This post was written in collaboration with CIMB Bank Singapore. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

I’ll never forget the day I collected the keys to my first home. This was the moment my extended childhood ended and my adulthood began.

Of course, once I finished feeling all the feels, there was a ton of work ahead of me. I had to jump straight into a real brain-wringer: planning the renovation. There was so much to think about!! From deciding what renovation work was needed to be done, to hunting for trustworthy contractors, to sourcing cheap furniture online, it’s a wonder I managed to get anything done while juggling my day job.

After wiping out my savings for the flat, I was pretty broke back then. I bet most new homeowners are, too. It’s no wonder many turn to renovation loans. A renovation loan is a special type of loan where the bank disburses money directly to your contractor instead of to you.

How much can I borrow for a renovation loan?According to unsecured credit limits permitted under regulation, the maximum one can borrow for a renovation loan is 6X your monthly income or S$30,000 (whichever is lower) as compared to up to 4X your monthly income for personal loans. This limit applies to each borrower, so, in theory, 2 co-owners could borrow up to S$60,000 in total as a joint application if necessary. |

If you’re sourcing for a renovation loan, naturally you’ll want to look for something with as low interest as possible. That’s challenging right now, since loan interest rates are on the rise… but good news — CIMB Bank has actually reduced the profit rate on their Renovation-i Financing, making it a good option for new homeowners.

Here’s the lowdown on CIMB’s Renovation-i Financing:

1. One of the lowest renovation financing rates from 3.88%* p.a. (EPR 4.29% p.a.)

CIMB’s Renovation-i Financing profit rate was previously at 4.20%* p.a. (EPR 4.61% p.a.), but, to ease homeowners’ financial strain amid inflation, they’ve decided to lower it to as low as 3.88%* p.a. (EPR 4.29%p.a.) from 1 Aug 2022.

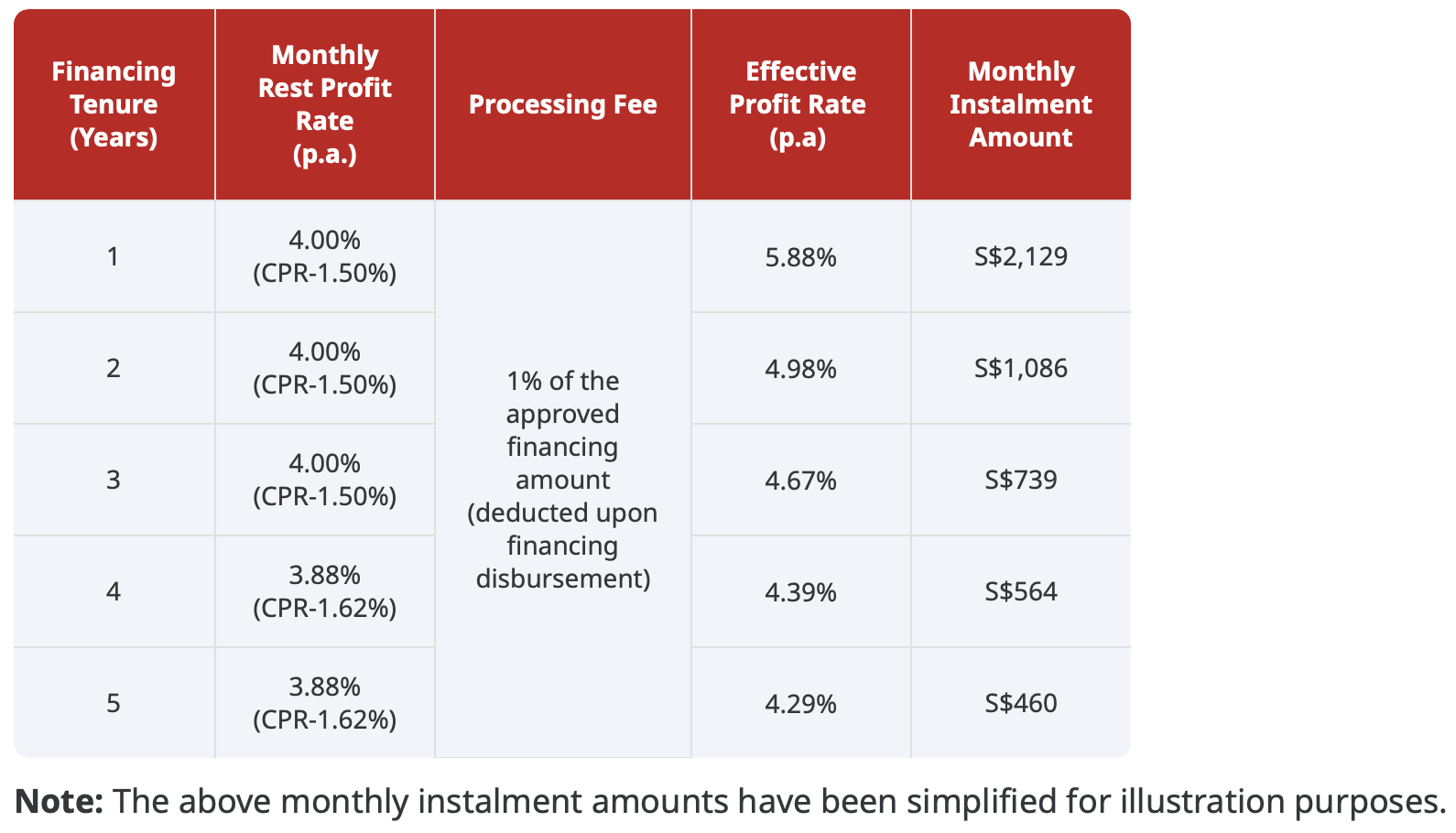

Here’s a chart showing how much you’ll be paying each month for a renovation financing of $25,000:

Source: CIMB Bank website

As you can see, the profit rate and monthly instalments depend on the financing tenure you opt for. In general, for the same financing amount, the longer your financing tenure, the less you pay in monthly instalments (because you have longer time to pay off the financing); for a shorter financing tenure, the more you pay in monthly instalments (because you have a shorter time to pay off the financing).

