A year ago, Singapore Savings Bonds (SSBs) were paying so little that they were easy to look past. By late 2025, the 10-year average return slipped to just 1.83%, the lowest in years. If you saw a rate starting with “1” and left your money elsewhere, that was a fair call.

However, the tables have turned this year. The latest bond, SBJUL26, now pays a 10-year average of 2.11% a year, lifted by pricier oil, stickier inflation, and a market that's stopped betting on rate cuts. At that level it quietly beats the best fixed deposits (around 1.6%) and the latest 6-month T-bill (1.48%), and you can still take your money out any month.

There's a catch: 2.11% is only the average. What you actually earn comes down to how long you hold, and the numbers are worth a closer look.

[ms-toc title="Singapore Savings Bond (SSB) Review 2026"]

Singapore Savings Bond interest rates (July 2026)

The newest bond, SBJUL26 (GX26070F), works like all the others. With a new release each month, MAS sets the rate based on what government bonds are paying at the time.

Here’s what $10,000 in this bond earns you, year-on-year:

The rate climbs the longer you hold. Year 1 pays the least and Year 10 the most. “2.11%” that everyone quotes is simply your average over the full 10 years.

Why have rates recovered? An SSB roughly tracks the 10-year government bond yield, which is the rate at which the government borrows. That yield slid through 2025, which dragged the SSB average down from over 3% in mid-2024 to its 1.83% low. The recent jump in oil prices and inflation pushed the yield back up, and SSB rates rose with it.

That 10-year term isn’t set in stone, either. You’re never locked in, and redeeming early costs just a flat $2 fee. The higher rates further along are simply a reward for holding longer.

Singapore Savings Bond calculator

To see what those rates mean in real money, here is the total interest a $10,000 investment earns by the end of each year:

On a $10,000 investment:

- Hold for 1 year: you earn about $146 (1.46%), then get your $10,000 back, minus a $2 fee.

- Hold for the full 10 years: you earn $2,134 in total, (average 2.11% interest per year).

However, you only earn interest on the principal. The SSB credits the interest earned directly into your bank account every 6 months, rather than leaving it to compound inside the bond. For a risk-free product you can exit any month, that’s a fair trade-off.

Can I still buy the latest release Singapore Savings Bonds?

Yes, you can. Here’s the full details of the bond that is currently open, SBJUL26 (GX26070F):

Demand is on your side right now, too. Because rates only recently climbed back above 2%, appetite has been soft and recent bonds haven’t sold out. That means you’ll almost certainly get the full amount you apply for. In 2023 and 2024, when rates were higher, popular issues were oversubscribed and some people received less than they asked for, but that’s unlikely in today’s market.

Do watch the deadline. Applications for SBJUL26 close on 25 June 2026 at 9pm. Miss it, and you’ll have to wait for next month’s issue. Before you commit, it’s worth understanding what a SSB is.

