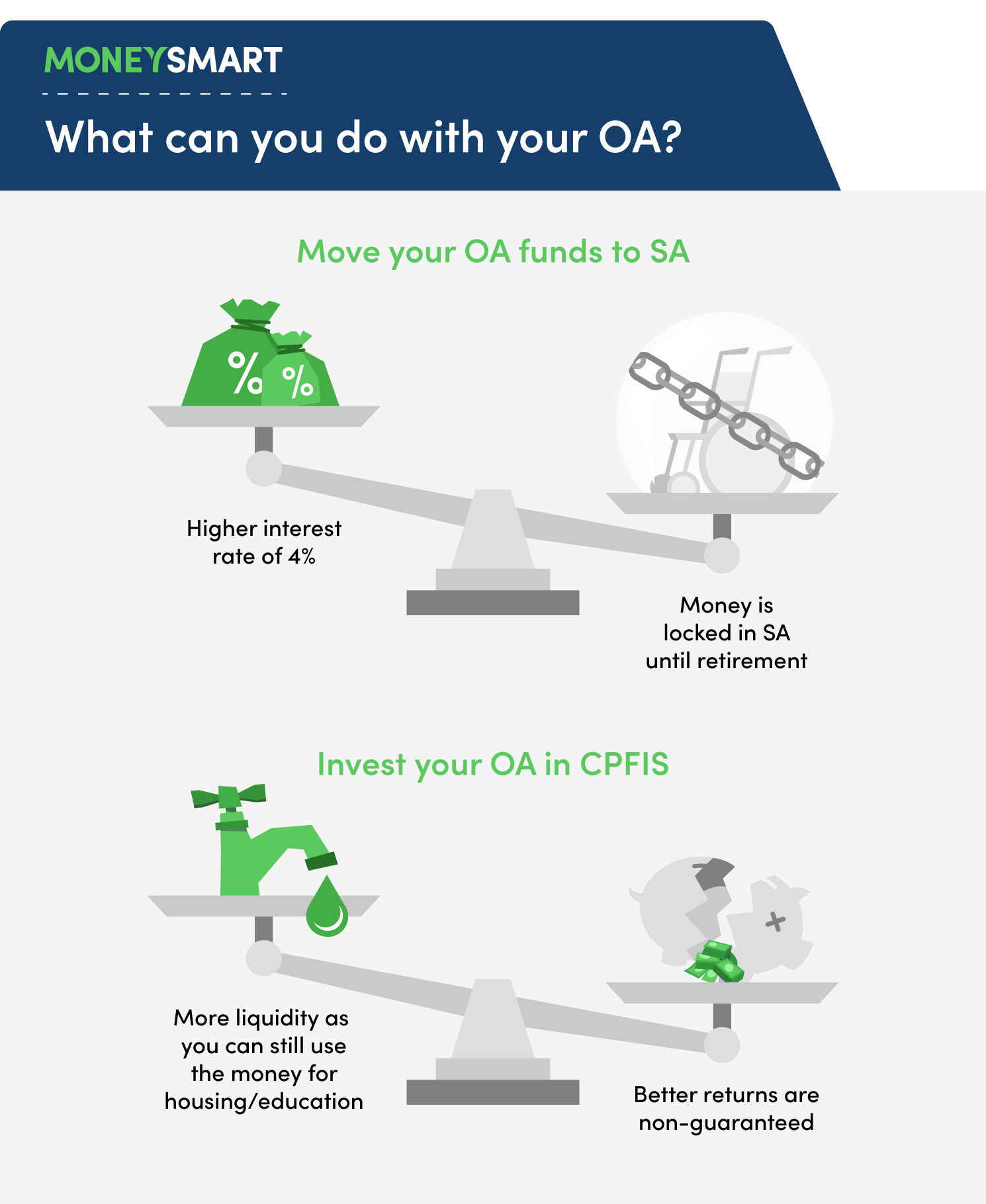

Obviously, the interest rate for SA is a lot more attractive than that of OA. So one way to get better returns from your CPF is simply to move your OA funds to your SA.

The problem is, this is a one-way street—you can’t transfer your SA funds back into your OA where you can spend it on housing or education. It’s just going to get locked up there until retirement. That’s why CPFIS is so attractive. You can get better returns than 2.5% on your OA savings without locking it up.

But here’s the part you need to bear in mind: interest from CPF is guaranteed. Interest from CPFIS is not. If you don’t invest wisely or are unlucky, you could end up with <2.5% in returns.

If you have no knowledge of investing, it’s probably wiser to leave your money where it is while you learn how to invest. Or maybe consider moving some excess OA funds (that you definitely won’t need for education/housing) to your SA.

Who is eligible for the CPF Investment Scheme?

