After letting account-based ticketing (ABT) languish in “pilot” mode for two whole years, the folks at TransitLink finally got their act together and are launching it for real. Presenting, at long last, SimplyGo.

As its name suggests, SimplyGo is very simple. It's the latest incarnation of TransitLink’s two-year-old pilot programme called ABT (account-based ticketing), which is a system that lets you pay for public transport with your credit card. All Mastercard, NETS and Visa contactless bank cards, including foreign-issued cards, can be used for SimplyGo.

“Uh, okay. Noted with thanks,” you say. “I’ll just continue using my EZLink card because it’s safe and familiar and feels like home. Also my mom got me the limited edition Pompompuri card.”

Fair enough. But might you be missing out on cashback, air miles and credit card promotions? Let’s have a look at what you can get.

Best credit cards for SimplyGo (cashback)

Credit card | SimplyGo cashback | Min. spend (monthly) |

BOC Qoo10 Mastercard | 15% Qmoney rebate | $800 |

CIMB Platinum Mastercard | 10% cashback | $800 |

Maybank Family & Friends | 5% / 8% cashback | $500 / $800 |

DBS Live Fresh Card | 5% cashback | $600 |

UOB One Card | 3.33% / 5% quarterly rebate | $500 / $1,000 / $2,000 |

Maybank Platinum Visa | 3.33% quarterly rebate | $300 / $1,000 |

DBS Visa Debit Card | 3% cashback | $400 |

StanChart Spree Card | 2% cashback | None |

Maybank FC Barcelona | 1.6% cashback | None |

HSBC Advance Card | 1.5% / 3.5% cashback | None / $2,000 |

StanChart Unlimited Card | 1.5% cashback | None |

There are 4 main types of cashback cards that give you rebates for SimplyGo, and I'll explain how they work:

Multi-category cashback cards: BOC Qoo10 Mastercard, CIMB Platinum Mastercard, Maybank Family & Friends. With these cards, your SimplyGo transactions are counted as "transport" spending, and you can get the highest rebates. However, the minimum spending requirements (and cashback caps) are the worst on these cards, so unless your spending habits swee swee fit the cashback structure exactly, you won't be able to maximise the rebates.

Contactless spending cashback cards: DBS Live Fresh, DBS Visa Debit Card, StanChart Spree Card. These are cards that give you bonus csahback on contactless payment, i.e. Visa PayWave, Apple Pay etc. Currently, SimplyGo transactions are counted as contactless payments too.

Quarterly rebate cards: UOB One Card, Maybank Platinum Visa Card. These cards don't care what you spend on as long as you consistently spend a certain amount each month for the whole quarter. Right now, SimplyGo counts towards that minimum spend, but be careful - if the bank decides to exclude SimplyGo, you may lose your rebates for the entire quarter!

No minimum spend cashback cards: Maybank FC Barcelona, HSBC Advance, StanChart Unlimited Card. These cards give you a straight-up small rebate (less than 2%) with no (or negligible) conditions for you to meet, so SimplyGo transactions qualify unless the bank explicitly states otherwise.

Best credit cards for SimplyGo (miles)

Credit card | SimplyGo miles / rewards |

UOB Lady’s Card | $1 = 4 miles (registration needed) |

Maybank Horizon Card | $1 = 3.2 miles |

UOB KrisFlyer Credit Card | $1 = 3 miles (min. spend $500 on SQ / Scoot) |

BOC Elite Miles Card | $1 = 1.5 miles |

UOB PRVI Miles Card | $1 = 1.4 miles |

DBS Altitude Card | $1 = 1.2 miles |

DBS Black Visa Card | $1 = 1.2 miles |

Again, 3 general types of credit cards that let you earn miles or rewards with SimplyGo transactions. The right one depends on what your spending habits and needs are.

Multi-category miles cards: Maybank Horizon Card, UOB KrisFlyer Credit Card. These are miles cards that count SimplyGo in the transport category, and that accelerate your miles for spending in that category. These would be great to use as everyday cards because you get bonus miles when dining, shopping, etc. as well.

The one exception is the UOB Lady's Card, which is a category-based miles card, but you can only choose one category at a time. It would be a bit of a waste to select the transport category, because most people don't spend all that much on commuting.

Contactless spending miles cards: UOB Preferred Platinum, DBS Black Visa Card. These cards give you bonus rewards/miles for contactless payment, and right now, SimplyGo transactions are not excluded from that payment mode (yet). (Update: UOB Preferred Platinum has excluded account-based ticketing from the "contactless" category. Now you only 0.4 mile per $1 spent, so it's hardly worth the effort)

"Regular" miles cards: BOC Elite Miles Card, UOB PRVI Miles, DBS Altitude. You can earn miles by tapping with any regular miles card, based on the normal earn rate for local spending, provided the bank has not excluded SimplyGo from its list of eligible spending. But the earn rates pale in comparison with the rest.

