Higher CPF monthly salary ceiling, Special Account closure for those aged 55 and above, raised Enhanced Retirement Sum (ERS), higher contribution rates for seniors, and more. These are some of the changes to CPF we can expect in 2025. If you’ve heard about these new changes, you may be wondering what all these mean for you.

Understanding how these changes affect you starts with figuring out how CPF works in the first place.

This might take a while as there are different parts to CPF and there are changes all the time. But the good news is that, it’s tedious, but not rocket science. By the end of this article, you’ll know your CPF contribution rates and ceilings, what happens to the money in your CPF accounts, and what you can do with it before and after retirement.

How does CPF work? Guide to CPF in Singapore (2025)

- What is CPF and why do we have it?

- What are the CPF contribution components?

- What are the CPF contribution rates in 2025?

- Did you know there’s a limit to how much you can contribute to your CPF accounts each month?

- What CPF accounts do you have?

- What are the monthly CPF allocation rates in 2025 for these accounts?

- When can you use the money in your CPF accounts?

- What is the CPF Retirement Sum and how does it affect you?

- What’s the difference between the CPF Retirement Sum Scheme and CPF LIFE?

- What are the retirement payouts under the CPF LIFE Scheme?

- What is the CPF interest rate in 2025?

- How to make CPF nominations: What happens to my CPF money after I kick the bucket?

