In an investment landscape where stock markets swing with global headlines and bank deposit rates shift with policy changes, Singapore Treasury Bills (T-bills) remain a safe, no-frills option. Their short tenor ensures quick returns without long lock ups.

In 2024, T-bill yields were much stronger. The 6 month T-bill started the year near 3.7 to 3.8% and by 1 August 2024 closed at 3.40%, slightly above the 25 July result of 3.38%. The 12 month T-bill ranged between 3.45 and 3.58% in the first half of the year, making them highly competitive against bank deposits and CPF OA rates.

By 2025, the picture has shifted. The 6 month T-bill auction on 28 August 2025 (BS25117E) closed at 1.44%, down from 1.59% earlier in the month and far below mid 2024 levels. With core inflation easing to 0.5% in July and overall inflation at 0.6%, yields are now modest. Still, for investors seeking capital preservation with government-backed security, T-bills remain a prudent short term parking option.

Got your eyes on T-Bills? Start like a pro with our other investment guides! |

What’s changed since the latest August T-bill auction?

After a strong run in 2023, when yields touched 4.0%, T-bills remained attractive through much of 2024 at around 3.4%. Fast forward to August 2025, and the latest auction closed at just 1.44%, the lowest level in over two years. How are the interest rates currently faring? Let’s find out.

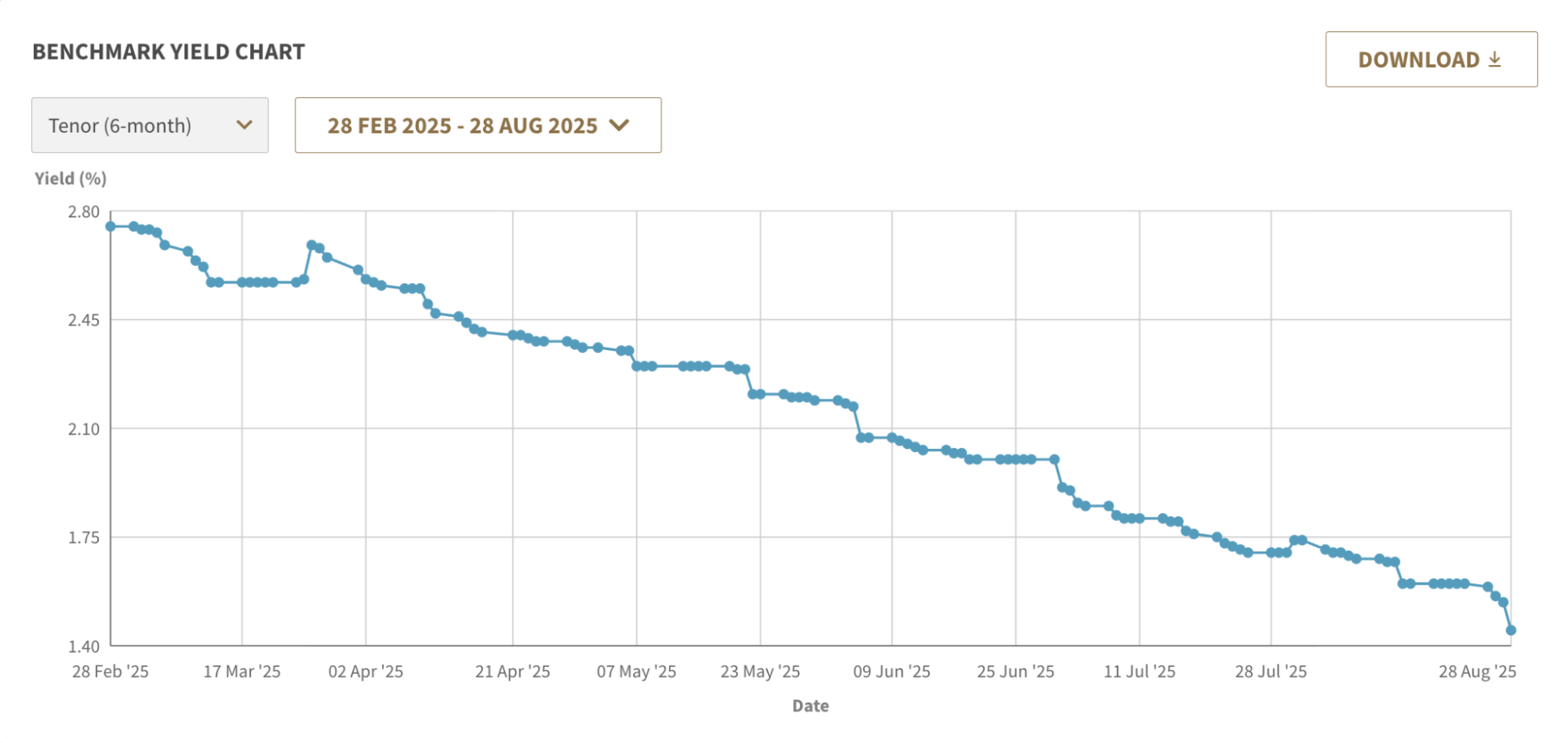

1. 6-month T-bill results (as of 28 Aug 2025)

