Everyone experiences bad luck now and then. Like when you don’t strike Toto, the MRT breaks down, or your HDB block didn’t get selected for en bloc.

But what about if you get hit by some ah beng on an e-scooter, fall onto the road and then get run over by a truck? You’re probably going to wish you were covered by personal accident insurance before the dreadful incident.

No clue what this whole personal accident insurance thing is about? Simply put, personal Accident insurance plans cover you if you suffer from an accident. But that’s not all. Some plans might also cover various other annoyances in life, such as infectious diseases like dengue and Zika.

7 best personal insurance plans in Singapore

Here’s a list of personal accident insurance plans offered by reputable insurers in Singapore. Many of these insurers offer a range of plans, depending on how much coverage you need and how much you’re willing to pay. Let's say you're looking to insure yourself with $100,000 accidental death and total permanent disability (TPD) in case you run into a personal accident. You don't have children currently and hold an executive office job:

Personal accident insurance plan | Annual premium |

FWD Personal Accident Insurance Plan A | $122 |

MSIG Protection Plus Silver | $125 |

ERGO AccidentProtect Individual Basic | $127 |

Tokio Marine TM 365 Plan B | $142 |

Bubblegum Enhanced | $147 |

HL Assurance Family Protect360 Silver | $151 |

AIG Sapphire Enhanced Basic Standard | $173 |

These insurance premiums sit on the cheaper end of the spectrum. Personal accident plans like the AIG Sapphire Enhanced Comprehensive Standard will cost you $227 in premiums per year, the Sompo PAStar Deluxe will cost $196, and the Sompo PA Ease Plan 2 comes at a premium of $233.

Your premiums may vary slightly depending on your age, gender, and even the nature of your job (e.g. your premiums will be higher if you tend to go out more in a sales job, or work outdoors since it's more risky).

1. FWD Personal Accident Insurance Plan A (100k)

In addition to the usual payout if you pass away or suffer from permanent total and partial disability due to an accident, FWD personal accident insurance plans have a few additional perks, including TCM, physiotherapy, and chiropractor treatment expenses, coverage for food poisoning, insect bites, and more.

Infectious viruses are on our minds these days—luckily FWD also offers protection against infectious diseases like dengue and Covid-19. Plus, if you’ve been hospitalised for 5 days or more for one of these infectious diseases, you get coverage for medical expenses and daily hospital income.

A useful feature of this plan is that you can get adventure sports coverage at no additional cost. Perfect for you adrenaline junkies out there.

FWD personal accident insurance starts from a coverage amount of $100,000 and goes up to $1 million.

View and compare FWD personal accident insurance benefits.

Sample annual premium for $100,000 accidental death and TPD coverage:$122

2. MSIG Protection Plus Silver

The basic version of this MSIG personal accident insurance plan offers payouts for death, permanent disablement both total and partial, as well as quite a wide variety of other costs, such as worldwide medical expenses, hospitalisation cash benefits and recuperation benefits.

What stands out about this plan is that it pays out 150% of your sum assured if you suffer from permanent and total disablement, and 100% if you suffer from permanent and partial disablement.

This plan is also a good choice for families with kids, as up to 3 children enjoy free coverage when you sign up for the plan with your spouse.

Sample annual premium for $100,000 accidental death and TPD coverage: $125

3. ERGO AccidentProtect Individual Basic

ERGO doesn’t have a very strong presence in Singapore, but the ERGO personal accident insurance actually has quite a decent list of benefits.

Other than the usual payout if you die, the plan will pay out double if the accident happens on public transport or in an earthquake, cyclone, typhoon, hurricane or flood. You also get 150% if you suffer from total and permanent disablement.

You are also entitled to reimbursement of medical expenses incurred due to an accident as well as 20 infectious diseases like dengue and hand foot mouth disease. Other perks include a weekly income benefit if you are unable to work and repair or replacement costs for personal effects and belongings damaged in an accident.

This plan covers TCM treatment, but not chiropractor treatment.

If you and your spouse are covered under the same policy, all your children get free coverage for 20% of your plan.

Sample annual premium for $100,000 accidental death and TPD coverage: $127

4. Tokio Marine TM 365 Plan B

Tokio Marine's personal accident insurance offers $100,000 if you suffer from accidental death or permanent disablement, as well as up to $4,000 reimbursement of medical expenses per accident.

You get double the sum assured if you die on public transport.

Other perks include a weekly income benefit for up to 104 weeks if you suffer from temporary total or partial disablement, recuperation or ICU benefits and trauma support if you suffer from PTSD due to permanent disablement.

