Lazy wannabe “investors", rejoice! DBS has now made its robo advisor (called DBS digiPortfolio) available to the public. Previously, it was available only to DBS ~Wealth~ customers.

Now, if you do most of your banking through DBS because you’re lazy (cough, me) and cannot remember more than one login ID to save your life (also guilty), this is a great development.

The DBS digiPortfolio is a very welcome addition to their investment offerings, namely, the expensive DBS Vickers brokerage and the cheaper-but-very-limited regular savings plan.

Now that DBS has launched its own robo advisor, n00b investors can dip their toes in passive investing for relatively low fees and a high level of convenience.

Disclaimer: This article is purely my opinion. As with all my other opinions on things like Daiso products, it's mostly for fun and should not be confused with "financial advice".

First, here’s how to register for DBS digiPortfolio

Getting your DBS digiPortfolio is a fuss-free process. All it takes is 5 clicks, to be exact.

Log in to DBS ibanking, click on the “Invest” tab and then go to “digiPortfolio”. From here, you can read about the robo advisor service, how it works and what the options are.

If you don’t have access, the DBS digiPortfolio page has quite a lot of info anyway. However, you will need access to the platform to deep-dive into the assets that make up each portfolio,.

What are DBS digiPortfolio’s fees & minimum investment?

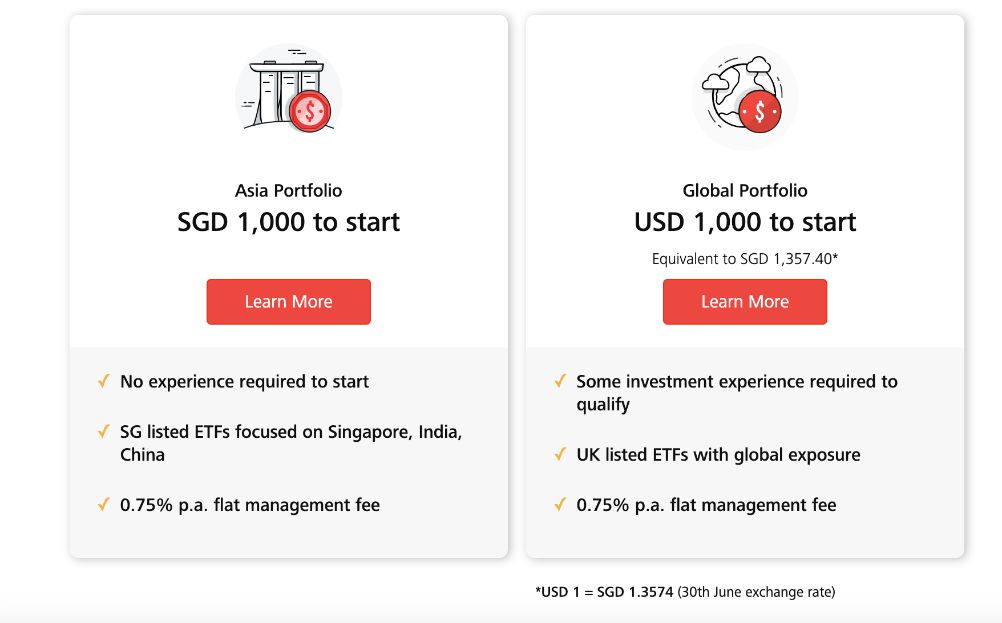

The minimum investment amount for DBS digiPortfolio depends on whether you opt for the Asia portfolio (S$1,000) or global portfolio (US$1,000), which is reasonable I think.

As for fees, DBS digiPortfolio claims to charge a 0.75% p.a. flat management fee regardless of how much or how little you invest.

If you’ve been monitoring the robo advisor scene in Singapore, you’ll realise that 0.75% is one of the lowest around. Here’s a comparison of popular robo advisor fees. To illustrate the actual cost of these fees, the amount in brackets is how much you’re paying every year just to invest.

Robo advisor | Fees per year (for $10,000) | Minimum investment |

DBS digiPortfolio | 0.75% ($75) | S$1,000 or US$1,000 |

AutoWealth | 0.5% + US$18 (~$75) | S$3,000 |

Stashaway | 0.8% ($80) | None |

OCBC RoboInvest | 0.88% ($88) | US$2,500 |

UTrade Robo | 0.88% ($88) | S$5,000 |

Syfe | 0.65% ($65) | None |

To me, robo advisors are like toilet paper. I don’t care about how well its engineered or whether it’s covered in Tsum Tsum characters — any brand will do. I just choose whatever is cheapest.