If you’re interested in CPFIS, there are a few requirements you need to meet (apart from having a CPF account, duh):

Factor | Minimum requirement |

Age | 18 years old |

Legal status | Not undischarged bankrupt |

CPF (OA) balance | $20,000 (for CPFIS-OA) |

CPF (SA) balance | $40,000 (for CPFIS-SA) |

CPFIS Self-Awareness Questionnaire (SAQ) | You must have completed the questionnaire |

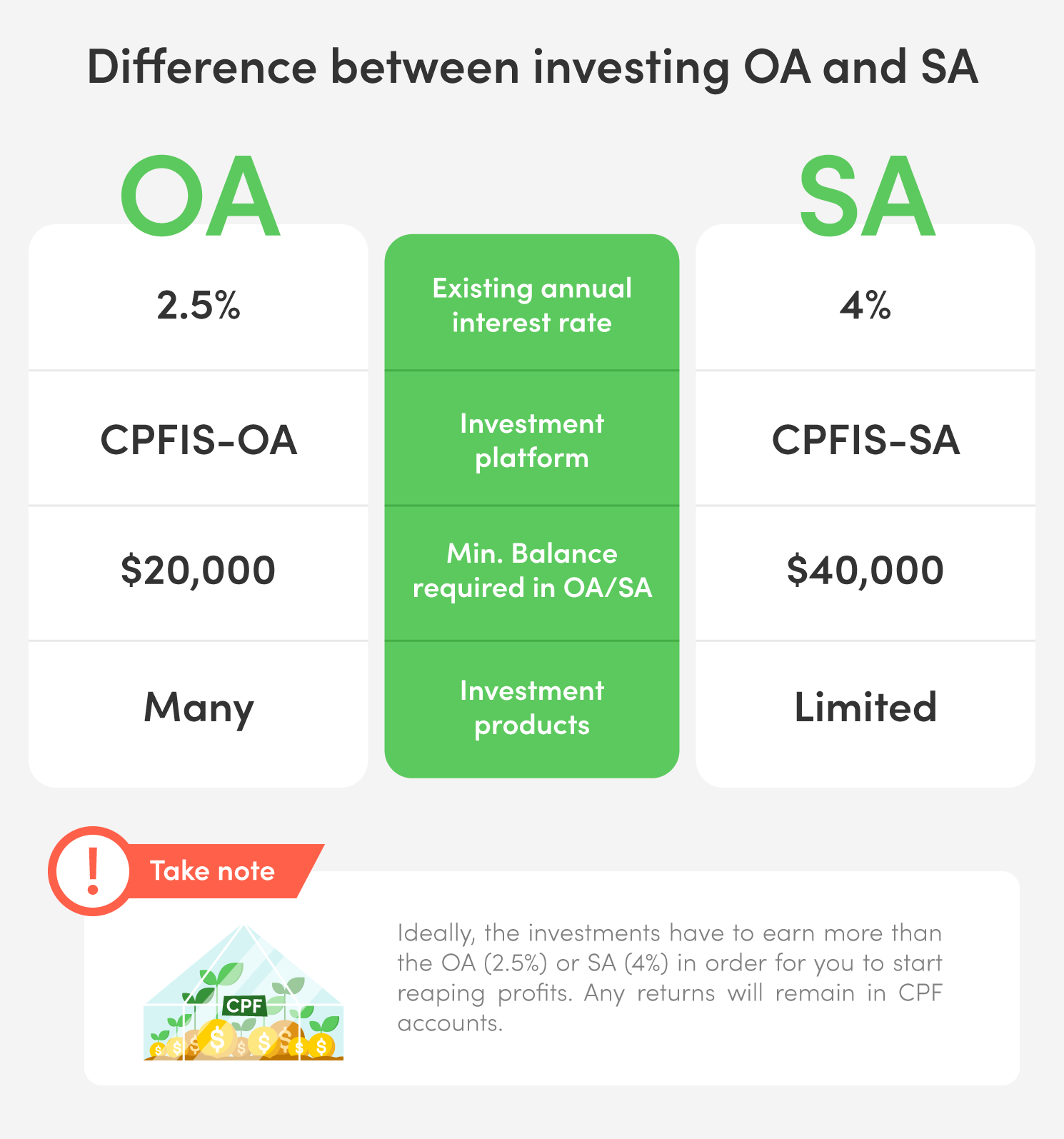

The CPF account balance has two different requirements because there are two CPF investment schemes, one for OA and one for SA.

Broadly speaking, using your OA savings to invest under CPFIS-OA will give you more investment product options, including shares, gold, higher-risk ETFs, and unit trusts.

These investments aren’t allowed under CPFIS-SA (remember that it’s also harder to beat the 4% interest rate on your SA).

