Despite prices almost doubling over the past decade—from around $800 to $1,500 psf—executive condominiums (ECs) remain one of Singapore’s most sought-after property types.

A recent study by NUS’s Institute of Real Estate and Urban Studies (Ireus) found that 4 in 5 property players still see ECs as highly desirable. These public-private hybrids often outperform other private homes in resale profits, with some units reselling at double their original purchase price.

ECs offer private condo-style features—pools, gyms, and security—but are sold through HDB and come with CPF housing grants. For the first 5 years, they can only be sold to Singapore Citizens or Permanent Residents who meet HDB eligibility. After 10 years, ECs become fully private and can be sold to anyone, including foreigners.

Thinking of buying an EC in 2025? This guide covers everything you need to know—from eligibility and CPF grants to downpayment schedules, resale rules, and beyond.

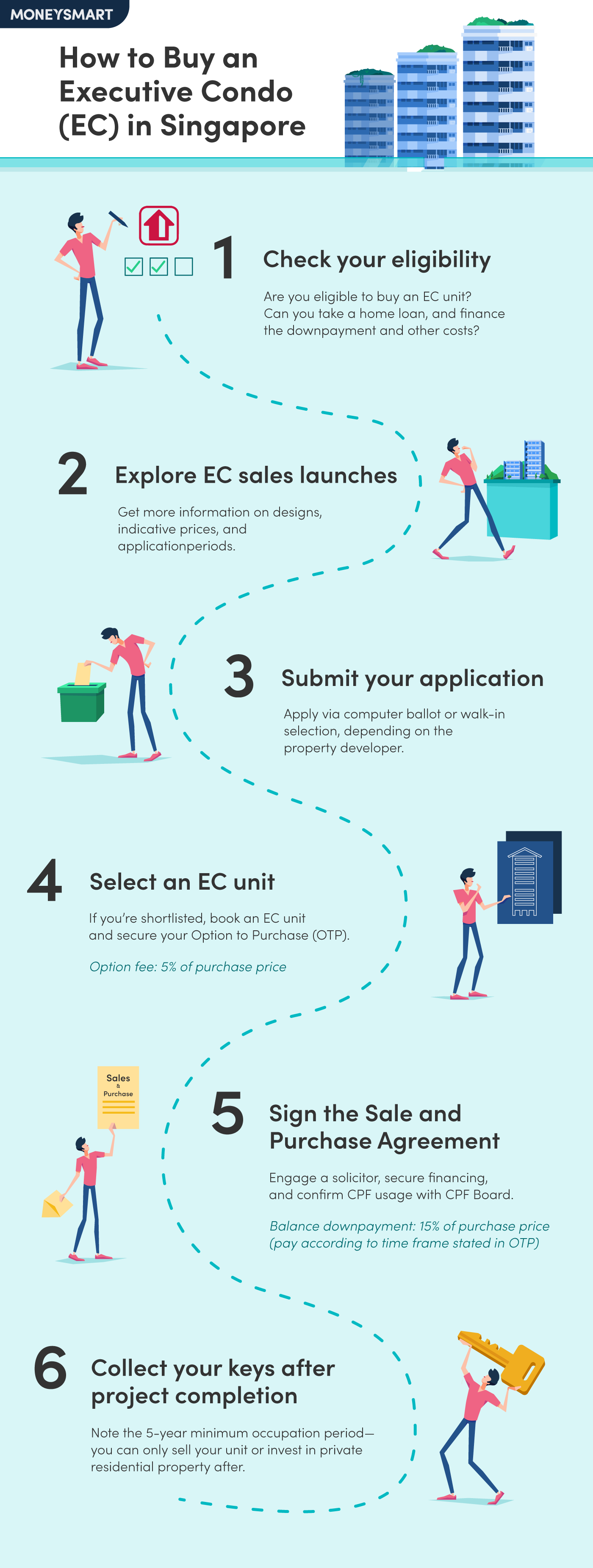

Summary: 6 steps to buying an Executive Condominium (EC)

Stage | What to do | Payments needed |

|---|---|---|

1. Check your eligibility | Ensure you meet HDB rules for household type, citizenship, age, and income | None |

2. Explore EC launches | Research new projects, layouts, indicative pricing, and launch dates | None |

3. Submit your application | Apply to the developer; may involve balloting or walk-in selection | None |

4. Select an EC unit | Book your preferred unit and receive Option to Purchase (OTP) | 5% option fee (via cash or CPF) |

5. Sign the S&P agreement | Engage solicitor, confirm loan, use CPF and arrange payment | 15% downpayment, legal and stamp fees |

6. Collect your keys | Move in after project completion; follow MOP and resale rules | Remaining payments per loan schedule |

Step 1: Check your eligibility

Payment required: None

Before you can buy an EC, you’ll need to meet a specific set of eligibility criteria set by HDB. These cover everything from household composition and citizenship to age and income ceiling.

