Wondering where to park your spare cash in Singapore? You’re not alone. With the cost of living always climbing and rates on savings accounts, many are searching for smarter ways to make their money work harder.

Enter Singapore Treasury Bills (T-bills). While they don’t currently boast sky-high returns on their own, T-bills stand out right now because their yields look relatively attractive compared to other low-risk options like fixed deposits, which in 2025 have been falling month after month (RIP 4% p.a. rates).

If you’ve been curious about what they are, how they work, and whether they deserve a spot in your portfolio, this beginner-friendly guide breaks it all down—so you can decide if T-bills are a fit for your financial goals.

Beginner’s Guide to Singapore Treasury Bills for Individual Investors 2025

- What are T-bills?

- How do T-bills work for investors?

- Why is the Singapore government offering T-bills?

- What’s the difference between SGS bonds, T-bills, and Savings Bonds?

- How are T-bills issued?

- Who can take part?

- What do I need to start?

- Bank cut-off time

- How do I check my auction results?

- What happens when T-bills are oversubscribed?

- What do I do when I’m done with T-bills?

What are T-bills?

Treasury Bills, commonly known as T-bills, are short-term Singapore Government Securities (SGS). For those new to financial jargon, here’s what T-bills are at one glance:

- T-bills are investment securities

- They're issued by the Singapore government

- They have a short investment duration

While T-bills may sound similar to bonds, they operate differently.

ALSO READ: Top 11 Frequently Asked Questions (FAQs) about T-Bills in Singapore [2024]

How do T-bills work for investors?

T-bills provide investors with a fixed return, known as the yield. This yield is essentially your earnings as an investor. The main distinction between T-bills and bonds lies in how and when you receive your interest.

With bonds, you receive interest payments every 6 months. T-bills, however, work differently:

