Did you know Singapore is a "blue zone"? The term was coined by Dan Buettner, an American National Geographic Fellow and New York Times-bestselling author. It refers to places that have 10 times more centenarians (people that live to 100) compared to the USA. In fact, according to data from the World Bank, Singapore has one of the highest life expectancies at birth in the world.

Given these statistics, it's natural to look forward to your golden years, right? Well, not exactly. If you're in your 30s like I am, retiring in Singapore is the stuff of nightmares. With inflation, rising house prices and the fact that Singapore is the most expensive city in the world to live in, who knows how much even our "cheap" hawker food and kopi will be by then? What will life be like then, and how can we afford it?

This is why it's really important for us to understand CPF LIFE, which is the default retirement plan for Singaporeans. In fact, it's probably the only retirement plan for some people. (Having kids and hoping they’ll be filial to you doesn’t count.)

Let’s find out what CPF LIFE is all about, what you need to join the scheme, and what the payouts are like. Warning: It's a long read.

Disclaimer: All information is from CPF's website and correct at the time of publishing.

What is CPF LIFE? Understanding Payouts, Plans & Minimum Sums in 2024

- What is CPF LIFE? How is it different from CPF Minimum Sum?

- Who is eligible for CPF LIFE? How do you sign up?

- What's the minimum sum required to join CPF LIFE?

- Hang on, what about the CPF Retirement Sum?

- How much CPF LIFE payouts will you get?

- Which CPF LIFE plan should you choose?

- What if you want higher CPF LIFE payouts?

- What happens to your CPF LIFE when you die?

- Is it possible to opt out of CPF LIFE?

- Can you supplement CPF LIFE with your own plan?

1. What is CPF LIFE? How is it different from CPF Minimum Sum?

CPF LIFE (Lifelong Income For the Elderly) is the current incarnation of the Central Provident Fund’s retirement scheme. Previously, the retirement scheme was called the CPF Minimum Sum Scheme, later renamed as the CPF Retirement Sum Scheme.

The old scheme is being phased out, so CPF LIFE will be the default scheme for most of us.

But in case you're curious...

The older CPF Retirement Sum Scheme draws its payout from your CPF Retirement Account (RA), essentially treating it as a retirement fund. But this means your payouts will stop when your account balance dwindles to $0. Those on the CPF Retirement Sum Scheme will receive a minimum of $350 in monthly payouts, but these payouts will end by age 90.

CPF's new scheme, CPF LIFE, works differently.

First, you need to pay a lump sum premium, deducted from your RA, when you join the scheme. This means there’s a chance your Retirement Account will be depleted right from the start.

On the other hand, as the “Lifelong” bit suggests (the L in LIFE), your retirement payouts will never stop.

In short, CPF LIFE is a much more attractive retirement scheme for the simple reason that you just don’t know how long you’ll live. So even if you live to be over 100, you can rest easy in your retirement knowing you won't run out of money.

2. Am I eligible for CPF LIFE? How do I sign up?

Can't wait to sign up for CPF LIFE? Chill out. There's no need to look for a sign-up link frantically, because, guess what, you'll be automatically enrolled in the scheme!

Anyone who meets these criteria will be auto-enrolled in CPF LIFE:

- Singapore Citizen or Permanent Resident

- Born on 1 January 1958 and after

- At least $60,000 in your CPF retirement savings before age 65

If you’re not automatically placed on CPF LIFE for some reason, you can still opt in for CPF LIFE anytime from age 65 to 79. (Yes, even if you’ve already started receiving Retirement Sum payouts!) Here's how:

- Login to my cpf Online Services with your SingPass

- Select My Requests > CPF LIFE > Apply for CPF LIFE

- The cut-off date is 1 month before your 80th birthday

3. How much CPF savings do I need to join CPF LIFE?

Here's where things get slightly complicated.

There is no minimum amount of CPF savings you need to join CPF LIFE. I repeat: There is no minimum sum required to join CPF LIFE.

But if you join CPF LIFE with only a small amount of CPF savings, you'll get correspondingly small monthly payouts. Which may defeat the purpose of a retirement plan.

Here's a table from CPF that illustrates this. Let's say you join the scheme at age 65 with $97,300 in your account. Your estimated monthly paycheck is just $540 to $570—not exactly comfortable...

