This post was written in collaboration with HSBC. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best recommendations and advice in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

As the Christmas, New Year and Chinese New Year celebrations approach, that’s when our spending likely increases as well.We’re feasting over catch-ups with friends, buying Christmas presents and decorations, spring-cleaning and sprucing up our homes...the list goes on — and before you know it, Chinese New Year rolls around again and you have to dish out those angpows. If you’re always overspending during festive seasons (ouch, post-holiday debt) and want to save money, here are some smarter ways to maximise your savings.

1. Scaled down celebrations = scaled down spending

Covid-19 restrictions on the number of people allowed for social gatherings have been a headache for those of us with large families or groups of friends larger than 5 (still waiting for lucky number 8 and beyond from 28 Dec).On the bright side (for your wallet), this means that the festivities are now much smaller scale events. Chill, there’s no need to go all out to order/prepare food and drinks for the army you’re used to.If you’re having an intimate gathering at home, opt for a potluck where everyone contributes 1 home-cooked dish instead of a catered meal, which can cost up to several hundreds. You can also take advantage of promotions for your party planning and festive dining to save even more money.

2. Reduce fixed costs such as your mortgage

Homeowners know that the biggest loan they will ever take is their mortgage. Although it’s something one cannot avoid paying for, there are ways to reduce the cost of it.

Step 1: Get a home loan with a lower interest rate

Right now, bank home loan interest rates are much lower than HDB’s loan interest rate (2.6% p.a.). When you get a loan with a lower interest rate, you pay less in overall interest in the long run.

Step 2: Even better, get an interest offset home loan

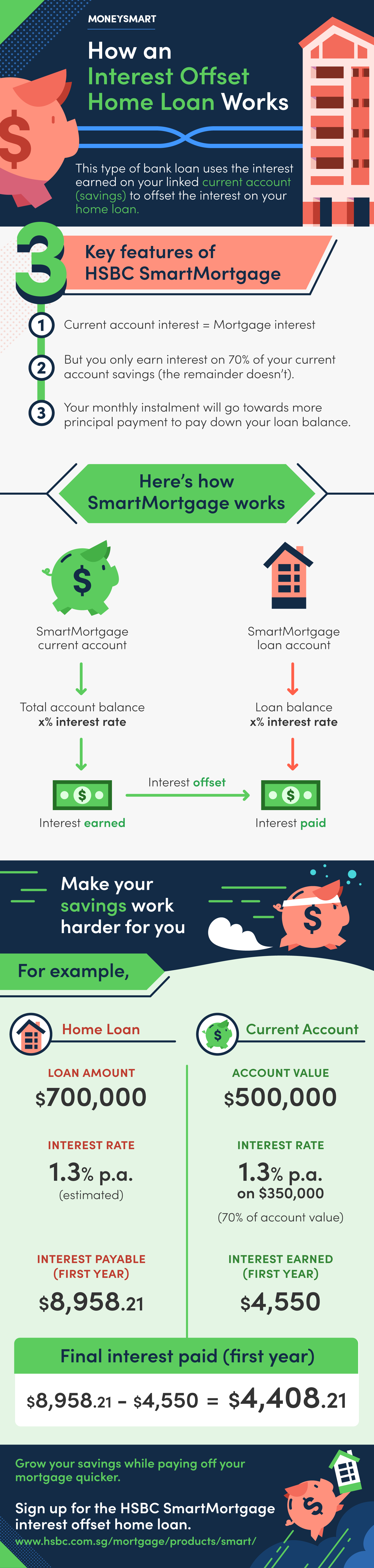

In addition to enjoying a lower interest rate, those on an interest offset home loan can literally offset the interest on their home loan with the interest earned on their linked current account with the same bank.When you save on the loan interest, your debt can be paid off sooner — that’s when you can call your home truly yours.For example, HSBC’s SmartMortgage allows you to link a HSBC current account to your HSBC home loan. Interest earned on your savings in the current account can be used to offset some of the interest you need to pay on your home loan.How HSBC SmartMortgage (interest offset home loan) works: Note:

Note:

- 70% of the lower of (1) Account Balance i.e. funds in the SmartMortgage current account and (2) Loan Balance will earn an interest rate that matches that on their home loan

- Hence, interest earned from the SmartMortgage current account can offset the interest payable, which means their monthly instalment will go towards more principal payment to pay down the loan balance

- The remaining 30% of the funds in the SmartMortgage current account do not earn any interest

- Other terms and conditions apply

Scenario: Let’s say John plans to take out a home loan of S$700,000 at 1.3% p.a. (estimated). He is deciding between HSBC SmartMortgage and a typical home loan from another bank. He has S$500,000 in savings and maintained it throughout the year.Here’s a simplified* look at how much he can save in his first year:

