Banks love their fine print—and savings accounts are no exception. Many accounts dangle attractive interest rates, but only if you maintain a minimum monthly balance, usually $1,000 (like the UOB One) or even $3,000 (like the OCBC 360). Slip under that threshold and you’ll get slapped with a fall-below fee.

That’s why accounts with no minimum balance are such a lifesaver. They’re simpler, more flexible, and let you spend your money without worrying about unexpected fees.

After all, paying fall-below fees on a savings account feels as silly as paying annual fees for a credit card (which, by the way, you should never do. Get your annual fees waived!). If there are credit cards with no annual fees, you might be wondering if there are savings accounts with no fall-below fees. It only makes sense, right?

Right. Here’s our roundup of the best savings accounts in Singapore that give you no minimum balance, no fall-below fees, and maximum liquidity.

Best savings accounts in Singapore with no minimum balance, no fall-below fees

- Best savings accounts in Singapore with no minimum balance

- Citibank Basic Banking Account

- DBS My Account

- DBS Multiplier Account

- Maybank SaveUp Account

- OCBC FRANK Account

- RHB High Yield Savings Plus Account

- Standard Chartered Basic Bank Account

- Standard Chartered JumpStart Account

- Standard Chartered SuperSalary Account

- Trust Savings Account

- Why does “no minimum balance” mean different things?

1. Best savings accounts in Singapore with no minimum balance

Here are the savings accounts with no minimum balance in Singapore.

Savings account | Minimum balance (age limit) | Monthly service fee | Interest rate |

Citibank Basic Banking Account | $0 (all ages) | $2 (fixed) | – |

DBS My Account | $0 (all ages) | $0 (eStatements) $2 (paper statements) | – |

DBS Multiplier | No fall-below fees until 29 | $0 if under 29 | Up to 1.8% p.a. with salary credit ($2,500) + $200 card spend |

Maybank SaveUp Account | $0 until 25 | $0 until 25 | Base 0.25% p.a. |

OCBC FRANK Account | $0 until 26 | $0 until 26 | 0.05% – 0.2% p.a. |

RHB High Yield Savings Plus Account | $0 (all ages) | $0 | 1.20% – 1.50% |

Standard Chartered Basic Bank Account | $0 (all ages) | $2 (fixed) | None |

Standard Chartered JumpStart Account | $0 (ages 18–26 only) | $0 | 1% p.a. (up to $50k) + 1% p.a. with investment (max 2% p.a.) |

Standard Chartered SuperSalary Account | $0 (all ages) | $0 | 0.01% p.a. |

Trust Savings Account | $0 (all ages) | $0 | 0.50% p.a. – 2.50% p.a. |

By the way, PSA: If you’re looking for your super old school POSB passbook account, it’s not in this list because it actually comes with a minimum balance. If you’re not in the habit of checking your bank statement and transactions a couple of times per month, now is the time to check if you’ve been continually charged a $2 fall below fee!

ALSO READ: Best Savings Accounts in Singapore with the Highest Interest Rates

2. Citibank Basic Banking Account

The Citibank Basic Banking Account suits lower income individuals earning a monthly salary below $2,000. With this basic savings account, you get the usual ATM card with free cash withdrawals, monthly statements, free Citibank Global Transfers, and other banking services.

You don't need to meet any minimum balance, and likewise don't need to pay any fall-below fee. You do, however, need to pay $2 every month as an account maintenance fee. After all, you do need to pay the people who make your iBanking, ATM card services run smoothly.

3. DBS My Account

Most of the basic savings accounts from POSB and DBS (those old passbook accounts?) come with minimum balances of $500, $1,000, or higher. If you’ve drained your childhood account and left it aside to die a slow death, beware! You may have been charged $2 fall below fees monthly.

The only DBS account without fall-below fees is their most basic account, DBS My Account. This account is free and easy, with no age restrictions, account fees, minimum balance, initial deposits, or service charge. It’s also a multi-currency account that gives you access to 13 currencies and—you guessed it!—no FX conversion fees. Noice.

One small caveat: you do get charged a $2 account fee if you insist on receiving your statements on paper. But why would you? Just go for eStatements to enjoy $0 account fees.

The biggest downside is that DBS My Account doesn’t give you interest. If you’re after interest, check out our next DBS account below.

4. DBS Multiplier Account

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 4.10%

- Min. Balance

- S$3,000

The DBS Multiplier Account technically comes with a minimum balance of $3,000, but the service charge if you fall under this figure is waived for those under 29 years old. Otherwise, you have to pay $5 each month.