And since it’s one of the lower cost robo advisors in Singapore right now, the DBS digiPortfolio is one TP that’s definitely worthy of consideration. That said, it’s still more expensive than going the DIY route (more on that later).

Should you choose the DBS Asia portfolio or global portfolio?

Assuming you’re okay with the fees and all, the next decision is to decide between the “Asia” vs “global” portfolios.

Both portfolios are all-ETF (exchange traded fund) portfolios, which is common to almost all robo advisors. ETFs are like those sushi platters with a little bit of everything; they’re supposed to be crowd-pleasing, relatively failsafe, and cost-effective.

However, the Asia one requires no prior investing experience, whereas the global one is more advanced.

The DBS Asia portfolio is actually very, very local — actually, it’s more like a Singapore portfolio with some token Asia exposure in there. It’s mainly driven by familiar instruments like the STI ETF and Singapore bond ETFs. (“I heard of it before, so it must be safe…”)

If you’re new to investing and hesitant to venture beyond your comfort zone of fixed deposits and Singapore Savings Bonds, this portfolio is a nice place to start.

The DBS global portfolio, on the other hand, requires some experience. As with most robo advisor portfolios, it’s in USD and you’d be investing in the US and Europe markets. Therefore, you’re exposed to both forex and global economy risks.

It’s worth noting that DBS’ global instruments are UK listed rather than US listed (like those with Stashaway for instance). This neatly avoids tax problems associated with the US market.

With both portfolios, the fees are the same, and dividends are re-invested into the portfolio for compounding purposes.

Let’s take a look at DBS digiPortfolio’s Asia portfolio

The Asia portfolio will definitely be of interest to a lot of Singaporean investors. Most of us have a lot of faith in the strength of Singapore’s economy and want to invest in our motherland, yet it’s scary to have to pick our own local stocks.

The DBS digiPortfolio’s Asia portfolio takes the analysis paralysis away by not giving you a choice. You just have to pick 1 of 3 risk levels: Slow & Steady, Comfy Cruisin’ and Fast & Furious (in ascending order of risk/return).

Again, all portfolios are ETF-only, so the main difference is in what asset classes these ETFs are in. The lower the risk, the more of the portfolio would be in bonds (technically “fixed income”), while the higher the risk, the more is in equity i.e. company shares.

Here’s a breakdown of what ETFs are in each variation.

DBS digiPortfolio: Asia Portfolio (Slow & Steady / Level 2)

Weightage | Asset | ETFs |

18% | Equity | Nikko STI ETF, Nikko StraitsTrading ex. Japan REIT, Xtrackers MSCI China ETF, Lion-OCBC Hang Seng Tech ETF |

78% | Bonds | ABF Singapore Bond Index Fund, Nikko SGD Investment Grade Corporate Bond ETF |

4% | Cash | — |

DBS digiPortfolio: Asia Portfolio (Comfy Cruisin’ / Level 3)

Weightage | Asset | ETFs |

53% | Equity | Nikko STI ETF, Nikko StraitsTrading ex. Japan REIT, Xtrackers MSCI China, iShares MSCI China ETF, Lion-OCBC Hang Seng Tech ETF |

43% | Bonds | ABF Singapore Bond Index Fund, Nikko SGD Investment Grade Corporate Bond ETF |

4% | Cash | — |

DBS digiPortfolio: Asia Portfolio (Fast & Furious / Level 4)

Weightage | Asset | ETFs |

78% | Equity | Nikko STI ETF, Nikko StraitsTrading ex. Japan REIT, Xtrackers MSCI China, iShares MSCI China ETF, Lion-OCBC Hang Seng Tech ETF |

18% | Bonds | Nikko SGD Investment Grade Corporate Bond ETF |

4% | Cash | — |

Note that all portfolios contain 4% cash to “take advantage of market opportunities & cover annual management fee”. I don’t like it either.

What about DBS digiPortfolio’s global portfolio?

