So interest rates have been on the rise and you, a home owner, are in a real pickle. Do you stick out your feelers for a refinancing option for your home loan and attempt to lock in a more attractive interest rate OR cower and kowtow to the interest rates gods?

Unfortunately, the latter might be a situation rather than an option for some, especially for those saddled with bad debts, defaults or heavy financial obligations. And when credit facilities close off due to high outstanding balances and late payments, consumers who want to rebuild their credit again might find themselves trapped in a vicious cycle.

How do you attain a new credit when you do not hold any active credit…which is the only way to prove you have learned to manage credit?

But there’s light at the end of the tunnel. A bad credit score can be fixed. And your dream house doesn’t have to remain a dream.

In this article, we give you the lowdown on improving credit scores, refinancing home loans, and taking charge of your credit.

ALSO READ: Refinance Home Loan in Singapore

First things first, how does a poor credit score affect your home loan application?

When submitting an application to refinance your existing loan, the lender will conduct a risk assessment on you by understanding your income versus debt. The credit report is a widely-used tool to understand a consumer’s risk level as a borrower.

To enjoy the lowest rate package, a good credit record is fundamental. In other words, a consumer’s poor credit score can deter a lender from granting him or her a refinancing of his or her home loan, hence subjecting the borrower to high interest rates until the credit score is improved, or when the interest rates are cut.

Generally, home loans from the banks have a 2 to 3 year lock-in period. The rates after the lock-in period will typically be higher and prompt consumers to refinance to a lower home loan package.

Wait, how do I check my credit score for real estate loans?

To get a copy of your credit report, visit the Credit Bureau website.

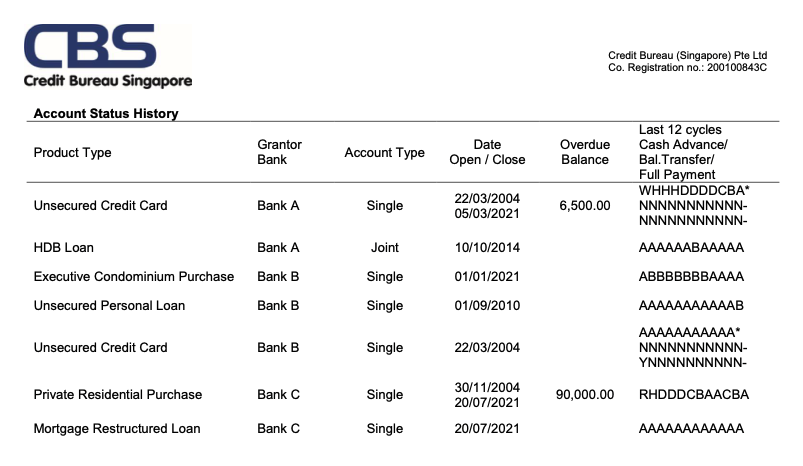

Under the account status history section of your consumer credit report generated by Credit Bureau Singapore, real estate loans are categorised into 3 groups: HDB Loan, Executive Condominium Purchase and Private Residential Purchase. The section displays information on the last 12 months of repayment made by the consumer, including the monthly instalments paid by the due date, and those made after.

Photo: Credit Bureau Singapore

When a consumer struggles with punctual home loan repayment, the account status starts to deteriorate from “A” to “W”. Over 12 cycles of payment pattern, Credit Bureau Singapore is able to observe the possibility of the consumer defaulting on the loan or requiring a loan restructure.

ALSO READ: Credit Bureau Singapore: How to Get Your Credit Score and Credit Report

Oh right, back to the tough part. Trying to rebuild your credit? Start with these helpful tips:

Start with credit facilities with a low credit limit

If applying for new credit facilities has become challenging because of your deteriorated credit score, you might want to try two things: 1) unsecured credit cards with a low credit limit or 2) secured credit cards. It might seem daunting to open new credit cards on a bad score but take this as your first step to rebuilding your credit reputation.

To learn how secured credit cards work and about the best ones in town, check out our list of Best Secured Credit Cards for Bad Credit in Singapore (2023).

Don’t go overboard though!

Applying for too many credit cards within a short span of time can be harmful to your credit score. Banks can sometimes misinterpret a hunger for credit as a sign of financial difficulties. While there is no hard and fast rule on how much you should space out credit card applications, we’d suggest leaving a breathing room of about 90 days.

Always pay the full outstanding amount by the due date

Sure, maybe you can count on your friends to forgive you when you’re chronically 15 minutes late for every brunch meeting. But banks aren’t as kind. Believe us when we say, it pays to be punctual when trying to maintain a good credit score or rebuild one.

If punctuality remains an issue for you, consider setting up automatic payment systems and/or reminder alerts to help you keep up.

Even if you can’t pay in full, try to pay as much as you can and meet the minimum payment amount. At the very least, we want to avoid incurring any late payment penalties.

Always check your credit reports and rectify errors

You are the master of your finances. If you sense something amiss that could be pulling your score down, flag it up to your credit reporting company and/or bank right away. At Credit Bureau Singapore, the organisation will process your request and carry out an investigation. If the investigation uncovers an error in your personal profile, the Bureau will amend your information immediately.

But if the disagreement is in the credit data, Credit Bureau Singapore will consult with the data source and inform you of the progress and outcome of the investigation. Should an error be uncovered and rectified, the revised report will be sent to all Bureau members who have made enquiries on you in the last 12 months to inform them of the amendment in your credit report.

Don’t just work hard, work smart

Bear in mind that using a debit or prepaid card to repay debts will not impact your credit score, so don't waste your effort with them. Both debit and prepaid cards do not operate based on credit, meaning that you don’t need a credit score to obtain one, and your account activity isn't reported to the credit bureau.

Last words

A bad credit score can take away the perks we enjoy in life, from big ticket items like home and car purchases to small items like lifestyle credit cards (with free airport lounge access and dining discounts)! And much like repairing a soured relationship, rebuilding a credit score can take months, even years. But, it has to start somewhere. The keywords are: prompt payment patterns, discipline, and consistency.

Found this article useful? Share it with your family, friends, and colleagues.