SimplyGo promotions

Looking for SimplyGo cashback promotions? You're a little late to the game, my friend. Most of the carrots were dangled in April 2019, when SimplyGo launched with Mastercard exclusively. They've all since expired, and there are currently no SimplyGo promotions.

|

|

|

|

| |

|

| |

|

| |

|

| |

|

|

There's a small something from StanChart though, but only if you care about mandopop star JJ Lin. You can get a chance to win tickets to JJ Lin Sanctuary 2.0 World Tour per $1 when you tap and go with StanChart Mastercard from 22 Sep to 31 Oct 2019.

But if you're serious about maximising the benefits of SimplyGo, you'll want to pick the right credit card to get cashback or air miles from your everyday transport spending.

How do you sign up for SimplyGo?

Step 1: Create an account on TransitLink’s SimplyGo website or the TL SimplyGo app.

Yes, it's the one with a terrible App Store rating.

Step 2: Add a credit card to your account.

Step 3: Tap in and out as per normal while taking the bus or MRT, except using your registered credit card instead of EZLink.

Step 4: At the end of the month, you’ll see your consolidated transport spending reflected on your credit card bill. Don’t worry about being overcharged - public transport rates are standard.

Alternatively, you can also enable SimplyGo at the General Ticketing Machine with your Mastercard. You have to make sure it has a CEPAS logo at the back, though. (Infographic courtesy of Mastercard.)

What is it like using SimplyGo?

I signed up for the TransitLink ABT trial before SimplyGo launched and have been using it since last year. After SimplyGo launched, I have continued using it until today.

I love it and will probably never go back to EZLink.

The best thing about SimplyGo is that you can use your registered credit card via your mobile wallet, i.e. Apple Pay, Google Pay, Samsung Pay. This capability was always there even during ABT, but it was in beta mode, so prone to glitches. Since SimplyGo officially launched in April last year, I have not encountered any glitches yet (using Apple Pay).

Since I now use Apple Pay for taking the MRT/bus, I can now leave my wallet at home! #minimalistgoals My only gripe is that Apple Pay's Touch ID is a little slow, but I found a workaround: Use Touch ID to authenticate the transaction before tapping in.

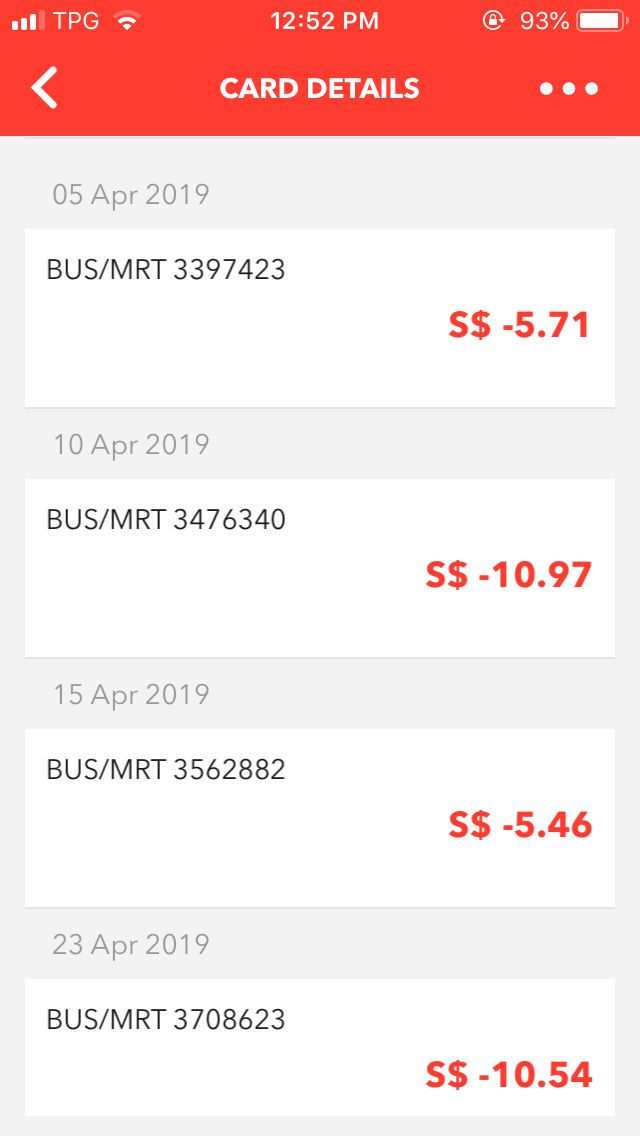

What about checking your SimplyGo transaction history?

