The days of T-bills as a high-returns option seem to be behind us (at least for now). After enjoying yields of over 4% in 2023 and staying strong throughout much of 2024, the recent 6-month T-bill auction has seen rates fall to a much lower 1.44%.

This raises a question for anyone who wants to save up for big-ticket goals like a BTO downpayment, children's education, or build a solid emergency fund: Where else can we get better returns?

Let's explore better alternatives out there—whether you're looking for a similar risk-free way to grow your money, or wanting a more active approach in maximising your returns.

The best T-bill alternatives for 2025

- Singapore Saving Bonds (SSBs)

- Fixed deposits

- High-yield savings accounts (HYSAs)

- Other options to invest in

- FAQs

- Final words

Got your eyes on T-Bills? Start like a pro with our other investment guides! |

1. Singapore Saving Bonds (SSBs)

SSBs, similar to T-bills, are a type of government-backed bonds that possess the highest credit rating of AAA. The rating shows our country’s high-level of financial creditworthiness, ensuring you will receive your money with minimal default risk. Apart from Singapore, only 11 countries hold an AAA rating, including Canada and Switzerland.

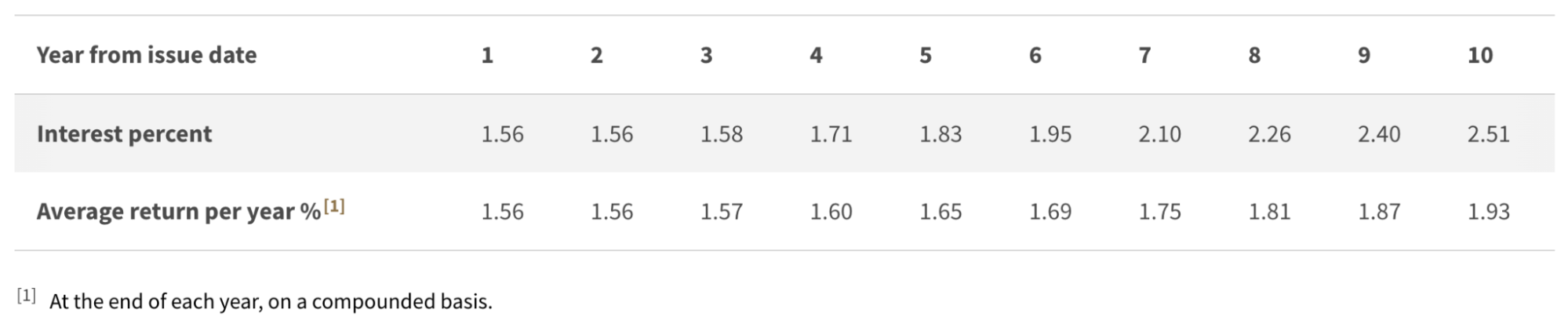

Unlike T-bills, SSBs are designed for the long haul. Instead of a single fixed yield, their interest rates are set to increase every year you hold them, up to 10 years. With the latest SSB (SBOCT25 GX25100S), here’s how much you can earn from a $10,000 investment:

Image: MAS, Singapore Savings Bonds

Are they right for you?

If you're an entry-level investor or withless cash flow, SSBs might be your best bet. There are low barriers to entry, with a minimum investment of just $500, making them the most accessible option out of the three government-issued securities.

Since they can't be traded on the secondary market, they're also less likely to be affected by the ups and downs of the market, giving you a peace of mind. However, keep in mind that there's a limit–you can only hold up to $200,000 worth of SSBs at any one time.

- Example: If you bought $50,000 in an SSB issue in 2022 and another $50,000 in 2023, you can only apply for a maximum of $100,000 in future SSB issues.

2. Fixed deposits

Also known as a time deposit, this account essentially gives you a guaranteed interest rate. The catch is you agree to keep your money there for a set period, like putting it in a temporary lockbox to earn a reward.

One of the best things about fixed deposits is their flexibility. Unlike T-bills, which typically last for 6 months or a year, you can find fixed deposits for as short as one month. Of course, to get a better rate–like the current offers up to 1.60% for an 8-month term–you'll want to choose a slightly longer duration.