- CPF Calculators

- How to contact CPF

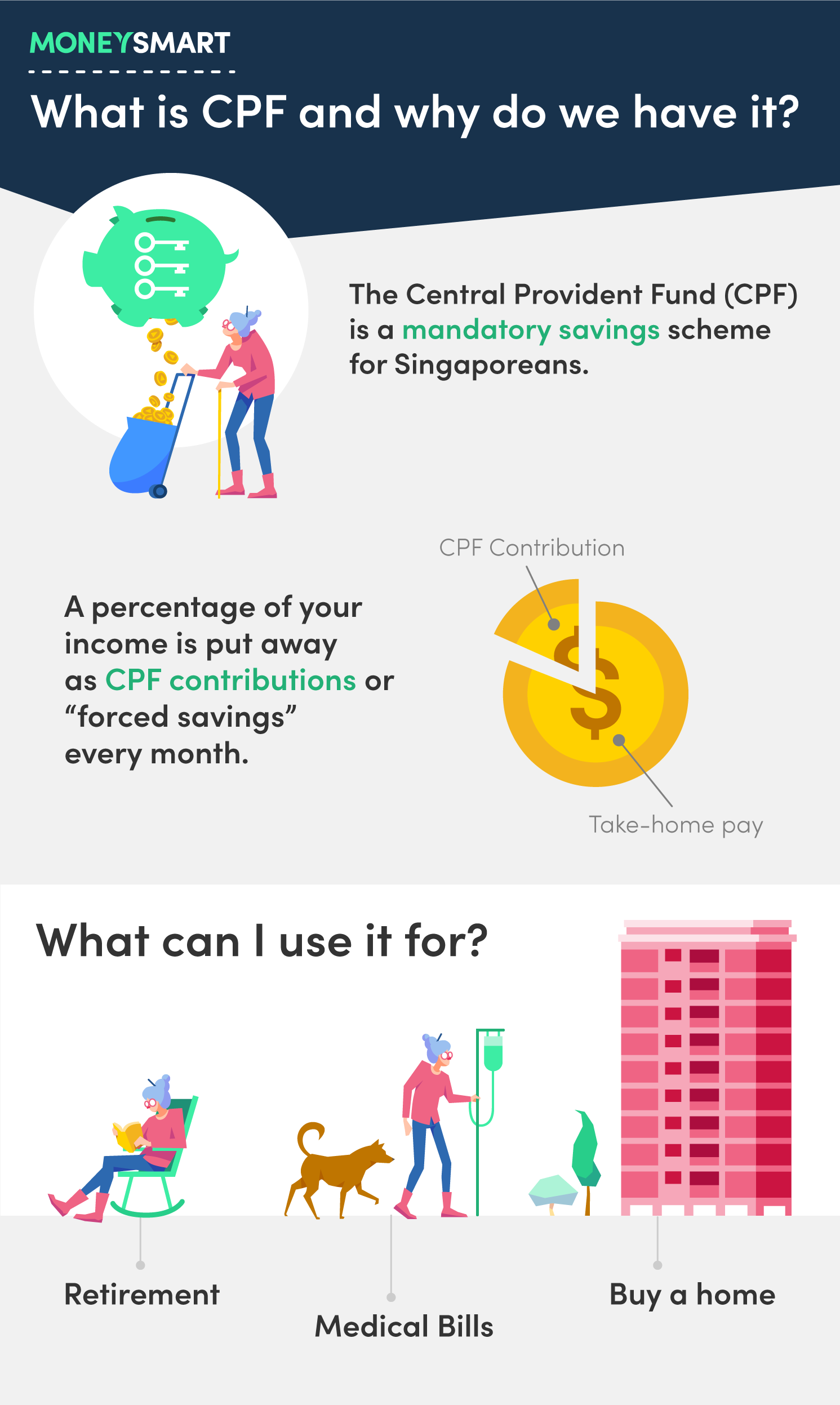

1. What is CPF and why do we have it?

The Central Provident Fund, or CPF, was set up to play one of the most important functions in Singapore’s social security system.

The main purpose of CPF is to ensure that Singaporeans have enough money for retirement, to pay for medical bills when they fall ill, and to buy a home with.

And one of the chief ways these goals are achieved is by forcing people to put away a percentage of their income every month in CPF accounts set up for these purposes.

That’s why, if you’re an employee, your take-home pay is lower than your official salary. A percentage of your salary is automatically deducted as CPF contributions every month and deposited into your CPF accounts.

The rationale is that if Singaporeans weren’t forced to save money in their CPF accounts, some people would spend all their money at once. They'd then be in trouble when the time came to pay for their retirement or medical bills.

CPF also ensures that the home ownership rate in Singapore continues to be relatively high, since it can only be used to pay for home purchases and not rent.

2. What are the CPF contribution components?

For salaried employees who are Singapore Citizens or Singapore Permanent Residents (PRs), your CPF contributions comprise the employee’s contribution (that’s you) and your employer’s contribution. These contributions are made automatically for you.

- Every month, when paying out your salary, your employer is required to declare your wages to the CPF board and withhold the portion of your pay that needs to go into your CPF accounts. That portion will be paid into your CPF accounts as your employee’s contribution.

- In addition to the employee’s contribution, there is also an employer’s contribution. This is the amount your employer is required to pay into your CPF accounts out of their own pocket, above and beyond your stipulated salary.

For employers, you’re obligated to:

These are applicable to your employees who are Singapore Citizens/Singapore PRs and earn more than $50 per month.

You have to do this on a monthly basis, with the due date for CPF contributions being the last day of each month. Don’t be late, or you’ll have to cough up late payment interest at a rate of 1.5% per month for each day after the due date.

3. What are the CPF contribution rates in 2025?

As of 1 Jan 2025, the CPF contribution rates have increased for those aged 55 to 70 who are still working.

This is on top of the increase in CPF Ordinary Wage (OW) ceiling—it it will be increased from $6,000 to $8,000 by 2026, taking place in 4 steps.

Here’s how much each person contributes, by the percentage of the employee’s wage, for Singapore Citizens or Singapore PRs from the third year onwards:

Age of employee | CPF contribution by employer | CPF contribution by employee | Total CPF contribution rate |

Up to 55 years old | 17% | 20% | 37% |

Above 55 to 60 years old | 15.5% (+0.5%) | 17% (+1%) | 32.5% |

Above 60 to 65 years old | 12 (+0.5%) | 11.5% (+1%) | 23.5% |

Above 65 to 70 years old | 9% | 7.5% (+1) | 16.5% |

Above 70 years old | 7.5% | 5% | 12.5% |

From the table above, CPF contribution rates look pretty straightforward, don’t they? But the truth is, they’re not quite so simple.

CPF contribution rates are actually further tiered based on citizenship status (Singapore Citizens vs first year, second year and third year PRs) and total wages. To find out exactly how much will go into you or your employee’s CPF, you can view this comprehensive CPF Contribution Rate table or use this CPF contribution calculator.

By the way, if you’re self-employed, none of the above applies to you. Any CPF contributions are voluntary except Medisave contributions, which you’ll be prompted to pay after filing your taxes each year.

Why did CPF contribution rates increase, and will they keep increasing?

Will CPF contribution rates keep increasing? For those above 55 years old up to 70 years old, and who earn monthly wages of >$750, yes. From 1 Jan 2025, employee and employer contribution rates for workers aged >55 to 70 years old have since increased by an additional 0.5% or 1.5% each, as announced in Budget 2024, to boost their retirement income.

The CPF contribution rate increase in 2025 is all part of the plan to gradually increase CPF contribution rates for older workers from now till 2030 or so. The goal? Hit a 37% total contribution rate for those aged >55 to 70 years by 2030.