Think you might need to visit a chiropractor or TCM physician? This plan will reimburse you up to $1,000 for these treatments.

Sample annual premium for $100,000 accidental death and TPD coverage: $142

5. Bubblegum Enhanced

Bubblegum Personal Accident Insurance comes in 3 tiers, with the middle tier (Enhanced) offering $100,000 coverage for accidental death and TPD. The coverage doubles from one tier to the next, but thankfully the price doesn't follow suit.

Coverage | Essential—$74 | Enhanced—$147 | Elite—$286 |

|---|---|---|---|

Accidental Death | $50,000 | $100,000 | $200,000 |

Permanent Disability | $50,000 | $100,000 | $200,000 |

Medical & Surgical Expenses (per accident) | $1,000 | $2,000 | $4,000 |

Medical Expenses by TCM Practitioner/Chiropractor | $500 | $1,000 | $2,000 |

Ambulance/Transport Fees | $50 | $100 | $200 |

Mobility Aids/Home Modification Benefit (per accident) | $500 | $1,000 | $2,000 |

Infectious Disease Hospitalisation Benefit (medical and surgical reimbursement per event) | $500 | $1,000 | $2,000 |

Daily Hospital Cash (max 30 days/accident) | $50 | $100 | $200 |

Bubblegum is a good option to cover your bases. The Enhanced plan covers all the basics with $100k for death, disability, $2,000 for medical, and $1,000 for any mobility aids like crutches or home renovations (mounting hand railing or slopes) to help yourself with moving around.

What about extra perks? Like the Tokio Marine plan above, you can get reimbursed up to $1,000 for chiropractic or TCM treatments too. If you're a parent, you can get up to 10 children covered $25,000 each for death/TPD. Adding 1 child will bring the premium for the Enhanced plan up to $164, which is just an additional $17.

Premiums will be higher if you're involved in manual work, but you'll be happy to know that they don't increase with your age.

Sample annual premium for $100,000 accidental death and TPD coverage: $147

6. HL Assurance Family Protect360 Silver

As you can guess from the name, this HL Assurance personal accident insurance plan is aimed at families with kids.

In addition to the usual protection from accidental death and permanent total disablement, the plan also offers reimbursement for accidental medical expenses, payouts for children’s education and parent’s support, as well as family cash relief.

Children in the family get free coverage, and the plan offers a unique 15% cashback bonus for every 12 months you go without making a claim.

Sample annual premium for $100,000 accidental death and TPD coverage: $151

7. AIG Sapphire Enhanced Basic Standard

You have a few options for AIG personal accident insurance. Perhaps the most value for money option is the AIG Sapphire Enhanced Basic Standard, which offers $100,000 coverage for accidental death or TPD.

AIG also offers coverage for things like TCM expenses, chiropractor treatments, dental treatments due to accidents, ambulance services, mobility aids, dengue fever, insect bites, food poisoning, motorcyling, and reservist training! There's a lot of areas this plan will cover for you.

Notably, AIG personal accident insurance also offers a parent support fund. In the event of your accidental death, they'll give $1,000 to each surviving parent. That's not a lot in the grand scheme of things, but it's better than nothing. Plus, this benefit goes up to $5,000 for their Prestige tier.

What if you're the parent? If you insure your child(ren) too, they get free coverage of up to 20% or 25% of your benefits.

What if you're a pawrent? AIG has thought of that too. If you get hospitalised and your pet needs a place to stay, they will pay out $50 per day for the cost of placing your cat or dog at a kennel, cattery, or pet hotel.

Sample annual premium for $100,000 accidental death and TPD coverage: $173

What is personal accident insurance anyway?

Personal accident insurance is designed to give you or your family financial support should you die in an accident or become permanently disabled. It will also take care of some of your medical expenses.

While different policies are going to cover you in slightly different ways, it’s helpful to know the main types of Personal Accident coverage policies insurers tend to offer.

Accidental death: If you pass away within a time limit (usually 12 months) from the date of an accident, your family will receive a payout worth 100% of the sum assured. It must be proven that your death was due to an accident, rather than natural causes or an illness or injury that wasn’t due to accidental causes.

Total permanent disability (TPD): If you get disabled seriously enough to qualify as permanently and totally disabled within a time limit (usually 12 months) from the date of an accident, you will receive a lump sum payment. In order to be considered permanently and totally disabled, you usually need to lose your sight in both eyes, lost both your hands and feet, or any combination of the above, or lose your hearing and speech. You should also no longer be able to work in any job.

