This post was written in collaboration with Prudential. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best recommendations and advice in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

I don’t know about you, but growing up, I thought the only way to live was the conventional 3-stage life — study till my 20s, work till 65, retire.

How anyone could deviate from this preconceived norm, I couldn’t fathom. Unless they were born with a silver spoon, how could people afford to take a long break from work to study or travel the world and still feed their family?

In addition, more people in Singapore are living to 100 years old. According to this Ready for 100 whitepaper, “in 1950 just 50 people were 100, but in 2015 it was 1,100, and this rate continues to rise”. This means that after retirement, we have at least 30 years to go…

Then I realised, with the right financial planning, our lives needn’t be a chore but a series of adventures!

With increasing longevity, we could instead be living “multi-stage lives” — multiple careers perhaps, a second (or third) wind, career breaks to do something we’ve always wanted to, the chance to be there for our family’s growing years, and even attaining financial freedom earlier to pursue our passions.

Just look at Marie Wee, who wore various hats as a writer/editor, real estate agent, public relations professional, mum and now, company owner. There’s also Darren Ho, founder of AUGUSTMAN magazine who decided to take time off to reassess his life, travel and pick up a new skill. Read on for their stories.

Could us, too, experience fruitful multi-stage lives without worry? How can we plan and save for our many milestones? Here are some tips and common scenarios to help kick start your journey:

Fiscal discipline is key

In all of the scenarios below, our characters all have 1 thing in common — discipline when it comes to money matters. Here are some general tips:

- Set up savings goals that you can work towards

Do all of your sums beforehand and set up a savings goal with quarterly targets to hit, on a fixed schedule. For example, you can put aside a small sum of money each month to fund your goal. Those with more commitments can consider setting aside smaller amounts of money, over a longer time horizon.

- Work out ways to reduce monthly expenses

Log your expenses and look into ways to reduce fixed costs such as mortgage, by refinancing with a bank that offers a lower interest rate. You can also prepare more healthy home-cooked meals instead of eating out, or switch to cheaper alternatives. More savings tips here.

- Reduce debt

Don’t take up more loans if you don’t need to (i.e. car loan if you don’t need one to get around), and it’s best not to rack up a large credit card bill as the interest rate on money owed can be very high.