HSBC SmartMortgage (John) | Typical Home Loan | |

SmartMortgage Home Loan | SmartMortgage Current Account | |

Loan amount: S$700,000 | Account value: S$500,000 | Loan amount: S$700,000 |

Interest rate: 1.3% p.a. (estimated) | Interest rate on S$350,000 (70% of account value): 1.3% p.a. | Interest rate: 1.3% p.a. (estimated) |

Interest payable (first year): S$8,958.21 | Interest earned (first year): S$4,550 | Interest payable (first year): S$8,958.21 |

Final interest paid (first year): S$8,958.21 - S$4,550 = S$4,408.21 | Final interest paid (first year): S$8,958.21 | |

*Scenario is for illustration purposes only; it includes assumptions of loan amount, interest rate, interest payable, etc.Thanks to the savings in his SmartMortgage current account, John pays less interest yearly on his home loan. This means more money for the festivities!If you want to make your savings work harder for you, sign up for the HSBC SmartMortgage interest offset home loan. In addition, if you’re refinancing your existing home loan with HSBC, you’ll receive a cash incentive of up to S$2,000. T&Cs apply.

3. Use the right credit card(s)

Sales have been happening practically every month — 9.9, 10.10, 11.11 (Singles’ Day), Black Friday, Cyber Monday, 12.12, Boxing Day...you name it. While it’s a great time to enjoy all the wonderful discounts, you should also maximise your spending (buying things on discount still means money is spent, okay!) with a cashback credit card. The HSBC Advance Credit Card lets you earn up to 3.5% cashback* on your purchases, without being limited to a specific merchant category. This means that you can spend on all the things you love and earn up to S$370 cashback* per month.*Terms and Conditions apply. More details, visit www.hsbc.com.sg/advancecard.

- Base Cashback

- 1.5%

- Cashback when you spend more than S$2,000

- 2.5%

- Cashback Cap per month

- S$70

Get S$400 Cash or 6,140 SmartPoints (worth up to S$649 of Gifts) when you spend S$500 from Card Account Opening Date to end of the following calendar month! T&Cs apply.

PLUS celebrate Singapore's birthday with a S$61 Cash Bonus when you are the first 10 customers to submit the claim form during the National Day Flash Deal! T&Cs apply.

For HSBC TravelOne Card: Enjoy S$120OFF (min. spend S$1,000) promo codes on flight bookings every Thursday!

If cashback is not your thing, you can also choose the right credit card that rewards your usual spending habits.For example, the HSBC Revolution Card allows you to accumulate rewards points/air miles from the activities that you usually do. The good thing about this HSBC credit card is that it has no minimum spend and no limit on the rewards that you can earn. This card also offers 10X Reward points (or 4 miles per dollar) on up to S$1,000 of your online and contactless spending. Score!

4. Utilise offers and rewards

Remember to fully utilise your available credit card offers and rewards. If you want to celebrate, why do it at full price when you can do it at a discount? To get you started, here are some festive promotions HSBC Credit Cardholders can enjoy:

Validity | Campaign | Details |

Till 31 Dec 2020 | Up to 25% off festive goodies, buffets, takeaways and more | |

Ongoing | - 1-for-1 dining deals and 25% off express deals - 1-for-1 one room night for local and overseas stay - 1-for-1 lifestyle offers for family fun | |

Varies | - Exclusive room rates - Up to 25% off bookings at top hotels | |

Varies | Shop up to 50% off online deals for food, apparel, shoes, flowers, appliances and more | |

Varies | Exchange HSBC Rewards points for vouchers at selected merchants |

*Please refer to the HSBC webpage for full details. T&Cs apply.

5. Be smart like Santa: Make a list and check it twice

Sometimes, it does pay to be more selective. It’s nice to give (and receive) gifts, but when you need to rein in your budget, every Peter, Paul and Mary shouldn’t be on your list. Set yourself a fixed budget and jot down the people you absolutely have to get gifts for. The rest of the money can go towards “spare” gifts for a friend’s surprise plus one, or cousin Sally’s newborn.Buying presents shouldn’t be done on a whim. Think carefully about what you can get for each person that fits your budget, so you don’t go on a whirlwind shopping spree and realise you’ve bought too many spontaneous presents that might not be suitable afterall. And of course, with all the neverending holiday sales, merchant offers and credit card promos, you can definitely get something nice to fit your budget. But if you’re shopping online, do make sure that the gifts can be delivered on time! You can also opt for self-pick up if available, it’s quicker and removes delivery fees.Being thrifty needn’t strip your festivities of enjoyment. Go on, treat yourself! The key is to set a budget, reduce costs, spend wisely and be moneysmart to get the best bang for your buck. Disclaimer: This article is brought to you by MoneySmart and HSBC. The information contained herein is for information only and should not be relied upon as financial advice. For more details on the products and offers, please visit wwww.hsbc.com.sg. Terms and conditions apply for all promotions.