The UOB One account is getting nerfed—again.

The UOB One account will now earn you a maximum effective interest rate (EIR) of 3.30% p.a., down from 4% p.a., which was in turn down from 5% p.a. Here's a brief, recent history of the UOB One savings account:

- 1 Dec 2022: The UOB One savings account raised its maximum rates to a generous 7.8% p.a.—the highest in the account's (then) 7-year history. All you needed to was credit your salary to the account via GIRO and spend on your UOB credit card. The EIR then was 5% p.a. on your first $100,000.

- 1 May 2024: UOB dropped its maximum interest rate to 6%, bringing the EIR down to 4% p.a. At the same time, they raised the account balance cap—you could enjoy bonus interest on your first $150,000 instead of $100,000.

- 1 May 2025: Exactly a year later, UOB will nerf their flagship savings account further. The new highest tier interest rate you'll get with the UOB One account is 5.3% p.a., with an EIR of 3.3% p.a. on the same $150,000 balance cap.

Is the UOB One savings account still worth your time and money? Which savings accounts will earn you more than the UOB One account after it slashes its rates? Let's find out.

UOB Savings Account Review (2025)

- How does the UOB One Account work?

- What are the new UOB One account interest rates?

- UOB One Account effective interest rates

- Should I use the UOB One account after the nerf?

- OCBC 360 vs UOB One account—which is better?

- UOB One vs DBS Multiplier account—which is better?

- UOB One account minimum balance, fall below fee and more

- Which UOB credit card should you use with your UOB One account?

1. How does the UOB One Account work?

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 3.40%

- Min. Balance

- S$1,000

Like any other savings account, the UOB One savings account needs you to perform certain actions every month to hit the maximum interest rates.

You have 3 options, all of which include spending on a UOB card:

- Credit/debit card spend (minimum $500 per month)

- Credit/debit card spend (minimum $500 per month) + 3 GIRO debit transactions

- Credit/debit card spend (minimum $500 per month) + salary credit (min. $1,600)

These are the eligible cards:

Eligible UOB credit cards | Eligible UOB debit cards |

| UOB One Card | UOB One Debit Visa Card UOB One Debit Mastercard UOB Lady’s Debit Card UOB FX+ Debit Card |

According to the UOB One Account bonus interest FAQs, recurring insurance payments actually count towards your monthly minimum credit/debit card spend. Neat! This is a category often excluded. However, the usual exclusions like remittances, hospital bills, and EZ-link payments remain exclusions. See the FAQs (Q4) for the full list.

The main draw of the UOB One account is that you can get the highest tier interest rates simply by hitting 2 categories—many other banks ask you to jump through many more hoops before the grant you their best rates.

The best 2 categories to hit for UOB One are salary crediting and credit card spending. However, if you aren't a conventional salaried worker (think freelancers, part-timers, retirees, landlords, etc.) you'll still be able to earn bonus interest with the UOB One account if you make at least 3 GIRO bill payments per month. And bills are one thing we’re definitely not short of in Singapore.

Just how much bonus interest can you earn? Let's unpack that in the next section.

2. UOB One account: What are the NEW interest rates?

Here's a screenshot from UOB detailing the changes that are soon to take place with the UOB One account:

Image: UOB

What is the UOB One account changing from 1 May 2025?

- The highest maximum interest rate will drop from 6% p.a. to 5.3% p.a. (on your next $25,000 after the first $125,000). This is the big number UOB might advertise front and centre, but it isn't the end of the story. More on that in the next section, but for now just know that...

- ...the maximum EIR will decrease from 4% p.a. to 3.3% p.a. (on $150,000).

- Correspondingly, the maximum absolute interest you can earn decreases from $6,000 to $4,950 per year, or from $500 to $412.50 per month.

