This post was written in collaboration with Syfe. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

Most Singaporeans wouldn’t even dream of uttering the words “financial independence” in the same breath as “being a parent”.

In our competitive society, we’re conditioned to believe that raising a child equals spending boatloads of money on his education, entertainment, food, clothing, electronic gadgets, and so on, to give him a head start in life.

Perhaps that’s why Singaporean parents spend more on their kids than their retirement. According to a survey of 1,000 families here, most parents set aside a paltry $250 to $500 a month in cash for their retirement. This sum pales in comparison to the amount spent on their kids each month, which is estimated to be at least 2.5 times more!

But yes, it’s still possible to achieve a goal like attaining FIRE by age 50, while still raising a family! Read on to find out more.

What is FIRE?

Let’s back up for a minute here and talk about what FIRE even means. FIRE stands for “Financial Independence, Retire Early”, and it’s a movement that’s captured the imagination of people around the world who wish to exit the rat race before they get too old to enjoy life.

Ahhh, sounds wonderful already! It’s easy to see why this is such a popular concept. Who wouldn’t want to work less (or quit entirely), spend more time with family, and pursue our passions?

But achieving FIRE isn’t that easy. It requires you to build up your wealth such that it generates enough passive income for you to live off. Only then can you safely quit or work less.

This dream is close to impossible if you only put a mere $250 a month towards retirement, like other Singaporean parents (it costs up to $560,000 to raise a child in Singapore!). However, the more willing you are to come up with a good strategy — and stick to your plan — then the easier it will be to achieve FIRE as a parent.

Here are some thought starters to kick off your plan.

Determine which stage of the financial life cycle you are at

Financial independence isn’t binary; it’s a spectrum. So, first, take a good look at yourself to figure out where you are in the financial life cycle.

- Financial Dependence: As a child, you have no income and depend on your parents for money.

- Financial Solvency: You’ve started working, but don’t earn much, so you live from paycheck to paycheck.

- Financial Stability: Your income is growing, you’ve saved up some money for a rainy day, and are beginning to insure and invest. You’re financially stable enough to purchase a home and pay your mortgage.

- Financial Security: You’ve cleared most of your debt, including your home loan. You’re now investing and starting to earn passive income.

- Financial Freedom: Hooray, you now earn enough passive income to cover your expenses! Now you can opt to work less or quit if you choose.

- Financial Independence: Your passive income has grown to cover both your needs and your wants. You’re now safely in the FIRE zone.

- Financial Abundance: You have so much wealth that you can’t possibly spend it all in your lifetime. Well, one can dream…

For example, I’m currently at Stage 4, having cleared my mortgage and built up a modest investment portfolio. While my passive income isn’t enough to live on, being in this stage allows me to take a career risk by going freelance. I know that I may be in this stage for a while, but I will work towards Stage 5 gradually.

My parent friends are mostly around Stage 3 or 4. They’ve saved enough money to tide them through a rough patch, own a home and have found financial balance. Some of them are paying off the last few dollars of their debts, and are generating passive income to prepare for their retirement years.

Regardless of where you are, you should gradually work towards the next stage in the life cycle. The keyword here is “work towards” — you don’t want to stagnate in one stage forever.

Relook your financial habits

It’s time to get serious, so if you don’t have a handle on your finances, you’ll want to do an audit of where all your money is. Total up the following:

- Incoming cash flow: Salary, bonuses, passive income, rental income, any side hustles

- Outgoing expenses: Mortgage, bills, family expenses, personal expenses, etc.

- Assets: Cash savings, investments, property value, CPF savings

Now you can start optimising. First, make sure that you’re setting aside enough for important funds like your emergency (at least 6 months’ expenses) and any long-term goals (like your kid’s university tuition fund). In addition, do budget for short-term goals (a holiday, ang bao money, birthday presents and so on).

Then pare down your day-to-day expenses — food, groceries, kid stuff, fun, transport, bills and so on. What can you trim? What switches can you make to save money? For example, you can save by prepping meals at home (it’s healthier too!) and taking public transport instead of driving (which is also better for the environment).

Related article: The 5 Things You Should Start Doing Now That Can Change Your Finances Forever (In A Good Way)

Gradually, you’ll build better financial habits and reduce your overall expenses. Not only does this allow you to attain FIRE earlier, it’ll also free up more funds to invest in your retirement.

