Everyone from the kopitiam uncle to K-pop stans seems to be chasing air miles these days. I get it—racking up points for a jet-setting lifestyle sounds way sexier than hoarding cash rebates. But as someone who doesn’t travel much, I’m firmly, unabashedly in the cashback camp. What? Don’t judge.

If you’re like me and prefer cold, hard savings over glamorous airport lounges, this article’s for you. I’ve reviewed the best cashback credit cards in Singapore and narrowed it down to 6 winners across 5 categories: unlimited cashback, groceries, dining, online shopping, and transport.

Ready to earn those cash rebates? Let's take a look at the best cashback credit cards in Singapore in 2025.

Best cashback credit cards Singapore 2025

- TL;DR: Best cashback credit cards in Singapore (2025)

- Best cashback credit card for dining

- Best cashback credit card for groceries

- Best cashback credit card for shopping

- Best cashback credit card for transport

- Best cashback credit card for unlimited cashback

- Finding the best combination for you

1. TL;DR: Best cashback credit cards in Singapore (2025)

If you want the short version, here it is. Whether you’re a die-hard supermarket loyalist, a dining-out fiend, or just want fuss-free unlimited cashback, there’s a card that fits your spending habits. We picked the winners based on cashback rate, minimum spend, category breadth, and caps so you don’t have to dig through the fine print.

Category | Winner | Runner-up |

Dining | HSBC Live+ Card | Maybank Family & Friends Card |

Groceries | DBS yuu Card | CIMB Visa Signature |

Shopping | UOB EVOL Card | OCBC FRANK Card |

Transport | UOB One Card | Standard Chartered Smart Credit Card |

Unlimited cashback | UOB Absolute Cashback Card | Citi Cash Back+ Card and OCBC INFINITY Card |

