If you’re considering a robo advisor, you might be considered a “lazy investor”. Don’t worry; that’s nothing to be ashamed of. After all, with the number of hours Singaporeans spend at work, not everyone has the time to actively invest in the market.

Lazy investing (or passive investing) is a great way to grow your wealth without unnecessary stress and effort. And robo advisors are designed to help you do just that—with the use of some advanced algorithms.

Here’s a guide on how robo advisors work.

Guide to Best Robo Advisors in Singapore

- What are robo advisors? Why choose them?

- What are the robo advisors in Singapore and how much are their fees?

- Which are the best robo advisors for beginners?

- Which robo advisors are more pricey?

- Are robo advisors regulated in Singapore?

- What are the pros of robo advisors?

- What are the cons of robo advisors?

- What sorts of investors are robo advisors suitable for?

1. What are robo advisors? Why choose them?

Robo advisors are digital investment apps. They do have some variations, but generally, you sign up on an online platform, input your goals and risk appetite, and, using some fancy algorithms, the robo advisor will recommend an investment portfolio for you.

As the word “robo” suggests, there is no direct human involvement in the advice rendered. Yet, every robo advisor is subtly different because it uses different algorithms based on the company’s knowledge of markets and investing.

Typically, robo advisors help automate your international investments in a low-risk way by helping you invest in ETFs (exchange-traded funds). These are funds that invest in a variety of assets, which might include stocks, bonds, gold and more. Most of the ETFs that robo advisors deal with are US or worldwide.

Once you’re happy with a recommended portfolio, you can start investing. Robo advisors usually have a very comprehensive dashboard for you to monitor your investments, as that’s mostly all you’ll be doing.

In short, robo advisors are investment instruments that help you invest passively in the long term, not to make short-term gains by buying and selling frequently.

2. What are the robo advisors in Singapore and how much are their fees?

Robo advisors started rising in popularity in 2016. The "OG" robos were Stashaway and AutoWealth, but lots of banks and startups jumped on the bandwagon in the past couple of years. For your convenience, here are the main local options for Singapore investors:

Robo advisor | Annual fee* | Minimum investment |

Syfe (Blue tier) | 0.65% | None |

0.2% – 0.8% | None | |

AutoWealth Flexi Cash: 0.1% AutoWealth Starter: 0.5% + USD18. | S$1,000 (AutoWealth Flexi Cash) S$3,000 (AutoWealth Starter) | |

0.25% – 0.85% | S$100 (for SaveUp portfolio) or S$1,000/US$1,000 (for Income, Asia and Global portfolios) | |

0.88% | US$100 | |

SqSave (formerly known as SquirrelSave) | 0.5% | S$1 |

Philip SMART Portfolio | 0.5% | S$300 |

Endowus | 0.15% – 0.6% | S$1,000 |

Kristal.AI | 0 – 0.3% | Based on investment |

|

|

|

Some notes on robo advisor fees:

Many robos charge tiered fees, i.e. the more you invest, the cheaper the management fee. In this article, which is aimed at beginner investors, we’re going to compare the lowest tier (usually up to S$20,000 invested).

Robo advisor fees are supposedly “all in”, but there might be additional costs depending on what products the robo invests in. For example, if it invests in ETFs, there might be a minor (0.1% or less) ETF fee hidden in there.

*What happened to SaxoWealthCare?

Saxo announced in Nov 2024 that they're closing SaxoWealthCare along with their SaxoSelect and Regular Savings Plan.

Got money in your SaxoWealthCare account and wondering what to do now? You first need to close the account before you can withdraw the money.

To close your SaxoWealthCare account: Go to Portfolio, find your SaxoWealthCare account, select the 3 dots '...', then select Close plan.

All positions will be sold within 3 business days. Saxo will then alert you when you can withdraw your funds.

To withdraw money from your SaxoWealthCare account: Select "Add or Withdraw Cash" under the SaxoWealthCare account OR go to My Profile > Withdraw funds.