Finding your FIRE numberHere’s how you might calculate your FIRE number, AKA how much money you need to invest so you can live off your passive income and attain true financial freedom. The formula is derived from a study by Trinity University that found a 100% probability that a person with an investment portfolio of at least half in stocks could safely withdraw 3% of their investments for 40 years without depleting them. Annual Expenses divided by 0.03 = FIRE number So, if your annual expenses are $42,000/year ($3,500 expenses a month — includes bills, insurance, child-rearing and personal enjoyment), you will need $1.4 million to achieve FIRE. It’s quite simple really. Lower annual expenses = lower FIRE number. |

Set targets & automate your investments

Instead of going all laissez-faire and investing “whatever and whenever you feel like it”, it’s key to have a plan in place to attain your financial goals, such as achieving FIRE by age 50.

So the next step is to get an investment plan in place. Luckily, you don’t need to read investing books or pay a professional to manage your money these days. Thanks to digital wealth managers like Syfe, planning your investment strategy is as simple as ABC (or rather, 1-2-3).

All you need to do is input your...

- Target savings goal: In this case, how much wealth would generate the passive income you need for an early retirement (in our example above, the FIRE number is $1.4 million)

- Time horizon: How much time you have to attain your goal. For example, if you’re 35 and intend to FIRE by 50, your time horizon is 15 years

- Risk appetite: How much risk you can tolerate. Remember that risk correlates with returns. Also, the longer the time horizon, the more risk you can afford to take on