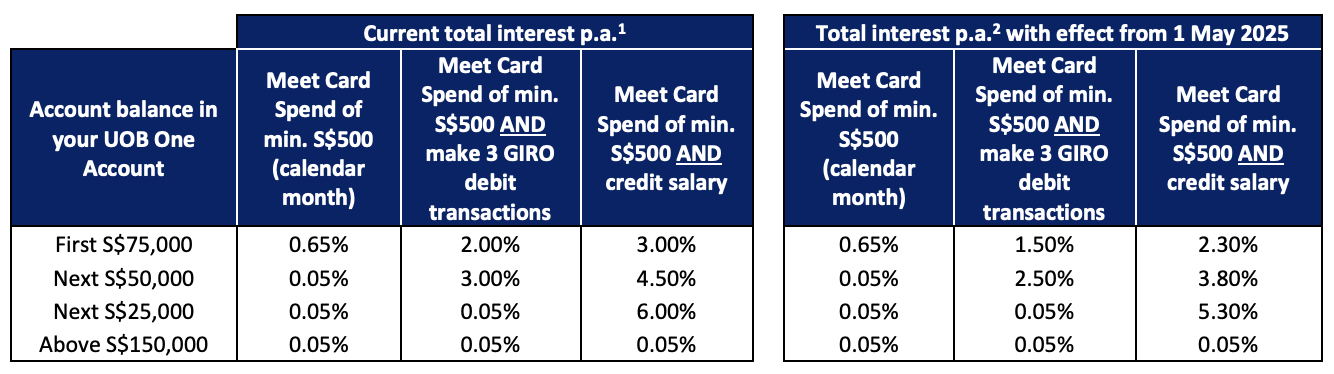

Account Monthly Average Balance | $500 spend per month on eligible UOB Card | $500 spend per month on eligible UOB Card + 3 GIRO debit transactions | $500 spend per month on eligible UOB Card + credit salary via GIRO |

First $75,000 | 0.65% |

|

|

Next $50,000 | 0.05% |

|

|

Next $25,000 | 0.05% | 0.05% |

|

Above $150,000 | 0.05% | 0.05% | 0.05% |

What is the UOB One account not changing from 1 May 2025?

- The mechanics to earn the bonus interest rates. To unlock the highest tiers, you still need to fulfil only 2 requirements—credit your salary and spend on your credit card.

- The cap on how much of you savings can earn bonus interest—this remains at $150,000. Anything above that will earn a meagre 0.05% p.a. only.

3. UOB One Account effective interest rates

Now let's go even deeper into the new bonus interest rates. You'll notice that the highest 6% p.a. (from now till 30 Apr 2025) and 5.3% p.a. (from 1 May 2025) rates only apply to $25,000. So while these high numbers are extremely enticing, to think it applies to the full $100,000 pot of gold you put into your UOB One Account would be a gross error.

This is where the concept of effective interest rates (EIR) comes in very useful. EIR refers to the actual return on your savings, taking into account things like the tiered bonus interest rates I mentioned in the preceding paragraph and compound interest. Compound interest is the addition of interest to the principal sum of a loan or deposit, where the interest that has been added also earns interest. For example, if you had $10,000 and earn $10 interest, you're next earning interest on $10,010 instead of just $10,000.

But let's save you from the complicated math and return to the EIR of the UOB One Account. Here's what you'll really earn from it:

Effective interest rates on UOB One Account—Changes from 1 May 2025 | |||

Account Monthly Average Balance | $500 spend per month on eligible UOB Card | $500 spend per month on eligible UOB Card + 3 GIRO debit transactions | $500 spend per month on eligible UOB Card + credit salary via GIRO |

$75,000 | 0.65% |

|

|

$100,000 | 0.50% |

|

|

$125,000 | 0.41% |

|

|

$150,000 | 0.35% |

|

|

To make the most of the UOB One Account, you'd want to put in $150,000 and fulfil both the UOB credit card spend and salary criteria. Once you fulfil these requirements, you'll earn 3.30% interest each year on $150,000, which works out to be $4,950 a year.

4. Should I use the UOB One account after the nerf?

From 1 May 2025, the UOB One account's best offer is this:

- What they want from you: Put in $150,000, credit your salary to the account, and spend at least $500 a month on a UOB credit card

- What they will give you in return: 3.30% p.a on your $150,000

Is this a fair ask?

Yes. The salary and credit card spend mechanics are easy to hit, especially if you already use or are currently eyeing a UOB credit card. Other savings accounts require you to buy insurance or investment products with them in order to unlock their highest rates.

The hardest part is probably having $150,000 in the first place. If you don't have $150,000, you won't be hitting 3.30% p.a., and other savings accounts may be able to give you higher interest for the amount you have.

Is 3.30% p.a. a good rate?

Compared to the previous rate, no one's dancing for joy. But compared to other easy, low-risk investment tools, 3.3% is good. To put things into perspective, the highest fixed deposit rates right now don't even hit 3%. The latest T-bill on 26 Mar 2025 closed at 2.73% p.a.

Comparatively, the UOB One Account can give you 3.3% interest and still keep your money liquid, unlike fixed deposits or T-bills.

Can other savings accounts give me a better offer?

It depends on how much money you are putting into your savings account.

If you intend to park more than $100,000 in your savings account, the UOB One savings account is your best bet. Other savings accounts generally only award you bonus interest rates on the first $100,000; anything further will only earn 0.05% p.a.