For the big comparison: T-bills. Recent auctions in September 2025 saw yields hovering around 1.40% to 1.60%. This means you'll want to compare those rates directly against what your bank is currently offering for fixed deposits to see which one work harder for your money:

- DBS (1.60% p.a.—min. $1,000 for 8 – 60 months)

- Syfe (1.50% p.a.—3 months with no minimum amount)

- ICBC (1.45% p.a.—$500 for 1, 3, or 6 months)

- Bank of China (1.45% p.a.—min. $500 for 1–5 months)

- CIMB (1.40% p.a.—min. $10,000 for 3 or 6 months)

- RHB (1.40% p.a.—min. $20,000 for 3 months)

- Maybank (1.35% p.a.—min. $20,000 for 6 months)

- State Bank of India (1.35% p.a.—min. $200,000 for 6 months)

- UOB (1.35% p.a.—min. $10,000 for 6 months)

- Hong Leong Finance (1.20% p.a.—min. $20,000 for 9 or 12 months)

- OCBC (1.15% p.a.—min. $20,000 for 9 or 12 months)

- Standard Chartered (1.15% p.a.—min. $25,000 for 6 months)

- HSBC (1.00% p.a.—min. $30,000 for 1 month)

If you only want to deposit $10,000 or less, there are several attractive options to consider:

- DBS (1.60% p.a.—min. $1,000 for 8 – 60 months)

- Bank of China (1.45% p.a.—min. $500 for 1–5 months)

- CIMB (1.40% p.a.—min. $10,000 for 3 or 6 months)

- ICBC (1.45% p.a.—$500 for 1, 3, or 6 months)

- UOB (1.35% p.a.—min. $10,000 for 6 months)

Looking to invest $50,000 or more? Explore options and find the best rates in our guide to the best fixed deposit rates in Singapore.

Are they right for you?

If you're keen on investments with shorter maturities, fixed deposits are right up your alley. But do note that unlike T-bills, fixed deposits usually come with a 0.5% to 1% penalty for early withdrawal. This typically means you'll either forfeit all the interest you've earned or be charged an administrative fee.

Note: Banks like DBS and POSB will not allow you to withdraw on the day of maturity or 1 day before. You must give at least one business day's notice if you have specific maturity instructions. Meanwhile, ICBC has been known to offer more flexible terms, sometimes allowing for withdrawalswithout extra fees–but this can depend on the specific product you chose.

It's always a good idea to check your preferred bank's specific terms and conditions before applying.

3. High-yield savings accounts (HYSAs)

In contrast to fixed deposits, T-bills and SSBs, high-yield savings accounts may offer lower interest rates initially. However, you can earn much more by meeting criteria issued by your banks (e.g. crediting your monthly salary of at least $1,800, increasing your monthly balance by $500, or spending on related credit cards..).

At the moment, some of HYSA offerings are yielding higher interest than the fixed deposits, including:

- Standard Chartered Bonus Saver — up to 8.05% p.a.

- OCBC 360 Account — 7.65% p.a.

- Citi Wealth First Account —up to 7.51% p.a.

Here's an in-depth look of how interest rates fare should you meet several banks’ criteria:

Bank | Interest rate (p.a.) | Amount valid for | Key criteria |

Standard Chartered Bonus$Saver | Up to 8.05% p.a. | First $100,000 | Fulfill 4 criteria (Credit salary, spend, insure, invest) |

UOB One | Up to 4.50% p.a. | First $150,000 | Fulfill 2 criteria (Spend, credit salary OR make GIRO transaction) |

UOB Stash | Up to 3% p.a. | First $100,000 | Maintain or increase your Monthly Average Balance (MAB), as compared to the previous month |

OCBC 360 | Up to 7.65% p.a. | First $100,000 | Fulfill 5 criteria (Credit, salary, save, spend, insure, invest) |

Citi Wealth First Account | Up to 7.51% p.a. | First $50,000 (Citibanking & City Priority); First $250,000 (CityGold) | Fulfill 5 criteria (Insure, spend, credit, salary, pay, save) |

Bank of China Smart Saver | Up to 5.35% p.a. | First $100,000 | Fulfill 5 criteria (Insure, spend, credit, salary, pay, save) |

DBS Multiplier | Up to 4.10% p.a | First $50,000 (1 category); First $100,000 (2 & 3 categories) | Fulfill 4 criteria (Salary, spend, loan, insure, invest) |

Compare savings accounts easily on MoneySmart.