Partial permanent disability: If you’re permanently disabled but not seriously enough to be considered totally disabled, you can still get a percentage payout of the sum insured. For instance, you might receive a payout of 20% for the loss of an eye.

Temporary disability: If you’re disabled as a result of an accident for just a temporary period but are unable to work during that period, you might be eligible for benefits until you have recovered and are able to work again. These benefits are usually given in weekly cash payouts for a certain number of weeks. If you are suffering from a total temporary disability that makes you completely unable to work, you’re eligible for the full sum of temporary disability benefits. If you can perform your duties at work partially, you will get only a fraction of the temporary disability benefits.

Medical expenses: You can also make claims for medical expenses arising as a result of an accident. However, do note that coverage is paltry compared to what is offered by health insurance, and many types of treatment are excluded.

Daily hospital cash benefit: Some policies offer a daily allowance for each day you’re hospitalised because of an accident up to a maximum number of days.

Medical evacuation: Should you get into accident while overseas, some policies will pay for the cost of emergency evacuation, or repatriate your body back to Singapore if you die.

Do you need personal accident insurance?

Accidents can happen to anybody, but is personal accident insurance something you really need, or is it another way for insurers to prey on your fears? Let’s talk about who it’s important for and why.

You might need personal accident insurance more than the average person if…

You are working in a risky job: If your job contains an element of physical risk, personal accident insurance is a must. This is especially so if you are not eligible for compulsory Work Injury Compensation Insurance and you don’t have or have inadequate employer-sponsored insurance. So if you’re working in construction, doing factory work or are a delivery driver, you definitely want to consider getting insured.

You participate in risky or extreme sports: If you’re a parkour enthusiast who likes jumping off the roof of buildings or climb mountains for fun, your chances of fatal accidents might be higher than someone whose hobby is reading. Just make sure your activities are not excluded from coverage. FWD personal accident insurance might be a good option for you in this case because you can add sports coverage at no extra cost.

You commute by motorcycle or ride your bicycle or electric scooter on the road: Singaporeans aren’t exactly the most careful or considerate of drivers. That means plying the roads on a motorcycle, bicycle or e-scooter can be like trying to cheat death. If that’s your preferred mode of commute, your risk of accidents is higher than that guy who takes the MRT. If you ride regularly, check out AIG personal accident insurance—they include motorcyling in their coverage.

You travel often to remote or unsafe areas: Singapore might be as safe as it gets, but the same cannot be said of many other places in the world. If you often travel to remote areas where it would be difficult to get you to a hospital if you were to get hurt, or visit war-torn or crime-ridden countries, make sure you’re well insured.

You have family members who depend on you financially: If you die or become incapable of working, your family members will be in a very bad place financially. It is thus essential to protect them with insurance should something happen to you. Some good options for family-friendly personal accident plans include HL Assurance Family Protect360 Silver, MSIG ProtectionPlus Silver, and ERGO personal accident insurance, with which children can get free coverage.

