Bad news first: You and I will literally never see the day women and men are paid equally worldwide. According to the World Economic Forum’s Global Gender Gap Report 2024, the global gender gap will need a whopping 134 more years to close.

Now for the silver lining: Just because we likely won’t see it happen in our time, doesn’t mean that we shouldn’t challenge the status quo—in fact, it’s more reason that we do.

Economic inequality between men and women is driven by various factors, like men being employed in higher paying industries and positions than women, uneven access to education, and more.

But have you ever thought about how such economic inequality also affects retirement? What does the economic gender gap mean for a woman’s financial security in her golden years? We take a deep dive into economic gender inequality and assess if women need to save more for retirement than men.

1. Women earn lower pay than men

Like many other countries in the world, Singapore is beset with a gender pay gap. This refers to the difference between how much men earn and how much women earn.

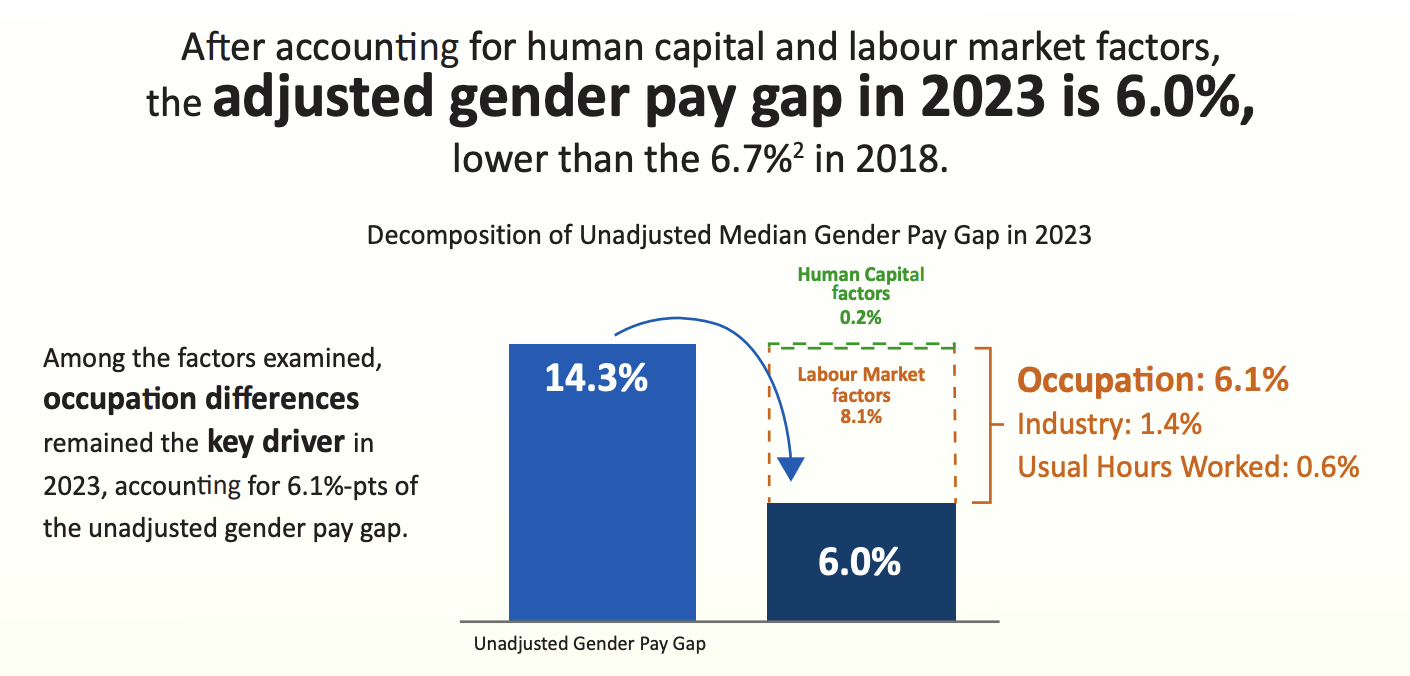

In Singapore, women earn 14.3% less than men, based on a 2023 study by MOM. That means if the average Singaporean man earns $5,000 each month, his female counterpart earns $4,285. Thus, for the same number of working years, women on average will earn less than men and have less money saved in the bank by the time they hit their retirement years. That’s a big reason (if not the biggest) why women need to save more now to ensure they have enough savings later.