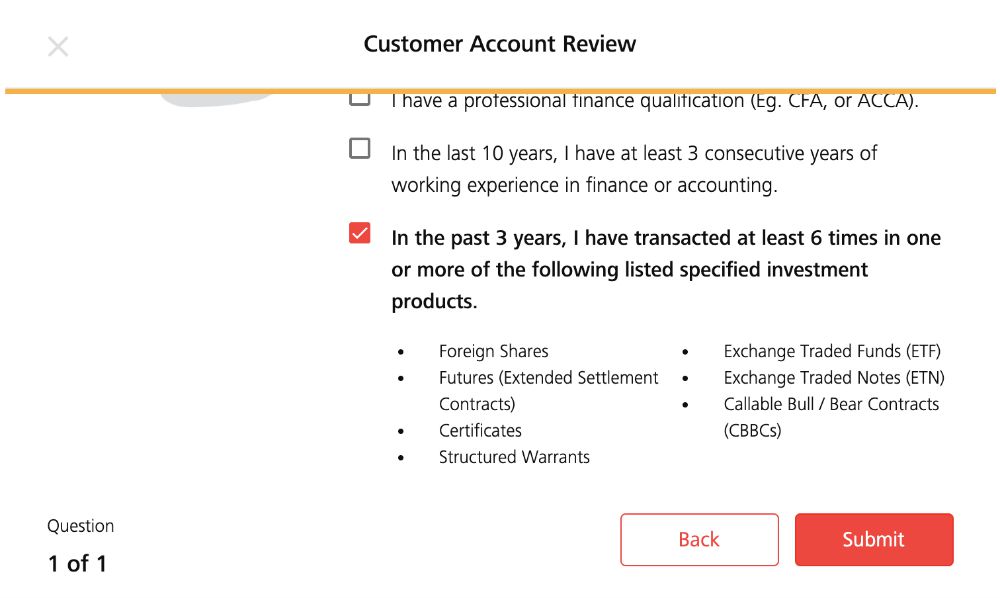

The global version of DBS digiPortfolio is denominated in USD, and the minimum is US$1,000 instead of S$1,000. It’s also recommended that you have some investment experience. You’ll have to pass the following 1-question “test” before you can open the portfolio.

Similar to the Asia portfolio, the global digiPortfolio comes in 3 risk “flavours”. For each risk level, the allocation of bonds vs equity is exactly the same as the Asia one.

What’s different are the ETFs that make up the portfolios, which I’ve listed here:

DBS digiPortfolio: Global Portfolio (Slow & Steady / Level 2)

Weightage | Asset | ETFs |

20% | Equity | iShares MSCI World ETF, iShares MSCI China A, VanEck Vectors Gold Miners |

75% | Bonds | iShares JP Morgan USD EM Bond, iShares Global Corporate Bond, iShares Core Global Aggregate Bond, Vanguard 1-3Y USD Corp Bond |

5% | Cash | — |

DBS digiPortfolio: Global Portfolio (Comfy Cruisin’ / Level 3)

Weightage | Asset | ETFs |

55% | Equity | iShares Core S&P 500, Xtrackers MSCI Europe, HSBC MSCI AC Far East Ex. Japan, Vanguard FTSE Japan, iShares MSCI China A, VanEck Vectors Gold Miners |

40% | Bonds | iShares JP Morgan $ EM Bond, iShares Global Corporate Bond, iShares Core Global Aggregate Bond, Vanguard 1-3Y USD Corp Bond |

5% | Cash | — |

DBS digiPortfolio: Asia Portfolio (Fast & Furious / Level 4)

Weightage | Asset | ETFs |

80% | Equity | iShares Core S&P 500, Xtrackers MSCI Europe, HSBC MSCI AC Far East Ex. Japan, Vanguard FTSE Japan, iShares MSCI China A, VanEck Vectors Gold Miners |

15% | Bonds | iShares Core Global Aggregate Bond, iShares Global Corp Bond, iShares JPM USD EM Corp Bond, Vanguard 1-3Y USD Corp Bond |

5% | Cash | — |

Do we really need to know what ETFs are in there?

While compiling the different portfolio allocations, it struck me that DBS is unusually upfront about the specific ETFs that comprise each investment portfolio.

This is different from most other robo advisors I’ve looked at recently. Most robos avoid telling you what exactly they’re investing in.

In fact, I’ve been investing with Stashaway for a few months and didn’t even know what the ETFs making up my portfolio are. It’s possible to find the list with a few taps, of course, but they don’t put it front and centre.

I am all in favour of transparency and knowing what you’re getting into, so I’m glad that DBS publishes the ETFs way up front. If you wish, you can find out more about each ETF online.

If you’re using a robo advisor like Stashaway, should you switch?

With robo advisors, the key selling points are (a) no need to use brain and (b) fees are affordable.

For (a), I’ve always thought that Stashaway was the height of simplicity, but the geniuses at DBS have somehow created a product even more brainless.