View Saxo's help article on how to close your SaxoWealthCare account.

If you also have a SaxoSelect investment, read Saxo's help article on how to exit and withdraw your SaxoSelect investment.

3. Which are the best robo advisors for beginners?

Each robo advisor uses a different investing strategy, so the portfolios generated (and, therefore, your returns) will differ. There are also differences in the experience of using each platform—some are buggy, while others are beautifully designed.

However, we can compare robo advisors in terms of their fees and minimum deposits. The following ones are beginner-friendly as they have low fees and practically no minimum:

- Annual Management Fees

- 0.25% - 0.65%

- Minimum Deposit

- S$0

- Platform Fees

- S$0

Syfe charges a low 0.65% per annum for investments up to S$50,000. The fee goes down as you invest more. There's also no minimum investment amount required.

If your starting capital is small, you can opt for the friendly-looking SqSave. It requires a minimum investment of just S$1, so you can get started with whatever spare cash you have. It's a great beginner option as you can withdraw your funds anytime, and it has a low fee of 0.5% per annum.

Stashaway is the big fish in this space. They are reputable, have a great app interface, and are constantly innovating. You'll often receive breakdowns of their performance and other news via emails. The annual fee is from 0.2% - 0.8% annually, depending on the investment option you choose.

If you're already an OCBC customer, it's super convenient to get on board OCBC RoboInvest. All you have to do is log in to your OCBC Digital app, tap on Invest, and click on RoboInvest. But there is a price to pay (literally) for the convenience: their management fees are among the highest I've seen, at 0.88% per annum.

4. Which robo advisors are more pricey?

While most robo advisers are meant to be entry-level platforms for people who want the simplest possible way to invest their money, some robo advisors are higher-end and more pricey.

AutoWealth is not for true beginners due to its high minimum investment amount. Their main product, AutoWealth Starter Portfolio, requires a S$3,000 deposit. On the other hand, it assigns each user a dedicated wealth manager who can offer support via WhatsApp.

Determining the fees you'll pay for Kristal.AI is a little difficult, as they're not explicitly listed. You'll need to first define your investment portfolio before you can view your "Investment Advisory and Management Services Fees". Judging from its website, I find this robo advisor quite complicated. There are too many portfolio options. I wouldn't recommend it to beginners due to the complexity and unclear fee structure.

Many people have heard about EndowUs thanks to its flagship portfolio, which allows you to invest with your CPF savings. But before you jump into that, learn all about investing your CPF funds in our article here. To get started with EndowUs, you'll need to fund your account with S$1,000 at a minimum.

Just like OCBC RoboInvest, DBS digiPortfolio is really easy to get started with if you're already in the DBS ecosystem. But again, you'll have to pay for the price of convenience. To invest in an international or Asian portfolio of diverse ETFs, you'll be paying 0.75% p.a. in management fees.

@4x.png)

Philip SMART is a robo advisor from a brokerage. If you're planning to build a portfolio of US equities (which is important for diversification), it's going to cost 0.8% p.a. in management fees. That's on the high side.

5. Are robo advisors regulated in Singapore?

In a nutshell, yes, robo advisors are regulated, but they get special leeway from the MAS.

MAS requires robo advisors to be licensed under the Securities and Futures Act (SFA) and/or the Financial Advisers Act (FAA). Which one(s) apply depend on the robo advisor's "scope of activities and business model", but the point is that you should find it in either one or the other.

At the same time, MAS doesn't want to be impede digital innovation, so in Oct 2018, they also loosened the licensing criteria:

Robo advisors can be licensed under the SFA even if they lack the usual corporate track record requirements, provided they have board/senior management members with relevant experience in fund management and technology, offer portfolios that comprise only non-complex collective investment schemes; and submit to an independent audit after the first year.

They can also be licensed under the FAA while being exempt from having to collect full data on a client's financial status. However, they're required to put in some form of data-gathering measure to prevent recommending the wrong types of investments.