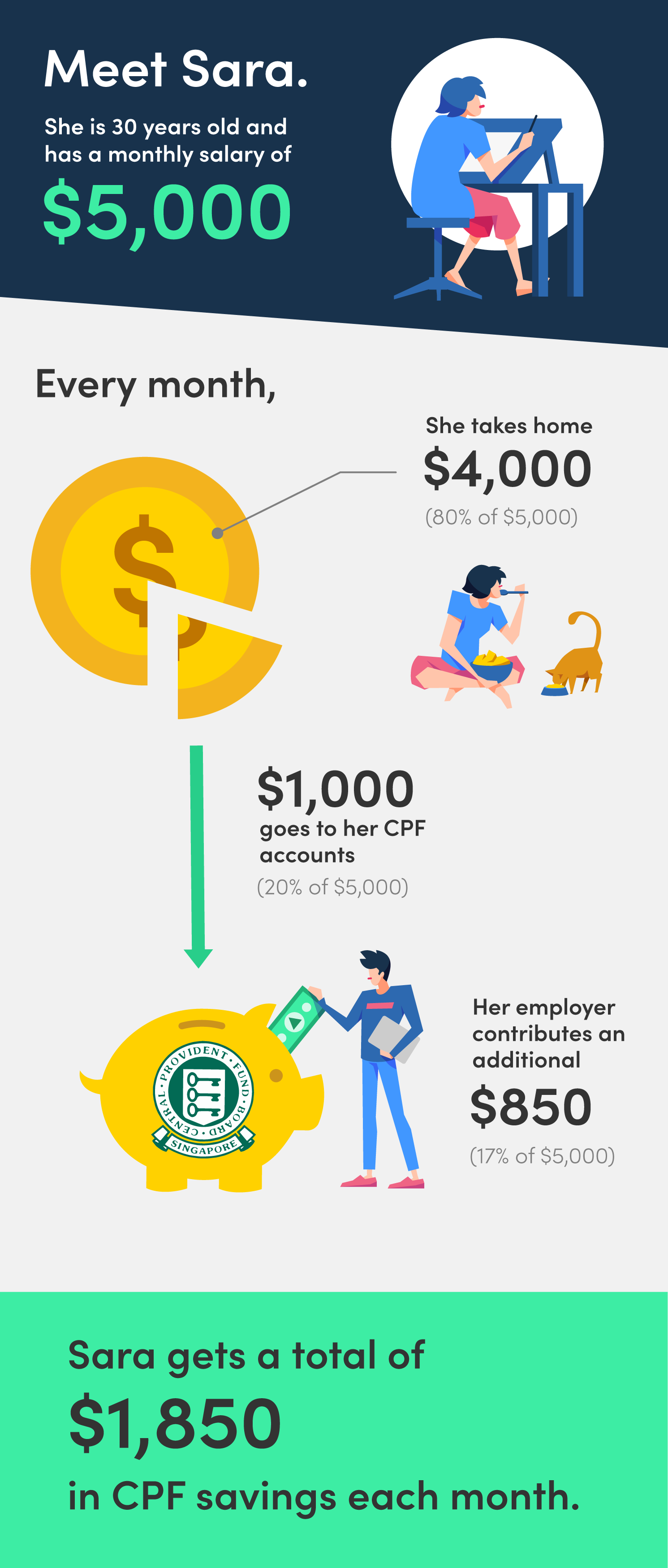

Example

Let’s say you are a 30-year-old earning a monthly salary of $5,000.

Every month, your employee’s contribution to CPF will be 20% of your wage. That means that $1,000 will be deducted from your salary every month and deposited into your CPF accounts.

Your take-home pay after CPF deductions is thus $4,000.

In addition, your employer is forced to make an employer’s contribution to your CPF accounts worth 17% of your salary, which adds up to $850. This is in addition to the $5,000 salary he’s paying every month.

The total amount of CPF contributions going into your account every month is thus $1,850.