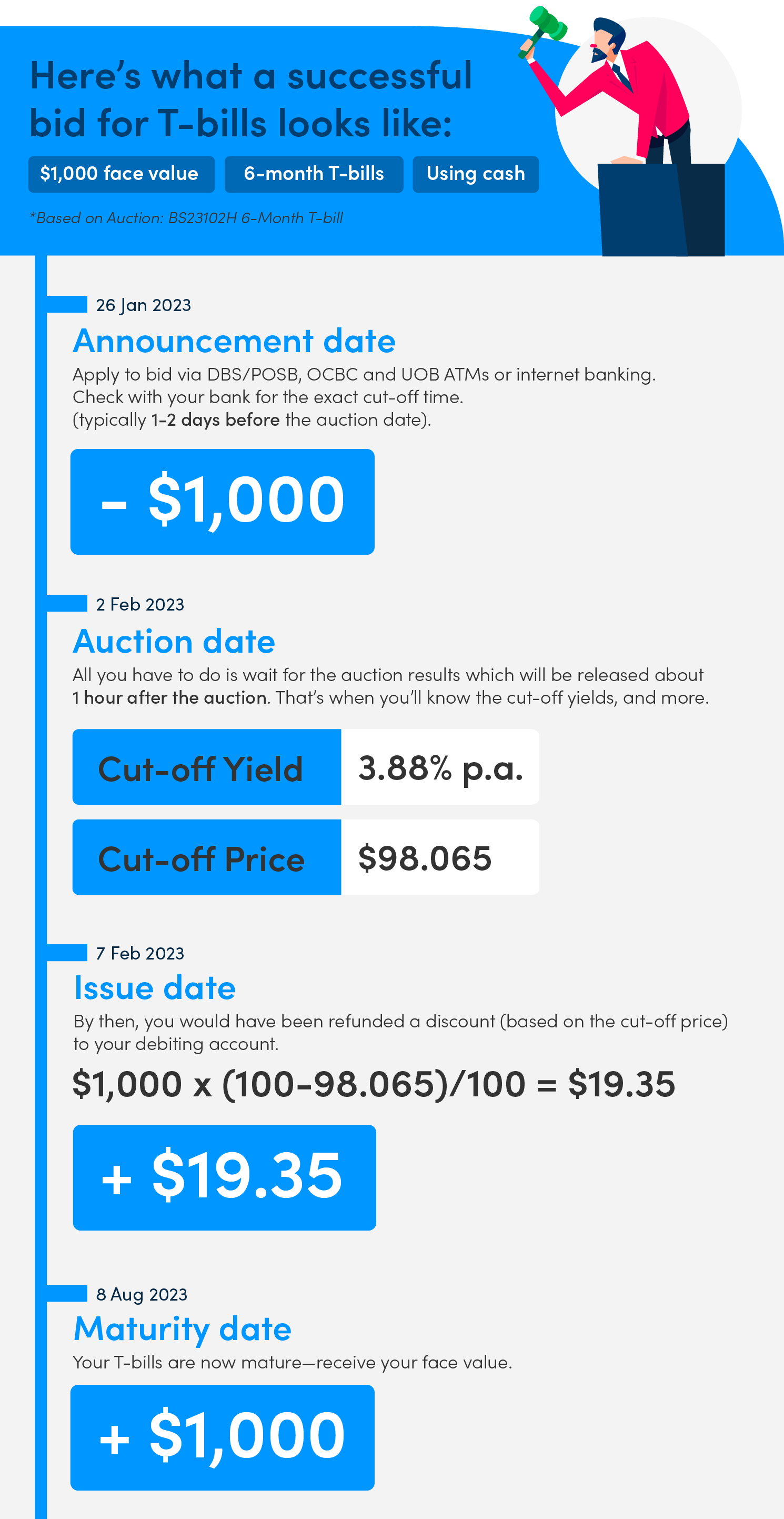

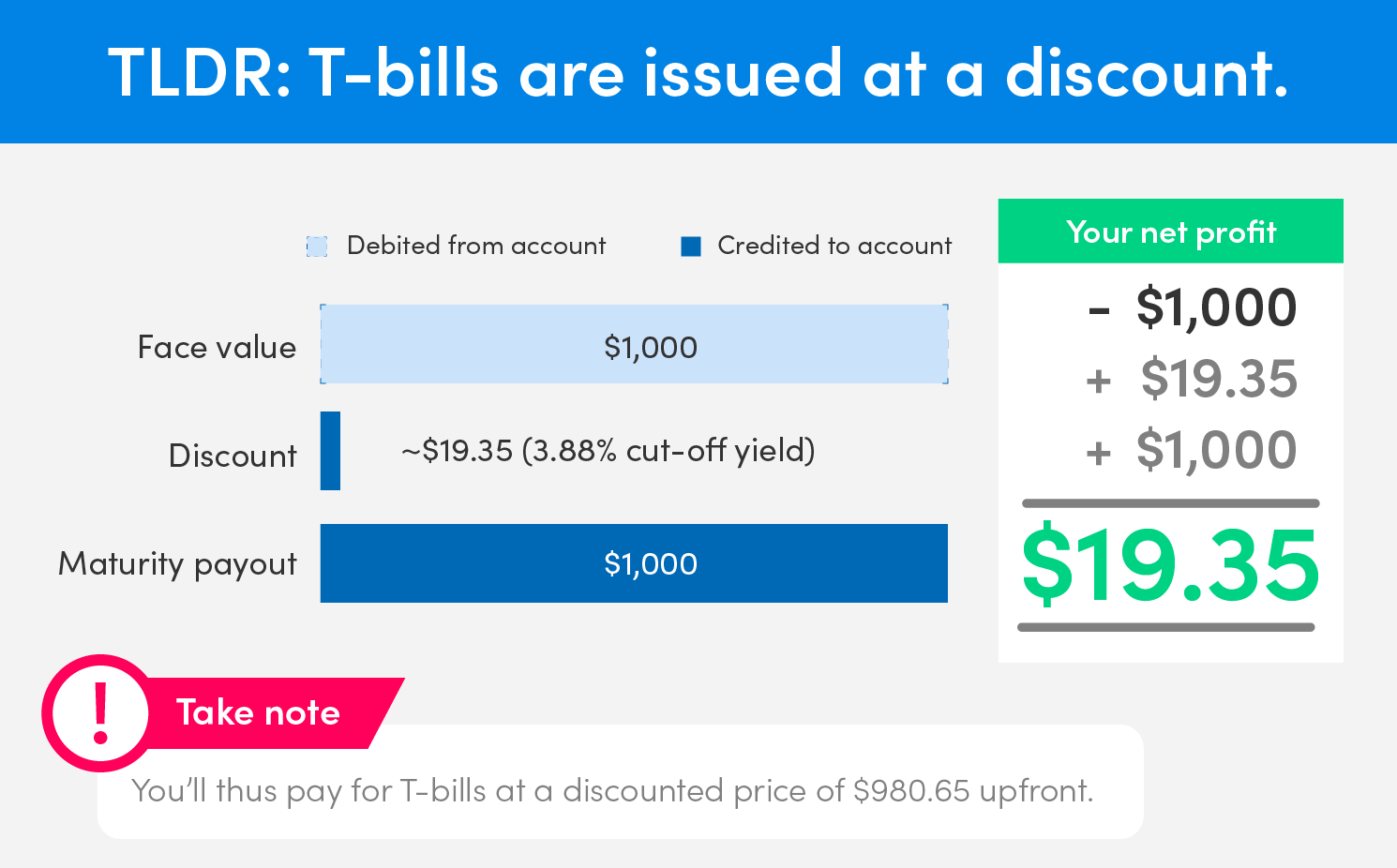

- When purchasing a T-bill, you buy it at a discount from its face value.

- At maturity (after 6 months or 1 year), the government pays you the full face value.

- Your earnings are the difference between the discounted price you paid and the full face value you receive.

At the time of writing, the benchmark yield for the latest 6-month T-bill on 28 Aug 2025 is 1.44% p.a. and 2.71% for the latest 1-year T-bill on 17 Oct 2024. You can always check the latest benchmark yields here. Let's illustrate with an example:

Suppose an investor buys a six-month T-bill worth $10,000 with a 1.44% p.a. yield:

- The investor pays $9,928 upfront (the discounted price).

- After 6 months, the investor receives the full $10,000.

The investor’s earnings are $72 (S$10,000 – S$9,928).

Why is the Singapore government offering T-bills?

T-bills allow the government to raise funds for its spending needs. When you purchase a T-bill, you're essentially lending money to the government, which they repay with interest at maturity.

However, T-bills aren't just about filling the government's cash expenditure. They serve multiple purposes in Singapore's financial ecosystem. Primarily, they help keep the Singapore Government Securities (SGS) market liquid. This liquidity ensures a smooth flow of transactions, provides stability to the financial system, and sets benchmarks for other financial products.

The SGS market generates a government yield curve, serving as a benchmark for the corporate debt market. This helps businesses price their own debt offerings. T-bills and bonds also contribute to a secondary market for cash transactions and derivatives. This secondary market plays a vital role in risk management for various financial institutions.