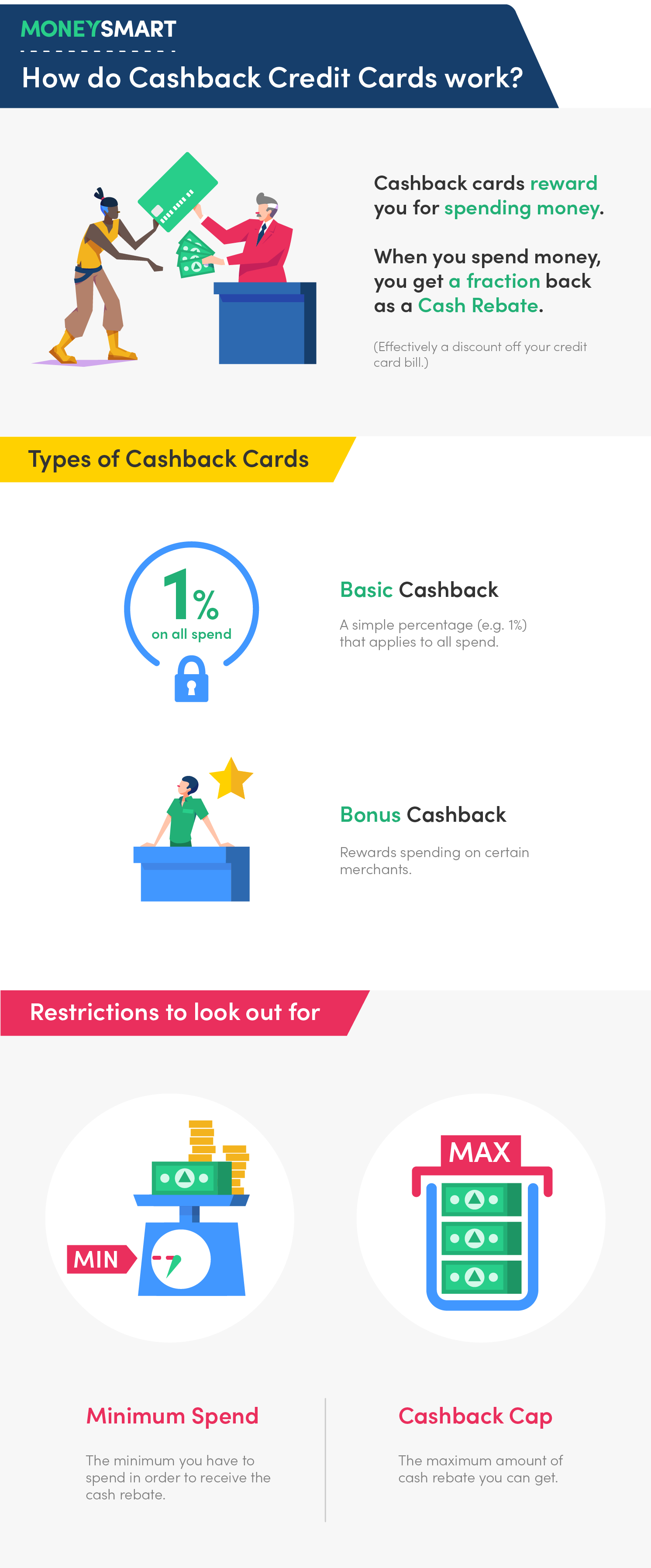

Before we go into more details, let’s get you orientated. Here’s a quick summary of how cashback credit cards work, so you understand the mechanics that underlie your rewards.

2. Best cashback credit card for dining

Winner: HSBC Live+ Card

- on Dining, Shopping and Entertainment

- 8% Cashback*

- on fuel at Caltex and Shell gas stations in Singapore

- 5% Cashback*

- on All Other Spends

- 0.3% Cashback*

Get HIGHEST IN MARKET S$430 Cash or 6,140 SmartPoints (worth up to S$649 of Gifts) when you spend S$500 from Card Account Opening Date to end of the following calendar month!

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

For now, the crown goes to the HSBC Live+ Card, thanks to its 8% cashback on dining, shopping, and entertainment for the first 2 calendar quarters. With a relatively low $600/month minimum spend (or $1,000 total if you’re issued mid-quarter), it’s not hard to unlock. Even better, the dining cashback is based on MCC codes, so you’ll earn at everything from your neighbourhood zi char to your favourite café abroad instead of just a fixed list of partner restaurants.

But why is it the winner only for now? The 8% cashback hinges on a promo that’s only valid until 31 Dec 2025. Yes, this promo has been renewed again and again since the card’s launch in Jun 2024, but there’s no guarantee HSBC will extend it again.

Runner-up: Maybank Family & Friends Card

The Maybank Family & Friends Card is wonderfully versatile because you can pick up to 5 categories on which to earn up to 8% cashback—the same rate as HSBC Live+, but with a higher minimum spend of $800/month.

Honourable mention: Citi Cash Back Card

With the Citi Cash Back Card, you take home a solid 6% dining cashback on MCC-based spend with the same $800/month minimum spend. Flexible coverage, decent rate, but not quite HSBC’s 8%.

Other dining cashback cards and why they didn’t win

Card | Dining cashback rate | Why it didn’t win |

2% unlimited on Wine & Dine with $1,000/month min spend | Lower rate than top contenders, with a high minimum spend | |

Up to 18% at yuu merchants (requires $600 total spend across all yuu categories) | Very high rate, but restricted to specific yuu partner outlets; doesn’t cover broader dining MCCs | |

5% on dining (shared $25/month cap across dining, entertainment & transport from Sep 2025) | Cashback cap is low, especially since it will be shared across 3 categories | |

5% on dining (including overseas & food delivery) with $800/month min spend | Good MCC breadth but lower rate than HSBC Live+ and Maybank F&F | |

5% on dining with $800/month min spend | Lower rate compared to top contenders | |

Up to 10% at “Smart Dining” merchants with $1,500/month min spend | Restricted to a fixed merchant list and high minimum spend of $1,500 to unlock highest rate | |

Up to 15% on a category of your choice, including dining, with $250/month cap | Cashback cap limits earnings potential; high $2,000/month min spend to unlock highest rate; your bonus cashback is limited to just 1 category | |

Up to 10% at selected partners only (e.g. McDonald’s, Grab) | Limited—as far as dining goes, you’ll only earn at McDonald’s; high $2,000/month minimum spend to unlock highest rate |