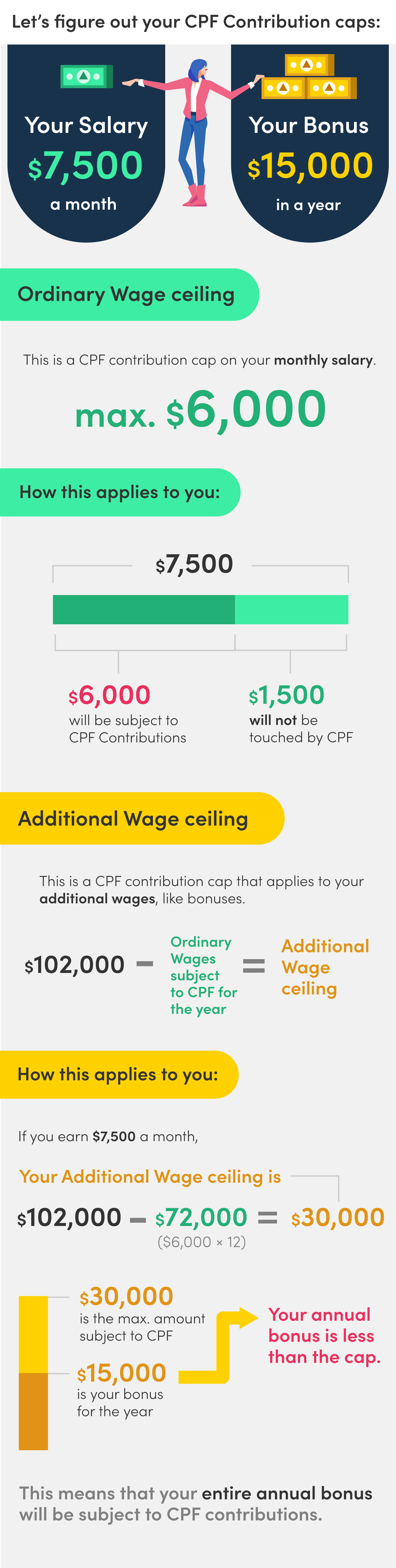

4. Did you know there’s a limit to how much you can contribute to your CPF accounts each month?

This is known as the CPF Wage Ceiling which is a form of CPF contribution cap. There are two parts to this: the Ordinary Wage Ceiling and the Additional Wage Ceiling.

The Ordinary Wage Ceiling is a CPF contribution cap on your monthly salary and is currently capped at $7,400. As part of Budget 2023, the government announced that this cap will increase progressively to $8,000 by 2026.

CPF Ordinary Wage ceiling | CPF annual salary ceiling | |

From 1 Jan 2016 to 31 Aug 2023 | $6,000 | $102,000 (no change) |

From 1 Sep to 31 Dec 2023 | $6,300 (+$300) | |

From 1 Jan to 31 Dec 2024 | $6,800 (+$500) | |

From 1 Jan to 31 Dec 2025 | $7,400 (+$600) | |

From 1 Jan 2026 | $8,000 (+$600) |

Source: CPF

How does the Ordinary Wage Ceiling work? Assuming the cap is $7,400, this means that the first $7,400 of your monthly salary is subject to CPF contributions. Any amount above that won’t have a portion deducted for CPF. It also means your employer doesn’t need to contribute to your CPF account for amounts above $6,800.

The Additional Wage Ceiling is a CPF contribution cap on your additional wages, such as your bonuses. The formula for calculating the Additional Wage Ceiling is [$102,000* – Total Ordinary Wage subject to CPF for the year].

*If you’re wondering why $102,000, that’s 17 months x $6,000, where $6,000 is the Ordinary Wage ceiling.

According to CPF, there is no change to the Additional Wage Ceiling and CPF Annual Limit, which is $37,740 for the latter.

You can use CPF's Additional Wage ceiling calculator to find out how much of your annual salary and bonus will go towards CPF.

Here's an illustrative example, assuming for the sake of easy math that the contribution cap is $6,000.

