"Buying a house in Singapore is easy!" ...said no one ever. The path to home ownership in Singapore is often a difficult, convoluted and arduous task. It's one tied to your wealth, marriage, family, and even luck.

Chances are, you landed upon this article about buying a condo because you’re trying to check out all your housing options before settling for one that suits your circumstances.

Here's all the information you need about that all-important condo downpayment in Singapore so you can decide on what to do next as a first-time home buyer.

[ms-toc title="How much downpayment do you need for a condo?"]

1. How much is the condo downpayment in Singapore for first-timers?

If you were wondering how much you need to have on hand to buy a condo—and be done with the circus that is public housing—this article is for you.

There are quite a few factors that affect your condo downpayment in Singapore:

- Loan-to-Value (LTV) Limit: the amount that you can borrow from the bank. This depends on how many outstanding home loans you have. If you have no other home loans, your loan tenure is 30 years or less and doesn’t go past the year you turn 65, your LTV limit is 75%.

- The outstanding condo downpayment, which you can use your CPF to pay partly.

- The minimum cash downpayment, which must come from your bank account

- Stamp Duty (BSD and/or ABSD), which you must pay in cash first (then request a reimbursement from CPF)

These factors vary depending on the price of the condo. For simplicity’s sake, let’s assume you're looking for a small condo in a non-central neighbourhood, and you've found a unit going at $800,000.

The table below breaks down the costs you need for your condo downpayment in Singapore:

Singaporeans | Permanent Residents (PRs) | Foreigners | |

Loan-to-Value Limit (75%) | $600,000 | $600,000 | $600,000 |

Outstanding Condo Downpayment (25%) | $200,000 | $200,000 | $200,000 |

Minimum Cash Downpayment (5%) | $40,000 | $40,000 | Not Applicable |

Stamp Duty (BSD + ABSD) | $18,600 (calculator here) | $58,600 (calculator here) | $498,600 (calculator here) |

Total Condo Downpayment (CPF + cash) | $218,600 | $258,600 | $698,600 |

Cash money you must have on hand | $58,600 | $98,600 | $698,600 |

2. How much do I need in cash + CPF for my condo downpayment?

In case you didn’t know already, you can use your CPF funds to pay for your condo downpayment. So no, you don't need to cough up the full sum in cash. Phew!

If you're using CPF for your condo downpayment, the funds have to come from your Ordinary Account (OA).

In the above mentioned example, the up-and-coming condo costs $800,000. You have a total downpayment of $200,000, or 25% of the condo's price.

Of this $200,000, you'll need to pay at least $40,000 in cash, i.e. 5% of purchase price.

The remaining amount can be borne from your CPF OA. This equates to $160,000, or 20% of purchase price.

But wait! Do you have $160,000 in your CPF account!? If you're a regular salaried worker earning a pretty high income of $4,000/month, it'll take a little over 8 years for your OA to accrue that much. Oof. That's a long time.

So if your CPF OA isn't quite as flush, you'll need to pay more than $40,000 in cash for your condo downpayment.