First let’s look at what the DBS Multiplier offers. With the DBS Multiplier, you can earn up to 4.1% p.a. if you credit your salary and make transactions on your account:

Image: DBS

However, you need to see a whopping $30,000 go in or out of your account each month to unlock 4.1% p.a. Yikes!

So what DBS has done is make an exception for younger people to enjoy the DBS Multiplier benefits without its requirements. If you are 29 years old and below, you earn 1.50% p.a. on your first $50,000 with any credit card or PayLah! spend.

If you are a young adult just getting started, consider the DBS Savings Account for Fresh Grads and Young Adults programme which comes with 1.8% interest. Essentially, it’s a DBS Multiplier account with young adult perks. Like the DBS Multiplier, fall-below fees are waived till age 29.

Credit salary to this account (min. $2,500)

+

Spend $200 a month on DBS/POSB credit card

=

1.8% interest

Do note that after you hit 29 years old, you’ll be smacked with the full requirements of the DBS Multiplier account—minimum balance included.

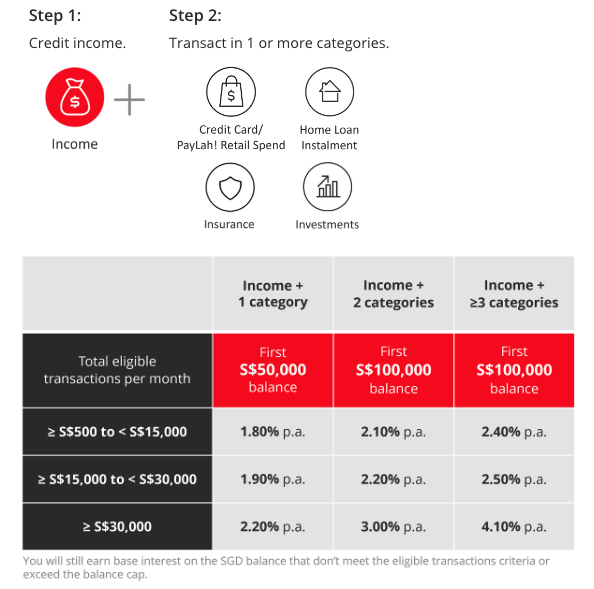

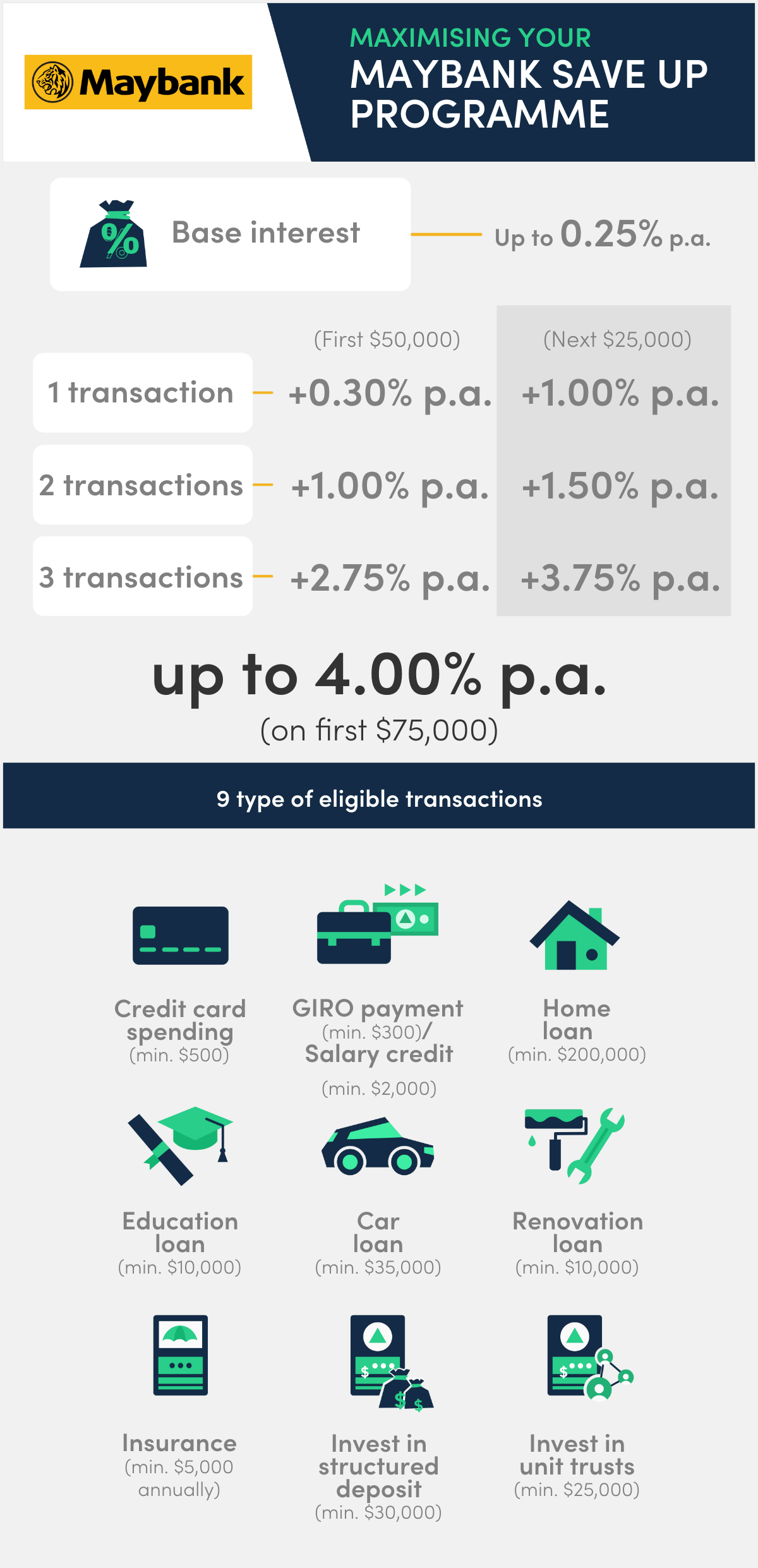

5. Maybank SaveUp Account

There’s only 1 savings account with no minimum balance or fall-below fee at Maybank—well, at least until you turn 25 years old. It’s the Maybank SaveUp Account.

The Maybank SaveUp account by right imposes a minimum initial deposit of $500 and a minimum balance of $1,000. If you fall below the minimum balance, you have to pay a $2 monthly fee unless you’re under 25 years old—then you get the monthly fall-below fee waived.

The SaveUp account itself doesn’t offer you any bonus interest. Instead, you’ll need to link your SaveUp Account to the MayBank SaveUp programme, which gives you a base 0.25% interest.

From there, any bonus you earn depends on how many products you take up with MayBank. These can be GIRO payments, salary crediting, credit card spend, investments, insurance, and loans. Fulfilling one of these earns you an extra 0.30% p.a. on your first $50,000. Taking up 3 earns you a bonus 2.75% p.a. on your first $50,000. The maximum effective interest rate you can earn is 3.08% p.a.