You’ll also notice that the EPR also changes accordingly, and gets lower as your financing tenure increases. However, you’d likely be paying more overall profit for a financing with a longer financing tenure versus a shorter financing tenure.

Here’s a closer look at how this works:

The 3.88%* p.a. (EPR 4.29% p.a.) rate is for 5 year tenure, which also results in the lowest monthly instalments. If you can afford it, though, consider choosing a shorter financing period. Despite the slightly higher profit rate of 4.00%* p.a. (EPR 4.67% p.a.) for 3 years financing tenure, you’ll be paying less profit overall.

Either way, CIMB Bank has one of the more affordable renovation loans in Singapore right now. Other banks typically charge 4.10% or more per annum on their loans. So it’s pretty much a no-brainer for new homeowners to consider financing with CIMB Bank.

Are there Shariah-compliant renovation loans in Singapore?CIMB Renovation-i Financing is the ONLY Shariah-compliant renovation financing in Singapore. The “-i” in the product name is to differentiate between a conventional product versus an Islamic product. The profit rates, fees and charges for CIMB Renovation-i Financing are transparent and available on CIMB Bank’s website. Profit rate here is what you typically understand as interest rate in conventional terms, same for financing which will be what you understand as loan in conventional terms. |

2. No hidden fees

Most of us fixate on the interest rate when comparing renovation loans, but the reality is that there are other fees to consider, too. Fortunately, CIMB Bank has only 1 upfront fee i.e. processing fee unlike other banks that charge insurance fee on top of the processing or admin fee. Refer to CIMB Bank’s website for further details.

The most important fee to consider is the processing fee of 1%. This is a one-off fee deducted from the amount disbursed to your contractor. For example, if you get a financing of S$25,000, the actual amount paid to your contractor will be S$25,000 minus S$250 (1% processing fee) = S$24,750.

To avoid any shortfall and possible disputes, do factor the processing fee into your financing application.

CIMB Bank disburses your contractor’s payment via cashier’s order and the first 3 are free. Do triple-check the cashier’s order details (e.g. names and registration numbers all correct) to avoid being charged fees for amendments.

To compare costs across different providers’ loans, always make sure you look at the banks’ published Effective Interest / Profit Rate (EIR / EPR). This is the “real” cost of the loan/financing and takes into account unavoidable fees like processing fees.

Here’s a quick glance at some of the standard renovation loan/financing interest/profit rates in the market.

CIMB | Bank A | Bank B | Bank C | |

1-year tenure | From 4.00% p.a. (EPR 5.88% p.a.) | From 4.10% p.a. | From 4.18% p.a. (EIR 4.91% p.a.) | 4.18% p.a. (EIR from 4.80% p.a.) |

2-year tenure | From 4.00% p.a. (EPR 4.98% p.a.) | |||

3-year tenure | From 4.00% p.a. (EPR 4.67% p.a.) | |||

4-year tenure | From 3.88% p.a. (EPR 4.39% p.a.) | |||

5-year tenure | From 3.88% p.a. (EPR 4.29% p.a.) | |||

Processing fee | 1% of financing amount | 0.5-1% of loan amount | 1% of loan amount | 0.5% of loan amount |

Other fee(s) | - | - | 1% insurance fee on loan amount | 1% of insurance fee |

Rates quoted and information are correct as of 23 August 2022

3. Quick approval time, covers all renovation needs

Given that every Singaporean wants to avoid the dreaded nightmare renovation, the demand for legit contractors is very high. So when you find a reputable contractor that fits your budget, you’ll want to lock them down ASAP to avoid further delays to your move-in date.

That’s why, if you’re looking for a renovation loan, it’s also important to consider the approval and processing time as well.

Some banks can take nearly a week to review and process your loan application, which can cause quite a bit of anxiety as you’re left wondering what’s going on. Meanwhile, other homeowners are already paying their deposits with your contractor, pushing your home’s renovation dates further and further behind! …And there’s also our usual pantang (superstitious) feeling about avoiding embarking on renovation works during the Hungry Ghost month.

Knowing how important renovation timelines are, CIMB Bank offers in-principle 1-day* approval regardless of whether your property is completed or still under construction.

This is provided you submit the complete application form and all required documents on a working day. While it’ll take longer to get the final go-ahead from CIMB Bank, at least you can use your in-principle approval to move ahead with your plans.

CIMB’s Renovation-i Financing reduces one renovation headache

Renovating and financing your new home can be super tough in today’s climate of supply chain disruptions and soaring prices. If you’re looking for ways to save on your renovation, the CIMB Renovation-i Financing is well worth considering.

It has one of the lowest* profit rates in town and this alone already makes it a no-brainer, in my opinion — one less renovation headache to check off your list! On top of that, homeowners will also appreciate the 1-day* in-principle approval and transparent fee schedule, while its compliance with Shariah law makes it an inclusive product for all creeds.

Learn more and apply for the CIMB Renovation-i Financing.

*Terms and Conditions apply.

Content sponsored by CIMB

For the avoidance of doubt, the information shared above is provided strictly on a non-reliance basis, and does not constitute any form of advice from MoneySmart or CIMB Bank Berhad. You should make your own assessment of your financial situation and needs.