For both individual and institutional investors, T-bills provide an opportunity to participate directly in the Singapore market. It's one of the common avenues to invest in government-backed securities.

What’s the difference between SGS bonds, T-bills, and Savings Bonds?

T-bills | Singapore Government Securities (SGS) bonds | Singapore Savings Bonds (SSB) | |

Interest payment | Upon maturity, full value of T-Bill refunded following initial sale at a discount | Every 6 months, fixed | Every 6 months, gradually increasing depends on the allotment |

Tenor | 6 months / 1 year | 2 to 50 years | 10 years |

Minimum investment | $1,000 | $1,000 | $500 |

Maximum investment | None (allotment limit applies at each auction) | None (allotment limit applies at each auction) | $200,000 |

Price and interest rate | Published at auction | Published at auction | Published monthly by MAS before application opens |

Early redemption? | No | No | Yes |

Buying and selling on secondary markets? | Yes | Yes | No |

Investing SRS savings | Yes | Yes | Yes |

Investing CPF savings | Yes | Yes | No |

How are T-bills issued?

T-bills are issued through an auction process. Think of it like an auction for a limited-edition collectible. Just as bidders compete to secure that coveted collector's piece, investors vie for T-bills in a similar fashion.

Potential buyers can place competitive bids, trying to outdo each other. While this competitive approach is often used by large institutions and experienced investors, the government has made sure there's an easier way for everyday investors to participate too:

a) Non-competitive bid

Non-competitive bidding is ideal for beginners or those comfortable with market-determined yields. In this bid, you only specify the amount you want to invest, not the yield.

