If you love collecting points and redeeming them, a rewards credit card will give you some added life satisfaction.

These days, there’s a lot more in banks’ rewards catalogues than boring old NTUC vouchers. You can redeem your accumulated points for cash rebates, air miles, nifty gadgets, and dining vouchers at fancy schmancy restaurants.

But with the dizzying number of rewards credit cards out there, comparing them all can be an insurmountable task. To save you the headache, we've compiled the best rewards credit cards for online spend, overseas spend, and day-to-day expenses.

7 Best Rewards Credit Cards in Singapore (2024)

- Summary: Best rewards credit cards in Singapore (2024)

- Citibank Rewards Card

- OCBC Titanium Card

- DBS Woman's Card

- Standard Chartered Rewards+ Card

- HSBC Revolution Card

- UOB Preferred Platinum Card

- UOB Lady's Card

- Who should use a rewards card?

- How do rewards cards work?

1. Summary: Best rewards credit cards in Singapore (2024)

Card | Bonus Category | Bonus Points | Bonus Spend Cap | Points Expiry |

Online spend, Selected retail stores | 10X Points per S$1 | First $1,000 per month | 60 months | |

Online spend, Selected retail stores | 10X Points per S$1 | First $10,000 per month | 24 months | |

Online spend | 5X Points per S$5 | First $1,000 per month | 12 months | |

Overseas spend: retail, dining, travel | 10X Points per $1 overseas spend | First $2,000 per year | 36 months | |

Online spend, contactless payments | 10X Points per S$1 | First $1,000 per month | 37 months | |

Online shopping, Contactless payment | 10X Points per S$5 | First $1,000 per month | 24 months | |

Choose 1 category: Beauty & wellness, dining, entertainment, family, fashion, transport, travel | 25X Points per S$5 | First $1,000 per month | 24 months |

We derived this list by comparing the bonus spend category, the bonus earn rate for spend in those categories, the cap on how much you can spend on the bonus categories, and the expiry of the points you accumulate.

All the credit cards mentioned on the list are also relatively accessible and are suitable as entry-level credit cards to start off with. Let's dive into the details.

2. Citi Rewards Card

- on Online Grocery, Food Delivery, Ride-Hailing

- S$1= 10X Points

- for in-store shopping purchases at Department Store, Clothing Stores

- S$1= 10X Points

- for all other purchases

- S$1= 1X Point

Get S$400 Cash Reward or 6,140 SmartPoints (worth up to S$499 of Gifts) —just spend S$500 within 30 days of card approval with your new Citibank Credit Card! Receive them as quickly as 5 weeks after meeting the spend criteria.

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

How many Citi rewards points can I earn?

At the moment, the Citi Rewards Card offers a generous up to 10X rewards (or 4 miles) per $1 spend with no minimum spend require.

However, there’s also a monthly expenditure cap of $1,000 on the 10X points, meaning that the maximum you can earn in a month is 10,000 points. So if you know you'll spend more than $1,000 in a month, other cards with higher monthly points caps may be more worth your while.

Where can I earn Citi rewards points?

You get points for spending on online purchases (including food and grocery delivery), physical retail stores, and ride-hailing. That makes the Citi Rewards Card a top choice for an everyday card, and perfect for those who buy everything online.

What can I redeem my Citi rewards points for?

When you get a rewards card, you definitely want to browse through the bank's rewards catalogue to know exactly what your points can get you. The Citi Rewards catalogue is filled with things you would actually want to spend your hard-earned points on, from Apple products to Amazon Points. So don’t worry about having to begrudgingly exchange your points for Popular Bookshop vouchers.

What are the Citi Rewards Card's income requirements?

The Citi Rewards Card is a suitable entry-level card with a minimum income requirement of $30,000 for Singaporeans and PRs, and $42,000 for non-Singaporeans.

3. OCBC Titanium Card

How many OCBC rewards points can I earn?

The OCBC Titanium Card offers 10x rewards points (or 4 miles) for every $1 spent on eligible online and retail purchases, and 1x points on all other spending. Additionally, the OCBC Titanium comes with some extra perks. These include a 2% cash rebate when you shop at Best Denki, up to 14% discount at Esso stations, and up to 16% discount at Caltex stations with the stations' onsite discounts.

