So it’s finally official. On 18 Sep 2024, the US Federal Reserve, the central bank of the world’s largest economy, announced a 0.5% (50 basis points) cut to its benchmark interest rate.

Big deal. You may ask, “What does a bunch of boomers gathering to talk about monetary policy have anything to do with you and me”? Well, as it turns out, quite a lot!

That’s because interest rates from the US impact the prices of all sorts of assets worldwide, from stocks and real estate to bonds and cash savings products.

It’s also a significant moment as this is the first interest rate cut from the US Fed in over 4 years. Remember that the last time the central bank cut its interest rate was at the start of the Covid-19 pandemic in early 2020.

We all like to say that “Cash is king” and it's the “best thing to own if interest rates are high”. That’s a completely normal assumption to make because high interest rates means we can get more moolah for our cash savings.

But now that the US Fed has cut its interest rate, what happens to “my precioussssssss” (i.e. our cash)? Let’s find out.

Falling interest rates = falling cash rates

What’s the actual “interest rate” we’re all talking about called, anyway? Well it’s referred to as the “Fed Funds rate” and it sets the precedent for how a whole host of other assets are priced, from loans on housing all the way through to the yields you receive on bonds.

Understanding the whole concept of interest rates is the first place to start. Some of us might remember that interest rates in the decade before the Covid-19 pandemic (and also during it) were close to 0%. As a reminder, right now (after the latest cut), the Fed Funds rate in the US is in a range of 4.75% to 5.0%. That’s pretty high by recent standards!

Overall, the US economy (and US dollar) are so central to how the world economy functions, that whatever the Fed does with interest rates impacts countries everywhere—including Singapore.

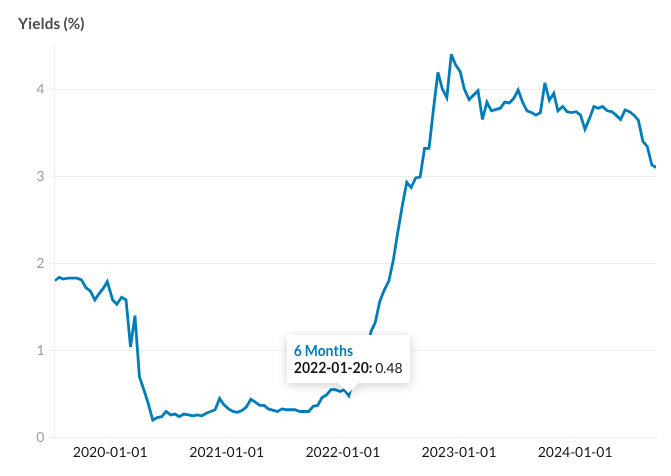

Indeed, in the depths of the Covid-19 pandemic when the Fed had its interest rate close to 0%, a lot of the yields (or annual return) you could expect to receive on “safe” investments also fell alongside it. Just taking a look at the yield on the Singapore 6-month T-bill during the pandemic tells you exactly that.

The 6-month T-bill yield dropped to as low as 0.2% in May 2020 and even at the beginning of 2022, the 6-month T-bill yield was still only 0.48%. Given Singapore’s government has a super safe and strong reputation, owning its T-bills is (almost!) like holding cash.

Singapore T-bill yields (6 months)

Sources: Business Times, MAS

But interest rates move in cycles and that was also the case with the US Fed. Interest rates at close to zero couldn’t stay that way forever, even though many of us wished it could—who doesn’t like cheap money?!

Less of a reason to be holding cash

Just look at the “peak” in what buying a T-bill could have got you in the past few years —if you had bought a Singapore 6-month T-bill back in August 2022 you would have received a yield of 4.4%. That’s pretty good, more than the 4.05% you’d get from whacking any money into your CPF Special Account (CPF SA). But fast forward to today and the most recent yield for the mid-September 2024 6-month T-bill offering was 3.1%.

We can already see that it’s fallen some way from where it was in 2022! That tells us something. Essentially, even before interest rates are officially cut, the yields on T-bills in Singapore have been falling. Why’s that the case? Well, basically, the Fed has been telling the market since late 2023 that its interest rate is high enough.

It went a step further last month (August) when the Fed Chairman Jerome Powell officially said that the time has come for an interest rate cut. So, even before last month’s remarks, you can see that the T-bill market was anticipating falling rates.

So, should investors actually be in cash when interest rates are falling? Well, besides having your normal emergency fund (6-12 months’ of your expenses) there is an opportunity cost to holding on to too much cash.