Criteria | Requirement |

|---|---|

Household type | Must fall under 1 of 6 recognised family or joint singles structures |

Citizenship | 1 Singapore Citizen (SC) + at least 1 other SC or Singapore Permanent Resident (SPR) |

Age | At least 21 years old (35 if applying as joint singles) |

Income ceiling | Total monthly household income ≤ $16,000 |

Household type

Your household must fit one of the following types:

- You and your fiancé or fiancée

- You, your spouse, and child(ren)

- You, your parents, and siblings

- If you’re single/divorced/widowed, at least 1 parent must be an SC or SPR

- You and your child(ren) under legal custody, care, and control

- If custody is shared with an ex-spouse, written consent is required to include your child

- You and your single siblings (if both parents are deceased)

- All siblings must apply together and not own/apply for another flat separately

- At least 1 deceased parent must have been an SC or SPR

- You and up to 3 other singles (all must be unmarried/divorced/widowed)

- Divorced or widowed persons with children who can form a family unit do not qualify under this category

Citizenship requirements

- For fiancé/fiancée pairs, married couples, and family groups:

You must be a Singapore Citizen and include at least 1 other SC or Singapore Permanent Resident (SPR) - For joint singles (up to 4 applicants):

All applicants must be Singapore Citizens

Age requirements

- Most applicants must be at least 21 years old

- If applying as a group of joint singles, each person must be at least 35 years old

Monthly household income ceiling

Your total monthly household income, including all listed applicants, must not exceed $16,000.

Loan eligibility

While no payments are required at this stage, you should:

- Check that you can take a housing loan from a financial institution

- Assess your financial situation to be sure you can afford the downpayment, fees, and loan payments to follow

Step 2: Explore EC sales launches

Payment required: None

This is the fun part—browsing new EC projects and visualising your future home. Property developers typically announce upcoming EC launches through newspapers, social media, their official websites, and property portals.

Once a launch is announced, it’s worth reaching out to the developer or their appointed marketing agents to learn more. This can help you evaluate whether the project fits your needs and budget before the booking period begins.

Here’s what you can find out:

- Preliminary designs: See layout options, floor plans, and artist impressions of the units and common areas.

- Total number of units available: Projects typically range from a few hundred to over a thousand units, across various configurations (e.g. 3-, 4-, 5-bedroom units).

- Indicative prices: Early pricing guidance can help you assess affordability before the official price list is released.

- E-application and booking dates: Some ECs require you to submit an e-application before you’re allowed to book a unit. Make a note of the application window and key sales events.

Keep your eyes peeled—EC launches tend to attract high demand, and choice units may be snapped up quickly. For example, last year's Lumina Grand, an EC project in Bukit Batok, saw about 70% of its units sold within a month.

Step 3: Submit your application

Payment required: None

Once you’ve shortlisted an EC project and are ready to take the next step, it’s time to submit your application to the property developer.

The application process is managed directly by the developer, and they will provide instructions on how and when to apply—whether through an online form (e-application) or an in-person submission. You submit your application to the property developer, not HDB.

Developers may choose to allocate units using a computerised ballot—especially when demand is high—or allow buyers to select units on a first-come, first-served walk-in basis.

After you submit your application, the developer will contact you with your result and booking slot (if balloting applies).

Step 4: Select an EC unit

Payment required: Option fee (5% of purchase price)

If your application is successful, congratulations—you’ll be invited to book a unit. This is when things start to feel real.

The property developer will contact you to schedule your booking appointment. During this session, you’ll choose your preferred unit (subject to availability) and be issued an Option to Purchase (OTP) if you’re eligible. The OTP helps you secure your unit, and requires you to pay an option fee of 5% of the purchase price. This amount will go toward your final purchase (i.e. it will offset the purchase price).