There's a monthly cap of 10,000 bonus points, which is equivalent to a spend cap of $1,110 per calendar month.

OCBC used to have an annual cap of 120,000 bonus points, but they changed this to a monthly cap in Nov 2023. Unfortunately, that removes one of the advantages of the card—an annual (instead of monthly) cap is perfect for big expenses. For instance, if you buy a new sofa online worth $3,o00, the Citibank Rewards Card will only earn you rewards points on the first $1,000 spent. Comparatively, the pre-Nov 2023 OCBC Titanium Card would have given you rewards points on the full $3,000 spent.

Where can I earn OCBC rewards points?

You only enjoy the maximum earn rate if you spend at a store on their list of merchants, so it pays to check beforehand. You might notice the list is full of Merchant Category Codes (MCC)—read our guide to MCCs for more details.

OCBC has also identified a few merchants at which you can earn bonus points by name, including: Guardian, Shopee, Lazada, Taobao, Amazon, NTUC, and Watsons.

What can I redeem my OCBC rewards points for?

OCBC rewards are extremely bare bones. You’re basically forced to choose between air miles and cash.

What are the OCBC Titanium Card's income requirements?

An entry-level card, the OCBC Titanium card's minimum income requirement is $30,000 for Singaporeans and PRs, and $45,000 for non-Singaporeans.

4. DBS Woman’s Card

- on Online Purchases

- S$5 = 5 DBS Points (2 Miles per S$1)

- on Other Purchases

- S$5 = 1 DBS Point (0.4 Miles per S$1)

- e-Commerce Protection for Online Purchases

- Complimentary

How many DBS rewards points can I earn with the DBS Woman’s Card?

If all your transactions take place online, the DBS Woman’s Card is a good rewards card to have as it offers 5 points for every $5 you spend on online. The 5X bonus points only apply to the first $1,000 you spend online in a calendar month. Do note that the DBS points are awarded in blocks of $5 spent, while miles are awarded per dollar—2 miles for every $1 spent.

If you have an income of at least $80,000 per annum, skip the DBS Woman’s Card and sign up for the DBS Woman’s World Card instead to get double the earn rate on online spend: 10X DBS Points per S$5, and 4 miles per S$1. The DBS Woman's World Card also has a higher spend cap of $1,500. You'll earn bonus DBS points on the first $1,500 you spend online in a calendar month—equivalent to 3,000 points or 6,000 miles.

Where can I earn DBS rewards points?

The card’s definition of "online spending" is extremely broad, and includes everything from online grocery delivery to GrabPay credits. So, in essence, the card could potentially reward you for the bulk of your spending.

On the downside, the DBS rewards points are the fastest to expire (just 1 year!) compared to the other rewards' credit cards. However, if you grocery shop for your household, you can redeem those points every now and then for NTUC vouchers which will come in very handy.

What can I redeem DBS points for?

The DBS rewards catalogue has a decent selection of dining and retail merchants you can redeem your points at. These include Apple products, dining credits at Crystal Jade restaurants, and the usual culprits like NTUC, CapitaMall, and Takashimaya vouchers.

Who is eligible for the DBS Woman’s Card?

The DBS Woman's Card is a bit of a misnomer—everyone, woman or man, can apply for it. You just need to hit the minimum income requirement of $30,000 for Singaporeans and PRs and $45,000 for non-Singaporeans.

5. Standard Chartered Rewards+ Card

- on Foreign Currency Spend

- S$1= 10X Points

- on Local Dining Spend

- S$1= 5X Points

- on All Other Spend

- S$1= 1X Point

Where can I earn Standard Chartered rewards points?

The Standard Chartered Rewards+ Card is marketed as an overseas spending rewards card—you get the highest earn rate on overseas spending. Locally, you earn the most on dining transactions.

You earn points in the form of 360° Reward Points.

How many Standard Chartered rewards points can I earn?