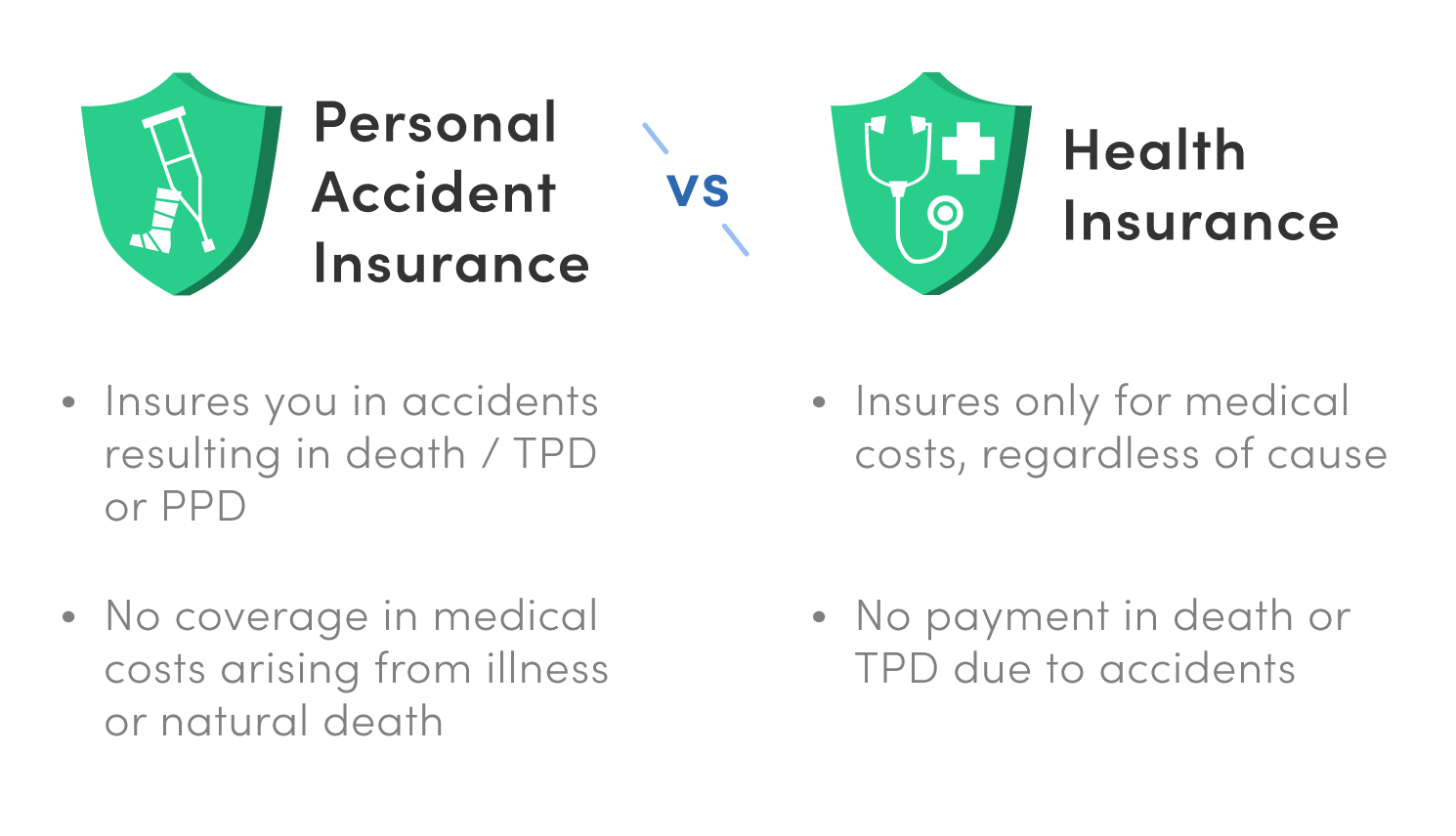

Personal accident insurance vs health insurance—what's the difference?

Personal accident insurance sounds nice to have, you say, but you already have health insurance that can save you if you get hospitalised. What’s the difference between the two?

Health insurance is designed to cover the costs of medical treatment should you get hospitalised. But your health insurance policy is not going to pay your family a single cent if you get involved in an accident and are killed on the spot.

If you survive an accident but are permanently and totally disabled, personal accident insurance will offer you a payout that will help you to survive your remaining years without working. Health insurance will only cover medical bills incurred after the accident, but will not provide you with anything beyond that.

It should be noted that personal accident insurance only covers you if you are involved in an accident, not if you fall ill or get injured because of natural causes or other reasons that can’t be classified as accidents. Health insurance, on the other hand, doesn’t care how you wound up in the hospital (unless the reason is excluded under the policy) and pays your expenses regardless.