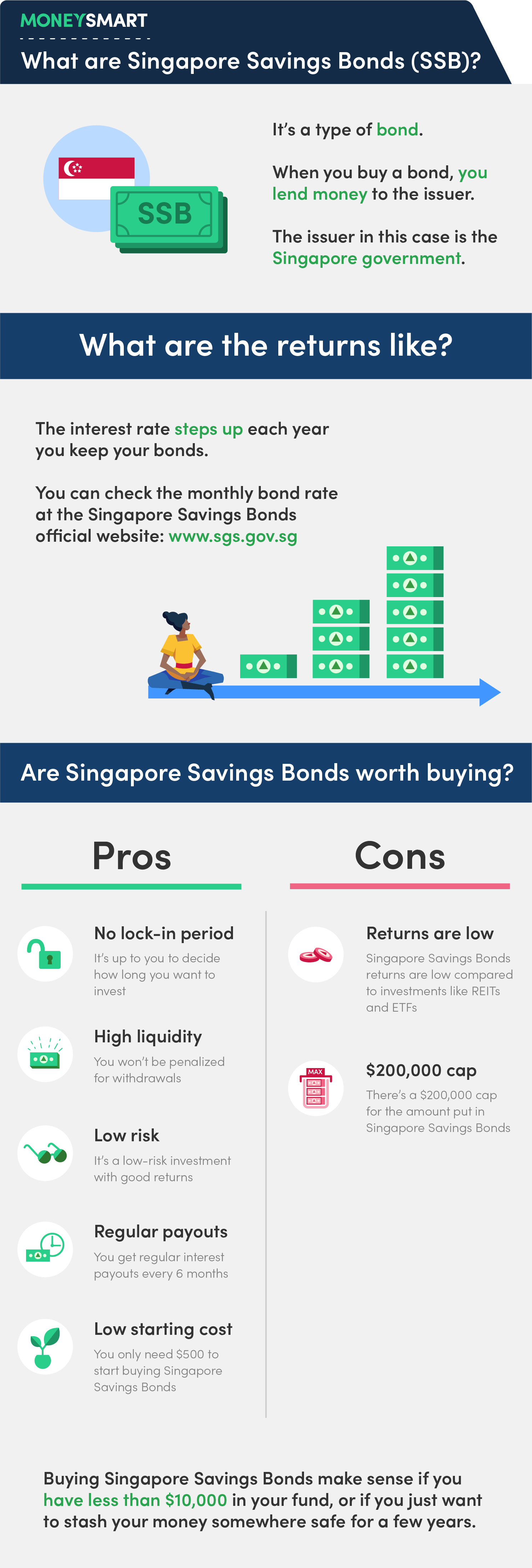

What are Singapore Savings Bonds or SSB?

At heart, a Singapore Savings Bond is a loan you make to the Singapore Government. You lend them your money, and they pay you interest for it. (In other words: once you buy one, you lose the right to grumble about the gahmen taking your money, since you have just handed it over yourself.)

People are happy to make that loan for 2 reasons: the returns are steady, and the risk is about as low as you will find. The SSB is fully backed by the Singapore Government, which holds the top “AAA” credit rating, so your capital is guaranteed. That makes it safer than cash in a bank, which could in theory fail.

In return, you get interest every 6 months, and there is no lock-in. Stay up to 10 years to climb the rates, or pull out early with no penalty. Getting started is simple, and the next section shows how.

How to buy Singapore Savings Bonds

Buying your first SSB takes three steps.

Step 1: Get a DBS/OCBC/UOB bank account and a CDP Securities account

Chances are you already bank with DBS, OCBC or UOB. If so, you only need to add an individual CDP account. Fill in the form and post it with your supporting documents.

You can also invest through your SRS (Supplementary Retirement Scheme) account, via your SRS operator. Singapore PRs and foreigners can take part too, as long as they have a CDP or SRS account.

Step 2: Apply for a Singapore Savings Bond

A new bond opens at the start of each month. You then have about three weeks to apply. Use your bank’s iBanking or an ATM, with your CDP account number ready. You choose how much to put in, with no fixed term to commit to. The amount, plus a $2 fee, comes out of your bank account when you apply.

Step 3: Secure your Singapore Savings Bond

After applications close, you find out at the end of the month if you got the bond. If it was oversubscribed and you did not get the full amount, the rest is refunded the next day. The bond is issued on the first business day of the next month. CDP notifies you, and your 6-monthly interest payments begin.