Yield Chart in the past 6 months (February – August 2025). Image: MAS

For the 28 Aug 2025 T-bill auction (BS25117E), the cut-off yield was 1.44%, down from 1.59% earlier in the month. While this is a sharp fall from the ~3.4% levels seen in August 2024, it reflects a steady decline since February 2025, when the 6-month yield started just under 2.8%

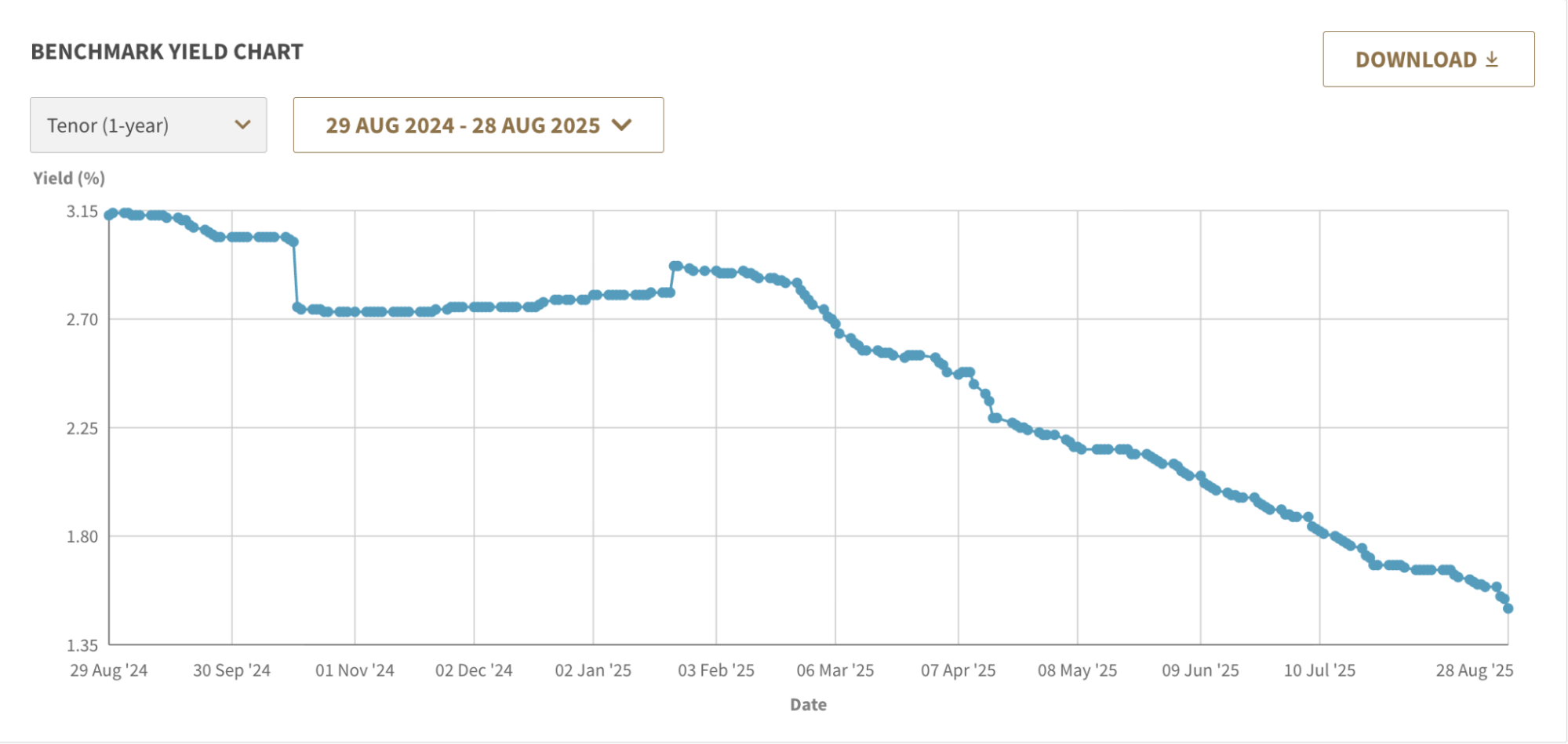

2. 12-month T-bill results (as of 28 Aug 2025)

Here’s a little relief for investors eyeing 12-month T-bills. The latest results in July showed the yield slipping to about 1.68%, down from 2.29% in April. By 28 Aug 2025, the rate had eased further to around 1.45%, marking the lowest level in over two years.

