Six months of 2020 have gone by, and we’re still trying to weather this Covid-19 pandemic and its economic impact on us.

With pay cuts, business projects on hold, retrenchments and overall job uncertainty, many of us are struggling to meet our family’s immediate financial needs — day-to-day expenses, necessities, mortgage, school fees, utility bills, medical fees… the list goes on.

Should we still take care of our future needs, such as saving for retirement? It’s likely that many of us have put this on the backburner in favour of the current pressing needs.

If this is not yet on your to-do list, or you’re starting to lose steam, here’s why we should still save for retirement despite tough times.

Don’t stop saving for retirement (start now if you haven’t begun)

The earlier you start saving for retirement, the easier it will be. Even if you start small, you will still end up with a sizable nest egg for a more comfortable life when you reach retirement age.

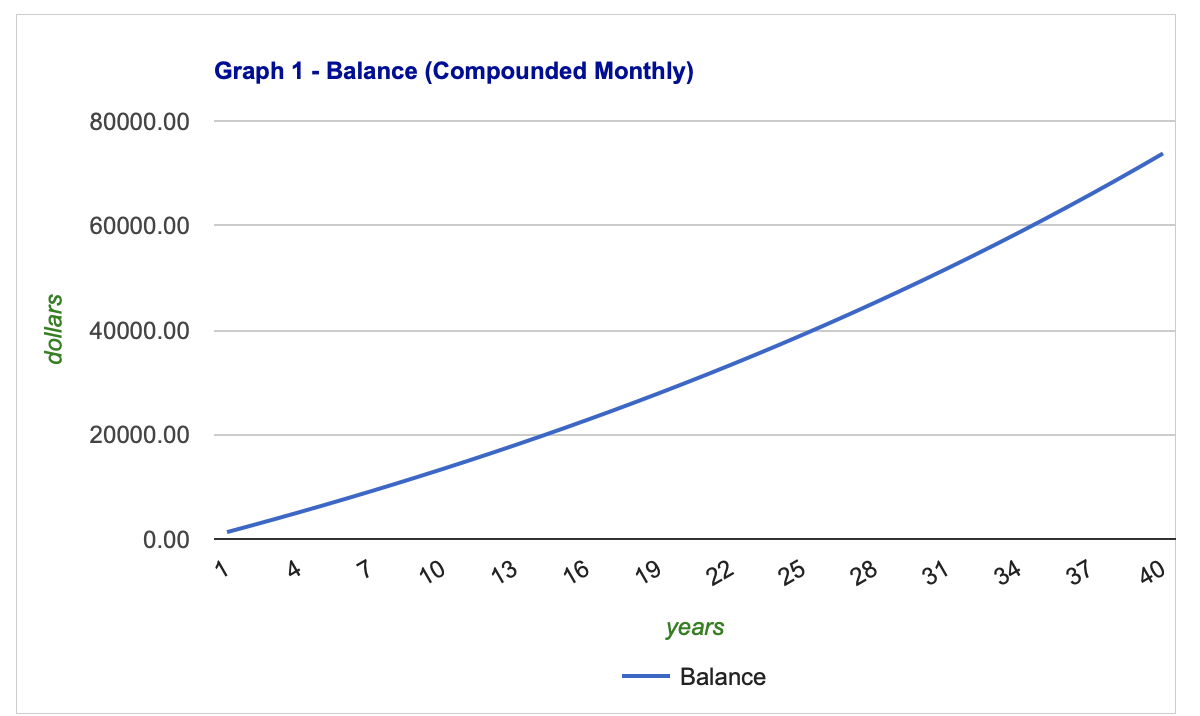

Here’s the difference when you start saving at age 25 versus age 35:

Scenario 1: If you start saving $100/month from 25 years old, when you reach age 65, you could end up with over $70,000. Assumptions: You’re getting about 2% p.a. returns in your savings account, without taking into account other fees and charges.

