Whether you’re buying a Built-To-Order (BTO) flat or a resale flat from HDB, there’s one slightly leh chey thing you’re gonna need to prepare. It’s not a 4-letter word like ABSD (shudders!), but a 3-letter one: HFE.

HFE stands for HDB Flat Eligibility, and is the most important letter you need to purchase a new BTO flat, new Sale of Balance flat, new flat under open booking, or resale flat. Here’s all you need to know about the HDB HFE letter—what it is, who needs it, when you need it, and how to apply for one.

Check out our review of the latest HDB BTO sales launch: HDB BTO Jul 2025 Review—Locations, Resale Values, Amenities, and More

All You Need to Know About the HDB Flat Eligibility (HFE) Letter (2025)

- What is the HFE letter?

- When do I need to apply for an HFE letter?

- How do I apply for an HFE letter?

- When will I receive my HFE letter?

- What’s the difference between the new HFE letter and old HLE letter?

- Is the HFE letter better?

- Wait…I can apply for bank loans on the HDB Flat Portal?

1. What is the HFE letter?

The HFE letter is an all-in-one document that summarises everything you need to know about your eligibility to buy a new/resale flat, get housing grants, and take a HDB housing loan. You apply for it at the very start of your house hunting journey, and can then make use of the letter’s grants, loan, and housing information when you’re choosing a flat.

Aside from the important information it contains on your grants and loan eligibility, the HFE letter is also essential for you to apply for BTO flats during a sales exercise or to get an Option To Purchase (OTP) for a resale flat.

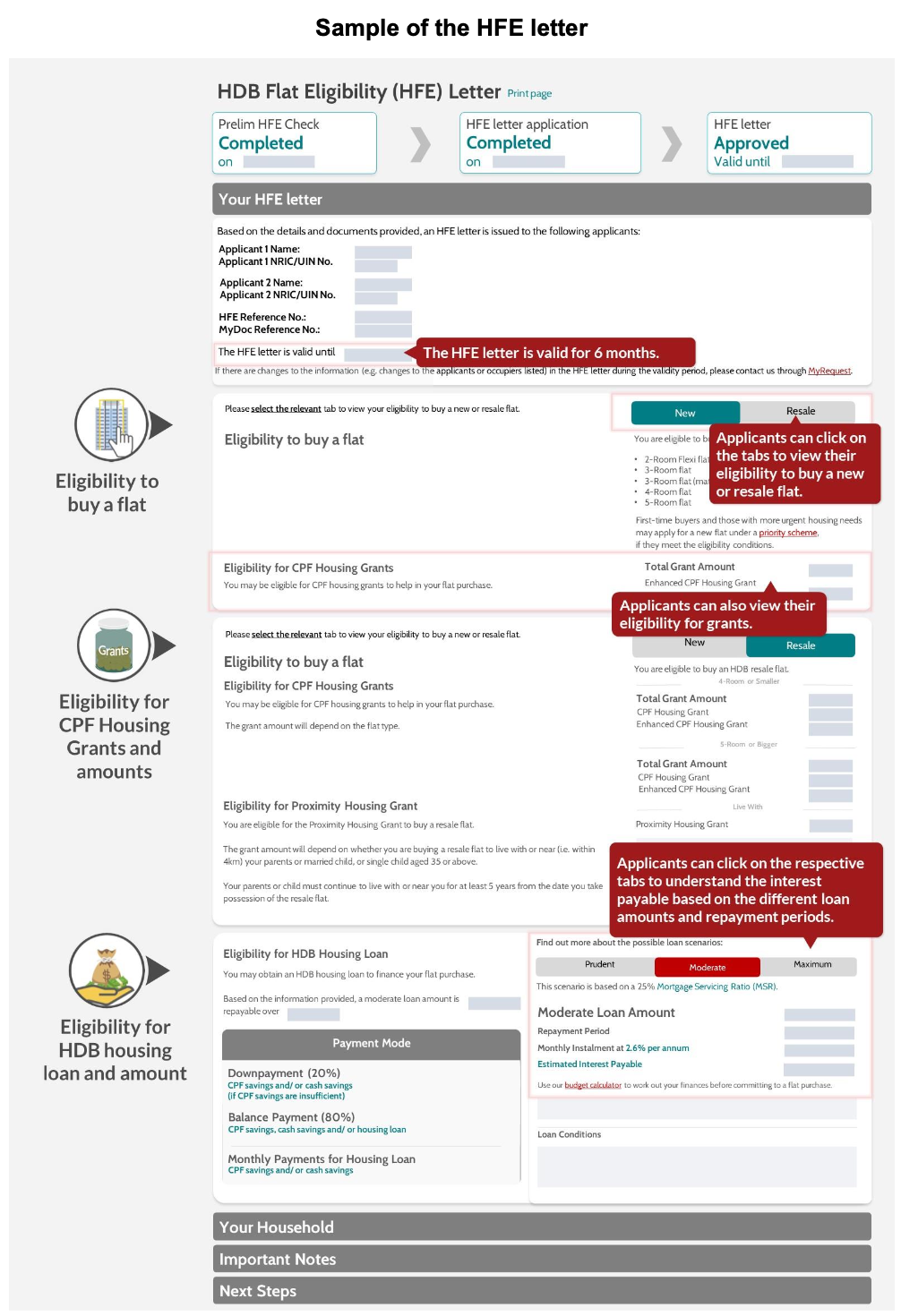

The HFE letter is the new and improved version of the HLE letter, which it officially replaced on 9 May 2023. While the HLE only assessed your eligibility for a HDB housing loan, the HFE looks at your eligibility for flats and grants too. Take a look at this sample HFE letter to see what it covers:

Image: HDB

Note: Although the sample letter above says 6 months, the latest info from HDB's website states that the HFE letter is valid for 9 months from the date it's issued to you.