What do you need to know before using your CPFIS?

One important thing to remember about CPFIS is that any returns you get will go back to your CPF accounts. That means you should invest with the future in mind. This money is for your retirement, not for you to enjoy during your working years.

To ensure that you don’t invest in volatile or high-risk options, CPF has shortlisted some investment products for you. After all, they don’t want you to gamble for CPF savings away.

What can I use my CPF to invest in?

As mentioned, CPF will not allow you to go berserk with your investing—you can’t go pumping all your cash into the latest cryptocurrency.

You can only invest in very specific products. The full details (down to the specific product names) are helpfully provided on the CPF website—see this complete list of CPFIS investments.

In summary, here’s a table of products ranked from least to most restricted:

Type of investment | CPFIS-OA | CPFIS-SA |

Yes | Yes | |

Yes | Yes | |

Yes | Yes | |

Yes | Yes | |

Yes | Yes, but not the higher-risk ones and currently no products are approved | |

Yes | Yes, but not the higher-risk ones | |

Yes | Yes, but not the higher-risk ones | |

Fund management accounts | Yes | No |

Corporate bonds | Up to 35% of investible savings | No |

Up to 35% of investible savings | No | |

Up to 35% of investible savings | No | |

Up to 10% of investible savings | No | |

Up to 10% of investible savings | No |

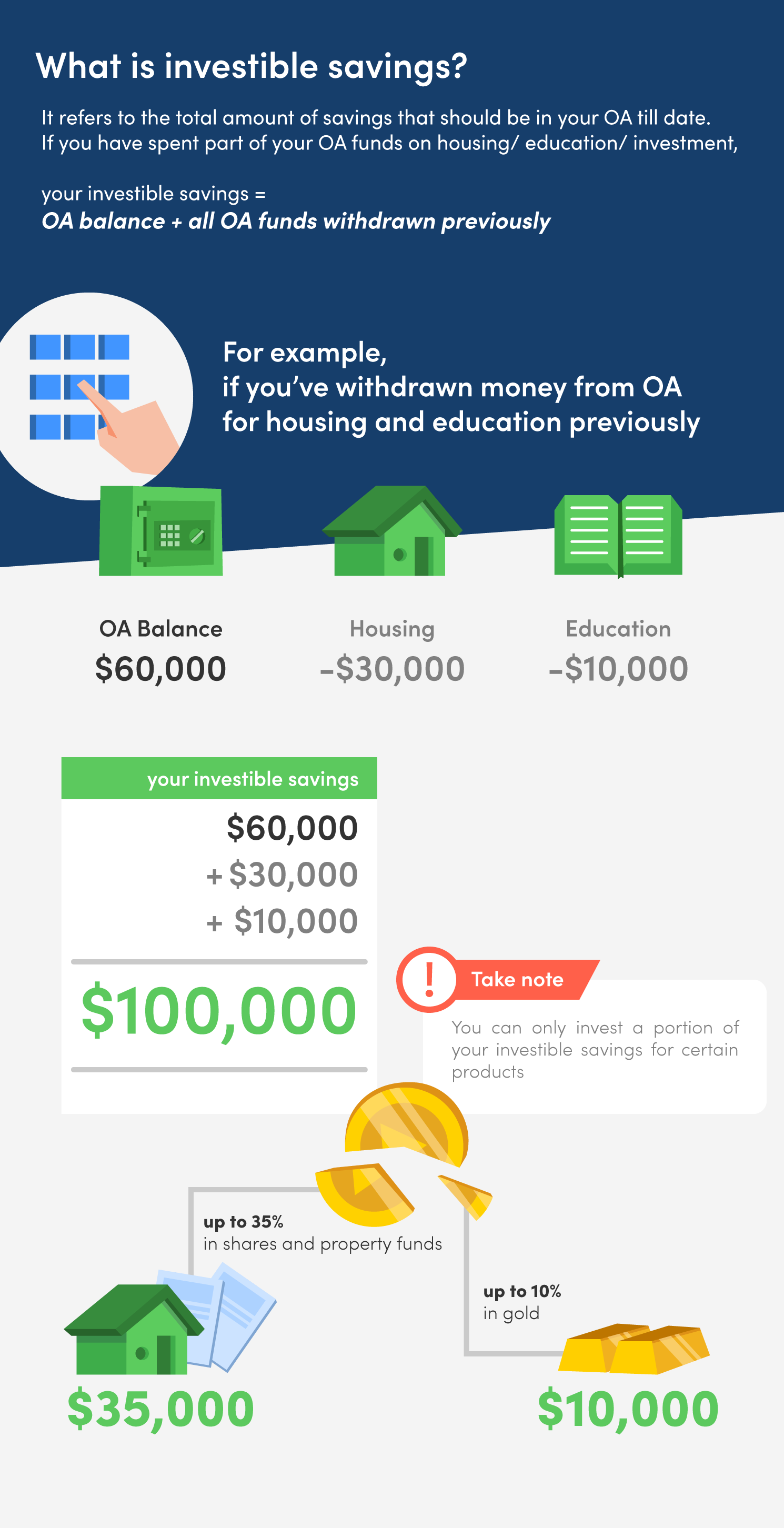

Note: "Investible savings" refers to your account balance + whatever you've withdrawn for housing and education.