3. What do the returns mean for Singaporeans?

The premise this year looks very different from a year ago. Both the 6-month and 12-month T-bills have seen their yields fall to around 1.4 to 1.7%, well below the highs of 2024. This means T-bills are no longer outpacing your CPF Ordinary Account, which continues to offer a base rate of 2.5% and up to 3.5% with bonuses.

T-bills are also less competitive against today’s fixed deposit promotions. Several major banks are offering 6-month FDs around 2.1% and 12-month FDs up to 2.45%, comfortably above the latest T-bill cut-offs. In other words, where T-bills once clearly beat bank deposits, the balance has now shifted, and savers may find better short-term returns in fixed deposits or CPF.

ALSO READ: CPF Changes in 2025–2026: What’s New, Who It Affects & What You Should Do No

2025 T-bill yields dropped sharply – What are the reasons?

1. Global rate cut expectations weighing on yields

Unlike in 2024, when higher US interest rates supported stronger returns, the story in 2025 has been one of anticipated rate cuts. With Singapore’s core inflation easing to 0.5% in July and global inflation cooling, markets are pricing in that the US Federal Reserve may start trimming rates before year-end. As a result, short-term yields around the world, including Singapore’s T-bills, have come down significantly.

2. MAS Easing Its Monetary Policy via the Exchange Rate (S$NEER)

In January 2025, the Monetary Authority of Singapore made its first monetary policy easing since 2020 by slightly easing the slope of the S$NEER policy band—the tool MAS uses to manage inflation and economic conditions through exchange rate policy rather than interest rates. This move reflects moderation in inflation and growth, ultimately translating into lower domestic interest rates and reduced yields on government debt like T‑bills.

3. Investors rotating back to fixed deposits

In 2024, T-bills offered higher returns than bank deposits, driving oversubscription. But by mid-2025, the tables turned. Fixed deposits began offering2.1% for 6 months and up to 2.45% for 12 months, comfortably beating the latest T-bill yields of 1.4% to 1.7%. This shift has drawn savers back to banks, reducing upward pressure on T-bill rates.

4. Strong liquidity and safe-haven inflows

Some retail investors believe that the fall in T-bill yields is also being driven by excess liquidity in Singapore’s banking system and safe-haven inflows from abroad. In their view, the abundance of local deposits and foreign capital seeking stability in Singapore’s AAA-rated assets have further suppressed yields.

Image: Reddit

While anecdotal, these opinions highlight how market participants themselves perceive the forces shaping today’s lower returns.