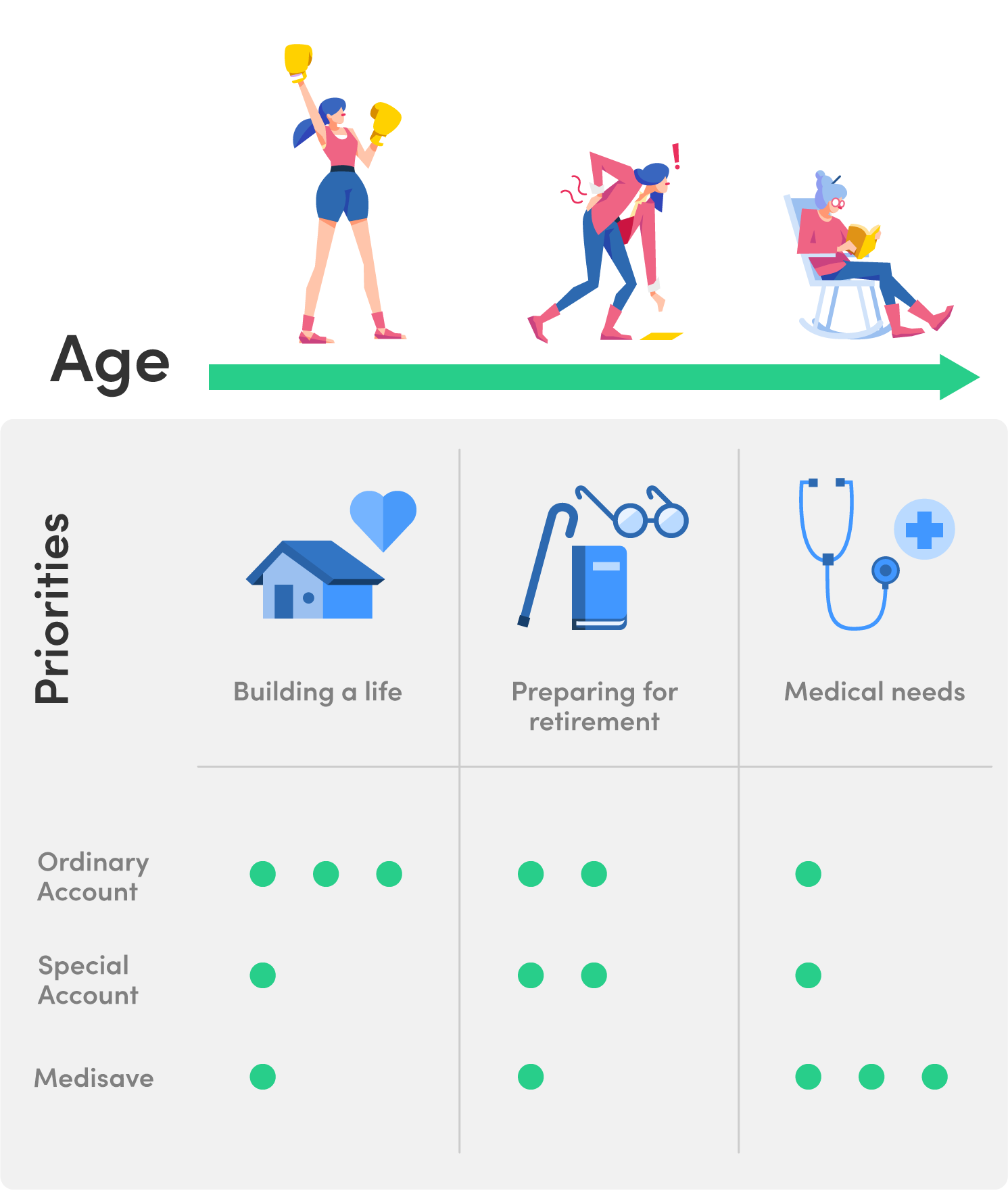

5. What CPF accounts do you have?

All Singaporeans and PRs have the following CPF accounts, which are opened to contain money for several purposes:

CPF account | What you can use it for |

Ordinary Account (OA) | Can be used for housing, higher education, and investing. Anything left over is to be used for retirement. |

Special Account (SA) | To be saved for retirement. Can also be invested to a certain degree. |

Medisave Account (MA) | To pay for hospitalisation, other approved medical expenses and to pay for MediShield / Integrated Shield plans. |

Retirement Account (RA) | The RA provides you with monthly payouts in your later years once you reach a certain payout eligibility age. You only get an RA when you turn 55. At that age, your OA and SA will merge to form your RA, which will contain your retirement savings. |

6. What are the monthly CPF allocation rates in 2025 for these accounts?

By now you should already have a rough idea of how much money goes into your CPF accounts every month. (If you don’t and are too lazy to figure it out, just use the CPF contribution calculator!) You should also know that you have several CPF accounts. So how are your monthly CPF contributions split across your CPF accounts?

Once the money is paid into CPF, it is divided between your various accounts in the following way, as long as your monthly wages are $750 and above. The percentages here refer to the percentage of your total CPF contribution:

Age of employee | CPF allocation for Ordinary Account | CPF allocation for Special Account | CPF allocation for MediSave |

Up to 35 years old | 62.17% | 16.21% | 21.62% |

Above 35 to 45 years old | 56.77% | 18.91% | 24.32% |

Above 45 to 50 years old | 51.36% | 21.62% | 27.02% |

Above 50 to 55 years old | 40.55% | 31.08% | 28.37% |

Above 55 to 60 years old | 36.94% | 30.76% | 32.30% |

Above 60 to 65 years old | 14.90% | 40.42% | 44.68% |

Above 65 to 70 years old | 6.07% | 3.03% | 63.63% |

Above 70 years old | 8.00% | 8.00% | 84.00% |

Source: CPF, correct as of Jan 2025

You’ll notice that when you’re young and strong, more money goes into your OA and less into your MediSave account. This is because you’re presumably more likely to need your OA money to buy housing and less likely to fall seriously ill.

However, as you get older, the allocation rates evolve. More money starts going into your SA in order to prepare you for retirement, as well as your MediSave account, since your healthcare needs are likely to rise.