Non-competitive bids are allotted first, up to 40% of the total issuance. If non-competitive bids exceed 40%, allocation is done on a pro-rata basis. The advantage here is that you'll receive the T-bill at the cut-off yield, which is the highest accepted yield of successful competitive bids.

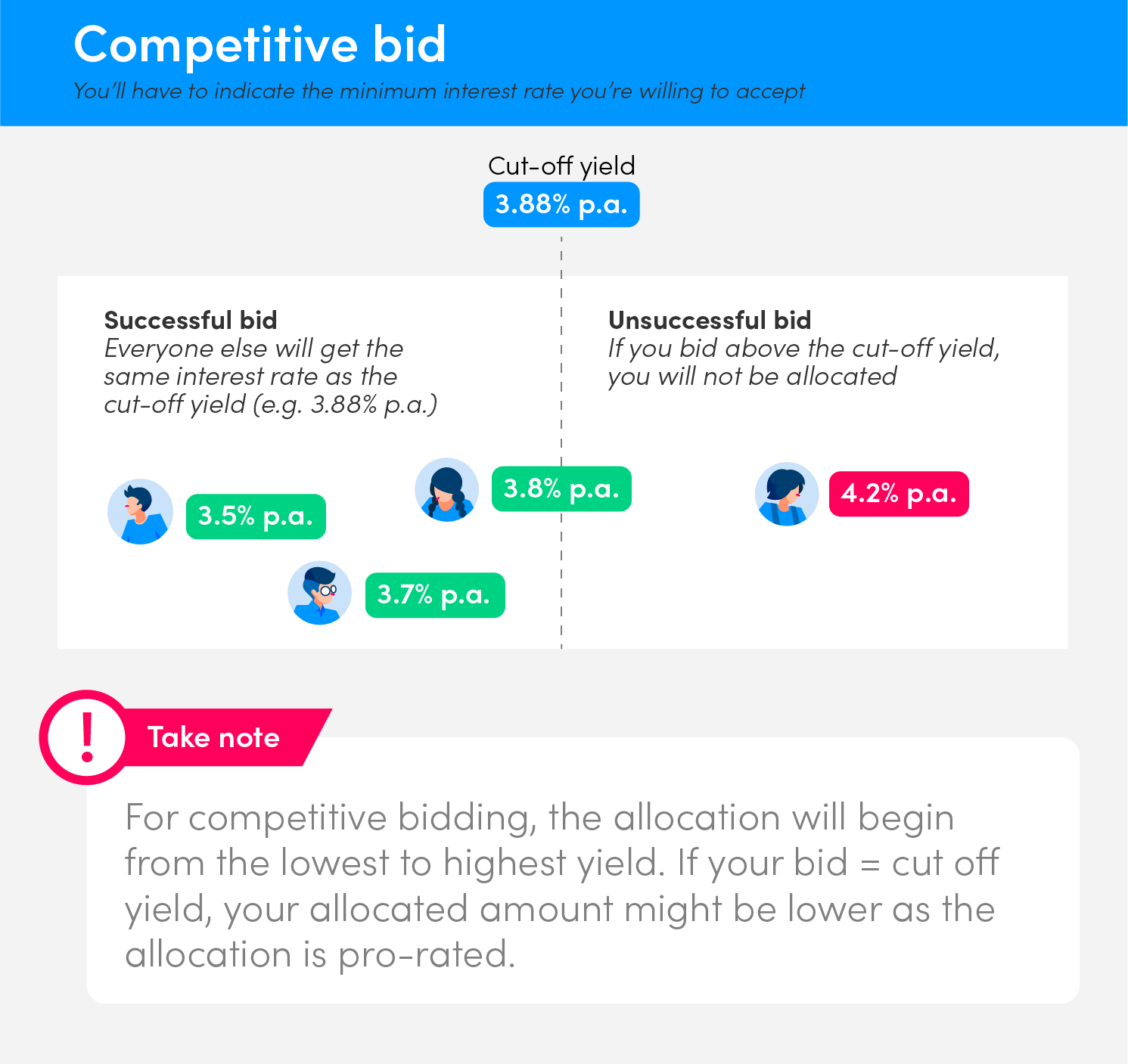

b) Competitive bid

Competitive bidding caters to those seeking a specific yield. In this application, you specify both the amount and the minimum yield you're comfortable with. Yields are indicated in percentage terms, up to two decimal places. You're allowed to submit multiple bids.