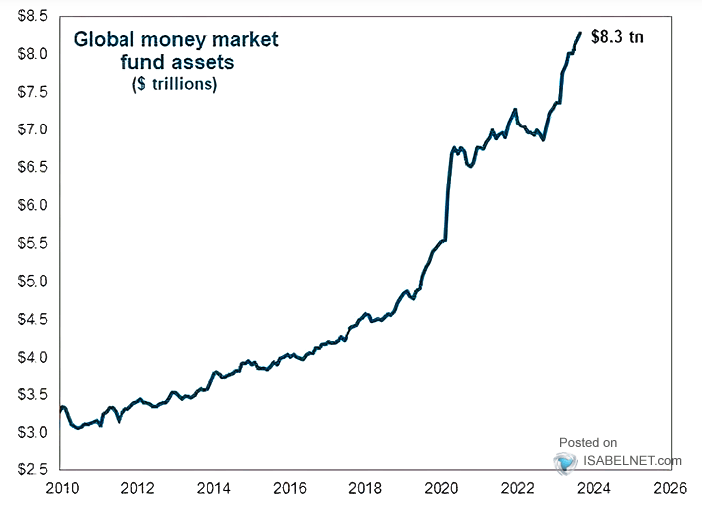

It made total sense to go hold cash and earn between 4-5% annually for basically doing nothing. In Singapore, we could get close to 4% in a Singapore Dollar money market fund (MMF). If you wanted to change your Singapore dollars into US dollars, you could actually get just over 5% in a US Dollar MMF. As a reminder MMFs are basically a short-term cash deposit fund, with your annual rate tied to global interest rates (i.e. the Fed Funds rate).

As you can see below, the timing of the interest rate hikes in 2022 also coincided with a massive increase in the amount of money that was going into global MMFs. No coincidence. People become less risk-averse when you can get a good yield for not taking any risk in the markets.

Sources: IsabelNet.com, Goldman Sachs

That chart was from late 2023 and it went even higher before the year was out, with the latest data from Fitch Ratings saying that by the end of 2023, there was an incredible US$9.9 trillion in global MMF assets.

However, now that interest rates are falling, there’s less of a reason for us to be holding on to so much cash as the annual return on that is going to fall as the Fed continues to cut interest rates in the rest of 2024 and into 2025.

What do interest rate cuts mean for Singapore investors?

For Singapore investors, one of the main effects of falling interest rates will likely be seen in the local stock market.

There are many companies listed on the Singapore Exchange (SGX) that are impacted by the Fed’s interest rate policy, with real estate investment trusts (REITs) and banks among the 2 biggest areas that could see a change.

Starting with REITS

Why is that? Well for REITs to grow, they need to rely on the Big D—Debt—to grow their portfolios of properties. That’s not ideal when interest rates are high (duh!) since debt costs more. That’s why we’ve seen many Singapore REIT share prices suffer in the past 2 years as debt costs skyrocket and their distributions (or dividends) fall.

However, we’re now seeing a reversal of that trend with interest rates starting their slow descent. Indeed, the day after the rate cut by the Fed (19 Sep 2024), the i-Edge S-REIT Index was up 1.7%. Over the past month, the index is up over 9%.

That tells you that investors are now willing to put some of their (hard-earned!) money into Singapore REITs given their yields are starting to look attractive versus what you can get on cash. Remember, the market always moves ahead and anticipates what’s actually going to happen.

In that sense, you might see the share price reactions or market movements before the actual event takes place. Interest rate cuts are a prime example of that.

And now, the banks

Meanwhile, as for Singapore’s big 3 banks—yes, the OGs of Southeast Asia bank stocks as our parents like to tell us—there are concerns that falling interest rates will hurt their main business of lending.

Banks don’t actually do anything too complicated to earn money; they take in deposits from you and me (pay us an absolute pittance in interest) and then lend it out to corporates or individuals at much higher rates of interest. Tada! You can make money. That’s called “net interest income” or “NII”.

Naturally, Singapore banks and their levels of NII might fall if interest rates come down. But that’s expected and Singapore banks still offer very attractive dividend yields of close to 6%. That’s probably the main reason we haven’t seen their share prices fall so much on the interest rate cut. Furthermore, these banks have other business lines that can actually benefit from falling interest rates—like wealth management (i.e. more people are going to be investing their cash in investment products sold by these banks).

ALSO READ: The Ultimate Guide to the Best Priority Banking Accounts in Singapore

Keep watching out for impact of further cuts

It’s normal to feel like “Christmas has come early” with the interest rate cut but we should also remember that the Fed typically cuts interest rates if it’s worried about the US economy’s prospects. Indeed, it is concerned right now about the labour market/jobs market in the US—which is showing signs of weakness.

If the US goes into a recession, then it’s likely going to impact the world. Overall, interest rate cuts by the Fed will certainly incentivise Singaporeans (as well as other people) to not hold as much cash but we should also watch how quickly the US central bank cuts interest rates from here.

Found this article useful? Share it with fellow investors!