Assuming you already have a multi-currency DBS bank account (the DBS Multiplier account works), you can start investing in just a couple of clicks; no need to PayNow or anything. For the global portfolio, there is an extra step: You need to do an internal transfer of SGD to USD, then fund the account.

As for (b), I don’t know how well either robo will perform in the long run, but the way I look at it, DBS’s 0.75% fee already gives you a slight head start over Stashaway’s 0.8%.

Of course, each ETF itself has management fees (which are an extra cost to the investor), but I am assuming that the ETFs these robos chose are all low-fee ones.

If you want to research the individual ETFs that comprise your portfolio, it's slightly easier to do so with DBS: Each portfolio has 4 to 7 ETFs, mostly generic ETFs that track entire markets. My Stashaway equity portfolio is more fine-grained, with 9 ETFs in total, including several sector-specific ones in the US.

Finally, if you’re interested in a brainless way to invest in Singapore / Asia ETFs, DBS digiPortfolio has a much better range than most robo advisors, which deal mainly in US-listed stuff.

TL;DR: Yes. Compared to other robo advisors on the market, DBS digiPortfolio is easy to use, cheaper, simple, and has good options for local investments.

Can DBS digiPortfolio hold a candle to DIY passive investing?

Lest I sound like I’m being paid by DBS to write this thing, I will now talk about the biggest downside of their robo advisor (applies to all robo advisors): The cost.

Yes, DBS digiPortfolio may cost a lot less than, say, Stashaway, but it still cannot beat DIY passive investing through a well-chosen investment brokerage.

Let’s say you’ve saved up about $10,000 to put into passive, long-term investments. If you open a DBS portfolio, that’s 0.75% p.a. in fees, which is about $75 a year. This is a recurring cost every year even if you buy and hold the investment.

However, you can easily buy the ETFs a la carte via any investment brokerage. Saxo Capital’s fees are some of the cheapest at 0.08% per trade, minimum $10.

- Min. Commission Fee US Stocks

- US$1

- Min. Commission Fee SG Stocks

- S$3

- Min. Funding

- S$0

[SmartRewards | MoneySmart Exclusive]

Get S$180 Cash via PayNow

• OR Apple AirPods 4 (worth S$199)

• OR Sennheiser Accentum Plus Wireless Headphones (worth S$349)

• OR TT Racing Swift X Pro Chair (worth S$429)

OR choose from many more rewards when you deposit a min. of S$3,000, maintain the funds for 30 days, and execute 1 trade within 14 days of account opening.

T&Cs apply.

Use SmartPoints to redeem your favourite product from our Rewards Store today.

There’s nothing stopping you from doing a copycat and buying Nikko STI ETF, Nikko AM StraitsTrading ex. Japan REIT, Xtrackers MSCI China + Nikko AM Investment Grade Corporate Bond ETF on Saxo. The total cost will be $40 ($10 x 4), and there will be no recurring cost year after year.

If you are investing in global stocks, you can do the same, just note that different fees may apply. Some brokers’ fees for overseas investments can be even lower than that of local ones. Saxo also charges US$12 a year as custody fees, so that’s a recurring cost to consider.

TL;DR: No. A $10,000 investment costs $75 a year with DBS, but if you DIY, it can cost as little as $40 with little or no recurring fees. That’s almost half the cost. Remember what I said about toilet paper…?

DBS digiPortfolio might be good for investing in drips and drabs

Despite the higher-than-DIY fees, I'm drawn to robo advisors because they typically make it easy to enter and exit your investments.

Many allow you to top up your portfolio, withdraw cash, do dollar-cost averaging by investing $100 every week... Basically, you can do whatever you like without worrying about the cost of each transaction.

With a non-robo investment brokerage, on the other hand, you’re charged per transaction instead of on the investment amount. That means you have to fork out that $10 commission fee every time you buy or sell something. If you’re prone to doing that a lot, then going DIY won’t work; it’ll be way too expensive.

Another "pro" is that consistent portfolio monitoring, rebalancing and tweaking is included in the cost of the robo advisor. If you were to do that in your DIY portfolio, again, the transaction fees will add up.

(I put "pro" in quotation marks because I personally dislike the idea of fiddling too much in a passive investment strategy, but you know, whatever floats your boat.)

Tried the new DBS robo advisor yet? What do you think?

Visit MoneySmart's curated list of Best Singapore Robo Advisors 2020 and start investing today

Related Articles