Desired Monthly Payout from 65 | CPF Life Premium at 65 (Savings you need at 65) | Savings you need at 60 | Savings you need at 55 |

$540 – $570 | $97,300 | $75,900 | $60,000 |

$840 - $900 | $159,600 | $127,100 | $102,900 |

$1,170 - $1,250 | $227,900 | $183,300 | $150,000 |

$1,560 - $1,670 | $308,900 | $249,900 | $205,800 |

$2,280 - $2,450 | $458,300 | $372,700 | $308,700 |

Source: CPF. Note: The calculations above are estimates based on the CPF LIFE Standard Plan and assume you'll turn 65 in 2034, computed as of 2024.

So, while there's technically no minimum amount to join, CPF LIFE is really only worthwhile if you have enough CPF savings to fund the retirement payouts you want.

Use the CPF LIFE Estimator to calculate the amount you need, then top up your Retirement Account before you join.

Don't worry. The payouts are pro-rated, so you won't rugi. No need to fret about hitting this or that tier macam trying to hit minimum credit card spends each month.

4. Can I withdraw the rest of my CPF?

There's no minimum required to join CPF LIFE... but there IS a minimum sumyou cannot touch when you reach age 55. Meaning you cannot withdraw your CPF savings to buy a private island. Sorry.

This "can-see-but-cannot-touch" money is called the CPF Retirement Sum. Actually there are 3 Retirement Sums: Basic, Full (Basic x 2), and Enhanced (Basic x 3, to be increased to 4x the Basic sum from 2025). They increase every year. Here's a table showing the current sums for those turning 55 soon:

Year of 55th birthday | Basic Retirement Sum (BRS) | Full Retirement Sum (FRS) | Enhanced Retirement Sum (ERS) |

2024 | $102,900 | $205,800 | $308,700 |

2025 | $106,500 | $213,000 | $426,000 |

2026 | $110,200 | $220,400 | $440,800 |

2027 | $114,100 | $228,200 | $456,400 |

So how much can you withdraw from your CPF then?

If you own a home in Singapore and used CPF savings to purchase it

You can withdraw CPF savings down to your Basic Retirement Sum if:

- You are 55 and above

- The property's lease will last you up to age 95 or older

- The expected CPF housing refund is able to top up your retirement account back to the FRS when you sell/transfer the property in the future; OR you pledge your property to secure the refund.

So if you're 55 this year with $200,000 in CPF, you can withdraw up to $200,000 - $102,900 = $97,100.

If you own a home in Singapore and did NOT use CPF savings to purchase it

You can withdraw CPF savings down to your Basic Retirement Sum if:

- You are 55 and above

- The property's lease will last you up to age 95 or older

- If you sell your home in the future, you must top up your retirement account back up to the FRS. You'll need to pledge your property to secure this.

Source: CPF

So if you're 55 this year with $200,000 in CPF, you can withdraw up to $200,000 - $102,900 = $97,100.

If you DO NOT own a home

- You can withdraw CPF savings as long as you leave the Full Retirement Sum untouched. That means if you turn 55 in 2024, you have to set aside $205,800 and can withdraw anything above that.

Whether or not you own a home

If you were born in 1958 or later...

- At age 55: If you have less than the Basic Retirement Sum in your account, you can withdraw up to $5,000.

- At age 65: You can withdraw up to 20% of your retirement savings. But this excludes the $5,000 at age 55 as well as any cash top-ups, CPF transfers or government grants.

CPF terms these unconditional withdrawals.

5. How much CPF LIFE payouts will I get when I retire?

Now let’s move on to how much you can actually get from CPF LIFE and when you can actually see the money.

First, I need to emphasise that you will only start getting CPF LIFE payouts from age 65 (you can defer this payout age up to age 70). So if you retire before 65, you'll need some kind of income stream until then.

With that out of the way, CPF LIFE payouts simply depend on 2 variables:

- Your CPF Retirement Account balance

- Which CPF LIFE plan you choose

Point 1 is straightforward. The more you have in your CPF, the higher your payouts. See the CPF LIFE payout table again to view the payouts you can receive each month from age 65 onwards for any given amount of retirement savings.

If you're not retiring anytime soon, it's better to use the CPF LIFE Estimator to calculate your expected payouts, since they change every year. You can also put in your desired monthly payout and it will tell you how much you need to have in your RA to get that. Nifty.

Now, on to point 2...