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 5.45%

- Min. Balance

- S$3,000

- Base Interest Rate

- 0.05% p.a.

- Max. Interest Rate

- Up to 5.85% p.a.

- Min. Balance

- S$3,000

Are they right for you?

Even though they're quite attractive, remember that these highest rates are only available should you meet all of the bank's criteria. If that's not possible, here's a more realistic look at what to expect from your investment:

Savings account type | Interest rate (Credit salary and spend only) | Amount valid for | Valid for |

Standard Chartered Bonus$Saver | Up to 3.05% p.a. | First $100,000 | Credit monthly salary of $3,000 or more AND monthly card spend of $1,000 or greater |

UOB One | Up to 4.5% p.a. | First $125,000 | Min. $500 card spend AND monthly salary credit via GIRO of $1,600 or more |

UOB Stash | Up to 3% p.a. | First $100,000 | Maintaining or increasing your monthly average balance |

OCBC 360 | Up to 2.8% p.a. | First $100,000 | Credit monthly salary of $18,00 AND increase average daily balance by at least $500 monthly AND spend at least $500 with credit card |

Citi Wealth First Account | Up to 3% p.a. | First $50,000 | Min. $250 card spend AND increase account’s average daily balance by $3,000 monthly |

Bank of China Smart Saver | Up to 1.6% p.a. | First $100,000 | Monthly salary of $2,000 (0.8% p.a.) AND min. $750 card spend (0.6% p.a.) |

DBS Multiplier | Up to 3% p.a. | First $50,000 | Credit income with no min. requirement AND spend at least $500 with PayLah/Credit Card |

Source: StashAway

While they might not boast the rates of 7% you might see advertised, a lot of HYSAs still offer much better returns than your basic savings account. In fact, their rates are much more competitive with what you're seeing for fixed deposits, and especially T-bills right now.

Do remember that these accounts often come with conditions & terms. You might need to make a fresh deposit or two, and some might even limit how many times you can withdraw money. Not only that, to avoid additional fees, you'll also need to maintain a minimum balance in your accounts.