6. OCBC FRANK Account

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- 0.2%

- Min. Balance

- S$1,000

With a minimum age requirement of just 16 years old, the OCBC FRANK Account targets the young (and kinda broke), which is probably why they’ve decided to have no minimum balance and no fall-below fees… but only if you are below 26 years old. Otherwise, you get charged $2 if your balance falls below $1,000.

On the bright side, the account’s interest rates are not that horrid compared to other savings accounts of this type. You get 0.1% a year on your first $25,000 and $0.2% on your next $25,000. Any amounts above $50,000 will earn 0.05%.

Account balance | Interest rates |

First $25,000 | 0.1% a year |

Next $25,000 | 0.2% a year |

Above $50,000 | 0.05% a year |

Another perk is that the OCBC FRANK debit card comes with unlimited 1% cashback on Lazada, Taobao, Shein, 7-Eleven, Cheers, Grab, SimplyGo, and more. You get this card for free, with no annual fee charged.

On a more superficial level, the debit also comes with over 60 card designs you can choose from at no extra charge. It’s not a material perk, but it may perk you up.

7. RHB High Yield Savings Plus Account

The only RHB savings account with no minimum balance is the RHB High Yield Savings Plus Account, which gives you a base interest of up to 1.50%:

Deposit balance amount | Interest rates (p.a.) |

First $50,000 | 1.20% |

Next $25,000 | 1.30% |

Next $25,000 | 1.40% |

Above $100,000 | 1.50% |

There’s no minimum initial deposit and no minimum balance. The only charge you may face is a $30 early account closure fee if you close the account within 6 months of opening it. Don't do that—with no minimum balance required, there is absolutely no harm leaving it open even if you have $0 in it.

To open the account, you just need to be a Singaporean, PR, foreigner with employment pass or work permit, and need to be at least 16 years old. That’s all. Easy!

8. Standard Chartered Basic Bank Account

With a very low minimum age requirement of just 15 years old, the old school Standard Chartered Basic Bank Accountoffers low-income Singaporeans affordable banking services.