The option fee is payable via:

- Cashier’s order

- Cheque

- Telegraphic transfer

- FAST (Fast and Secure Transfers)

- MAS Electronic Payment System (MEPS)

- GIRO (General Interbank Recurring Order)

If you're applying for a CPF Housing Grant

You must submit the following directly to the property developer:

- Completed EC application form

- CPF Housing Grant application form

- All required supporting documents (e.g. income statements, proof of eligibility)

Be sure to prepare your documents in advance—processing timelines can vary, and any missing paperwork could delay your booking.

ALSO READ: Buying a House? Here are 8 Terms You Need to Know Before You Meet Your Realtor

Step 5: Sign the Sale and Purchase Agreement

Payment required: Balance downpayment (15% of purchase price, to be paid according to time frame stated in OTP)

Once you’ve secured your unit with an Option to Purchase (OTP), the property developer will invite you to sign the Sale and Purchase (S&P) Agreement. This is a key legal milestone in your EC journey—it formalises the purchase and kicks off financing, legal, and payment procedures.

Key next steps:

- Engage a solicitor: Appoint a licensed solicitor to handle conveyancing and guide you through the legal documentation.

- Arrange financing: Coordinate with a bank or financial institution to secure your home loan. Make sure the loan package complies with the Mortgage Servicing Ratio (MSR) if you're using CPF.

- Check CPF usage: Confirm with CPF Board how much of your CPF Ordinary Account savings can be used toward the downpayment and other fees.

Payments to expect

You'll need to pay the balance downpayment, which is 15% of the unit's purchase price. This payment is due within the timeframe stated in your OTP. It can be made using:

- CPF Ordinary Account savings

- Cash

If you're using the CPF Housing Grant, it will count toward this downpayment. Be sure to inform your solicitor to reflect this in the documentation.

Other payments to expect include:

- Legal fees (payable to your solicitor)

- Stamp duty and registration fees (required for legal documentation)

These fees can be paid using CPF savings (if eligible) or cash. Always consult your solicitor or lender to confirm the exact amounts and payment methods.

Step 6: Collect your keys

Payment required: Remaining payments per loan schedule

Once the project is completed and you've fulfilled all financial and legal requirements, it’s time for the big moment—collecting your keys.

This marks the start of your home ownership journey, but it also comes with important restrictions to keep in mind.

The first thing to take note of is the Minimum Occupation Period (MOP)—the mandatory 5-year period during which EC owners must physically occupy their unit. During this time, you’re not allowed to sell the unit on the open market or invest in other private residential property, be it in Singapore or overseas

Resale restrictions

- After 5 years: You can sell your EC to Singapore Citizens (SCs) or Singapore Permanent Residents (SPRs) who meet eligibility conditions.

- After 10 years: Your EC becomes fully privatised. At this point, it can be sold to anyone, including foreigners, and is no longer subject to HDB regulations.

Rental restrictions

- Renting out the entire unit: Not allowed during the 5-year MOP.

- Renting out individual rooms: Permitted without prior approval from HDB. However, you must:

- Register the rental of bedrooms within 7 days of tenancy

- Notify HDB of tenancy renewals, terminations, or any changes in tenant details

Understanding these timelines is crucial if you’re thinking long-term—whether it’s for investment, future upgrading, or rental opportunities.

How much CPF Housing Grant can I get for an EC?

If you meet the eligibility requirements, you can also enjoy a housing subsidy of up to $30,000 when you buy an EC. How much grant you receive depends on your gross monthly household income.

- Gross monthly household income is $10,000 or lower: you will receive the maximum CPF Housing Grant for your household type.

- Gross monthly household income exceeds $12,000: you will not receive any CPF Housing Grant.

- Gross monthly household income is $16,000 or higher: you are not eligible to buy an EC.

Here's a breakdown:

First-timer households

Average gross monthly household income of all persons in the EC application | CPF Housing Grant amount | |

|---|---|---|

SC/ SC household | SC/ SPR household | |

$10,000 or lower | $30,000 | $20,000 |

$10,001 to $11,000 | $20,000 | $10,000 |

$11,001 to $12,000 | $10,000 | Nil |

$12,001 to $16,000 | Nil | Nil |

First-timer and second-timer couples

Average gross monthly household income of all persons in the EC application | CPF Housing Grant amount |

|---|---|

SC/ SC household | |

$10,000 or lower | $15,000 |

$10,001 to $11,000 | $10,000 |

$11,001 to $12,000 | $5,000 |

$12,001 to $16,000 | Nil |

This article was drafted with the help of AI, and has been reviewed and refined by the author.

Found this article useful? Share it with your family and friends!

Related Articles