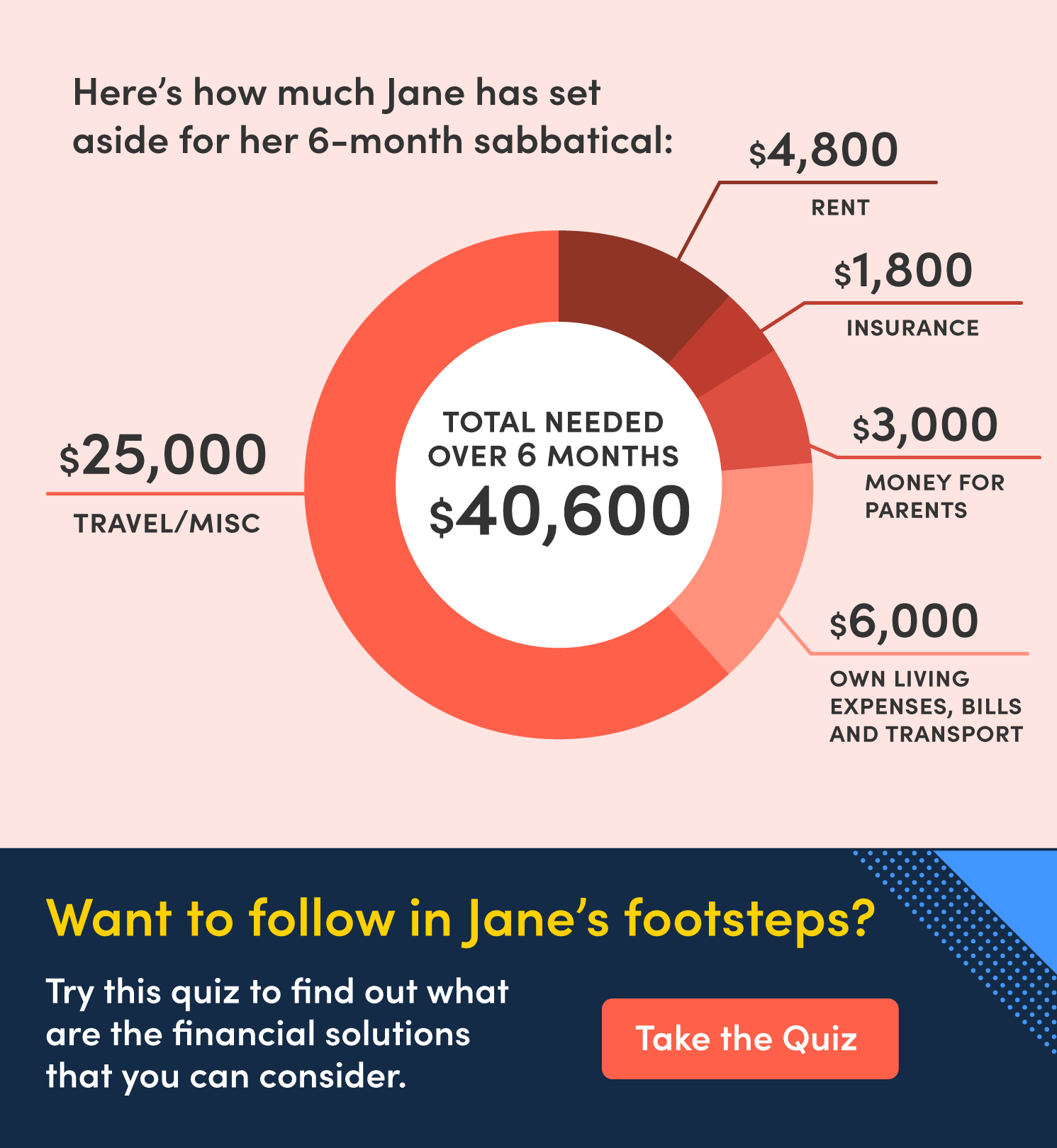

Scenario 1: Planning for a much-needed breather

Jane, 35, has been planning to take a 6-month sabbatical to travel the world (the trip was supposed to happen this year, but due to Covid-19, it’s a no-go). Nevertheless, she remains positive and wants to put the break to good use — serving the community by participating in volunteer work while taking up courses to enhance her work credentials.

Jane is single, so she only needs to provide for herself, cover her room rental, insurance, and other household costs. She and her other siblings give $500 a month to their parents. Her net monthly income (pre-sabbatical) is $4,000.

- Put her extra cash in an insurance savings plan and use the maturity payout to fund this milestone of her multi-stage life

Some ways Jane saved up for her sabbatical include:

Jane parked her extra cash in an insurance savings plan with growth potential and capital guaranteed at maturity. A plan such as PRUActive Saver II ticks these boxes, and offers the option of customising the number of years you save for and even the maturity date. Jane had been diligently contributing to her insurance savings plan since she joined the workforce, and plans to use the lump-sum maturity payout once the plan matures for her sabbatical.

- More mini sabbaticals, more often

Alternatively, Jane could have converted her 6-month sabbatical into a mini sabbatical every 1 or 2 years. With an insurance savings plan such as PRUFlexi Cash, she receives life protection against death, terminal illness and total permanent disability. She also has the flexibility to use her yearly cash benefit for a much-needed break or to accumulate it to earn annual interest. Jane also has an existing integrated shield plan, PRUShield for her hospitalisation coverage (includes overseas medical treatment coverage too).