2. When do I need to apply for an HFE letter?

As long as you’re looking to buy a flat, you need an HFE letter. This applies to:

- New BTO flats

- New Sale of Balance flats

- New flats under open booking

- Resale flats

If you’ve got your heart set on a swanky new flat, HDB usually advises you apply by the 15th of the month before the BTO sales launch. For example, apply by 15 Jun 2025 for the Jul 2025 BTO sales exercise.

If you want to buy a resale flat, you technically only need the HFE letter when you want the OTP for the flat you've decided on. However, getting your HFE preliminary assessment way ahead of looking at any flats is a good way for you to gauge what kind of housing is best for your financial situation.

Plus, if you do see a flat you really like but haven’t submitted your HFE application, you’ll have to wait up to a month or so to receive your HFE letter (longer if it’s a peak period!). So in this sense, it would be prudent to apply for the HFE early—even before you start looking at resale flats for purchase.

There’s no real harm in applying early for the HFE letter. The only possible downside is that the HFE expires after 9 months. So if you’re unlucky enough to be looking for a flat for over 9 months, you’ll need to apply for a new HFE letter.

3. How do I apply for an HFE letter?

Applying for an HFE letter is a 2-step process.

Step 1: Preliminary HFE check (10 minutes)

The first step is a preliminary HFE check, which takes about 10 minutes to complete. It'll tell you your eligibility to buy a flat, receive housing grants, and take up a loan from HDB.

Here's what you need to do:

- Log in to the HDB Flat Portal using Singpass

- Follow the instructions to submit your household particulars and income details

- Declare any private property ownership

- State whether you intend to take up a housing loan.

Once you hit submit, it’s an instant process—you’ll immediately get a preliminary overview of your flat purchase, housing grants, and housing loan eligibility. HDB’s goal here is to quickly share information that can help you roughly map out your housing budget and see what’s feasible for you. However, this preliminary check does not churn out any official HFE letter.

Step 2: Apply for an HFE letter

Ready to buy a flat? Apply for your official HFE letter within 30 days of starting the preliminary HFE check—if you’re late, you have to go back and update the employment details for the people you listed in your application.

To apply for the HFE letter, you should once again log in to the HDB Flat Portal via Singpass. Fill in and declare the information they ask for, such as your 15-month CPF contribution history and latest Notice of Assessment from IRAS. Don’t worry about logging in to your CPF and all that though—this can be a hassle-free process with the help of Myinfo via Singpass.

At this stage, you’ll also be able to compare housing loans from HDB and banks—and even apply for an In-Principle Approval (IPA) for a bank loan via the HDB Flat Portal.

4. When will I receive my HFE letter?

If you submit all your required documents correctly, the waiting time for your HFE letter should be about 1 month from the date HDB receives your application. This may take a little longer during peak periods, such as during and before a sales launch.

Once HDB has processed your HFE letter, you’ll get an SMS notification stating it’s ready. You can then log in to the HDB Flat Portal to view and download it.

5. What’s the difference between the new HFE letter and old HLE letter?

Here’s a quick look at the similarities and differences between the new HFE and its predecessor, the HLE:

New HDB Flat Eligibility (HFE) letter | HDB Loan Eligibility (HLE) letter | |

What information does it contain? |

|

|

When do you apply for it? | At the start of your flat buying journey, before you apply to buy a flat.

|

|

What do you need it for? |

|

|

Is it integrated with the process of securing an IPA for a bank loan? | You can apply for an IPA on the HDB Flat Portal itself when you’re applying for an HFE letter. | Applying for bank loans is a completely separate process from the HLE letter application. You’d need to liaise with the bank directly. |

How long is it valid for? | 9 months from the date of issue | 6 months from date of issue |

What is the period of income assessment? | 12 months, ending 2 months before the month of your HFE letter application. So if you applied for the HFE letter in May 2023, the assessment period is Apr 2022 to Mar 2023. | If you have monthly CPF contributions and a fixed salary: Latest 3 months’ payslips + 15-month CPF contribution history. |

6. Is the HFE letter better than the old HLE letter?

Definitely. The best thing about the new HFE letter is that it streamlines the entire assessment process for buying a flat. It tells you what flats, loans and grants you’re eligible for even before you begin looking for a flat.