Oh yeah, I hardly ever do this because I'm lazy, but I have to acknowledge that reconciling your public transport spending can be an issue with SimplyGo.

When I look at my credit card transaction history, it appears like this:

[Notice that the merchant is "Bus/MRT", not "TransitLink".]

Yep, it's a complete mess. The transactions seem to go through at random intervals instead of something sensible, like 1-week intervals, so it's hard for me to tell if there are any potentially fraudulent charges or any other errors.

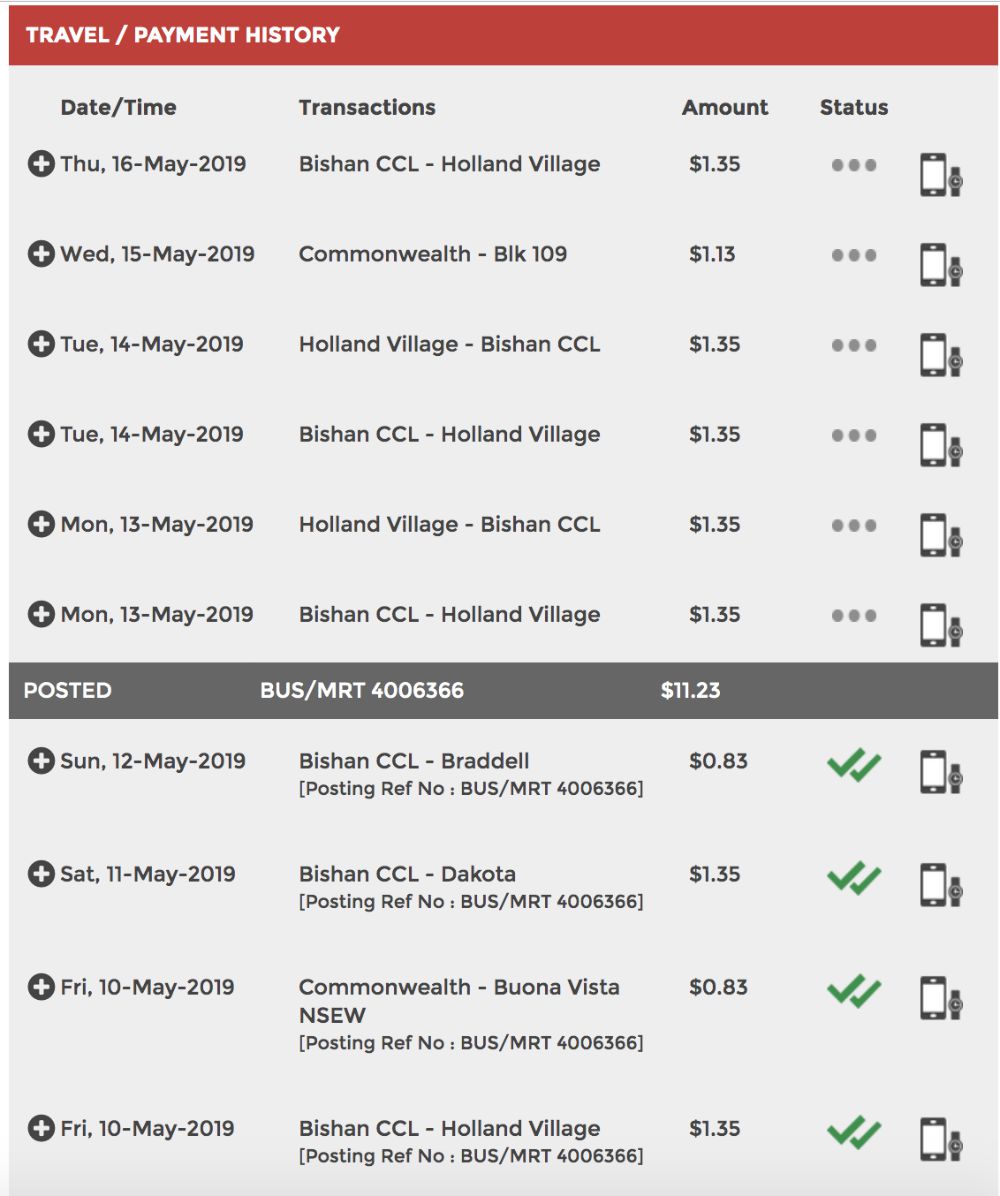

To do that, you have to go to the SimplyGo mobile app or portal to check the actual transaction history. It's broken down into individual rides, like this, and there's a lag of a few days before your trip is verified with those green ticks.

Have you tried ABT / SimplyGo? What do you think of it? Tell us in the comments.

Related Articles