You get up to 10x rewards points (or 2.9 miles) per S$1 on foreign currency, including online spend. So if you're in the midst of planning your holidays, the Standard Chartered Rewards+ Card is one of the best credit cards you can bring along.

ALSO READ: Best Travel Destinations and What To Do There, According to MoneySmart Staff

If you haven't been touched by the travel bug, the card Standard Chartered Rewards+ Card isn't going to be as useful for you. While it does earn you 5x rewards points (or 1.45 miles) per $1 spent on local dining, which other cards like the Citi Rewards Card definitely beat.

Another possible disadvantage to the Standard Chartered Rewards+ Card is the low annual cap of 20,000 points.

What can I redeem my Standard Chartered rewards points for?

Here's Standard Chartered's rewards catalogue. Not as exciting as Citibank's, but there are some restaurants, shopping mall and staycation vouchers that could be fun.

When do Standard Chartered rewards points expire?

Standard Chartered rewards points expire within 3 years from the date you opened the credit card account, not within 3 years from the date you earned them. This can be little confusing, so let us break it down for you. When it comes to their rewards points' expiration, Standard Chartered identifies 2 periods:

- Initial period: 3 years from the date you open your Standard Chartered credit card account.

- Further period: The next 3 years after the initial period.

During the "initial period", any rewards points you earn are only good for that 3-year initial period. Even if you earned points one week before the end of the initial period, those points will expire within the week.

During the "further period", any rewards points you earn will be valid for this new 3-year period.

What are the Standard Chartered Rewards+ Card's income requirements?

Singaporeans and PRs need to earn at least $30,000 annually to be eligible for the Standard Chartered Rewards+ Card. This doubles for non-Singaporeans, whose minimum income requirement is S$60,000.

6. HSBC Revolution Card

- on Contactless & Online Spending for cardholders who maintain at least S$50,000 average daily balance in your HSBC EGA SGD Account

- S$1 = 20X Points (8 miles)

- on Contactless & Online Spending for all other cardholders

- S$1 = 10X Points (4 miles)

- on All Other Spend

- S$1 = 1X Point

Get UPSIZED S$450 Cash or 6,140 SmartPoints (worth up to S$499 of Gifts) when you spend S$500 from Card Account Opening Date to end of the following calendar month!

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

How many HSBC rewards points can I earn?

With the HSBC Revolution Card, you can earn 10X rewards points (or 4 miles) per $1 on online spending (includes food delivery and travel bookings) and contactless payments. The bonus points are capped at 9,000 points, which is about $1,000 spend per month (of the 10X rewards points, only 9X are considered bonus ones). However, there's no limit on how many rewards points you can earn on all other spend.

Another nice touch is that there is no annual fee. So even if you don’t use the card much you won’t have to worry about accidentally getting charged for it at the end of the year.

You'll also get complimentary access to Entertainer with HSBC, a food and lifestyle rewards app which gives you 1-for-1 deals on dining, lifestyle and travel worldwide. However, note that only HSBC Visa Infinite & HSBC Premier Mastercard credit cardholders get full access to all deals and merchants.

What can I redeem my HSBC rewards points for?

The HSBC rewards catalogue isn’t the world’s biggest or most varied, but it does contain a nice selection of well-curated treats. Apart form the usual air miles and vouchers, you’ll find some interesting home and lifestyle gadgets like the Ninja Nutri-Blender Pro, Fitbit Versa 4, and Jura E4 Piano Black coffee machine.

What are the HSBC Revolution Card's income requirements?

The HSBC Revolution Card is a good option if you're looking for an entry-level credit card. Its minimum income requirement is $30,000 for Singaporeans and PRs and $45,000 for non-Singaporeans.

7. UOB Preferred Platinum Card

- on Online Shopping, Entertainment & Contactless Payments

- S$5 = 10X UNI$

- on SimplyGo Transactions

- S$5 = 10X UNI$

- Rewards to Miles Conversion

- 1 UNI$ = 2 Miles

How many UOB reward points can I earn with the UOB Preferred Platinum Card?