But once you hit the age of 55, your OA and SA contribution rates fall, since you’ve (hopefully) accumulated enough for retirement. Your MediSave contributions continue to remain high since you’re now older and frailer.

7. When can you use the money in your CPF accounts?

While there is no hard and fast rule as to how to get utility of your CPF accounts before you retire, here are some common ways Singaporeans use that painstakingly-saved cash.

Using the money in your OA to buy a home: Looking for an HDB home or forking out the cash for private property? You can use the money in your OA to pay for part of your property, subject to withdrawal limits and the compulsory cash portion that must be paid. Additionally, you can also use the money in your OA to make your monthly home loan repayments. There are also CPF Housing Grants you can apply for to help defray the cost of your property if you meet certain criteria.

Using the money in your OA to pay for education: The CPF Education Loan Scheme lets you use the money to pay for your or a family member’s tuition fees if taking a full-time subsidised diploma or degree course at local unis, polys or ITEs.

Using the money in your OA and SA to invest: The CPF Investment Scheme lets you use some of the money in your OA and SA for certain investments like shares, Unit Trusts, investment-linked insurance, Singapore Government Bonds and ETFs. Of course, there’s no guarantee that you’ll be able to beat CPF’s interest rates.

Using the money in your MediSave account to buy an Integrated Shield plan: Integrated Shield plans, which are private health insurance plans meant to boost your MediShield Life, are highly recommended if you can afford it. Part of the premiums can be paid for with MediSave.

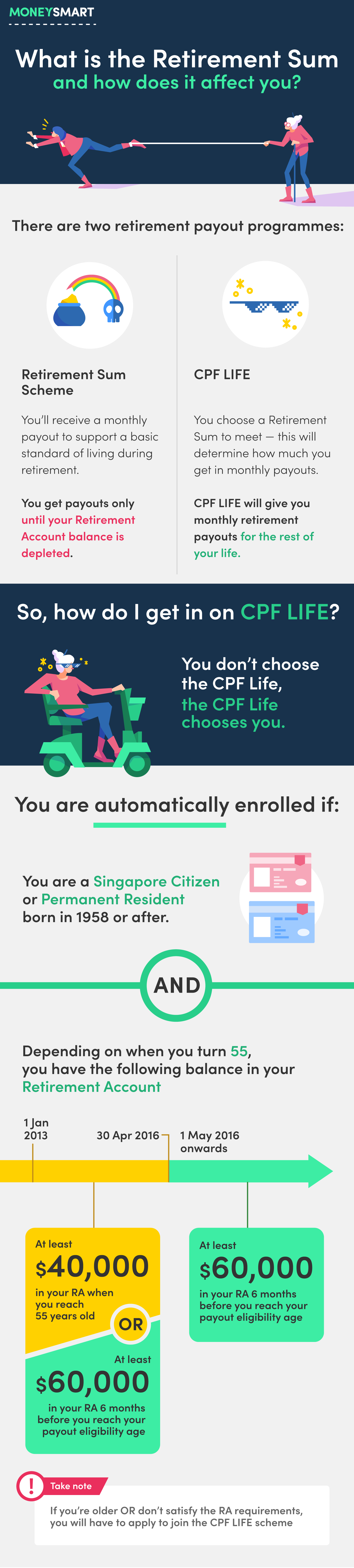

8. What is the CPF Retirement Sum and how does it affect you?

You’ve probably heard mutterings about this evil thing called the CPF Retirement Sum, and how it’s getting higher every year. It used to be called the CPF Minimum Sum, which both upset and confused Singaporeans, and so the decision was made to rename it to the CPF Retirement Sum.

But what the heck is it really, and how does it affect you?

When people are talking about the dreaded CPF Retirement Sum, they’re usually referring to 1 of 3 Retirement Sums. Why are there 3? Think of these 3 Retirement Sums as targets to hit in order to receive certain monthly payouts once you turn 65.

When you turn 55, your OA and SA will merge to form your Retirement Account (RA). You will be able to withdraw a lump sum, leaving the Retirement Sum behind in your RA. This sum forms your retirement income, and will be doled out to you in monthly payouts starting from the age of 65 to 70 years (you can decide when exactly between those years).

If the money you set aside in your RA meets the Basic Retirement Sum (BRS), your monthly payouts from 65 onwards will cover your basic living expenses. However, don’t expect a ton of room for indulgence in your retirement years.

The next tier is the Full Retirement Sum (FRS), which is 2 times the BRS, followed by the Enhanced Retirement Sum (ERS), which is 3 times the BRS.

As of 1 Jan 2025, the ERS is 4x the BRS. This means the is now $426,000, up from $308,700 last year. It will continue to increase till 2027:

Year | 2024 | 2025 | 2026 | 2027 |

Enhanced Retirement Sum | $308,700 | $426,000 | $440,800 | $456,400 |

If the money in your retirement account meets the FRS or ERS, you’ll receive higher monthly payouts.