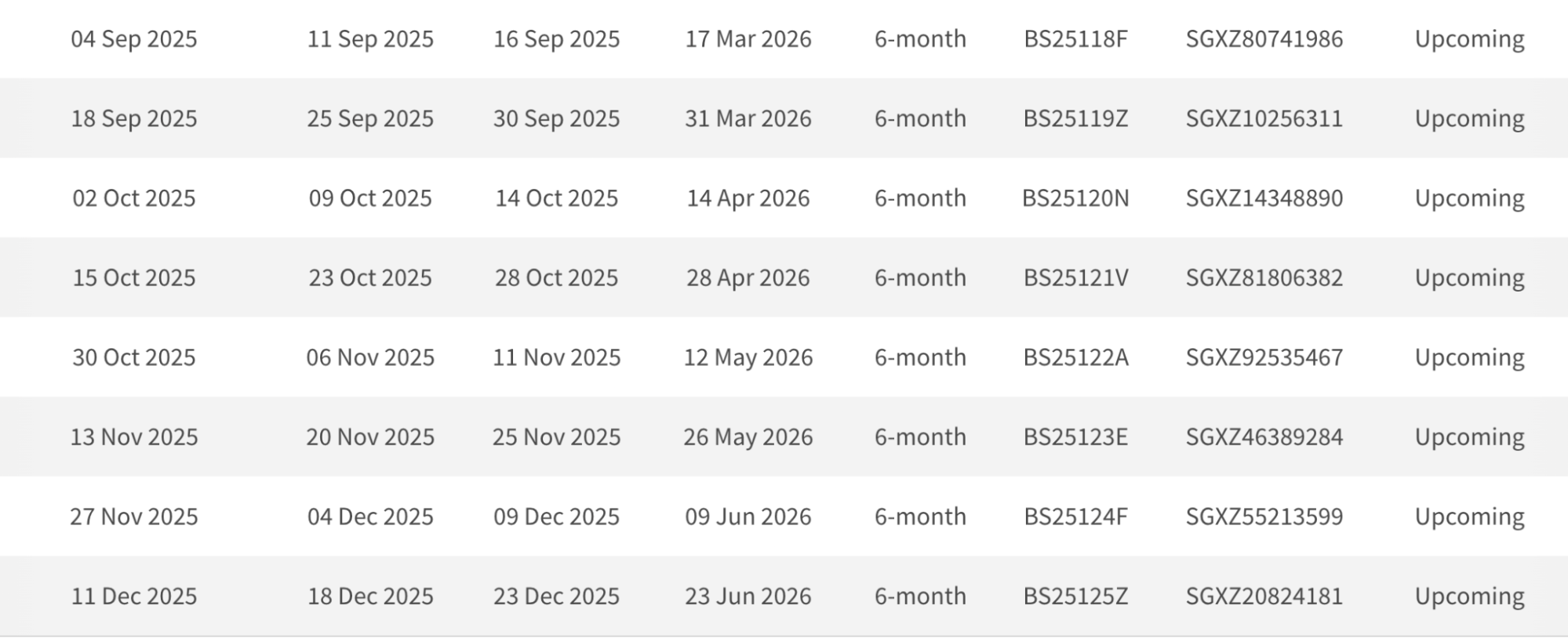

Upcoming T-Bill auctions in 2025

Should it slip your mind, here’s the complete list of the upcoming auctions scheduled for 2025:

1. 6-Month Auction Dates

Image: MAS

2. 12-Month Auction Dates

Image: MAS

The auction calendar for the rest of the year is packed, with fortnightly issues continuing into December and another 1-year T-bill scheduled for October. With yields having slipped significantly this year, many investors are questioning if it’s still worth setting aside spare cash for these auctions.

Should you still apply for T-Bills in 2025?

At this stage, the decision is less about chasing returns and more about how T-bills fit into your overall financial planning:

- For savers who value certainty of payout on a fixed date, T-bills remain unmatched. They are especially practical for households or businesses that need to lock away cash safely until a known expense, such as tuition fees, tax bills, or renovation costs. The government guarantee gives investors peace of mind that the funds will return in full, even if the rates are modest.

- In contrast, if your aim is to mid-long term maximise yield, upcoming auctions may not be attractive. Fixed deposits and CPF OA interest offer higher rates, and money market funds provide both liquidity and competitive returns. The opportunity cost of tying up your funds in T-bills has become much more significant.

Why do people still buy T-Bills in 2025?

Despite the lower returns, auctions remain heavily subscribed. Several factors explain this:

- Risk profile: Some investors see T-bills as a defensive anchor in their portfolio, balancing more volatile assets like equities, REITs, or crypto.

- Liquidity management: The short maturities fit those who want to park funds temporarily before deploying them into property, longer-term bonds, or equity markets.

- Institutional demand: Established investors (insurers and funds) continue to participate heavily, adding to the subscription pressure and keeping cut-off yields lower.

- Psychological comfort: For many retail investors, holding government securities still feels “safer” than relying on bank deposits, even if the rates are lower.

Are there any risks when investing in T-bills?

Although T-bills offer attractive rates in 2025 and have mostly remained low-risk, similar to other investments, they are subject to unpredictable market fluctuations. T-bill yields are usually influenced by factors such as:

- Inflation rates

- Central bank policy

- The broader economic conditions

- Investor sentiment towards risk

Note: Investing in T-bills alone might not generate sufficient returns to tackle the aforementioned ongoing inflation. They should only form a part of your diversified portfolio, not the entirety of it. Furthermore, selling your T-bills prematurely will result in losses.

Here’s a quick rundown of the pros and cons when investing in T-bills:

Pros | Cons |

Low minimum investment requirement ($1,000) | Relatively low rate of returns |

Can be bought & sold easily in the secondary market | No coupon interest payments in period leading up to maturity |

For individuals, interest income earned on SGS is tax exempt | Might hinder cash flow for those requiring steady monthly income |

Zero default risk | Potential interest rate risk |

Good for diversifying portfolio/ mitigating risks | Have to bid through auction processes |

Source: Yahoo!Finance

Closing thoughts

T-bills continue to stand out as one of the safest financial instruments, backed by the Singapore Government. For risk-averse or first-time investors, they offer a simple entry point into low-risk securities and a way to diversify a portfolio.

That said, the appeal of T-bills has shifted in 2025. With yields now around 1.4 to 1.7%, they are no longer ahead of fixed deposits or the CPF Ordinary Account, both of which provide higher returns. Investors should weigh the opportunity cost carefully.

It is also important to remember that T-bills are illiquid. Once purchased, your funds are locked in until maturity—six months or a year—so they may not be suitable if you anticipate needing quick access to cash.

Ultimately, the key is to align your T-bill investments with your broader financial strategy. Consider your risk tolerance, the need for liquidity, and the wider interest rate environment. Used thoughtfully, T-bills can still play a valuable role as a safe parking place for funds, even if they are no longer the yield leaders they once were.

Still considering whether you should invest in T-bills? Send this article to a friend who might be interested too!