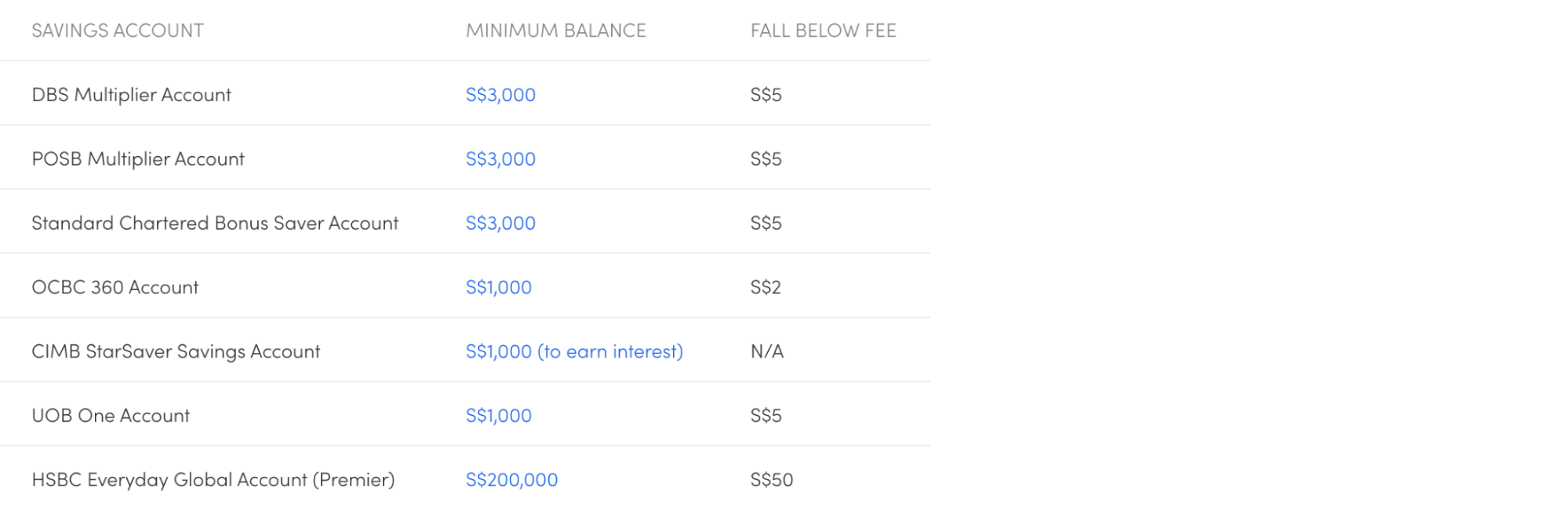

Here's a quick rundown of what to look out for with several major banks:

Image: MoneySmart

It's worth taking a close look at the fine print to figure out which account's rules you can stick to for higher returns.

4. Other options to invest in

Beyond the traditional banks, you've got several alternative options like digital banks or cash management solutions to park your cash.

DigiBanks

Take digital banks (i.e. Trust+), for example. They operate entirely through an app, so you can forget about queuing up at a branch. Without the costs of physical branches, they pass the savings on to you. Instead of waiting for a banker, you can do all your transactions right from your phone.

With a Trust+ savings account, the interest rate of up to 3.0% p.a, is on your first $500,000 deposit balance—a cap higher than what is offered by most local banks. You can earn up to$15,000 total interest in a year.

Are they right for you?

As opposed to fixed deposits, T-bills, or SSBs, that lock your money in for a set period and incur fees for early withdrawals, Trust+ accounts provide full freedom in liquidity. You can withdraw whenever you need without fear of being penalised.

Secondly, Trust+ requires no minimum balance, monthly, or fall-below fees that traditional banks typically charge.

Alt cash management solutions

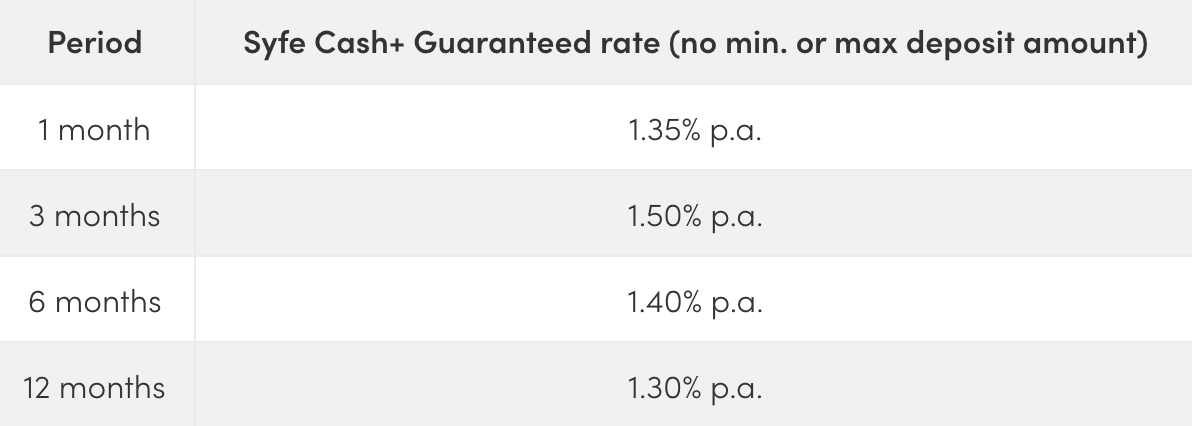

Then you have cash management e-solutions like Syfe Cash+ Guaranteed, which offers a straightforward, no-fuss way to earn guaranteed returns. Unlike most HYSAs that give you projected rates with multiple conditions, this product provides a specific, locked-in rate by placing your funds into fixed deposits with MAS-regulated banks. Plus, there are no minimums—so you can start with any amount.