3. Best cashback credit card for groceries

Winners: NTUC Link Credit Card by Trust, DBS yuu Card

.png)

- savings on groceries and food

- Up to 21%

- petrol savings (on Caltex and Esso)

- Up to 20%

- FX Fees

- 0%

- at participating merchants with no min. spend

- 5% cash rebates

- spend min. S$800 & at 4 participating merchants per calendar month

- Up to 18% cash rebates

- on all other spend

- 0.25% cash rebates

If you’re loyal to a single supermarket chain, merchant-specific cards can be unbeatable. The NTUC Link Credit Card by Trust gives market-leading rates of up to 21% savings at FairPrice stores (including FairPrice Online), while the DBS yuu Card does the same with up to 18% cashback at Cold Storage and Giant. These aren’t MCC-based, but if you do most of your grocery runs at one of these chains, the extra cashback is worth it.

Card | Minimum spend tier | Grocery cashback rate | Merchants |

$0 | 5% base cashback (no cap) | Cold Storage, Giant, Guardian, and other yuu merchants | |

$600/month | 18% (capped at $78/month bonus cashback; unlimited base cashback) | ||

$0 | Up to 4.5% for FairPrice members | FairPrice groceries include FairPrice supermarkets, FairPrice Online, Unity pharmacies. | |

$350/month | Up to 15% for FairPrice members | ||

$700/month | Up to 21% for FairPrice members |

Runner-up: CIMB Visa Signature

For those who want the highest MCC-based rate, the CIMB Visa Signature offers 10% cashback on all grocery spend, both in-store and online. The catch? You’ll need to hit $800/month minimum spend, and cashback is capped at $20 per category—meaning you’ll only earn cashback on the first $200 of grocery spend per month. Great for light-to-moderate shoppers, not for families doing $400+ grocery runs.

Honourable mentions: POSB Everyday Card, Citi SMRT Card

If you shop at Sheng Siong, the POSB Everyday Card is all for you: 5% cashback with a remarkable $0 minimum spend. That’s hard to beat for casual shoppers.

The other honourable mention goes to the Citi SMRT Card. Don’t judge it by its unglamorous name—with a low $500 minimum spend, this card offers 5% cashback on groceries from supermarkets, alongside online shopping and public and private transport.

Other grocery cashback cards and why they didn’t win

Card | Grocery Cashback Rate | Why It Didn’t Win |

6% on groceries (MCC-based) with $800/month min spend | Strong rate, but lower than CIMB Visa Signature with the same minimum spend | |

6% (capped at $20) at RedMart till 31 Aug 2025; 2% (capped at $20 shared with Lazada spend) from 1 Sep 2025 | Restricted to one merchant; cap is low and shared across multiple categories, limiting total savings potential | |

Up to 8% on groceries (choose as one of 5 preferred categories) with $800/month min spend | Competitive but falls short of the cards above, and the cap of $25/category limits big spenders | |

3% on groceries with $800/month min spend, capped at $80/month | MCC coverage is broad, but rate is too low to compete | |

8% with $2,000/month min spend, or 6% with $1,000/month spend | High rate, but very high spend requirement |

4. Best cashback credit card for shopping

Winners: UOB EVOL Card and UOB One Card

- on Local Online, Mobile Contactless, Telco, Gym, Streaming spend

- 10% Cashback

- FX Fees on overseas FX spend worldwide, with no min spend, no cap

- 0%

- Min. Spend per month for 10% cashback

- S$800

Looking at high rates, low minimum spends, and a wide range of shopping categories, the UOB EVOL Card comes out on top. It offers 10% cashback on combined online and mobile contactless spend, with just a $600/month minimum spend. On top of that, you'll also get to enjoy 10% cashback on selected gym, telco and streaming spend, and 0% forex fees on all overseas foreign currency spend. The only downside? A $30/month cap, so anything above $300 in eligible spend won’t earn cashback.