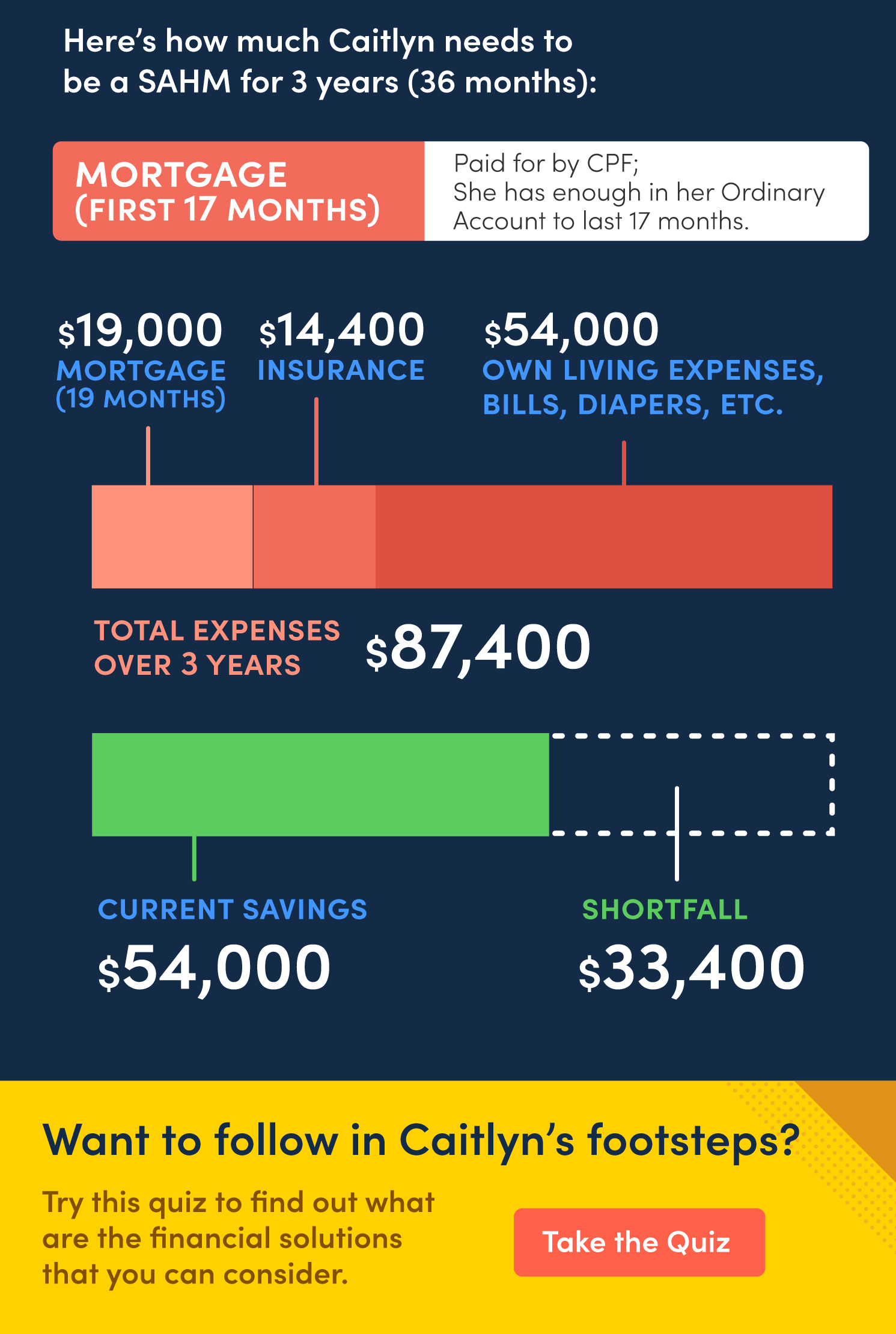

Scenario 2: Taking time to nurture the little ones

Caitlyn, 28, is thinking about quitting her job to be a stay-at-home mum (SAHM) for about 3 years. Her 2 kids are aged 3 and 6 months. Research shows that maternal, home-based care is beneficial for little ones. Older children could benefit too. According to the Labour Force in Singapore 2019 report, 51,600 female residents (aged 15 and above) are not in the workforce as they are caring for their own children aged 12 and below.

Though her husband is supportive and working in a well-paying job, she doesn’t want to stress him financially as his elderly parents aren’t doing too well and need support for their medical bills. As such, she has been planning for this since they got married 5 years ago. Once their children are more independent, she aims to return to the workforce.

Caitlyn is currently drawing a gross salary of $3,500 a month. She is currently living in a 4-room HDB flat and paying a monthly mortgage (via CPF) of about $1,000.