Robo advisors also get special leeway to pass their clients' orders to brokerages without having to obtain an additional capital markets services license under the SFA.

These relatively relaxed rules mean it's fairly easy for robo advisors to operate regardless of their performance history, so be careful when choosing one.

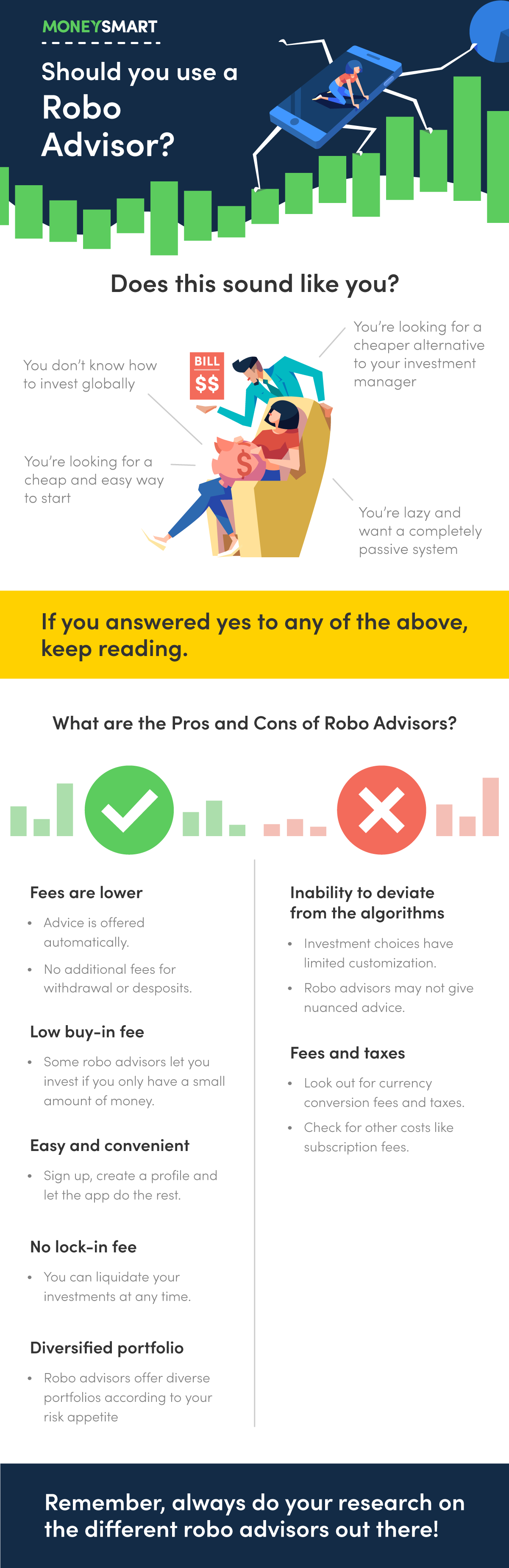

6. What are the pros of using robo advisors?

Technology and investing have always gone hand in hand. Afterall, who wouldn't want advanced algorithms and AI on your side when making investment decisions? Here are some advantages of robo advisors:

Easy and convenient

Ease of use is one big reason people prefer using robo advisors. You don't actually need to research what to invest in, deal with the intricacies of the stock market, submit heaps of paperwork, or even execute the investments yourself. You can simply sign up online, create a profile and let the app do the rest.

Low barrier to entry

Not that much money in your piggy bank? That's OK—many robo advisors let you invest if you only have a small amount of money. This is good for those who want to try investing and not worry about losing a fortune on the stock market.

Can be cost-effective

Robo advisors charge a percentage of the total you invest, so it doesn't matter how big or small or frequent your transactions are. If you're just starting to invest in small amounts to build up a habit of investing, this fee structure can be very forgiving. You also don't get charged for depositing or withdrawing, so you won't lose money to fees unnecessarily.