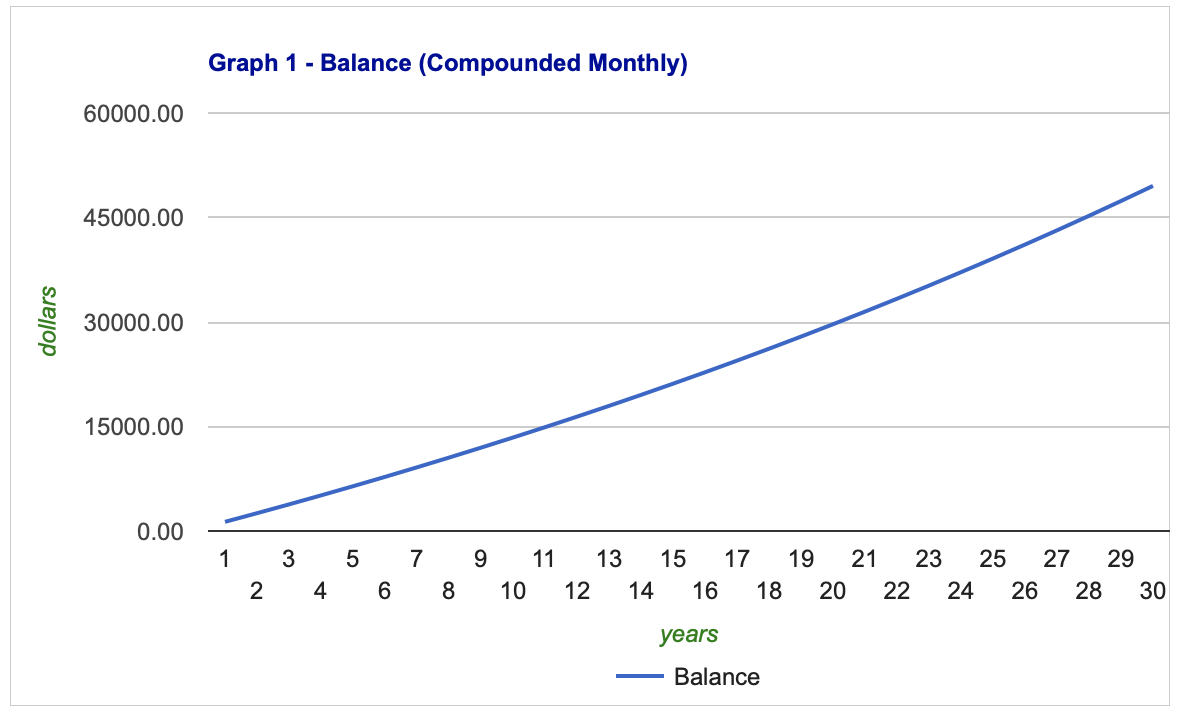

Scenario 2: If you start saving $100/month from 35 years old, when you reach age 65, you could end up with close to $50,000. Assumptions: You’re getting about 2% p.a. returns in your savings account, without taking into account other fees and charges.

Scenario 2: If you start saving $100/month from 35 years old, when you reach age 65, you could end up with close to $50,000. Assumptions: You’re getting about 2% p.a. returns in your savings account, without taking into account other fees and charges.

The difference is a whopping $20,000. But whether you’re in Scenario 1 or 2, your nest egg will only grow if the amount saved per month is increased as the person earns more, and if the money saved is also being regularly invested.

Conversely, if your target is to hit $X in retirement savings by a certain date, and you start to save now, you’ll need to put aside less each month, versus a higher amount should you start later. Why give yourself additional financial stress?

I got a pay cut and my finances are uncertain, what should I do?

From the example above, just setting aside $100 a month can make a huge difference 30 or 40 years down the road.

Even if you’re unable to put aside a lump sum for retirement right now, don’t ditch your retirement plans. If you really can’t afford it right now, temporarily put it on hold until you can find your financial footing in the wake of this pandemic storm.

We’re entering a new norm, but with some lifestyle tweaks and tightening of budgets, we should manage to set aside some money for our future. As our situation improves, we can always increase the amount.

It’s also not prudent to rely on the next generation for support — they’ll have their own plans, their own families to look after, their own financial commitments. Plus, there’s no guarantee that they’ll be in a better financial situation than we are now.

We’re also looking at a greying population. By 2030, it’s projected that the number of working-age citizens available to support senior citizens will fall to 2.7 from 4.5 in 2019.

How much is enough for my retirement?

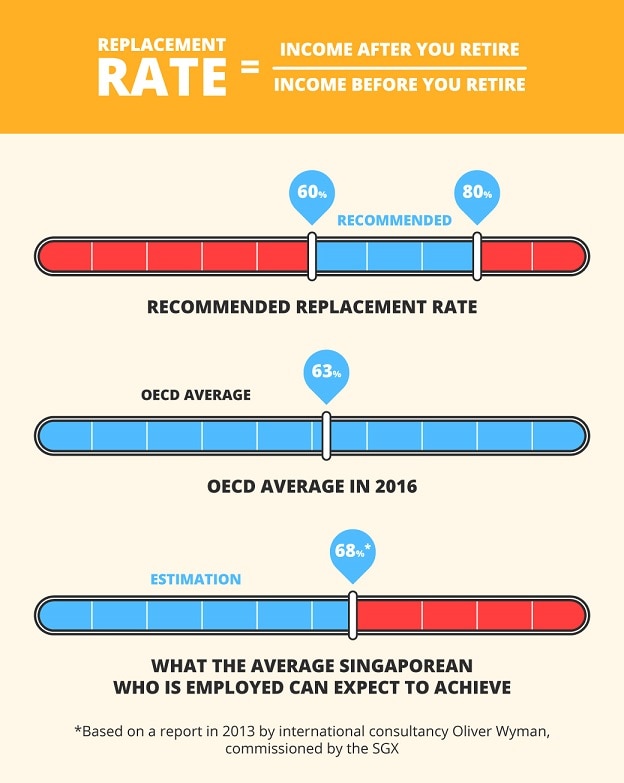

Let’s get a bit technical. To figure out how much is enough for our retirement, we need to calculate the replacement rate — equals to [income after you retire] divided by the [income before you retire].

You’re aiming for 60 to 80%, which should be enough... unless you plan to tour the world, buy a mansion for your family, go shopping every day, and spoil your grandkids silly with lavish gifts. It’s also assumed that you should have finished paying off your mortgage by then, and that you have sufficient healthcare insurance to cover your medical expenses.