It gives you a passbook, ATM card, and free ATM withdrawals with $0 minimum balance, and no fall-below fee. However, similar to Citibank’s basic bank account, it does come with a $2 monthly service charge regardless of your account balance. There’s also an initial account opening deposit of $20 required.

If you’re a beneficiary of the MSF Public Assistance Scheme/Special Grant Scheme, the service charge and minimum initial deposit are waived.

9. Standard Chartered JumpStart Account

- Base Interest Rate p.a.

- 1%

- Max. Interest Rate p.a.

- 2%

- Min. Balance

- S$0

The Standard Chartered JumpStart Account is open to young adults aged 18 to 26 only. If age is on your side, this account is a pretty good one as it gives you 1% p.a. on your account balance (up to $50,000) without needing any effort on your part—no lock-in period, minimum deposit, or requirement for salary crediting. Invest with Standard Chartered, and you’ll get an additional 1% p.a. interest for a total of 2% p.a. on your first $50,000.

The account also comes with a cashback debit card that gives you 1% cashback on all eligible spending, capped at $60 cashback per month, if you link the card to your JumpStart account. Like the savings account, this debit card doesn’t have any annual fees.

10. Standard Chartered SuperSalary Account

The Standard Chartered SuperSalary Account boasts $0 minimum initial deposit, $0 minimum balance, and $0 fall-below fee, which is supper. What isn’t so great is it’s not-so-super base interest rate of 0.01% p.a.

Once in a while, new customers may also be able to earn bonus interest during the first few months after opening the account. The last promotion ran from May to Dec 2024 and earned bonus interest of 1.99% p.a. on your first $100,000 for the first 6 months.

If the promotion rolls around again, you can consider using the account for 6 months to enjoy the bonus interest, and then traitorously switch to a different account after that. This is only worth it if you have quite a bit of cash on hand, though.

The account also entitles you to a Standard Chartered CashBack debit card, which lets you earn 1% on eligible spending, capped at $60 per month.

ALSO READ: Comparing Singapore’s 5 Digital Banks—and Figuring Out Which is Best for You

11. Trust Savings Account

- Minimum Initial Deposit

- S$0

- Base Interest p.a.

- 0.1%

- Max Interest p.a.

- 2.5%

The Trust Savings Account comes with no lock-in period, monthly fee, minimum balance, or account closure fee. So when it comes to a low commitment account, this one might just take the cake.

With no strings attached, you get to earn 0.50% p.a. interest on your Trust savings account under their Zen plan. Trust Bank offers 3 plans with this savings account, and you can earn higher interest on their other plans by fulfilling certain criteria. Here’s a breakdown:

Trust savings account plan | Minimum ADB required | Interest earned |

Zen | $0 | 0.50% p.a. |

Signature | None required, but keeping $100,000 ADB gives you an extra 0.40% p.a. interest | Up to 1.30% p.a. with: |

Flex | None required, but keeping $100,000 ADB gives you an extra 0.40% p.a. interest | Up to 2.50% p.a. with any 3: |

12. Why does “no minimum balance” mean different things?

When you’re comparing savings accounts in Singapore, the phrase “no minimum balance” can be a little confusing. That’s because it can mean 2 very different things depending on the bank and the product.

For some accounts, “no minimum balance” means no requirement at all. You don’t have to keep a certain amount of money in your account each month, and there’s no fall-below fee if your balance is low. The trade-off is that the bank may still charge you a flat maintenance fee.

Other accounts use the phrase differently. Here, “no minimum balance” applies only to interest. You can earn interest from the first dollar without needing to hit a threshold. However, the account may still require you to maintain a larger Total Relationship Balance (TRB) with the bank. If you don’t, you’ll face a fall-below service fee.

Take Citibank’s products as an example:

- Citibank Basic Banking Account: No minimum monthly balance, and no fall-below fee. Instead, you pay a $2 monthly account maintenance fee.

- Citi MaxiGain Account: No minimum balance required to earn interest. But you must maintain at least $15,000 TRB across your Citibank accounts, or you’ll be charged a $15 monthly service fee.

Understanding this difference is important because it affects the true cost of maintaining your account. One account might look simple but comes with a flat monthly fee. Another may offer higher interest, but only if you can consistently keep a larger balance.

MoneySmart tip: Always check whether a bank’s minimum balance requirement applies to earning interest or to avoiding service fees. This helps you figure out the real value of the account and avoid surprise charges.

ALSO READ: 8 Essential Tips for Comparing Credit Cards I Wish I Knew Earlier

Found this article useful? Share it with anyone who needs a new savings account.