The UOB Preferred Platinum Card offers up to 10 rewards points for every $5 (2 miles for every $1) spent on selected online shopping, online entertainment (including food delivery and ticketing) and mobile contactless payments—note that they have to be mobile contactless and not just contactless to count.

Ride hailing credits are not eligible. You can check out the UOB Preferred Platinum Card's full terms and conditions for a complete list of eligible transactions.

There is a bonus cap of 2,000 points per calendar month, which means you can only enjoy their preferential earn rate on a maximum of $1,000 worth of spending each month.

Another benefits of the UOB Preferred Platinum Card is its fuel savings—up to 15% savings at SPC and up to 14% at Shell.

What can I redeem UOB reward points for?

The UOB rewards catalogue is one of the most sought-after rewards programmes out there, letting you redeem points for spa vouchers, Dyson vouchers and dining vouchers at "atas" restaurants like Les Amis.

When do UOB reward points expire?

UOB reward points expire 2 years after the quarter in which they were earned. So if you earned points in Jan and Feb 2024, these points will expire 2 years after 31 Mar 2024.

What are the UOB Preferred Platinum Card's income requirements?

Like the other cards on this list, the UOB Preferred Platinum Card is a good entry-level credit card. For Singaporeans and PRs, the minimum income requirement is $30,000 a year. This increases to $40,000 for non-Singaporeans.

8. UOB Lady’s Card

- Base Earn Rate

- S$5 = 1X UNI$ (0.4 miles per S$1)

- Category of Choice

- S$5 = Up to 25X UNI$ (equivalent to 10 miles per S$1)

- Min. Spend

- S$0

How many UOB reward points can I earn with the UOB Lady’s Card?

The newly revamped UOB Lady's Card offers 25X reward points per S$5 spent on a preferred category of your choice, which works out to be a whopping 10 miles per dollar. Spending outside of your chosen category will earn you a base rate of 1X reward points or 2 miles per $5 spent.

There's no minimum spend for the UOB Lady's Card, but there is a maximum of 1,800 reward points you can earn each month. That means once you hit an expenditure of $1,000 for the month, you should try to reign in your inner shopaholic or charge your purchases to another card.

Where can I earn UOB reward points with the UOB Lady’s Card?

You can choose any one of the following categories to receive your 25x points per S$5 spend bonus on: beauty & wellness, dining, entertainment, family, fashion, transport and travel.

One great thing about the UOB Lady's Card is that you can change your preferred category online every quarter. This flexibility is particularly useful when you’re anticipating high one-off expenses. For example, if you’re having a baby, choose the family category just before you do your pre-baby shopping, and then see the rewards points roll in when you buy your baby clothes, stroller and so on.

What can I redeem UOB points for?

The UOB Lady's Card shares the same generous UOB rewards catalogue as the UOB Preferred Platinum Card we discussed above.

Who is eligible for the UOB Lady’s Card?

The UOB Lady's Card is open to both women and men, like the DBS Woman's Card.

In terms of income requirements, the UOB Lady’s Card is a good entry-level credit card. Just like for the UOB Preferred Platinum Card, it has a minimum income requirement of $30,000 a year for Singaporeans and PRs and $40,000 for non-Singaporeans.

9. Who should use a rewards card?

Are you sick and tired of tracking your expenses to the very cent in order to maximise your returns from a cashback card? Or maybe you'd like to earn more miles on top of what your air miles card already gives you?

You might want to consider switching to a rewards card, which is probably the lowest effort type of credit card on the market.

ALSO READ: Air Miles vs Cashback vs Rewards—Which is the Best Credit Card Type to Use?

Most rewards cards have no minimum spending requirements, so you don’t have to agonise over your expenses and track them in a spreadsheet. That makes them good for “fun” spending (e.g. shopping, entertainment, dining, travel) which can vary from month to month.

The rewards points you earn are also versatile. You can use them to redeem whatever is in your bank’s reward catalogue of goodies. Usually there’s a variety of shopping and dining vouchers, and some have gifts like fancy whiskeys and gadgets. A lot of banks also offer cash rebates.