Here’s an infographic that illustrates this concept better:

Graphic: POSB; OECD = Organization for Economic Cooperation and Development

Do note that the illustration above doesn’t take into account inflation levels and increased cost of living — for example, your $3.50 bowl of mee pok won’t cost the same 20 years later. Assuming an inflation rate of 2% per year, expect to pay at least $5.20 for that same bowl of mee pok in 2040.

Some ways to continue your retirement planning now

If you don’t know where to start or how to keep going, here are some ways to become #RecessionReady and continue saving for retirement:

1. Build up your savings

It’s always a good idea to save instead of spending our entire paycheck. For best results, choose a bank account that gives a good savings interest rate, and/or has bonuses that can further elevate your savings.

For example, you can get up to 3.8% p.a. interest on the DBS Multiplier Account if you meet all the requirements. Pair this with a POSB Save As You Earn (SAYE) Account for an additional 2% p.a. interest* on the amount that you decide to save monthly from your salary.

*Only for the first 2 years, terms and conditions apply

How this works: Save a fixed amount into your POSB SAYE account each month with funds from your DBS Multiplier Account and don’t withdraw anything from your POSB SAYE account to earn an additional 2% p.a. interest on your monthly savings for the first 2 years.

2. Invest your extra cash

Instead of leaving all of your money in your savings account, why not channel your extra cash into investment plans such as bonds, exchange traded funds and unit trusts? You can also consider a mix of lump sum investing or a regular savings plan such as POSB Invest-Saver from as low as $100 per month.

3. Get an SRS account

SRS stands for Supplementary Retirement Scheme. Although set up by the government, it’s totally voluntary and is designed to work in tandem with CPF (that we might have already drained dry to pay for our HDB flat).

SRS contributions are also eligible for tax relief, subject to a contribution cap. And while there is an early withdrawal penalty of 5%, the money in your SRS account can still be taken out before retirement age, unlike CPF.

I’m still not ready to put a big chunk of money into SRS, but I’ve already gone ahead to open an account with my bank (I did it online, it was really quick).

In addition, opening an SRS account right now and making a contribution (I’ve put $1 for now, the minimum amount) means that I have “locked in” the age where I can start withdrawing my SRS monies without any early withdrawal penalty, i.e. at 62 years old, following the current official retirement age as of 2020.

This SRS retirement age will remain valid for me, even if Singapore’s official retirement age is revised upwards to say, 67 years old, in the future. I won’t need to keep “chasing” the retirement age for my SRS account.

Although there’s currently only $1 inside my SRS account, it’s a friendly reminder for me to continue saving for my retirement.

SRS moolah needn’t sit stagnant in the account, either. It can also be invested — potentially more retirement funds for you in the future! Find out more about POSB’s Supplementary Retirement Scheme here.

4. Protect & grow your money with insurance

While we find all means and ways to save and grow our cash, we need to make sure that our hard-earned money is protected as well. A full suite of insurance plans that cover health, hospitalisation, life, critical illness, personal accident and more can help with that.

Others, such as insurance savings plans, endowment and investment-linked insurance policies can also aid us in growing our cash while providing additional protection to our existing insurance portfolio.

For example, with POSB’s Manulife SmartRetire and RetireReady Plus II plans, you can customise your retirement plan to fit your desired lifestyle and receive monthly income during your chosen retirement period.

5. Talk to your wealth planning manager

While almost everything can be done online on our own, sometimes the human touch makes a big difference. Newbie investors or those stuck between 2 important financial decisions might want to speak to an actual person with keen financial acumen — AKA a wealth planning manager.

It’s nice to know that POSB offers the option for a no-obligation chat with its experts on retirement planning or any other financial issues I may have. POSB also has a new TeleAdvisory service that allows me to chat with its wealth planning managers from the comfort of my home sofa.

6. Make full use of free online tools

As a kiasu Singaporean, I don’t let free things pass me by. Make use of free online tools and resources.

On the POSB website alone, there are calculators, as well as powerful web app NAV Planner to help you manage and analyse how you spend, save, grow and protect your money. There’s also a bunch of helpful articles for newbie investors to learn, and useful tips for everyone to get in better financial shape.

Times may be tough now, but it’s prudent to continue saving for retirement. Check out POSB’s one-stop guide to retirement planning here.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability. All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single product issuer. This advertisement has not been reviewed by the Monetary Authority of Singapore.

The material and information contained herein is for general circulation only and does not have regard to specific objectives, financial situation and particular needs of any specific investor individual and/or entity (collectively referred to as investor), wherever situated. The material and information contained herein does not constitute an offer, invitation, recommendation or solicitation of any action based upon it and should not be viewed as identifying or suggesting all risks, direct or indirect, that may be associated with any investment decision. Prospective investors should seek advice from a financial adviser regarding the suitability of the product before making a commitment to purchase the product. In the event that the prospective investor chooses not to seek such advice, he/she/they should carefully consider whether an investment in the said securities is suitable for them in light of their own circumstances, financial resources and entire investment programme.