3. Do I need to pay stamp duty (BSD or ABSD) in cash?

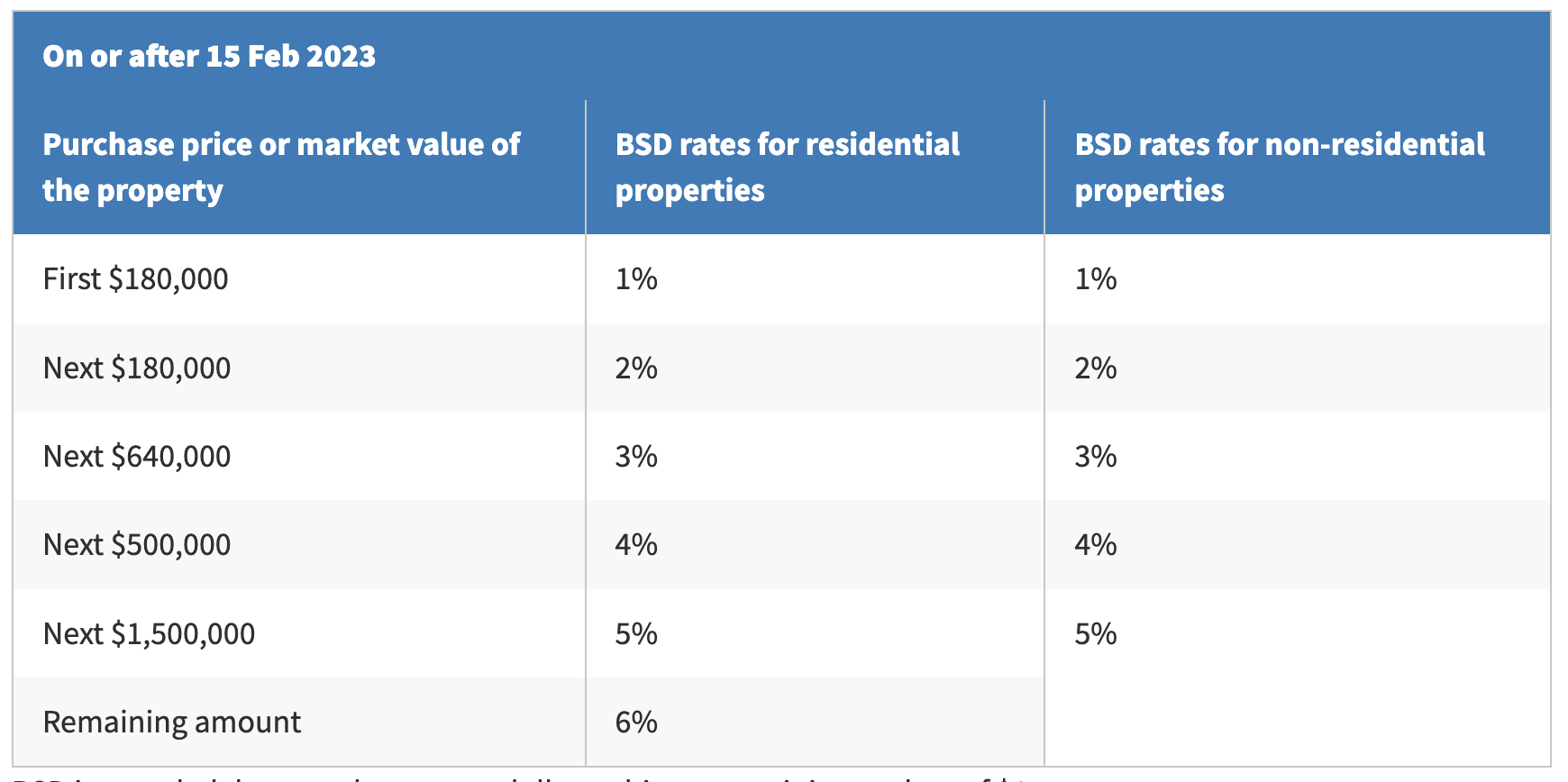

Buyer’s Stamp Duty (BSD) is an extra cost you need to factor in when saving up for your condo downpayment. It's applicable on all residential property purchases, regardless of whether you're a first-time buyer.

Here's a table from IRAS to show you how it's calculated:

Source: BSD rates from IRAS

For an $800,000 condo unit, the Buyer's Stamp Duty is $18,600 (calculator here). If you're a Singapore citizen, that's all you have to pay in stamp duties.

But if you're a PR or foreigner, you'll need to factor in Additional Buyer's Stamp Duty. For your first property purchase, PRs need to pay a tax of 5% while foreigners get taxed a whopping 60%.

In total, PRs need to pay BSD + ABSD (5%) = $58,600 (calculator here), while foreigners need to cough up BSD + ABSD (60%) = $498,600 (calculator here).

You can use CPF OA to pay Stamp Duty, but it's on a reimbursement basis. This means that you still have to fork out the funds from your bank account.

And obviously, your CPF needs to have enough balance to reimburse you in the first place.

4. How much are the monthly repayments for my condo with a home loan?

Thought coughing up the hefty downpayment was hard? Wait till you hear about the monthly repayments for your condo.

Right now, typical home loan bank rates hover around 3.7% – 5.5% p.a., with a lock-in period of 1 to 3 years. Most banks don't publish their rates online—Maybank is one of the few that do. Otherwise, you'd need to fill in a form with your home loan details to find out their home loan rates. Alternatively, get in touch with mortgage specialists—they may even give you exclusive rates!