Willing to sacrifice category breadth for a bigger cap? If you’re more of a Shopee-holic than a general shopaholic, the UOB One Card is worth a look. Even the lowest $600/month tier gives 8.33% cashback at Shopee, which is made up of 3.33% quarterly cashback and 5% additional cashback. Best of all, the card offers a generous $120 cap on the additional cashback you earn, equivalent to $2,400 worth of spending. The catch is that it’s Shopee-only, so not great for varied shopping.

Runner-up: OCBC FRANK Card

A strong all-rounder, the OCBC FRANK Card boasts 8% cashback on local online/contactless mobile spend and foreign spend with $800/month minimum spend. Rather than rewarding you based on MCC, it awards cashback based on your payment code, greatly widening your cashback net.

Honourable mentions: CIMB Visa Signature, HSBC Live+ Card

The CIMB Visa Signature comes with a generous 10% cashback, but only for online spend. Plus, it limits you to a $20/category cap and requires $800/month minimum spend.

With the HSBC Live+ Card, you can currently enjoy 8% cashback with a low minimum monthly spend of $600, but this is a promotional rate only valid till 31 Dec 2025. Fingers crossed—hopefully HSBC extends it!

Other shopping cashback cards and why they didn’t win

Shopping cashback card | Rate / Min spend / Cap | Why it didn’t win |

5% on online shopping / $500 min spend / 600SMRT$ cap per year | Decent rate and low min spend, but lower than top contenders and capped | |

6% on shopping (online & in-store) / $800 min spend / $50 per month cap for shopping | Solid coverage but rate lower than top contenders | |

Up to 8% on shopping (if you select is as 1 of 5 preferred categories) / $800 min spend / capped at $25 per month per category | High rate but cap limits heavy shoppers | |

8% at selected online merchants / $800 min spend / $20 per month category cap | Limited to specific merchants and not MCC-based; cap of $20/month | |

– Up to 5% / $500 min spend / $30 monthly cap | High minimum spend required to unlock highest rate; selecting this as your bonus category also limits you to only earn bonus rates on shopping |

5. Best cashback credit card for transport

Winner: UOB One Card

- cashback on daily spend at McDonald's, Grab, SimplyGo & Shopee

- Up to 10%

- cashback at all grocery spend

- Up to 8%

- cashback cap a year

- Up to S$2,240

For a mix of SimplyGo, petrol, and Grab rides, the UOB One Card delivers the highest overall earning potential. You can get up to 10% cashback at selected transport merchants like Grab and SimplyGo, plus strong petrol savings of up to 22.66% at Shell and SPC.

The UOB One Card’s 10% cashback on transport is unlocked for high spenders hitting the $2,000/month tier, but even the lower tiers ($600 or $1,000/month) give respectable returns of 8.33% cashback for daily commuters.

Runner-up: Standard Chartered Smart Credit Card

With the Standard Chartered Smart Credit Card, earn up to 10% cashback on “Smart Transport”, which includes SimplyGo and EV charging, alongside dining and streaming. You earn 8% with a $800/month spend, and 10% with a $1,500/month spend. While the latter is a high spend requirement, the UOB One Card’s ask to unlock the same 10% is even higher.

One great feature of the SC Smart Credit Card is that its cashback is unlimited for all tiers, so you don't ever need to worry about charging too much to this card. But what is limited about the Standard Chartered Smart Credit Card is that its bonus cashback only applies to SimplyGo and EV charging.

Honourable mention: Citi Cash Back Card

The SC Smart Card’s narrow category selection is why I think of the Citi Cash Back Card as something like the Smart Card’s alter ego. With this Citi card, you can similarly earn 8% cashback with $800 minimum spend, but this time on petrol and private commute instead of SimplyGo and EV charging. I bumped it to a spot below the SC Smart Card because it isn’t limitless; cashback is capped at $80/month, so high spenders will be limited.