- Drawing money from passive income sources or insurance savings products with a regular payout

Some ways Caitlyn can further maximise her finances include:

Caitlyn has some existing investments that give good quarterly dividends. She is also covered by the PRUFlexi Cash policy and has the option to utilise her yearly cash benefit if the need arises. When she got married, she purchased a PRUWealth II (SGD) insurance savings plan with the extras from her wedding angbao, which offers the flexibility of withdrawals to meet her life milestones — so that she can put her SAHM plans into motion.

- Taking on freelance work for additional income

As someone with a good track record with her colleagues and clients, those who have gotten wind of her departure to be a SAHM have reached out to offer freelance job opportunities. Caitlyn plans to take on gigs that offer her the flexibility to work from home yet still allows her to prioritise her kids’ well-being.

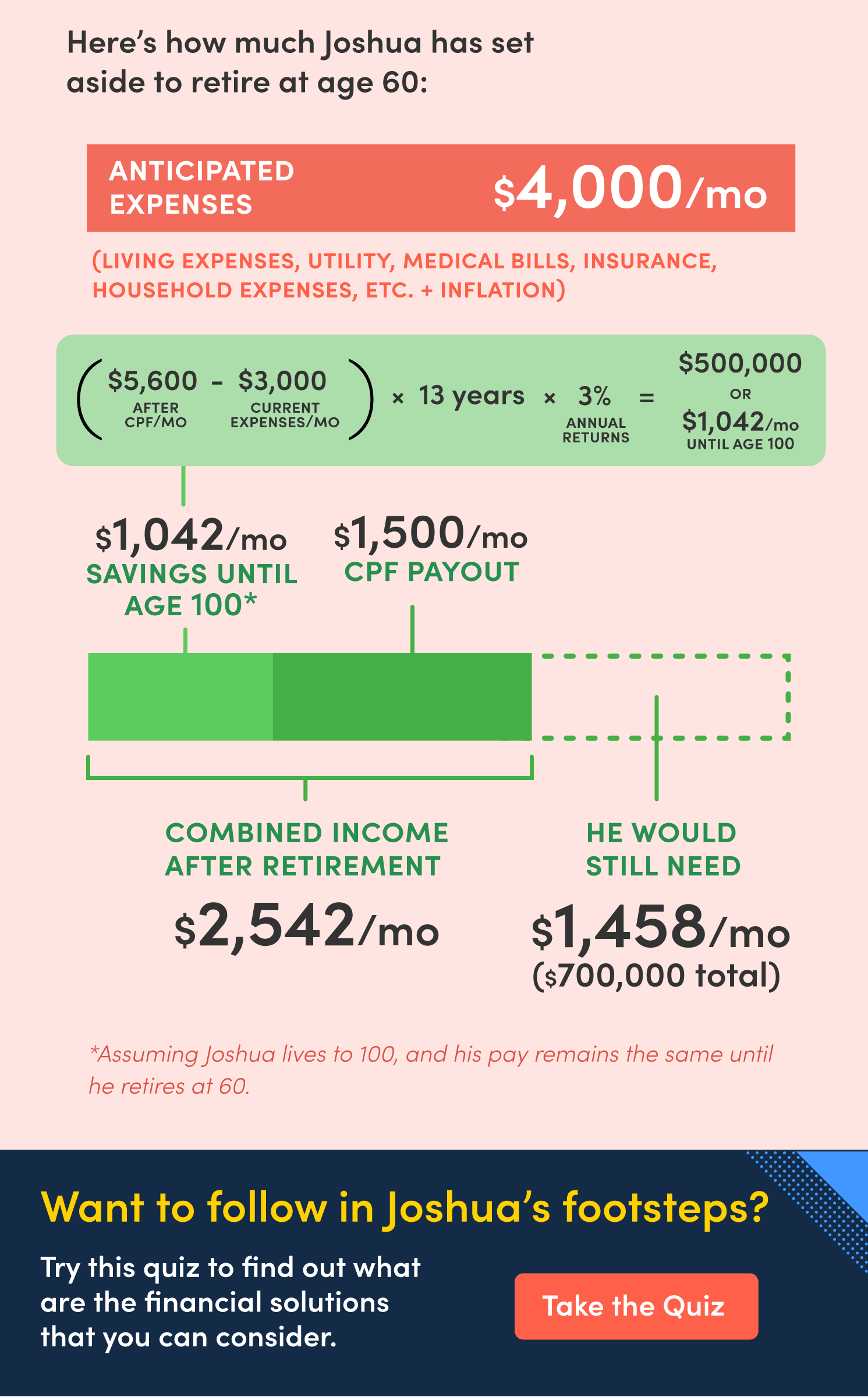

Scenario 3: Being able to gain financial freedom, earlier

Joshua’s boys are still in their late teens, but before long, they’ll graduate from university, settle down and have their own families. As a manager who has been constantly giving his all for the company he works for, the 47-year-old hopes to eventually devote less time to work and focus more on family, his long-ignored hobbies (fishing, cycling, music), travel the world and so on.

He is also currently taking care of his ailing parents, who are in their late 70s. As a filial son, he wants to spend more time taking care of them, accompanying them to doctors’ appointments, and to just be there when they need him.

The key to doing so, he thinks, is FIRE — financial independence, retire early. But while he’s been trying his best to stay disciplined, incidental expenses sometimes eat into his hard-earned savings. It doesn’t help that housing, marriage, raising a family and taking care of aged parents (i.e. sandwiched generation) are expensive.

Joshua is currently earning about $7,000 a month and hopes to retire by 60.

- Investing early and establishing diverse sources of passive income

Some ways Joshua can better prepare for early retirement include:

Joshua has been investing since he was in his 30s, so he has amassed a pretty good nest egg, which is still growing thanks to the power of compounded interest. He also has other investments that provide dividends of about $500 per month, on average.

With the help of financial products such as PRULifetime Income, he not only receives a lifetime of annual cash benefit from as early as his second policy anniversary (he can also accumulate the cash benefits for higher returns) but can transfer this wealth up to 3 generations. PRUActive Retirement, a plan which provides monthly income that never decreases and can potentially increase yearly, would allow him the flexibility to choose his premium payment term and payout age, as well as the payout period (from age 50 up to 110).