6. CPF LIFE Standard vs Escalating vs Basic plans: which is better?

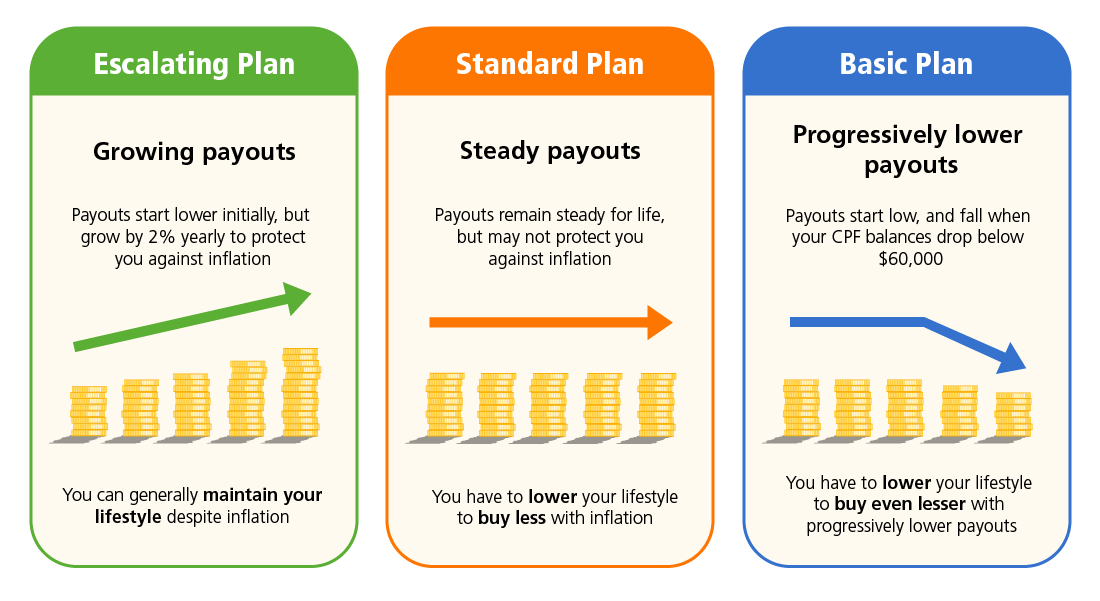

Image: CPF

Yes, there are different CPF LIFE payout plans! Mind blowing, huh?

1. CPF LIFE Standard Plan

- 100% of your RA savings will be used to pay a lump sum CPF LIFE premium when you join

- You then receive stable monthly payouts for life. Even after your premium has been depleted, CPF will continue handing you the same monthly payout using interest that you and other CPF LIFE members have accumulated.

- At first, payouts start higher than the Escalating Plan. But because the Escalating Plan payouts increase over time, the Standard Plan payouts will eventually become lower than those for the Escalating Plan.

- This is the simplest plan to understand and therefore the default plan we normally see in CPF LIFE illustrations. But it's not the only plan!

2. CPF LIFE Escalating Plan

- 100% of your RA savings go into the lump sum CPF LIFE premium when you join CPF LIFE between the age of 65 and 70

- Payouts start out lower than that of the Standard Plan.

- Every year, they increase by 2% to keep pace with inflation, eventually overtaking that of the Standard Plan. For example if you start with a monthly payout of $1,000 when you turn 65, the 2% increase each year will mean you'll be earning around $1,500 when you hit 85.

3. CPF LIFE Basic Plan

- Only 10-20% of your RA savings is deducted for the CPF LIFE premium. This will be used to provide payouts from age 90 for the rest of your life.

- The bulk 80-90% of your RA savings will directly fund your monthly payouts you turn 90.

- Once your RA falls below $60,000, your monthly payout will decrease.

- This is a "legacy" plan. CPF is nudging Singaporeans on this plan to switch to the newer Standard or Escalating Plans anytime if they want to have level or increasing payouts that will help with rising costs of living. Coupled with the fact that you can't change back to the Basic Plan once you make the switch, this makes me think that it might be phased out eventually.

Which one to choose? Well, if inflation is a big concern to you, it's a no-brainer to choose the Escalating Plan if you can. It's tough enough having to cope with inflation while you're working—just imagine what it'd be like in old age. No thanks!

I can only think of 2 problems with the Escalating Plan. Firstly, the starting payout is significantly lower than that of the Standard Plan payouts. If you’re going for this, you'll want to pump more money in your RA to afford a decent standard of living.

Secondly, touch wood but what if you don't live that long? That extra money that you could have gotten each month to enjoy your life's comforts in your retirement years would kinda have been wasted. At least nominate beneficiaries to receive your excess CPF LIFE money after you pass on. Read more about that below.

In any case, choose carefully because you can only switch plans within 30 days of joining the scheme. To request a change within the 30-day timeframe, request it on the CPF website via My Mailbox.