But why do women in Singapore earn less than men anyway? Let’s take a closer look at the factors that go into this difference in pay:

Source: Comprehensive Labour Force Survey

Hold up, why does the gender pay gap get “adjusted” to 6%? Basically, this is how we explain why the gap exists. MOM looks at human capital factors like age and education, as well as labour market factors like occupation, industry, and usual hours worked per week.

Technically, the adjusted gender pay gap of 6% is a more accurate reflection of whether men and women of comparable age, education, occupation, industry, and usual hours worked earn an equal pay. In other words, it answers the question, “does equal work mean equal pay for men and women?”

A small adjusted pay gap is good news—women and men are paid equally for the same work. But if the small adjusted gap is accompanied by a large unadjusted one, that could point to an unequal representation of women and men in high-paying industries or positions.

For example, if we look at high-paying positions, 12.5% of CEOs and 41.7% of CFOs in Singapore were women in 2023. If male and female CEOs of similar work experience in the same industry receive similar pay, we’d see a small adjusted gender pay gap. But the fact that there are more male CEOs than female ones overall might contribute to a larger unadjusted gap, especially for such a high-paying position.

In MOM’s 2023 report, the 14.3% unadjusted gap gets whittled down to a 6% adjusted one. That means we can explain 8.3%-points of the pay discrepancy between men and women in Singapore; this portion of the gap reflects unequal work, not unequal pay for the same work.

Of the 8.3%, occupational differences are the biggest factor. We can attribute 6.1%-points to the types of jobs that men vs women have, differences in the pay across their jobs, or a combination of both.

On the flipside, while we can explain 8.3% of the gender pay gap, we still don’t know why the remaining 6% gap exists. This is the gap that says even when a man and a woman of similar career levels do the same job, the woman earns 6% less. MOM suggests in their Adjusted Gender Pay Gap report that we might be able to attribute this 6% to, “unmeasured employment characteristics (e.g. type of firms, position within firm, and work experience), caregiving responsibilities, parenthood, and labour market discrimination.”

We’re covering caregiving responsibilities and parenthood reasons in our next section, but discrimination at work can be talked about now. While the majority of companies in Singapore give equal opportunities to women, there are probably still a few offshoots contributing to a portion of Singapore’s 6% adjusted pay gap.

We don't know where this is happening, but we do know that gendered workplace discrimination is an unfair employment practice. It's one of the reasons the Tripartite Alliance for Fair & Progressive Employment Practices (TAFEP) was set up. If you or someone you know faces discrimination at work, don’t hesitate to submit a report to TAFEP—let’s take that 6% down.

2. Women work fewer years than men

Generally speaking, women work for fewer years in their lifetime than men. In Singapore, the employment rate for women is 78.3% compared to 88.8% for men, as reported in MOM’s Labour Force in Singapore 2024. That means lower lifetime savings, which in turn leads to lower retirement funds.

Why do women work less in their lifetime than men? According to MOM’s Labour Force in Singapore 2024, after retirement and education, the top reason people cited for opting out of the workforce was family responsibilities. Of the caregivers looking after their own children, almost all (95.1%) were women.

Mindsets and perceptions appear to play a big role in skewing the caregiver role at home. In a survey of 500 married Singaporeans, Ipsos and United Women Singapore found that 32% of women and 41% of men in Singapore agreed that in a marriage, it’s the husband’s main job to work and support his family, and the wife’s job to look after the household.

The good news, however, is that the survey also found that these mindsets are changing for the better with each generation. We all know women and men are equally entitled to work, and women shouldn’t be pigeonholed into a gender role at home that makes them sacrifice their career.

3. Women are found to be less financially informed than men

Globally, 35% of men versus 30% of women are financially literate, according to a study conducted in 2017 by the Global Financial Literacy Excellence Center. In Singapore, a study conducted by professors at Singapore Management University (SMU) in 2020 showed that older women know less about finance than men, especially when it comes to stock diversification. Women are also less concerned about how they’ll cope financially after they retire.

