It doesn’t matter how old you are or how much income you earn every month — everyone needs insurance. Most people already know that, but how much insurance coverage do you need?

The hard truth (ha ha) is that too many Singaporeans don’t have enough insurance coverage because they simply don’t know how much insurance they need in the first place.

What do we mean by insurance coverage?

By insurance coverage, we generally refer to the number called "sum assured" or "sum insured" in a life insurance policy.

This is the amount of $$$ you or your dependents get if you die, become permanently disabled, or get a critical illness diagnosis (if covered by your policy).

Most life insurance policies allow you to choose your desired sum assured, and your premiums will vary accordingly.

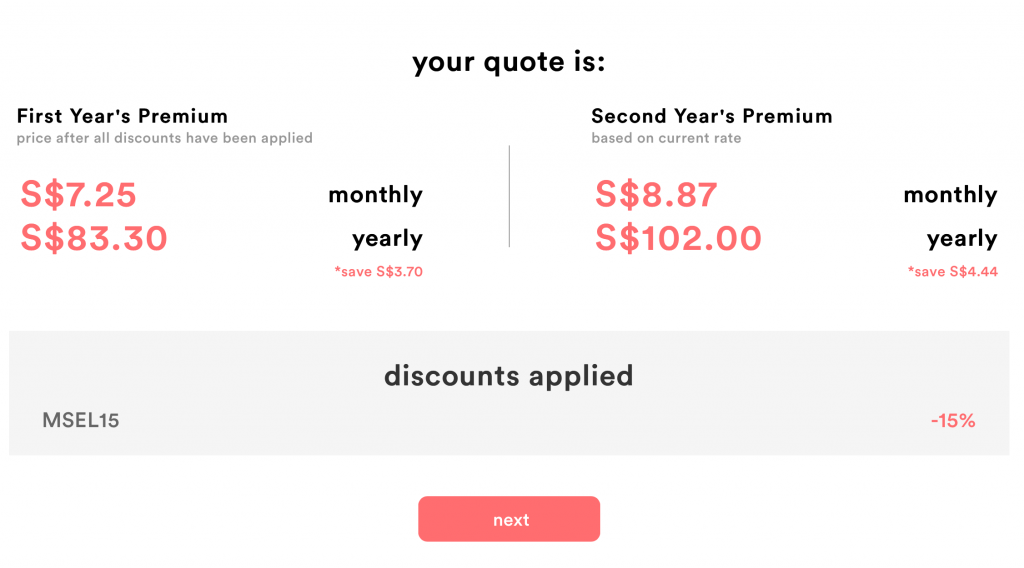

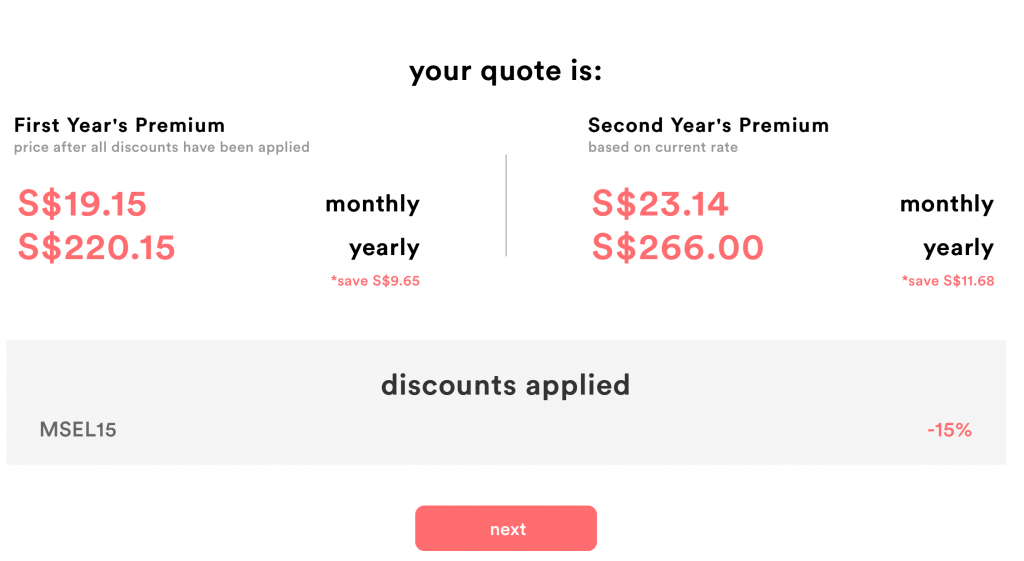

For example, let's look at the premiums vs sum assured for FWD Essential Life term insurance, which is a policy you can get quotes for and buy online.

Let's say you're a 28-year-old, non-smoking female looking for a policy with sum assured of $200,000. The annual premium is very cheap, starting from $83.30/year.

If you were to choose a sum assured of $700,000, your premium would naturally be higher, from $220.15/year.

So how much sum assured is enough?