For example, if you've withdrawn $30,000 for housing and you now have $70,000 in your OA, your investible savings are $70,000 + $30,000 = $100,000. That means you can invest up to $35,000 (35%) in shares and property funds and up to $10,000 (10%) in gold.

What are the potential returns of CPFIS investments?

This isn’t an easy question to answer because of the range of products available. For example, bonds tend to be lower risk, lower returns, while unit trusts are generally higher risk, higher returns.

Whatever you invest in, you need to earn more than the risk-free interest rates of the CPF Ordinary Account (2.5%) and Special Account (4%), or it will be pointless.

It's definitely doable but not that easy in practice.

Almost every investment involves some kind of extra cost—ranging from investment brokerage commission fees to hefty unit trust management fees—you need to make sure your returns earn enough to pay for those as well. Otherwise, these costs will erode your returns.

These pitfalls (in tandem with some irresponsible financial advisors’ aggressive sales tactics) have left some Singaporeans worse off than if they had never touched the money in the first place!

... But the Gahmen will help us, right?

Of course, this is Singapore—where the Government recognises the importance of protecting CPF members from unsuitable investment decisions. According to CPF Board data from recent years, the majority of CPFIS-OA investors still do not consistently outperform the OA’s risk-free rate, especially after accounting for fees.

One challenge in the past was the way financial advisors (FAs) were compensated. Previously, CPFIS unit trusts and investment-linked insurance products were distributed via financial advisers and could include sales charges, which formed part of advisers’ remuneration. This sometimes led to potential conflicts of interest, as the incentives for FAs were not always perfectly aligned with investors’ best interests.

To address this, the Government has steadily introduced measures to make CPF investing safer and more cost-effective. Since 2018, various “cooling measures” have been rolled out to encourage responsible advisory practices and reduce costs for CPFIS investors.

As of October 2020, FAs can no longer charge upfront sales fees for CPFIS investments, and wrap (platform) fees are now capped at 0.4%. These changes have helped lower the overall cost of investing, but it’s still important for members to remain informed and cautious, especially when considering more complex products.

As always, do your own research and make sure you understand all fees involved before making investment decisions.

Got it! How do I start investing under CPFIS-OA?

Provided you meet the eligibility criteria and understand the potential pitfalls, it's easy to get started with CPFIS.

We recommend starting with CPFIS-OA as the interest rate of 2.5% is lower and, therefore, easier to beat through investing than your SA's 4%. Here are the next steps.

Step 1: Open a CPF Investment Account with DBS, OCBC or UOB

Open an account with your favourite local bank. Fees and charges are the same for all three, so it doesn't matter which. This account is purely to allow your bank to administer the funds. You will still need a brokerage account to actually invest the money.

(FYI, for CPFIS-SA, there's no need to open an Investment Account. Just approach the investment product providers directly.)

Step 2: Open an investment brokerage account

The next step is to open an account with one of the CPFIS-eligible investment brokerages. You can compare fees and apply for an account through MoneySmart.

- Min. Commission Fee US Stocks

- US$25

- Min. Commission Fee SG Stocks

- S$25

- Min. Funding

- S$0

- Min. Commission Fee US Stocks

- US$20

- Min. Commission Fee SG Stocks

- S$25

- Min. Funding

- S$0

- Min. Commission Fee US Stocks

- US$20

- Min. Commission Fee SG Stocks

- S$18

- Min. Funding

- S$0

@4x.png)

- Min. Commission Fee US Stocks

- US$3.88

- Min. Commission Fee SG Stocks

- 0.08% (no min.)

- Min. Funding

- $0

Your brokerage doesn’t necessarily have to be with the same bank as your CPF Investment Account. For example, you can open a CPF Investment Account with DBS and invest in ETFs with Phillip Securities. Phillip will liaise with DBS to execute the purchase.

Read more:How to Buy Stocks in Singapore: Start Investing in 5 Easy Steps

Alternatively: Go through a (robo) advisor

If you have no wish to get all DIY with your CPF investments, you can invest through an advisor—human or otherwise.

As of 2026, Endowus and AutoWealth are the only two robo-advisors offering CPFIS access.

Found this article useful? Share it with anyone who wants to invest their CPF.

Related Articles