Customisable to some degree

Thanks to robo advisors’ algorithms, they can offer advice that is customised (to a limited degree) according to your needs. It can take into account details such as risk appetite, income/cash-out needs, financial goals and more, to offer advice fine-tuned to your needs. Of course, don’t forget that the efficacy of the advice given depends on the sophistication of the algorithm.

Diversified portfolio

Maintaining a diversified portfolio is essential to reducing risk, as you won’t go broke if one or two of your assets crash and burn. Robo advisors operate like funds by offering a mix of assets, except that instead of human analysts managing the assets, it’s an algorithm doing the work.

Low commitment

Unlike other investment funds or savings products with lock-in periods, you can choose to liquidate your robo advisor investments at any time with no penalties. There’s nothing stopping you from taking out your funds at any point and switching to another robo advisor if you find a more suitable one later on.

Rebalancing your portfolio is done automatically

Wait, what is rebalancing? Here's a simple way to understand it:

Imagine your investment portfolio is like a garden. You have different types of plants (stocks, bonds, etc.) growing at different rates. Some plants may grow taller and overshadow others, while some may wither away.

Rebalancing your portfolio is like tending to this garden. It involves periodically checking the allocation of your investments and making adjustments to ensure they're still in line with your original plan.

So, if certain investments have grown significantly and now represent a larger portion of your portfolio than you intended (overshadowing the others), you might sell some of those and reinvest the proceeds into other areas that have underperformed. This helps you maintain balance and manage risk according to your investment goals.

Rebalancing is an important part of long-term investing and keeping your portfolio properly diversified. With Robo advisors, it's done automatically for you.

7. What are the cons of using robo advisors?

Of course, it’s not all rainbows and unicorns when it comes to robo advisors. As you get more confident about investing, you'll start noticing their limitations, such as the following:

Inability to deviate from the algorithms

With robo advisors, investment choices are only customisable up to a certain point and cannot deviate from the algorithm’s parameters. So, if you want full control over every single investment decision, robo advisors are probably not the best for you.

More expensive than DIY

While robo advisors generally charge lower fees than investment managers, you might still end up paying quite a bit in fees if you invest significant sums. That's because they charge a percentage of your total investment. On the other hand, if you DIY your own investment portfolio, you only get charged per transaction. That might work out cheaper for buy-and-hold investors.

Some people stick with robo advisors for years simply because you can't beat their ease of use and intuitive platforms. But if you're interested in DIY investing, here are some articles you might find useful:

- Which Investing Strategy Is Suitable for You? Find Out With These 5 Simple Questions

- “How Should I Invest $100k?”: We Rate Advice From Reddit

- Which Investment Brokerage in Singapore is Best? Here's How to Decide

- Top 10 ETFs in Singapore — The Total Beginner’s Guide to Investing in ETFs

8. What sorts of investors are robo advisors suitable for?

As you can see, there are some disadvantages mixed in with the advantages. So what kind of person are robo advisors ideal for? Well, you might want to consider using one of the following apply to you:

You don’t know how to invest globally

One reason robo advisors have become so popular is that they offer an “investment for dummies” experience for those who have no idea how to get started. They’re easy to use and require no knowledge of how global stock markets work. You just transfer your money, let the robo advisor invest using their algorithm and hope your wealth grows.

You are lazy and want a completely passive system

No matter how much or how little you know about investing, if you’re so lazy that you wouldn’t lift a finger to invest if someone didn’t do it for you, robo advisors can manage your investments with almost zero effort. Rebalancing can also be done automatically. Just know that you’re paying a price for the convenience.

You’re looking for a lower cost alternative to your investment manager

If you’re already using an existing investment manager and haven’t been too pleased with their performance or think their fees are too high, you might want to consider switching to a robo advisor.

If you know any lazy investors looking to grow their savings, share this article with them!

Related Articles