Previously, HDB would assess your eligibility to buy a BTO flat at the application stage, but only assess you for housing grants and an HDB housing loan after you get a queue number. And mind you, these assessments were all done via separate applications, each of which you need to dig out a bunch of documents for.

For resale flats, HDB would assess you for flat purchase and housing grants at the flat application stage, then have you submit more documents to assess your loan eligibility before you can get your OTP.

Old HLE process—When you get assessed for your eligibility for: | |||

Flat purchase | Housing grants | HDB housing loan | |

BTO flat buyers | At flat application | At flat booking | At HLE letter application (before booking a flat) |

Resale flat buyers | At flat application | At flat application | At HLE letter application (before obtaining an Option to Purchase) |

Source: HDB

The old process carried uncertainty for the home buyer—how much grant or loan can you get? If you're looking to buy a BTO flat, you'd only know about your grants during the flat booking at HDB Hub. How is one supposed to choose a flat without really knowing their housing budget?

Enter the HFE letter, which tells you upfront which flats you can buy, how much housing grant you can get, and how large a home loan you can take. Here’s what the new process looks like:

New HFE process—When you get assessed for your eligibility for: | |||

Flat purchase | Housing grants | HDB housing loan | |

BTO flat buyers | At HFE letter application, which you must do before you can apply for any BTO during a sales exercise | ||

Resale flat buyers | At HFE letter application, which you can do before you start looking for a resale flat, and must do before you can get an OTP for the flat you want. | ||

The HFE letter is far more streamlined and comprehensive than the HLE letter. It asks for all the information needed to assess you upfront, and also gives you your flat purchase, grants and loan eligibility information upfront. The new system prepares you for your housing and home financing decisions right from the get-go—a vast improvement from the previous system that had flat buyers asking “now what?” at each stage.

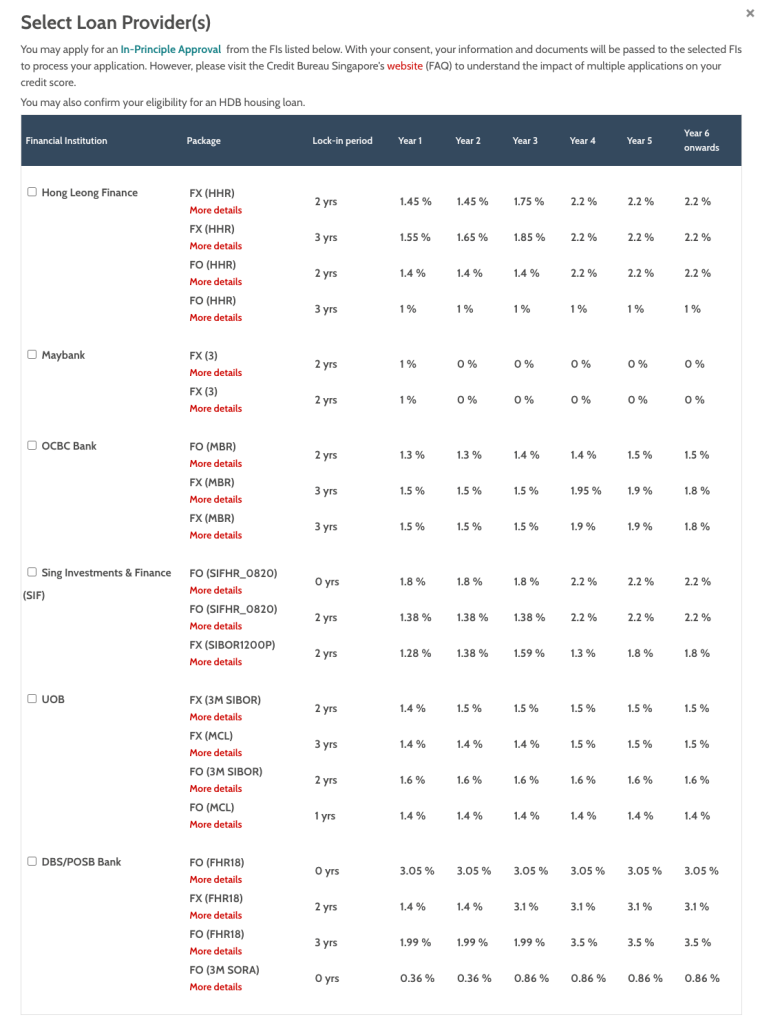

7. Wait…I can apply for bank loans on the HDB Flat Portal?

One hugely beneficial new feature of the new flat application process is that you can now see and compare bank loans on the HDB Flat Portal, all on one page. Here’s what it looks like:

Source: My Nice Home by HDB

See a bank loan you want to apply for? HDB will help you with that. At this stage, you can indicate for HDB to pass your information and documents to the bank to request an In-Principle Approval (IPA) for a housing loan from them. The IPA is a document from a bank saying that they will lend you money for your house.

After you submit the IPA request via HDB, the bank will liaise with you directly to let you know if your request is approved or not. Then, after booking a flat, you can go back to the HDB Flat Portal to confirm the bank loan offer.

Know friends or family applying for an HDB flat? Share this article with them!

Related Articles