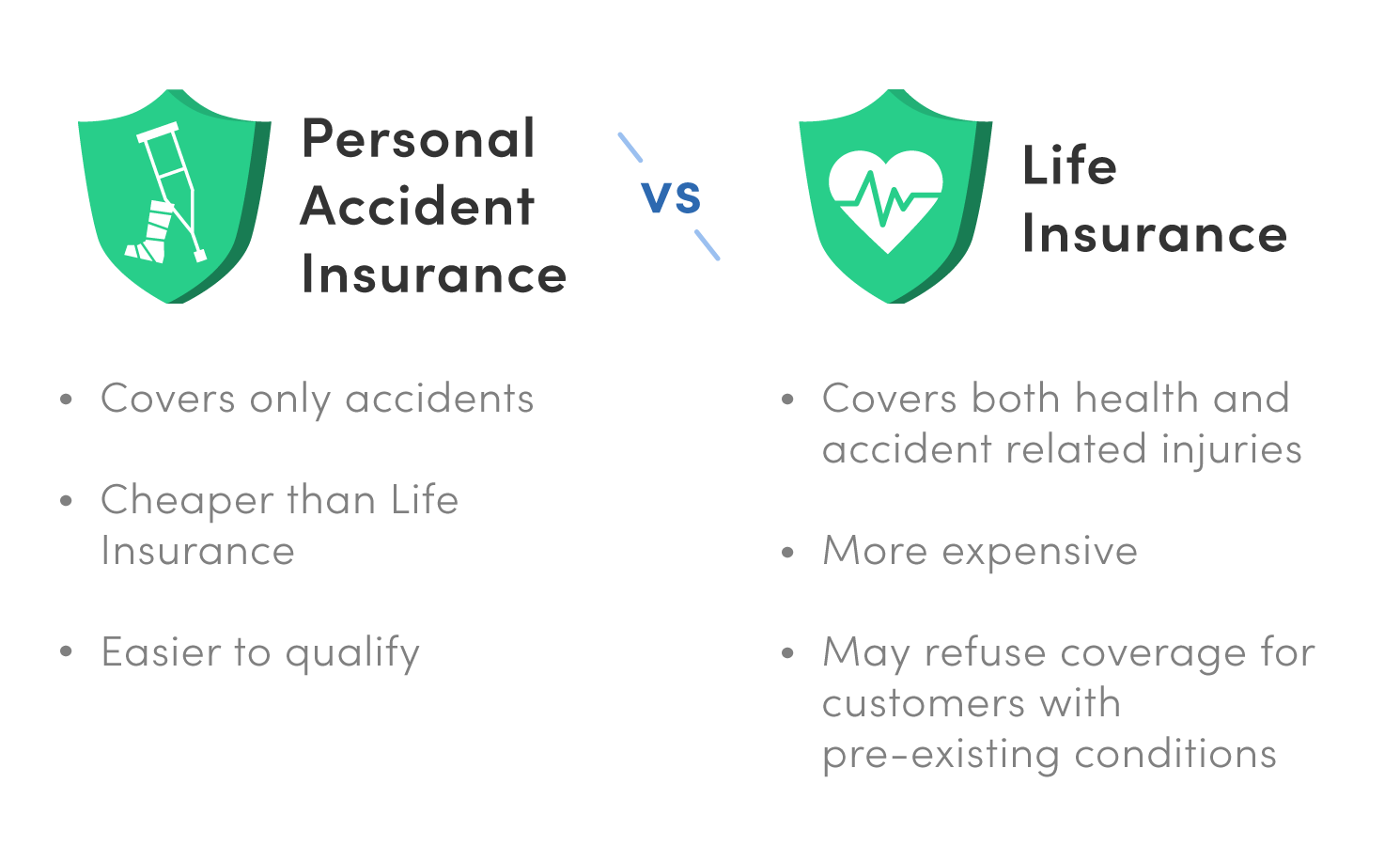

Personal accident insurance vs life insurance—what's the difference?

Well, what about life insurance? This looks very similar to personal accident insurance, since both offer payouts if you die or are totally and permanently disabled.

Life insurance is broader in coverage, as it offers a payout if you die or become disabled for any reason (except those that are excluded in the policy). So basically, life insurance tends to offer better protection.

That sounds great… but it also tends to be a lot more expensive than personal accident insurance. What’s more, insurers may refuse to offer you life insurance if you have pre-existing medical conditions. Personal accident insurance is not only cheaper but easier to qualify for.

Of course, some people choose to have both life and personal accident insurance to ensure their family gets well taken care of if they die or are no longer able to work.

Verdict: Which is the best personal accident insurance plan?

In terms of cost, for someone looking for a sum assured of $100,000, FWD Personal Accident Insurance Plan A is hands down the most affordable option, and is particularly worth it for those who do sports since they have a free sports cover.

If you’re looking for the most well-rounded plan, the MSIG ProtectionPlus Silver has average premiums compared to the others on the list, but still packs a punch in the range of benefits offered.

The plan stands out thanks to the generous permanent disablement limit of 150% your sum assured. Although the medical expense benefit could be better, the former more than makes up for it.

But that’s not all. The plan also offers benefits for temporary total disablement, temporary partial disablement, hospitalisation cash benefits, recuperation benefits, bereavement grant and terrorism cover. And very importantly for families, up to 3 children receive free coverage when you and your spouse enrol at the same time.

It would actually cost you less to sign up for this plan than to pick one the cheapest plans on the list and then add on cover for temporary disablement, hospital or child benefits.

Share this article with anyone who might need personal accident insurance!

Related Articles