On the other hand, if you only have $100,000 to put into a savings account, there are 2 banks that can best UOB One.

#1: The Bank of China will give you 3.4% p.a. on $100,000 with their SmartSaver account for the same requirements of crediting your salary and spending $500/month on one of their credit cards. If you spend $1,500 or more per month instead, you get 3.7% p.a.

#2: The OCBC 360 Account will reward you with an EIR of 3.3% p.a. on your first $100,000 from 1 May 2025 (yes, OCBC 360 just got nerfed too). You need to fulfil 3 criteria:

- Credit your salary to the account

- Save at least $500 a month

- Spend at least $500 a month on an OCBC credit card

Wait, isn't 3.3% p.a. the same EIR as the UOB One account? Yes—but 3.3% is the EIR if you have a balance of $150,000, since the highest interest tier for UOB One only applies after the first $125,000 you park with them. If you only have $100,000, you only unlock the lower tiers, making your EIR on $100,000 only 2.68% p.a.

Read my full comparison of OCBC 360 vs UOB One below, or check out MoneySmart's review of savings accounts in Singapore to find out which one is the best for you.

5. OCBC 360 vs UOB One account—which is better?

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 4.45%

- Min. Balance

- S$3,000

The UOB One account’s “rival” is the OCBC 360 account, which is quite similar in that it also doesn’t come with salary crediting as a pre-requisite in order to earn bonus interest.

Come 1 May 2025, they will share another similarity—both will get nerfed, and both will have a maximum EIR of 3.3% p.a.

With the OCBC 360 savings account, you start with the same 0.05% base interest and then earn extra interest depending on what actions you complete that month. Here's a breakdown of the tiered bonus interest rates and the EIR you'll earn from 1 May 2025:

Transaction | Bonus interest on first $75,000 | Bonus interest on next $25,000 | EIR on $100,000 |

Salary credit (min. $1,800) | 1.6% p.a. | 3.2% p.a. | 2.0% p.a. |

Increase account balance (save min. $500 monthly) | 0.6% p.a. | 1.2% p.a. | 0.75% p.a. |

Credit card spend (min. $500) | 0.5% p.a. | 0.5% p.a. | 0.5% p.a. |

Selected insurance (min. $2,000 annual premium) | 1.2% p.a. | 2.4% p.a. | 1.5% p.a. |

Selected investments (min. $20,000) | 1.2% p.a. | 2.4% p.a. | 1.5% p.a. |

Maintain $250,000 in your account | 2.2% p.a. | 2.2% p.a. | 2.2% p.a. |

So which account is better? It depends on which requirements you're going to fulfil.

Credit card spending only: What if you can't or don't want to credit your salary to the account and all you do is spend on your credit card? It's a toss-up. Both the OCBC 360 account and UOB One account will give you an EIR of 0.5%.

Credit card spending + bill payments: The UOB One account is the winner—it'll give you an EIR of 1.75% p.a. on your first $100,000 for meeting these 2 criteria. The OCBC 360 account doesn't reward you for paying bills, so you'll only get 0.5% interest from your credit card spending.

Credit salary + save $500 each month: The OCBC 360 account rewards you with an additional 0.75% p.a. on your first $100,000 for saving money. Together with the base interest (0.05%) and bonus interest from crediting your salary (2.0% p.a.), that comes up to an EIR of 2.80% a year. Comparatively, the UOB One account will only earn you bonus interest for crediting your salary if you first also spend on your credit card.

Credit salary + credit card spending: You'll get an EIR of 2.55% with the OCBC 360 account compared to 2.68% with the UOB One account on your first $100,000.

Credit salary + credit card spending + save: However, if you're already crediting your salary into your OCBC 360 account, chances are you're also going to be able to save at least $500 of that salary each month. OCBC will reward you with an additional 0.75% p.a. bonus interest for that, nudging the EIR for the OCBC 360 account up to 3.3% p.a on your first $100,000.

While that beats the UOB One account's 2.68% p.a. on your first $100,000, remember that the UOB One account will have an EIR of 3.3% if you're parking $150,000 in the account.

You might also have noticed that the OCBC 360 account gives you 2.20% bonus interest for maintaining at least $250,000 in the account. But if you take a closer look, you'll realise that this 2.20% applies to only the first $100,000 of your account balance. That means $150,000 is going to sit there idle! There's a ton more you could do to invest $100,000, so I don't recommend stashing away $250,000 just to earn interest on less than half of it.

6. UOB One vs DBS Multiplier account—which is better?

The DBS Multiplier account is certainly a viable alternative to UOB One if you're a salaried worker.