Other transport cashback cards and why they didn’t win

Card | Rate / Min spend / Cap | Why it didn’t win |

2% unlimited on taxis & automobiles / $1,000 min spend / No cap | Low rate compared to top contenders; better suited for those wanting unlimited coverage | |

Up to 5% on SimplyGo / $500 min spend / 600SMRT$ annual cap | Decent rate for $500/month minimum spend, but it just isn;t as competitive as our winning cards | |

6% on transport (SimplyGo) / $800 min spend / $20 cap for transport | Wide breadth, but high minimum spend and high cap that would limit heavy commuters | |

Up to 18% at Gojek / $600 min spend / Capped at $78/month bonus cashback; unlimited base cashback | Very high rate at Gojek, but also a very narrow merchant list of just 1— no earnings for petrol or SimplyGo | |

(from 1 Sep 2025) 5% on transport / $700 min spend / $25 shared cap with dining & entertainment | Low shared cap reduces earnings potential for transport | |

Up to 8% on transport (choose as 1 or 5 preferred categories) / $800 min spend / $25 per category cap | High rate but capped at equivalent of $312.50 spend, not ideal for frequent commuters or drivers | |

6% on petrol; 3% on taxis, private commute and EV charging / $800 min spend / $80 monthly cap | Strong for petrol, but weak for taxi and private hire, and no SimplyGo coverage | |

Up to 10% on SimplyGo and BlueSG (mobile contactless) / $800 min spend / $25 cap per category | High rate, but cap limits earnings | |

10% with SimplyGo / $800 min spend / $20 monthly cap6% at SPC (petrol) / $0 min spend / No cap | Good SimplyGo and single-merchant petrol savings, but no coverage for taxis/private hire | |

– Up to 5% / $500 min spend / $30 monthly cap | High minimum spend required to unlock highest rate; selecting this as your bonus category also limits you to only earn bonus rates on shopping |

6. Best cashback credit card for unlimited cashback

If optimising specific spend categories is too much work for you, let’s take a step back and look at the all-in, catch-all type of cashback card: unlimited cashback credit cards. These cards offer cashback on almost everything, and usually come with a $0 minimum spend requirement. They’re great for:

- People who cannot be bothered remembering which card to tap on the train, which to use when eating out, etc.

- Earning cashback on large purchases like furniture or electronics—these would otherwise bust the cap on most other cashback credit cards that have monthly or annual caps

Winner: UOB Absolute Cashback Card

- Cash Back on Eligible Spend

- 1.7%

- Min. Spend per month

- S$0

- Cash Back Cap

- Unlimited

When it comes to unlimited cashback cards in Singapore, the UOB Absolute Cashback Card isn’t just the highest no-minimum-spend rate after promos, at an impressive 1.7%. It’s also an ultra-rare card that earns you cashback on things like insurance premiums—and this is after its May 2024 nerf, before which it even earned you 1.7% on categories like education, tax payments, pet stores and veterinary services, medical services and hospitals, utilities, and more.

The only catch? The UOB Absolute Cashback Card is an American Express card, so acceptance can be slightly more limited compared to Visa or Mastercard.

Runner-ups: Citi Cash Back+ Card, OCBC INFINITY Card

The Citi Cash Back+ Card and OCBC INFINITY Cashback Card both offer 1.6% unlimited cashback with no minimum spend. They’re both Mastercard, which might be preferable if you’re worried the UOB Absolute Card may not be accepted due to it being with Amex.

How do you decide between them then? Consider:

- Which has a better welcome gift? This factor was what made me choose the Citi Cash Back+ for myself. Check out our article on credit card promotions in Singapore for a summary.

- Do you prefer redeeming cashback in your own time, or have it automatically offset your next bill? The former is the OCBC INFINITY, and the latter the Citi Cash Back+.

- Do you have or plan to open a savings account like the OCBC 360 savings account? In my opinion, the OCBC 360 is better than the Citi Wealth First account, and the OCBC INFINITY Card can help to earn you higher bonus interest. Read more in my review of savings accounts in Singapore.

Honourable mentions: American Express True Cashback Card, Standard Chartered Simply Cash Credit Card

We have 2 cards whose regular rates aren’t high, but stand out now thanks to limited-time promotions. The American Express True Cashback Card offers a juicy 3% cashback on up to $5,000 spend in the first six months before reverting to an unlimited 1.5% cashback. It’s perfect if you have known big purchases you’re planning for at merchants that take Amex.