Budget 2024 announced that from early 2025, the Special Account (SA) will be closed for those aged 55 and above. What happens is:

- What’s in the SA will be transferred to the RA up to the FRS — these can’t be withdrawn and will continue to earn the long-term interest rate

- The balance amount in the SA will be transferred to the OA — these can be withdrawn and will earn the short-term interest rate

So if you’re planning on withdrawing money from your CPF once you turn 55, do factor in how much you need to leave in there to meet the BRS, FRS or ERS.

How much money can you withdraw in a lump sum when you turn 55 anyway?

- If you have met the Full Retirement Sum in your CPF, you can withdraw everything else remaining in your Special and Ordinary Accounts if you wish.

- If you have not met the FRS but own property with a lease that will last you until you’re 95, you only have to leave the Basic Retirement Sum in your CPF. You can withdraw the rest.

Regardless of which sum applies and how much excess you have, you’re allowed to withdraw at least $5,000 at age 55.

9. What’s the difference between the CPF Retirement Sum Scheme and CPF LIFE?

While both are retirement payout programmes, the CPF Retirement Sum Scheme gives payouts until your CPF balance runs out, while CPF LIFE gives you payouts for as long as you live—yes, even if your age hits 3 digits. Let’s take a closer look at these schemes.

The older CPF Retirement Sum Scheme requires you to have a minimum amount in your CPF accounts when you retire. This is to ensure you receive monthly payouts that can support a basic standard of living until the money in your CPF runs out.

Under the CPF Retirement Sum Scheme, how much you get each month depends on how much you have in your RA. Provided you have enough CPF balance, the monthly payouts start at $350 a month.

The newer CPF LIFE (Lifelong Income For The Elderly) scheme will give you monthly payouts for the rest of your life. So you don’t have to worry about outliving your CPF savings if you become immortal… so long as you are able to accumulate enough before starting your payouts.

Singaporeans will be automatically enrolled in CPF LIFE, as long as they fulfil the following conditions:

Factor | Automatically enrolled in CPF LIFE? |

Citizenship | Singapore Citizen or PR |

Birth year | 1958 or after |

CPF RA balance | At least $60,000 when you start your monthly payouts |

Those who don’t satisfy the RA requirements can apply to join the CPF LIFE scheme if they wish any time from 65 to one month before you turn 80 by logging into the my cpf Online Services website and submitting an online application.

You can choose to start receiving your monthly payouts between the ages of 65 and 70. If you don’t inform the CPF Board that you’d like to start monthly payouts, they will start giving them to you when you reach 70 years old anyway.

10. What are the retirement payouts under the CPF LIFE Scheme?

Your monthly payouts when you turn 65 will depend on whether the amount you’ve accumulated in your RA meets the Basic, Full or Enhanced Retirement Sum (whichever is highest).

As you can probably imagine, the rising cost of living makes it necessary to raise the CPF Retirement Sums every year. The ERS is now $426,000 in 2025, and is set to increase gradually in the next few years..

Here are the retirement sums for Singaporeans/PRs who turn 55 up till 2027:

Year of 55th birthday | Basic Retirement Sum (BRS) | Full Retirement Sum (2x the BRS) | Enhanced Retirement Sum (3x the BRS) |

2023 | $99,400 | $198,800 | $298,200 |

2024 | $102,900 | $205,800 | $308,700 |

2025 | $106,500 | $213,000 | $426,000 |

2026 | $110,200 | $220,400 | $440,800 |

2027 | $114,100 | $228,200 | $456,400 |

Source: CPF

Have a monthly payout sum in mind for your retirement? Here’s a guide to how much you’ll need to have saved by 55, 60, and 65 years old in order to receive your desired monthly payout.

Desired Monthly Payout from 65 | Savings You Need at 65 | Savings You Need at 60 | Savings You Need at 55 |

$540 - $570 | $97,300 | $75,900 | $60,000 |

$860 - $930 | $164,800 | $131,400 | $106,500 |

$1,170 - $1,250 | $227,900 | $183,300 | $150,000 |

$1,610 - $1,730 | $319,400 | $258,500 | $213,000 |

$3,100 - $3,330 | $628,600 | $512,700 | $426,000 |

Source: CPF LIFE Payout Examples

These payouts will continue all your life, even if you end up living a crazy long life and your account runs out of money.

11. What is the CPF interest rate?

As you might know, leaving your cash in a bank account means that its value will erode over time, since bank account interest rates tend to be so pathetic that they probably can’t effectively hedge against inflation.