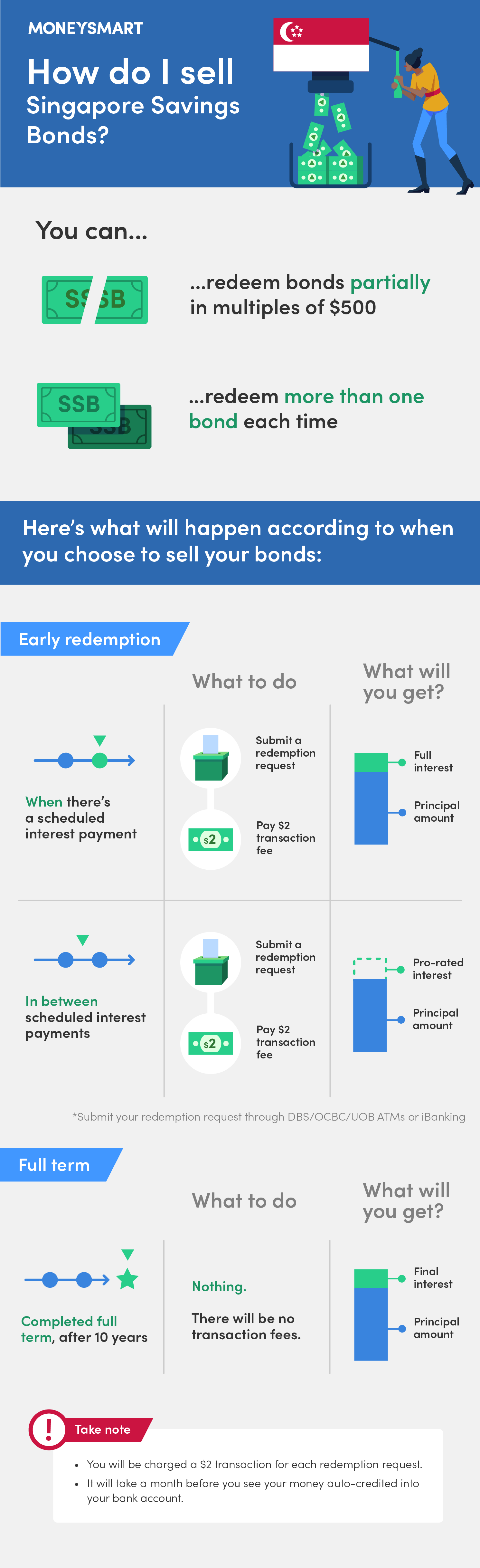

How to redeem your Singapore Savings Bonds

Need your money back? You can redeem an SSB in any month before the 10 years are up, with no penalty, as MAS sets out. What you get back depends on the timing:

To redeem early, send your request through a DBS, OCBC or UOB ATM or iBanking. You can take out part of your holding, in multiples of $500. You can also redeem several bonds at once. Each request costs $2.

Plan around the timing, though. There is a one-month wait before the money is credited back into your account. Do not leave it to the last minute if you anticipate the need for cash soon.

Are Singapore Savings Bonds worth buying in 2026?

After a quiet 2025, the SSB has become a lot more appealing. It now edges out both the best fixed deposits and recent T-bills, and unlike either of them, you can redeem in any month.

Just keep in mind that the rate isn’t fixed for the future. Each month’s bond is priced off prevailing government bond yields, so the next issue can come in higher or lower than the last.

Already holding older SSBs?

If you’re holding older bonds paying 3% or more, keep them. Switching to a newer bond only makes sense if its rate clearly beats your current one. Weigh up each bond on its own, rather than going by the latest headline rate.

Bottom line: an SSB won’t make you rich, but it keeps your capital safe and pays a little more than most no-risk options. For anyone who values stability, it’s one of the easiest places to park money you’d rather not put at risk.

SSB alternatives: fixed deposits, T-bills and savings accounts

Say you have $10,000 to set aside for the next couple of years, perhaps for a wedding, a renovation or a car. An SSB is one safe place for it, but it isn’t the only option.

The main alternatives are a fixed deposit, which locks in a promotional rate for a set term, and a high-interest savings account, which pays bonus interest. Savings accounts can offer eye-catching rates, but only if you meet monthly conditions, such as crediting your salary, hitting a minimum card spend, or buying an insurance or investment product.

This is how a year on $10,000 compares across all 3 options:

A few honest notes on that table:

- Fixed deposits currently top out at around 1.60% a year. Rates are creeping up again, but the better ones usually want $10,000 to $20,000, locked away for a fixed term.

- High-interest savings accounts can look hard to beat, with UOB One up to around 3.40%, OCBC 360 up to around 2.45% and Standard Chartered BonusSaver up to around 7%. But those top rates only apply to certain balance bands, and only if you meet every monthly condition. Miss one, and your real rate drops fast.

- If you have less than $10,000 to $20,000 to set aside, you may not qualify for the better fixed deposits anyway. That is where the SSB, and its $500 minimum, come in handy.

An SSB isn’t meant to hold everything, of course. For money you can lock away for the long term, growth assets like dividend stocks aim higher, while CPF pays 4% a year, though it stays out of reach until retirement. Each person can hold only $200,000 in SSBs in total, so anything beyond that will need another home.

One final note on Singapore government bonds

Maxed out your SSBs? Two other government-backed options carry the same “AAA” backing. Both involve lending to the government, and both need a little more know-how:

- Singapore Government Securities (SGS) Bonds pay interest every 6 months and run for up to 30 years. Unlike SSBs, you can sell on the open market.

- Treasury Bills (T-Bills) are short-term, either 6 months or a year. You buy them at a discount and get the full amount back at the end. The difference will be your returns. The latest 6-month T-bill came in at 1.48% a year.

To see what is on offer now, head to the MAS website.

Already holding SSBs, or sitting on idle cash and thinking about your first one? Share this review with your family and friends!