Another strong contender is the Standard Chartered Simply Cash Credit Card, with its ongoing 2% unlimited cashback promo (until 31 Oct 2025) for those who can meet the $800 minimum spend threshold.

Other unlimited cashback cards and why they didn’t win

There are many other unlimited cashback cards in Singapore that generally offer between 1.5 – 1.7% with no minimum spend. If you ask me, 0.1% isn’t going to make a huge difference—I myself use the Citi Cash Back+ just because the welcome gift appealed to me—so here’s a summary if you want to browse the alternatives:

Unlimited cashback card in Singapore | Cashback rate | Why it didn’t win |

– 3.0% cashback on up to $5,000 spend in the first 6 months | The 3% is impressive, but only lasts for 6 months and is limited to $5,000 spend | |

– 2% unlimited cashback on dining, online food delivery, entertainment, transport, and luxury goods with ≥ $1,000 spend in a statement month. | 2% cashback comes with a high minimum spend of $1,000; otherwise, the 1% cannot compete | |

– 2% unlimited cashback on travel, overseas spending, and online spend in foreign currency with ≥ $2,000 spend in a statement month | 2% cashback comes with an even higher minimum spend of $2,000; again, otherwise, the 1% cannot compete | |

Unlimited 1.6% with no minimum spend; cashback does not expire | Decent, but it falls just 0.1% short of UOB Absolute Cashback | |

Unlimited 1.6% with no minimum spend; cashback automatically offsets your next credit card bill | Decent, but it also falls just 0.1% short of UOB Absolute Cashback | |

– [Limited time] 2% unlimited cashback, from now to 31 Oct 2025 if you spend ≥ $800 within 30 days | 2% is for a limited time; otherwise its 1.5% rate is not as competitive | |

Unlimited instant 1% cashback with no minimum spend | 1% is low for an unlimited cashback credit card | |

– Unlimited 1.7% with no minimum spend on almost everything, even insurance premiums | With the highest unlimited cashback rate in Singapore (excluding limited-time promotions), it won! |

7. Finding the best combination for you

While we’ve crowned the best cards for each category, the reality is your personal “best” might be a mix—either across 2 or more cards, or within a single card that covers multiple categories well.

If you have high, consistent spend in different areas (say, dining and groceries), pairing two specialised cards could maximise your returns. But if your monthly spend isn’t high enough to meet the minimum spends on multiple cards, a versatile card that earns well across categories might be the smarter move.

For example, I wanted a card for my daily commute and online shopping. On paper, the Citi SMRT Card isn’t a winner in any single category, but it gives me decent cashback on SimplyGo rides and online spend with just a $500 minimum. I also keep the Citi Cash Back+ Card in my wallet to whip out for big purchases that would bust other cards’ cashback caps.

Medium.jpeg)

- on Online Purchases, Groceries, Taxi, Ride-hailing, SimplyGo & Malaysia Ringgit Spend

- 5% Savings

- on Other Retail Spend

- 0.3% Savings

- Min. Spend per statement month to earn max rebates

- S$500

Get S$400 Cash Reward or 6,140 SmartPoints (worth up to S$499 of Gifts) —just spend S$500 within 30 days of card approval with your new Citibank Credit Card! Receive them as quickly as 5 weeks after meeting the spend criteria.

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

- Cash Back on Eligible Spend

- 1.6%

- Min. Spend per month

- S$0

- Cash Back Cap per month

- Unlimited

Get UPSIZED S$430 Cash Reward or 6,140 SmartPoints (worth up to S$499 of Gifts) —just spend S$500 within 30 days of card approval with your new Citibank Credit Card! Receive them as quickly as 5 weeks after meeting the spend criteria.

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

The key is to map your spending patterns by looking at your actual monthly expenses first. Then choose a combo of cards or a single all-rounder that covers your biggest spend categories without overcomplicating your wallet.

Want to find out more about the best cash back credit cards in Singapore? Compare and apply on MoneySmart!

We also have a comparison tool for the best cash back credit cards in Hong Kong!

This article was first drafted with the help of AI and later reviewed and refined by the author.

Related Articles