While there are always exceptions, financial savviness is typically associated with greater wealth and retirement readiness. Being more familiar with the workings of the stock market and retirement annuity plans means one is probably in a better spot to grow their wealth and plan their retirement well.

In fact, the 2020 SMU study we mentioned above found that being able to answer just one additional financial literacy question correctly meant an additional $166,800 in a person’s total net wealth, $97,700 in non-housing net wealth, and $52,600 in net financial wealth.

Thankfully, things are looking up. More and more women are taking financial and retirement planning into their own hands. A 2025 YouGov survey found over 60% of women in Indonesia (76%), Hong Kong (66%) and Singapore (62%) manage their finances independently. A lot can change in just one generation—for example, two-thirds (66%) of women in Singapore now report having better finances compared to their mothers at their age, according to a 2025 Sun Life Asia survey.

4. Women live longer than men

This is a fight Singaporean women win the moment they’re born: the life expectancy at birth for Singaporean females is a ripe old 85.2 years as of 2023. For men, this is 80.7 years, meaning women in Singapore live almost 5 years more than men on average.

Now that we’ve told you the good news, we have to break the bad news: Living longer also means needing more money for retirement. This widens our gender retirement gap even further.

We know what you’re thinking: Doesn’t CPF LIFE cover everyone’s retirement no matter how long you live, male or female? Well, yes. When it comes to CPF LIFE, its name is its virtue, and it does give all Singaporeans monthly retirement payouts for life. The problem isn’t if you’ve covered, but by how much.

Let’s do a quick recap. The amount you get each month for your CPF LIFE payouts depends on how much you’ve saved in your CPF Retirement Account (RA) by the time you turn 65. The fatter your RA, the higher your CPF LIFE payouts.

If you have $97,300 in your RA when you turn 65, you’ll only receive $540 – $570 each month—barely enough to get by. You’d need to have saved $227,900 to cross the $1,000 payout mark, and have $628,600 in savings to receive $3,100 or more per month.

This is the problem: Not all of us will have enough saved in our RA by the time we turn 65 to receive monthly payouts sufficient to live on. Especially not women who earn lower salaries and work fewer years.

One might argue that CPF LIFE is just the base layer of your multi-layered retirement portfolio, and that’s 100% true. You’ll also need annuities and income-generating investments like rental income, dividends, and bonds for your retirement. But if women are also less financially informed, they’ll be less likely to beef up their retirement portfolio and grow their money through investments. If CPF LIFE is all they have, that’s not a lot to live on.

5. So, do women in Singapore need to save more for retirement than men?

Women in Singapore are more likely to need to save more for retirement than men if they earn less, work less, invest less and live longer. But that’s a lot of if’s. Though more probable statistically, that isn’t to say all women are guaranteed to take home lower salaries or leave their jobs to look after the household.

A woman’s personal choice counts for more than any number on a page, and there’s plenty of room for antiquated mindsets that assume gendered roles to change. Increasingly, there’s also no reason for women to be financially less informed than men, and we can’t wait for the day this becomes a question so obsolete no one would even think to ask.

Singapore’s been making good progress in some key areas of the economic gender gap, such as narrowing the adjusted gender pay gap from 8.8% to 6% from 2002 to 2018.

As for quashing gender stereotypes, awareness is key. And bit by bit, we’re seeing the needle move. For example, Ipsos and United Women Singapore found that younger couples below 35 years old are more likely to share household responsibilities. While 28% of married women between 35-44 years of age reported they share cleaning tasks at home, 38% of married women below 35 years old said the same.

So while the question we asked was if women in Singapore need to save more for retirement than men, its answer asks another question: Can we narrow Singapore’s economic gender inequality? Reducing the gender pay gap, putting female caregiver stereotypes to rest, and increasing financial literacy among women is possible. Both genders can work to get there, one generation at a time.

Found this article useful? Share it with your family, friends, and colleagues—whatever their gender.

Related Articles