Allocation starts from the lowest to highest yields, after the non-competitive bids are fulfilled.

Here's the key point: the lower the yield you're willing to accept, the more likely you are to get your T-bills. It's like saying, "I'm okay with less profit," which makes your bid more attractive to the government.

However, with competitive bids, you may not get the full amount you applied for, depending on how your bid compares to the cut-off yield.

If you're new to T-bill investing, we recommend starting with non-competitive bidding. Whenever you opt for competitive bidding, here's what to expect:

ALSO READ: Is Investing in T-bills Worth It?

Who can take part?

As long as you are an institution or an individual at least 18 years old and not an undischarged bankrupt, you can invest in Singapore T-bills, regardless of residence or nationality.

Cool. So, what do I need to start?

To get started with T-bill investing, you'll need:

- An account with DBS/POSB, UOB, or OCBC

- An individual Central Depository (CDP) account with Direct Crediting Services activated

Note: While you can't buy T-bills with a joint CDP account, you can pay for them from a joint bank account.

Next, decide on your funding source:

- Cash: Apply through an ATM or internet banking. UOB charges a $2 transaction fee, while DBS and OCBC have waived this fee.

- CPF savings: Apply to invest your Ordinary Account (OA) and/or Special Account (SA) savings through the CPF Investment Scheme.

- SRS savings: Apply through the bank administering your SRS account.

For cash applications, ensure your CDP account is linked to your bank account. This allows coupon and principal payments to be credited directly to you.

Remember, each funding source has its own application process and requirements. Choose the one that best fits your financial goals and situation.

The minimum bid amount is $1000, and you can buy your T-bills in multiples of $1,000.

Bank Cut-off time

If you plan to submit your bid through ATMs or internet banking, be aware that these application channels typically close 1 to 2 business days before the auction.

It's advisable to check with your bank for the exact cut-off time for different application methods. Keep in mind that primary dealers need to submit all bids by noon on the auction closing date, so they require your application in advance to allow for processing.

How do I check my auction results?

After the auction closes, you want to know if your bid was successful. Here's how you can find out:

The aggregate auction results are published about an hour after closing on the issuance calendar. It's a quick way to get a general sense of how the auction went.

If your bid is successful, you'll see the T-bills reflected in your account three business days after the results are announced. Where exactly you'll find this information depends on how you applied:

- For cash applications: Check your CDP statement

- For SRS applications: Review the statement from your SRS Operator (DBS/POSB, OCBC, or UOB)

- For CPFIS-OA applications: Look for the CPFIS statement from your agent bank

- For CPFIS-SA applications: Check your CPF statement

What if you make an unsuccessful or invalid bid? Don’t worry, the money will be refunded to the account you used to make the application one or two business days after the auction.