Assuming your condo costs $800,000 and you take a loan of $600,000, here's an idea of what your monthly repayments will look like with various fixed interest rates:

Fixed interest rate | Monthly instalment | Total of 240 payments (over 20 years) | Total you're paying in interest |

3.5% | $3,479.76 | $835,141.99 | $235,141.99 |

4.0% | $3,635.88 | $872,611.67 | $272,611.67 |

4.5% | $3,795.90 | $911,015.10 | $311,015.10 |

5.0% | $3,959.73 | $950,336.26 | $350,336.26 |

5.5% | $4,127.32 | $990,557.72 | $390,557.72 |

For the fellow mathematically challenged folks out there wondering how this is calculated, it's not a simple matter of taking 3.75% x $600,000. Compounding is confusing. Let a free online loan calculator do it for you.

The above mentioned rates assume that you take up a fixed home loan, but there are many other types of home loans. For home loans from banks, you can choose a fixed interest rate or a floating one. Floating interest rates are pegged to the Singapore Overnight Rate Average (SORA), an interest rate benchmark that MAS calculates and that banks use to determine interest rates on their home loans.

The current 3-month compounded SORA is 1.29% as of Nov 2025.

To see how a bank uses SORA, let's take Maybank's 3M Compounded SORA home loan package as an example.

Maybank charges an interest rate of 3M Compounded SORA + 0.70% p.a. for the first 3 years and 3M Compounded SORA + 1.00% p.a. thereafter. That means you'll be paying 1.99% p.a. for the first 3 years.

In this case, you're better off with the floating package instead of their fixed rate home loan package, which fixes the interest at 3.75% for the first 3 years.

Do note that after the initial lock-in period, fixed home loan interest rates will revert to the floating rates.

Always keep up to date with the interest rates and do not hesitate to refinance your home loan if need be!

Check the best available home loan rates from all banks on MoneySmart.

5. Do I have enough money for a condo downpayment?

To summarise, Singaporeans need at least $160,000 in CPF OA and $58,600 cash on hand for a condo downpayment if you're buying a $800,000 condo and taking a loan of $600,000. (If you do not have enough in your CPF OA, you'll need to pay more in cash.)

If you're weighing that against the other options, here are guides for you to mull over:

Most home purchases follow a similar structure: work out your downpayment from the borrowing limit, then how much you have in your CPF vs cash you actually need to pay. Your circumstances may be unique, which is why we have property financing tools for you to work out what’s best for you.

But if you've got your heart set on a condo unit, then you definitely need to work and save hard for that 6-digit sum.

Consider low-risk investments to attain higher returns if you have years to save for your condo downpayment. Otherwise, your best bet would be side gigs and other income streams for extra cash in the short term.

6. Why would first-time home buyers splash out on a condo?

In the past, it was a standard rite of passage for Singaporean first-time home buyers to purchase an HDB BTO flat, thenupgrade to a condo at some point. Nowadays, that standard home ownership path is no longer the norm. Here are some reasons why.

Some of us don't qualify for a BTO flat.

There are the restrictions around buying an HDB flat. For example, you need to be a citizen, form a nuclear family (or be over 35), and be earning within the income ceiling. Read more about the HDB BTO eligibility requirements.

Some of us can't afford a resale flat either.

The HDB resale market is hot. While resale price growth has slowed—up 0.4% in Q3 2025—resale activity has increased 1.7%, and prices have increased by 54.9% since early 2020.

Plus, have you heard of million-dollar flats? There've been 1,235 million-dollar flats sold just in the first 9 months of 2025—already greater than the 1,035 sales we saw in the whole of 2024.

Not all resale flats are going to cost such astronomical prices. But all these numbers do give us an idea of the crazy demand that even resale flats can bring.

With BTO flats, you don't really get a choice.

If you're offered the chance to book a BTO flat, even if the remaining units are the last thing you wanted, HDB will pressure you to book it. From 2023, first-time applicants who are offered the chance to book a flat but choose not to will lose their BTO priority status. Yup, that refers to the additional first-time ballot chances that new-to-BTO couples have. They'll be treated as second-timers for a year thereafter.

If they are given the chance to book a flat again during that 1 year and again don't book a flat, they'll not be allowed to apply for a BTO flat for a whole year.

It's no wonder first-time home buyers like you might be considering buying a condo instead.

Know someone who might find this article useful? Share this knowledge with them!

Related Articles