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 4.10%

- Min. Balance

- S$3,000

While the UOB One Account mandates you spend on your credit card to earn bonus interest, DBS makes crediting your income a compulsory criteria to earn bonus interest. Then, you need to perform 1 to 3 extra transactions in any of the following categories to earn bonus interest:

- DBS credit card spending or PayLah! spending

- Home loan instalment

- Insurance

- Investments

Here's a quick look at the interest you can get with these actions.

Total monthly transactions | Income + 1 category | Income + 2 categories | Income + 3 categories |

First $50,000 | First $100,000 | First $100,000 | |

$500 to $14,999 | 1.80% | 2.10% | 2.40% |

$15,000 to $29,999 | 1.90% | 2.20% | 2.50% |

$30,000 and up | 2.20% | 3.00% | 4.10% |

DBS only awards you bonus interest on balances greater than $50,000 if you fulfil the income requirement and at least 2 others. Meaning, if you have more than $50,000 stashed away and want to earn interest on it, the only way DBS Multiplier will let you is if you also have a home loan, insurance policy, or investment product with them.

If you only credit your salary and spend on a credit card, go with UOB One. The DBS Multiplier earns you 1.8% to 2.20% on your first $50,000. Comparatively, the UOB One account would earn you an EIR of 2.30% on your first $75,000.

Planning to refinance your home loan with DBS? Then the DBS Multiplier makes sense for you as you'll be getting extra interest on top of potentially saving on your mortgage payments. Transact at least $500 a month to get 2.10% interest, or $30,000 and above to get 3% interest. Since the UOB One account doesn't reward you any bonus interest for home loan instalments, the DBS Multiplier is a better choice in this case.

Are you a freelancer, self-employed person, retiree, or in a position where you can't credit your salary to your bank account? Stick with the UOB One account. DBS is not going to give you any bonus interest if you don't credit your income to them.

Made up your mind on opening up a UOB One account? The next few sections walk you through the eligibility requirements and the best credit card to use with the account.

7. UOB One account minimum balance, fall below fee and more

The UOB One account is about as “no strings attached” as such savings accounts get. Here are some of the basic things to note about the UOB One account:

Minimum age: 18 years old

Nationality: Singaporeans, PRs, E-Pass, S-Pass & Dependent Pass holders

Minimum initial deposit: $1,000

Minimum balance (monthly): $1,000

Fall-below fee: $5 if monthly average balance is less than $1,000 (This fee is waived for 6 months for accounts opened online)

Early account closure fee: $30 (If account is closed within 6 months from opening)

Bonus interest cap: $100,000

8. Which UOB credit card should you use with your UOB One account?

There's a reason UOB's given their signature bank account and credit card the same name.

Regardless of which bonus interest tier you're on, the minimum requirement is to spend $500 a month on a UOB credit card. The best credit card for this purpose is... drumroll.... the UOB One card! If you couldn't already tell, the clue is in the name.

Not only do you perform the bare minimum to get bonus interest on your UOB One account, you get extra cash rebates of up to 10% (up to 20% for new UOB Credit Cardmembers) on top of it. There is a minimum spend of $500, but hey—that's the same minimum spend for the UOB One Account. Coincidence? Decidedly not. These 2 were meant to work together.

- cashback on daily spend at McDonald's, Grab, SimplyGo & Shopee

- Up to 10%

- cashback at all grocery spend

- Up to 8%

- cashback cap a year

- Up to S$2,240

Alternatively, opt for the UOB EVOL Card. It's a better option if you spend mostly on dining, shopping and Grab as you can get up to 8% cash back in those categories. However, do note it has a minimum spend of $600/month.

- on Local Online, Mobile Contactless, Telco, Gym, Streaming spend

- 10% Cashback

- FX Fees on overseas FX spend worldwide, with no min spend, no cap

- 0%

- Min. Spend per month for 10% cashback

- S$800

Finally, you can also opt for the UOB Lady's Card to get rewards points in your choice of spending category. The categories are beauty and wellness, fashion, travel, family (including groceries), entertainment, and transport. With the UOB Lady's Card, you earn rewards in UNI$ which you'll have to convert later.

- Base Earn Rate

- S$5 = 1X UNI$ (0.4 miles per S$1)

- Category of Choice

- S$5 = Up to 25X UNI$ (equivalent to 10 miles per S$1)

- Min. Spend

- S$0

If you prefer a more direct cashback mechanic, the UOB One Card and the UOB EVOL Card would be better options.

Know anyone who has or is thinking of applying for the UOB One account? Share this article with them!