- Identifying all protection gaps

As Joshua gets on in years, he knows that he will have more age-related health issues. Thus, he makes sure he has adequate medicaland critical illness protection as a safeguard for his finances, as medical costs can wipe out one’s savings in a flash.

- Using financial products to make his journey easier

Joshua is also looking at insurance savings plans such as PRUActive Saver II as well as PRUWealth II (SGD). The former allows him to customise the maturity date to meet his goal, capital guaranteed; while the latter (better suited for long-term disciplined saving) provides healthy returns in the long run, and allows him the flexibility to withdraw his savings to fund key life milestones or aspirations (vacation, charity, etc). Both products include a death benefit payout.

Time to #BringOn100 ways to live

Beyond these scenarios, everyone’s life is different. Whether you have a plan in mind or prefer to go the spontaneous route, it’s best to be financially prepared for the “what ifs” so that you’ll have the freedom to live your life, however you want, whenever you want.

If you need financial guidance or advice on how to #Bringon100 ways to live, get in touch with a Prudential Financial Consultant today.

Disclaimer: You are recommended to read the product summary and seek advice from a qualified Prudential Financial Consultant for a financial analysis before purchasing a policy suitable to meet your needs.

As buying a life insurance policy is a long-term commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid.

Premiums for some supplementary benefits are not guaranteed and may be adjusted based on future claims experience.

The information on this website is for reference only and is not a contract of insurance. Please refer to the exact terms and conditions, specific details and exclusions applicable to these insurance products in the policy documents that can be obtained from your Prudential Financial Consultant.

The information contained on this website is intended to be valid in Singapore only and shall not be construed as an offer to sell or solicitation to buy or provision of any insurance product outside Singapore.

These policies are protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policies is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact your insurer or visit the GIA/LIA or SDIC web-sites (www.gia.org.sg or www.lia.org.sg or www.sdic.org.sg).

Information is correct as at 2 Dec 2020.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

This post was written in collaboration with Prudential. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence.

Related Articles