Image: MoneySmart

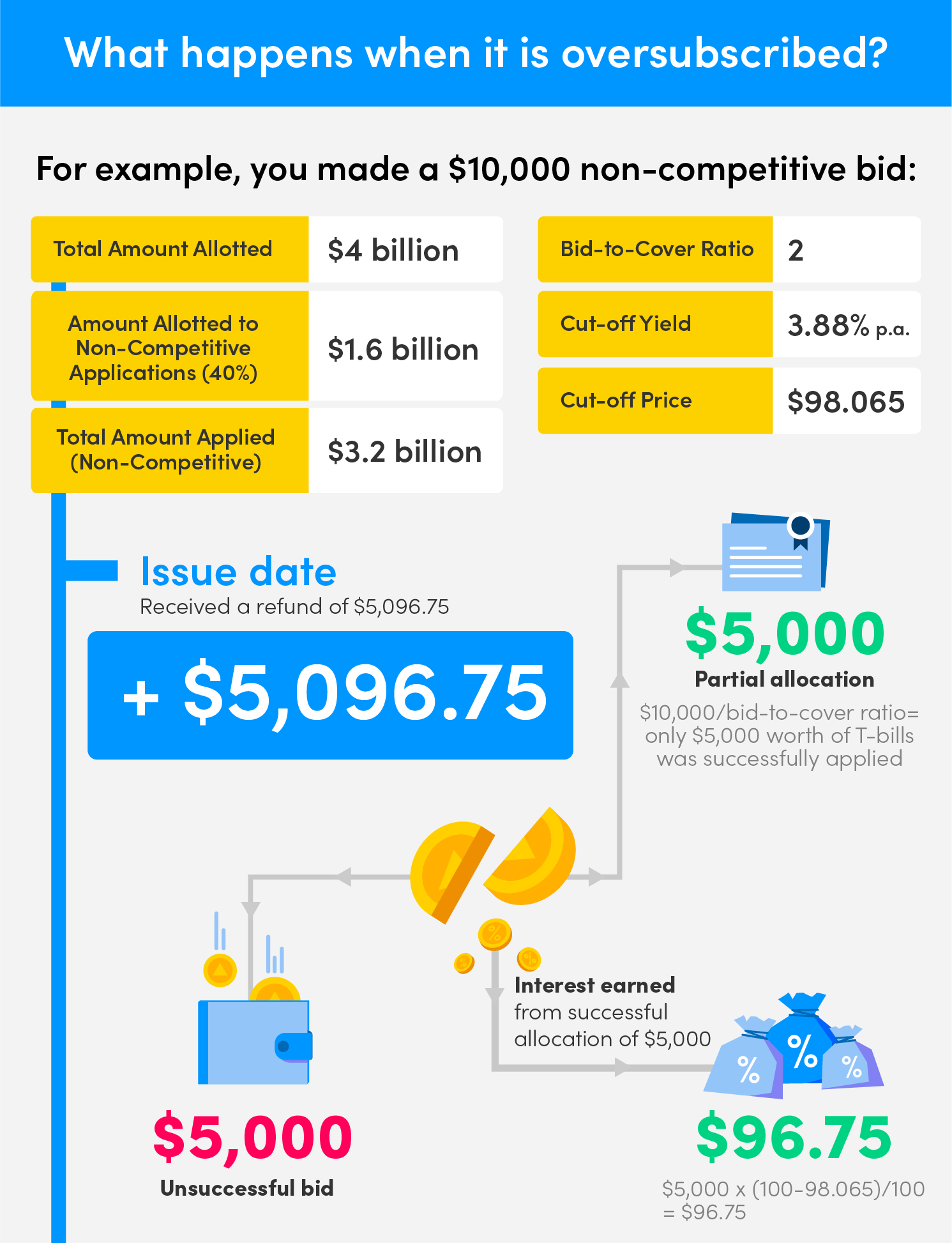

Help. I made a $10,000 non-competitive bid and was refunded more than half that amount.

So that’s where you got to keep a lookout for this thing called the bid-to-cover ratio. This ratio shows how many people want T-bills compared to how many are available. A high ratio means there's strong demand for these bills.

However, don't judge T-bill popularity based on just one auction. It's better to look at the ratios from the last 8-12 auctions to get a clearer picture.

The bid-to-cover ratio also affects how many T-bills you'll receive. For example, if you bid for $10,000 worth of T-bills and the ratio is 2, you might only get to invest $5,000 worth. This happens because the available T-bills are shared among all bidders when there's high demand. We’ll walk you through this:

What do I do when I’m done with T-bills?

Congratulations on your T-bill investment! Now, you have 2 main options:

- Hold until maturity: This is the most straightforward approach. Simply wait until the T-bill reaches its maturity date, and you'll receive the full face value.

Your earnings will be the difference between the face value and the discounted price you paid, which is equivalent to the advertised interest rate. Remember, unlike some bonds, T-bills can't be redeemed early. - Sell on the secondary market: If you need the funds before maturity, you can try selling your T-bills through DBS/POSB, OCBC, or UOB.However, be aware that the secondary market for T-bills isn't very active. This means finding a buyer isn't guaranteed, and you might have to sell at a less favourable price.

Got your eyes on T-Bills? Start like a pro with our other investment guides! |

That's it, you're all set.

Bookmark this page so that you easily refer to this article when you get round to buying your first T-bills. Don’t forget to spread the love and share this guide with your family, friends, colleagues, or anyone you think might find it useful.

Related Articles