Are they right for you?

Overall, what solutions like Syfe Cash+ Guaranteed really does is solve the common headaches of fixed deposits—having to find the best rates yourself and dealing with all those high minimums. Syfe uses its size as a large company to get better rates for you than you'd likely get on your own.

If you have a lump sum you know you won't need for a few months and want a guaranteed return with no fees and no minimums, it's a choice worth considering. As of today, here's a look at the rates they offer:

Source: MoneySmart

5. FAQs

Can I use CPF to purchase T-bills or any of these investments?

Yes, you can for T-bills and fixed deposits:

CPF for T-bills

You can apply for T-bills at your CPF Investment Scheme (CPFIS) agent bank (DBS/POSB, OCBC, UOB) or online if you’re a DBS, OCBC, or UOB customer. Banks will charge a one-time $2.50 fee (excluding GST) per transaction and a quarterly $2 service fee (excluding GST) per counter. Using your CPF Ordinary Account (OA) will cost S$7.09 after GST.

Only CPF-OA can be used to purchase T-Bill, with several limitations, which is understandable considering CPF is meant for your retirement:

- The total investment in T-bills and non-guaranteed investments cannot exceed 35% of your investible savings.

- The total amount of your investment in T-bills, including other non-guaranteed investments and gold, cannot exceed 10% of your investible savings.

- An update–You can now use your CPF-OA to invest in both 6-month and 1-year T-bills

CPF for Fixed Deposits

Meanwhile, you can still use CPF to purchase fixed deposits with any of the 4 major banks (DBS, Maybank, OCBC and UOB) under the CPFIS. If you are unsure whether your banks are offering CPFIS-supplemented fixed deposits, you can reach out to them and ask about the fixed deposits’ rates and placement processes.

Note: Even if the fixed deposit bank you visit is not your usual CPFIS-OA agent bank, you can still place your fixed deposit there. Meanwhile, the transfer of funds from your CPF-OA for the fixed deposit must still be done via your designated CPFIS agent bank.

How to apply for & redeem SSBs

Application for SSBs

SSBs are open to apply for anyone from age 18 and above, although you must:

- Have a bank account with at least one the major banks in Singapore & an individual CDP Securities account.

- Apply through DBS/POSB, OCBC & UOB ATMs or internet banking. SRS investors may apply through their respective SRS Operator's internet banking portal

- For cash-based investments, the interest will automatically go into the bank account linked to your individual CDP Securities account.

SSBs (selling) redemption requirements

For early redemptions, submit your request through DBS, OCBC or UOB ATMs or iBanking. You can redeem the bond partially, in multiples of $500 and redeem more than one bond each time.

The redeemed amount will then arrive by thesecond business day of the month after SBB withdrawal. You don’t have to worry about penalties for leaving early, though there will be a $2 transaction fee awaiting you. Here’s an overview of what will happen:

When you redeem SSB | What to do | What you’ll receive |

Early redemption (when there’s a scheduled interest payment) | Submit redemption request + pay $2 transaction fee | Principal amount + full interest |

Early redemption (in between scheduled interest payments) | Submit redemption request + pay $2 transaction fee | Principal amount + pro-rated interest |

Full term (after 10 years) | Nothing. No need to pay $2 transaction fee | Principal amount + final interest payment |

Source: MoneySmart

6. Final words

With a variety of options available, it's good to reconsider where you're putting your money in. Whether you're a first-time investor or just looking to diversify beyond T-bills, the key is finding a strategy that works for you.

There's no "best" option. It all boils down to understanding your risk tolerance and what you want to achieve. Take some time to do your homework—look at the pros and cons, and decide which is the best fit for your investments in 2025.

Found this article useful? Share it with your friends!

Related Articles