If shopping or cashback rewards don't appeal to you, many people also redeem air miles with their rewards points. In fact, rewards credit cards are actually great for travel junkies—some rewards cards outperform miles cards in earning air miles! This is especially the case for miles earned from local or online spending. For example, the UOB Preferred Platinum Card earns you up to 2 miles for every $1 spent online, while the UOB PRVI Miles Card earns only 1.4 miles per $1 local spend.

Just be aware of the expenditure cap, if any, as you won’t get bonus points beyond that. Check the expiry date of your points too, so you don’t get a nasty shock when you try to redeem stuff. For a quick overview, we've compiled this information in the summary table above.

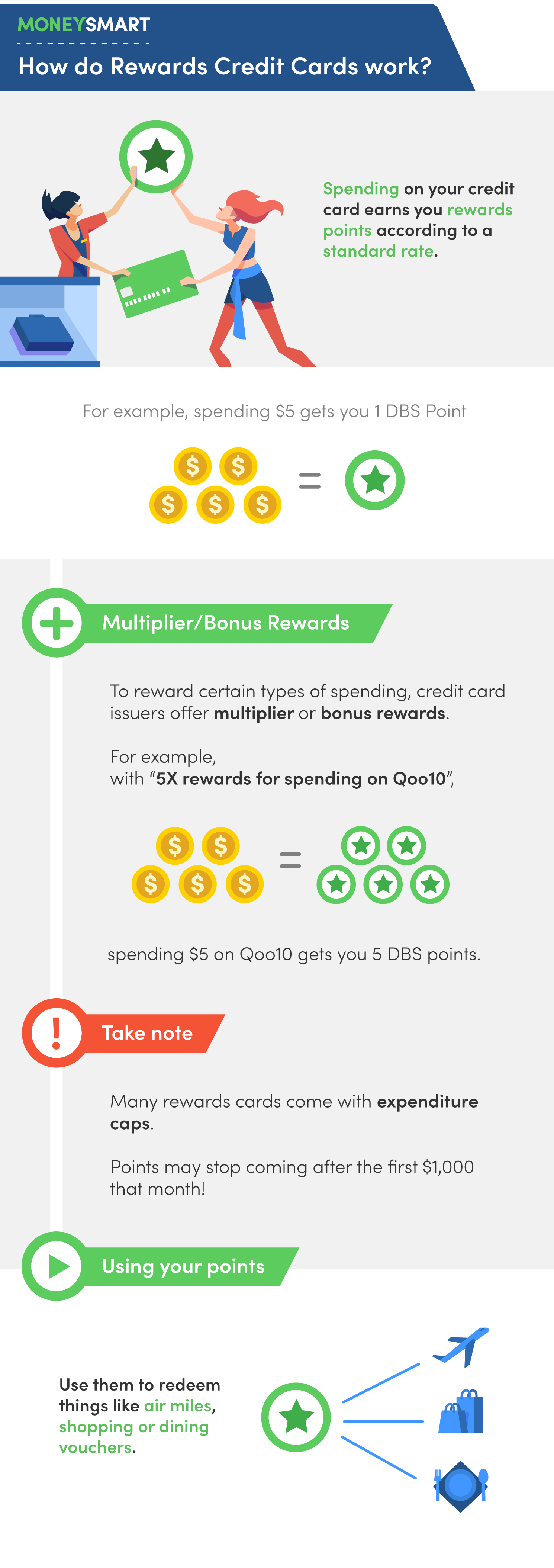

10. How do rewards cards work?

Because of banking jargon, rewards cards might seem complicated, but they’re actually really easy to use. Even the most tech-illiterate of Singaporean aunties can find their way around them. Here’s a 4-step guide:

Step 1: Know which spending categories (e.g. dining, entertainment, beauty, etc.) give you the most points.

Step 2: Go ahead and spend in those categories! (But know your expenditure cap so you don’t go overboard.)

Step 3: Rewards points are magically credited to your account.

Step 4: When you have enough points, redeem stuff you want from the rewards catalogue.

Want to find out more about the best rewards credit cards in Singapore? Compare and apply at MoneySmart!

Related Articles