Notice how the premium increase isn't exactly proportionate to the difference in sum assured?

While some insurers advertise their cheap premiums at their lowest sum assured, it may be more bang-for-buck to opt for a higher sum.

In fact, it's important not to be too distracted by the premiums, because it's a lot more important to figure out what insurance coverage you need. That is the point of insurance, after all.

Being underinsured puts you and your dependents financially at risk. Young Singaporeans in their 20s and 30s are particularly vulnerable to being underinsured — which is ironic because these are the years when you should be buying enough insurance to protect your earning power and wealth.

To illustrate how much insurance every young Singaporean needs, let's take look at an average Singaporean’s journey as he meets with an experienced financial planner to get an idea of how much insurance coverage he needs.

Say hello to Mark, a young 25-year old Singaporean professional earning $3,000 a month.

Part 1: Determine liabilities

Mark chose an insurance agent to help him make sense of his financial situation so that he knows how to protect his wealth. In Mark’s case, the first thing his financial advisor asked him was “What are your liabilities?”

Liabilities include monthly bills and any outstanding loans. This is Mark's list:

Liability | Amount Paid Each Month | Necessity (Is it a life essential?) |

Handphone bill | $100 | Yes |

Gym membership | $100 | No |

Utilities bill | $200 | Yes |

Car loan ($40,000 outstanding) | $600 | No |

Personal loan (laptop purchase, $2,000 outstanding) | $200 | Yes |

Part 2: Determine expected living expenses (if "something" happens...)

Next question - "What happens if you become completely disabled in a car accident?" Mark has no real answer, so this is when his financial planner does his calculations.

Judging from his debt liabilities, Mark would be an upfront lum sum payable of $42,000 (outstanding car loan + personal loan). That’s because in the event of an accident, there’s no way he would be able to make payments on his obligations.

His necessities on the other hand would amount to $300 (handphone + utilities) per month – payments that would still need to be made even if Mark had no way of paying them!

Additionally, Mark's monthly expenses would increase drastically. He would need medication, regular medical consultations and a caretaker to watch over him. Not to mention there would be huge medical bills to pay off as well (since we all know hospitals won't treat your injuries out of charity).

Mark’s financial planner provides him a list of possible monthly living expenses IF an accident did occur:

- Food ($450)

- Medication ($100)

- Maid/nurse ($1,000)

- Medical consultation ($200)

- Transportation ($100)

- *Initial lump sum for medical treatment after accident ($50,000)

Falling off your chair? It gets worse. This is actually a very frugal estimation – your monthly expenses and initial lump sum for treatment are expected to be much higher.

Part 3: Tally up how much insurance coverage is needed

The financial planner will then evaluate the total lump sum and monthly expenses that would be needed after looking at the revised expenses in the event of an accident that may leave Mark permanently disabled.

Lump sum payments | Monthly expenses | ||

Car loan | $40,000 | Total liabilities | $300 (handphone + utilities) |

Personal loan | $2,000 | Food | $450 |

Initial lump sum (treatment) | $50,000 | Medication | $100 |

Maid/nurse | $1,000 | ||

Medical consultation | $200 | ||

Transportation | $100 | ||

Total lump payment | $92,000 | Total monthly expenses | $2,150 |

After tallying up these numbers for Mark, his financial planner asks him to think about the possibility of living another 10 to 20 years. Adding 3% annual inflation, the total amount he would need over the span of 10 to 20 years would be (with 3% annual inflation):

Liabilities | Total expenses | Grand total | Annual inflation (3%) | |

10 years | $92,000 | $2,150 X 12 (months) X 10 (years) = $258,000 | $350,000 | $472,000 |

20 years | $92,000 | $2,150 X 12 (months) x 20 (years) = $516,000 | $608,000 | $820,000 |

It becomes immediately apparent that he needs $472,000 to $820,000 in his bank account just to survive another 10 to 20 years!

That amount will wipe out his savings and investments. Take for instance he has savings amounting to $10,000 and $50,000 in investments, he will barely be able to pay off his immediate liabilities ($92,000).

If Mark has no insurance, it means that Mark is severely underinsured. To cover his current and future expenses, he has to get insurance with a sufficient sum assured that will enable him to live for another 10 to 20 years.

As an estimate, you need at least $500,000 insurance coverage for 10 years

So how much insurance do you need if you’re a single Singaporean? Roughly $500,000 in coverage (or sum assured) is the answer – and that’s if you’re A) living on a very frugal $2,000+ a month, and B) if you’re expected to survive another 10+ years.

That insurance coverage number is in line with what the amount of insurance recommended by the Life Insurance Association (LIA) Singapore for the average working adult in an average household – which is $490,000.

Just remember that it only takes one accident to wipe out your savings. Don't simply choose the cheapest policy available or skip out on insurance entirely. It's important to protect your wealth before you invest.

Found this article useful? Share it with anyone who needs to know about insurance coverage.

Related Articles