7. What if I want higher CPF LIFE payouts?

If you’ve done the calculations and found your projected CPF LIFE payouts rather dismaying, there are 2 ways to boost them from within CPF.

1. Top up your CPF Retirement Account

Remember: The higher your RA balance, the higher your CPF LIFE payouts. You can increase your retirement income by topping up your RA with cash, up to the Enhanced Retirement Sum (currently $308,700).

Don't worry—you can even do this after CPF has already deducted the premium for CPF LIFE. Top up your CPF LIFE premium online via cash top-ups or CPF transfers to your RA.

2. Defer CPF LIFE payout date

By default, we start receiving CPF LIFE payouts at age 65. To increase your payouts, you can defer the payout starting date up to age 70.

This gives your retirement savings up to 5 more years to grow in your CPF. You end up with a larger lump sum premium which, in theory, results in larger payouts.

To defer your CPF LIFE payout date, use the Plan my monthly payouts service.

If you have exhausted these options or are unwilling to pursue them, we have some more options in the final section—scroll down.

8. What happens to my CPF LIFE when you die?

Receiving monthly payouts for life sounds very well and good, but what if you die shortly after you start receiving CPF LIFE payouts?

Apart from the tragedy of dying while there’s so much life ahead of you, there’s also the matter of what happens to the payouts you were supposed to get.

Before you start posting on Facebook about the evils of CPF—no, CPF won’t just quietly absorb everything and put it towards nation building.

Instead, CPF will refund the unused portion of your annuity premium back into your CPF account. This amount, along with any CPF Retirement Account savings left over, will be bequeathed to your CPF nominee(s) in cash (by default) or their CPF (if you so choose). So while you're still here, nominate your beneficiaries!

If you haven’t made any CPF nominations at the point of death, the money goes to your next-of-kin according to Singapore’s intestacy laws.

9. Can I opt out of CPF LIFE?

Most of us will be automatically placed on CPF LIFE once we retire, whether we like it or not. Is there any way to opt out of the scheme?

Yes, you actually can—if you buy your own retirement insurance (a.k.a. private annuity) plan. In fact, you can be exempted from the CPF Retirement Sum as well.

But not just any plan will do. To apply for exemption:

- You must be age 55 and above

- Your private annuity must give you lifelong monthly payouts

- The annuity can be paid using cash or under CPF Investment Scheme

- The monthly payouts need to meet certain benchmarks (example: a 55 y/o male must receive $1,534/month from the private annuity to be fully exempted)

- You may be fully or partially exempted depending on how much payouts you get

Otherwise, you can only leave CPF LIFE under the following circumstances:

- You have a reduced life expectancy due to a medical condition or you have a severe medical condition that makes you permanently unfit for work or permanently lack mental capacity.

- You are not a -Singapore Citizen or a non-Permanent Resident and have closed your CPF account.

If you successfully leave the scheme, CPF will refund the unused portion of your CPF LIFE premium minus any monthly payouts you’ve already received.

10. How to supplement CPF LIFE with my own retirement plan?

There is a maximum for CPF LIFE: It's pegged to the Enhanced Retirement Sum ($308,700 this year). So for those who are 55 this year, the highest CPF LIFE payout is $2,260 a month based on the CPF LIFE Estimator.

And that's for the Standard plan. If you opt for the Escalating plan, it will be even lower.

If you're used to a $3,000/month lifestyle and have no intention of downsizing your life, living on CPF LIFE payouts alone might be tough. Here are a couple of ways to supplement your retirement income:

Retirement insurance/annuity

As mentioned above, private annuities are basically like CPF LIFE but with private providers. You can get one without applying for CPF LIFE exemption—CPF has absolutely no problem with that. In that case, you can enjoy 2 retirement income streams.

You can tailor the plan depending how much much income you’d like to receive. Plus you might be able to fund your private annuity with y0ur SRS account or under the CPF Investment Scheme, which reduces your out-of-pocket expenses.

Your own investments

If your objective is just to increase your retirement income but not to get exempted from CPF LIFE, then you can also look beyond annuity plans.

Any kind of investment would work as a CPF LIFE supplement, as long as it's stable enough to provide steady income. For example, lots of Singaporeans like receiving dividends from local blue chip stocks or Singapore REITs. You can even park your funds in a diversified ETF like the S&P 500 and start investing with as little as $1,000.

Not keen on DIYing your own retirement plan? There are also robo advisors, unit trusts, insurance products and many more. The sky is the limit.

Found this article useful? Share it with someone who needs it.

Related Articles