When I think "groundbreaking”, I think of Marvel and the first Guardians of the Galaxy movie, which starred a talking raccoon and a walking tree and still managed to pocket US$773.3 million at the worldwide box office to become 2014's #1 superhero film.

When I think groundbreaking, I don’t think of the FHR, a DBS home loan that is leading the wave of Fixed Deposit-linked home loans from banks.

But DBS has definitely broken some new ground by introducing their Fixed Deposit Home Rate, or FHR.

Since 2014, this DBS home loan rate has become the preferred alternative to the Singapore Interbank Offered Rate, or SIBOR, spawning similar products like FDPR (the UOB home loan rate) and FDR (the Standard Chartered home loan).

What is FHR based on?

DBS is now offering the FHR6 package, which is essentially the 6-month S$ Fixed Deposit (FD) rate, which currently stands at 1.4%.

DBS has also added a new product, CHR, for CPF Home Rate. The CHR is based on the CPF Ordinary Account interest rate, which is currently 2.5%.

Over the years, DBS has changed the benchmark for their home loan rates. The previous packages were based on FHR8, FHR9 (which used the 9-month S$ Fixed Deposit rate of 0.25%), and the FHR18 (used to be 0.6% pre-2018).

When it was first introduced, the formula used for calculating the FHR was an average of the bank’s 12-month and 24-month Fixed Deposit (FD) rates in SGD. We're talking about an original FHR of 0.4% back then!

Customers who had previously signed up for a package on the old rates will still have their interest rate based on the old calculation method.

So why is FHR a board rate?

Unlike the SIBOR, the FHR (whether it's FHR8, FHR9 or FHR18) is still considered a board rate because it is internally determined, but it is a bit of a hybrid in this sense.

DBS still reserves the sole right to adjust the rate as and when it pleases, by adjusting their Singapore dollar fixed deposit rates.

Unlike other banks’ board rates, which have no transparency when it comes to how it is determined, DBS has pegged the FHR solely to their own internally determined FD interest rates.

However, it's important to note that ultimately, Fixed Deposit rates are controlled by the Monetary Authority of Singapore (MAS). This is a monetary policy that provides a floor and ceiling to the banks to keep the Fixed Deposit rates in control. So in this regard, the rates are semi-transparent in that the banks still publish their rates, but there is a margin by which they can adjust the rates.

What are the advantages of a DBS home loan like the FHR?

The FHR6 is relatively easy to calculate. It's simply the 6-month DBS bank Fixed Deposit interest rate, and it is openly published on the bank’s website.

In contrast, the former SIBOR was determined by at least 8 banks and changes on a daily basis.

It is also good business sense that DBS will want to keep its Fixed Deposit interest rates low, since they represent a cost to the bank.

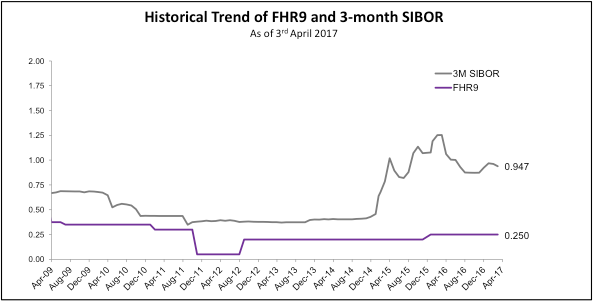

For example, here's a historical chart of the FHR9 versus the 3-month SIBOR just to give you an idea of the fluctuations.

Source: DBS

Are there any disadvantages of FHR?

Just because the bank says that the board rates have not changed in the past whatever number of years, they continue to have every right to adjust them, anytime they want to.

The FHR is a board rate. It is much more transparent than other banks’ board rates, but it is still a board rate. Even if it means incurring a cost by raising their fixed deposit interest rates, there is nothing to stop DBS from increasing it as and when they need to.

As Warren Buffett famously said, “Risk comes from not knowing what you're doing”.

DBS is saving you the stress of figuring out the SIBOR (and all its permutations) and how it can affect your DBS home loan. They want you to choose the simpler, more straightforward option they propose, a rate that is easily calculated.

But unless you’re a child playing Monopoly, you shouldn’t be making a decision about your money solely based on how easy the options are to understand.

Is FHR better than other banks’ board rates?

This is something that's very subjective. There is a transparency in how the FHR is calculated, one that is pegged to information about the bank’s FD interest rates that is readily available online.

As we mentioned above, the popularity of the DBS home loan led to other banks like UOB creating their own version of the fixed deposit-linked home loan rate.

As of September 2022, the FHR6 DBS home loan package is at FHR6 + 1.3% = 2.7%.

Still can’t decide between FHR and fixed home loans? Find the best DBS home loan interest rates here!

Image Credits: Choo Yut Shing