The money in your CPF accounts earns interest, too, but thankfully at much better rates than your typical bank account. At the moment, the CPF interest rates are as follows:

Account name | Current interest rate | |

Age below 55 years | Age 55 years and above | |

Ordinary Account | 2.5% p.a. | 2.5% p.a. |

Special Account | 4% p.a. | 4% p.a. |

MediSave Account | 4% p.a. | 4% p.a. |

Retirement Account | NA | 4% p.a. |

As you can see, your SA offers a much higher interest rate than the OA. That's why one way to get a much better interest rate on your OA savings is to transfer money from your OA into your SA.

The catch, obviously, is that once your money goes into your SA, you can’t transfer it back into your OA. As you can’t use the money in your SA to buy property or pay for education, the chief purpose of that money can only be for retirement.

So before making any transfers from OA to SA, make sure you absolutely do not need the money for housing or education.

You can also earn extra interest on the first $60,000 of your combined account balances (with up to $20,000 from your OA). This is basically to encourage you to keep your money in your CPF account, and to maximise it by leaving it in your SA or RA:

Age | Extra interest on combined CPF account balances |

Below 55 years old | 1% p.a. on first $60,000 (capped at $20,000 for OA) |

55 years old and above | 2% p.a. on first $30,000, 1% per annum on next $30,000 (capped at $20,000 for OA) |

Just in case you’re thinking of gaming your CPF contribution and earning loads of interest, note that there is an Annual Limit to how much you can contribute. The maximum CPF contribution is known as the Annual Limit, and is currently set at $37,740.

12. How to make CPF nominations: What happens to my CPF money after I kick the bucket?

That cash in your CPF accounts is your money, you say. So when you die, you should be able to will it to whomever you like, right?

Well, here’s news for you: the money in your CPF account cannot be distributed through a will. So even if you write a beautiful will bequeathing all your assets to the SPCA, it will not apply to your CPF savings.

To work around that, the CPF Nomination Scheme lets you specify who will receive your CPF savings when you die, and how much.

To make a nomination, you simply have to submit a CPF Nomination Form with all the necessary supporting documents. It can be submitted in person at a CPF Service Centre after booking an appointment, or by post.

Don’t panic; your CPF money won’t vanish if you didn’t make a nomination. The Public Trustee’s Office will distribute your money to your next-of-kin (according to the law of intestacy). However, the Office will charge a fee for this administrative work.

ALSO READ: Estate Planning Checklist—7 Important Things to Settle Before You Die

13. CPF Calculators

Still not sure how much CPF money you should be receiving or how much you can use?

These CPF calculators do the job for you.

- CPF Contribution Calculator (for Singapore Citizens and PRs in their 1st, 2nd, or 3rd year and onwards)—Check how much your CPF contributions are supposed to be.

- CPF Contribution Allocation Calculator—Check how your CPF contributions are split between your Ordinary, Special and MediSave accounts.

- CPF LIFE Payout Estimator—If you’re between the age of 55 and 79, estimate how much you can receive in monthly retirement payouts.

- CPF Housing Usage Calculator—Find out how much money from your Ordinary Account you can use to pay for your home.

- Self-Employed Medisave Contribution Calculator—For self-employed folks to check how much they need to fork out for Medisave.

- Retirement Payout Planner—Figure out if you're on track for the retirement lifestyle you want with this simple financial planning tool.

14. How to contact CPF

If you have any problems, it's easy to get in touch with CPF online.

Through my cpf digital services: Use your Singpass to log into my cpf digital services. From there, you can access information about your CPF account including your account balance.

Submit online form: Alternatively you can submit an enquiry via the webform here.

CPF hotline: CPF has 3 main hotlines you can call:

- For enquiries on member enquiries, e.g. retirement, housing, nomination:

- 1800-227-1188 (within Singapore)

- +65-6227-1188 (from overseas)

- For enquiries on healthcare, e.g. MediSave, MediShield Life or CareShield Life:

- 1800-222-3399 (within Singapore)

- +65-6222-3399 (from overseas)

- For employer-related enquiries, e.g. CPF contribution rates and e-submission:

- 6220-2340 (for local calls)

- +65-6220-2340 (from overseas)

Operational hours:

- Monday to Friday (except public holidays), 830 am – 530pm

- Eves of Christmas, New Year and Chinese New Year, 830 am – 1pm

Visit in person: If all else fails, you can make an appointment to visit the CPF Service Centres in Maxwell, Bishan, Tampines, Jurong or Woodlands. Do make your appointment at least a day in advance, and note that services for employers and self-employed are not available at the service centres.

Found this article useful? Share it with anyone else who needs to understand CPF.

Related Articles