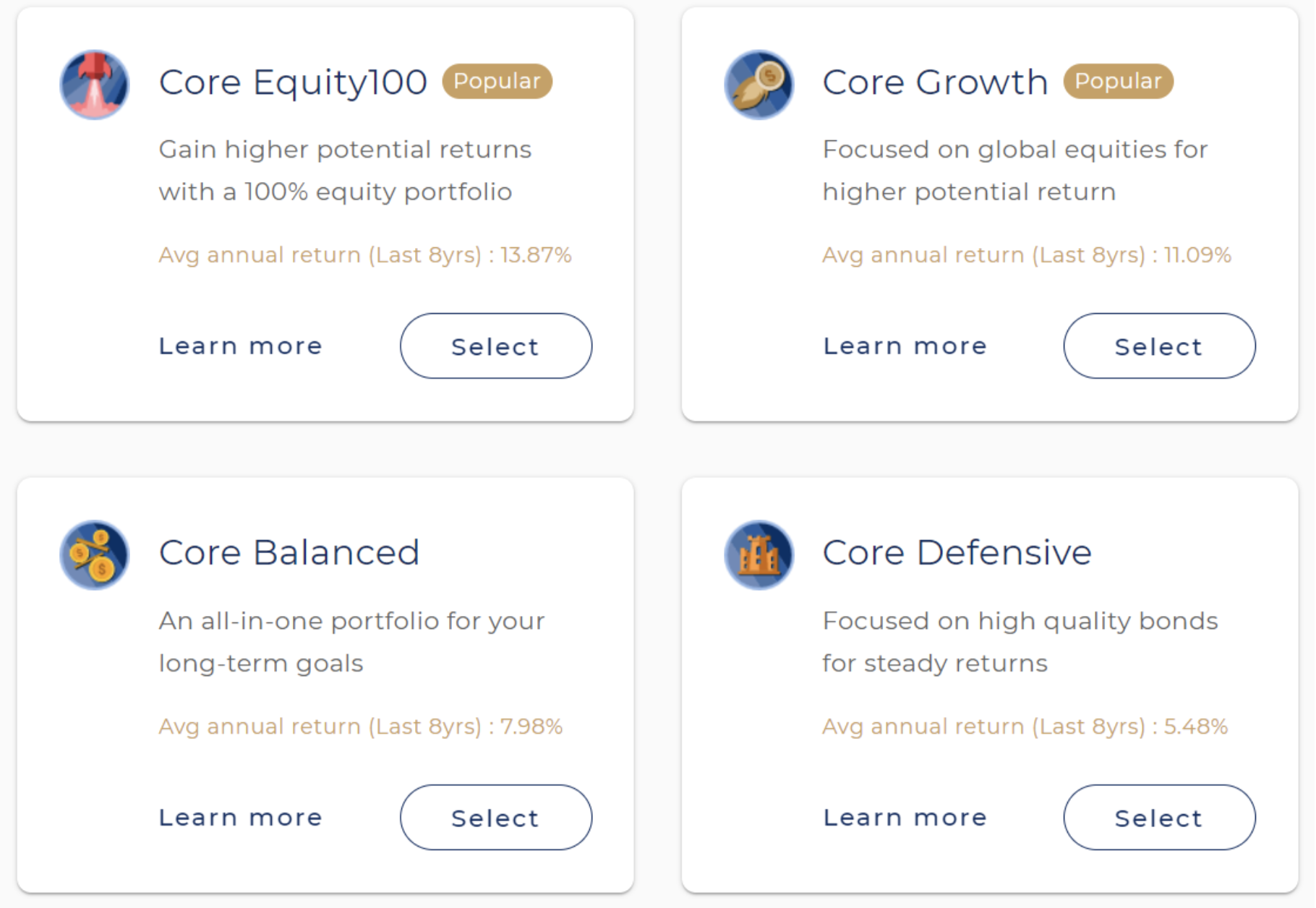

…and Syfe will recommend a Core diversified portfolio of investment assets for you. All Core portfolios are designed for long-term investing and hold investments in the world’s top companies like Apple, Microsoft, Tesla, Facebook and more. In addition to your Syfe Core portfolio, you can add on thematic Satellite portfolios for specific areas of interest, such as Singapore REITs or ESG.

While setting up your Syfe Investment Plan, we strongly recommend that you automate your investments by opting for monthly recurring deposits in addition to your initial lump sum.

This allows you to easily set aside the money earmarked for FIRE before you can spend it — sort of like CPF. Trust us, this takes away the stress of having to watch your spending for the month to make sure you have enough left over to invest. Of course, do make sure you’ve allocated enough for your regular expenses and already have an emergency fund to tap on.

But the question is, how would you put all this into practice? Let’s look at some scenarios, based on actual parents, to see what their plans and portfolios look like for them to achieve FIRE by 50:

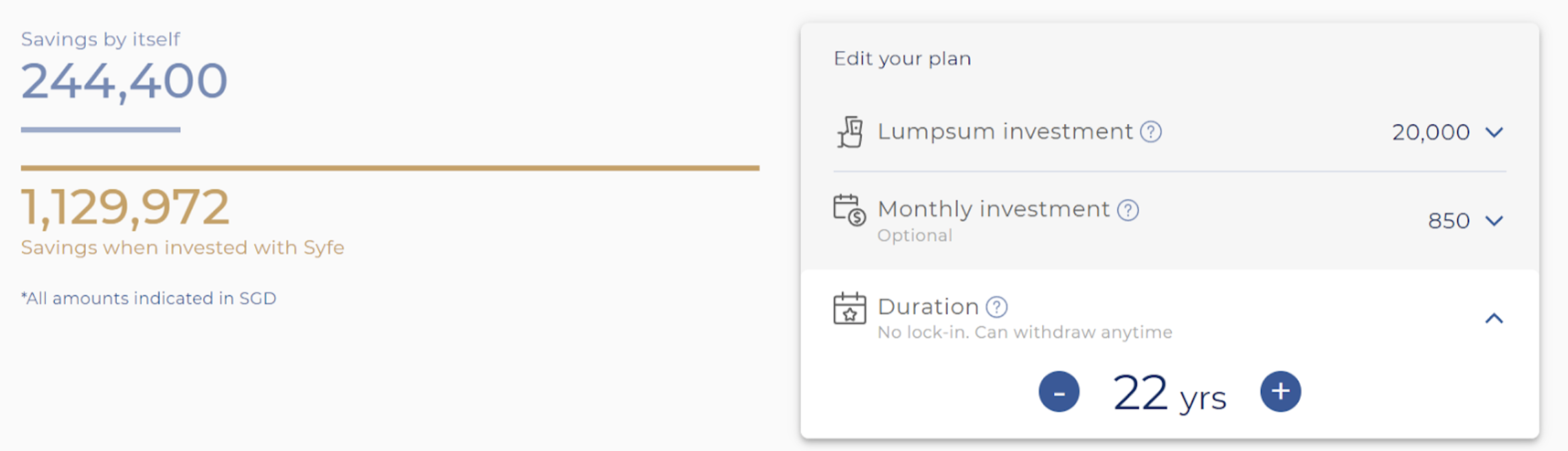

Scenario 1: Abby, working mum, 30

FIRE number: $1,100,000

Abby’s personal monthly expenses are $2,500 and she wants to set aside $100,000 for her child’s university expenses. Thus, her total FIRE number is $1,000,000 + $100,000 = $1,100,000.

Setting aside $850 a month on her own would be impossible to achieve this. But thanks to the power of compounded interest and wealth management platforms such as Syfe, Abby could achieve her FIRE number in 22 years with the following plan.

Abby’s investment with Syfe Core Growth; for illustration purposes only.

For Abby, FIRE may sound like a distant dream, but with the right planning, relooking her financial habits and setting more achievable targets, she can accumulate a forecasted amount of $1,129,972 by age 52.

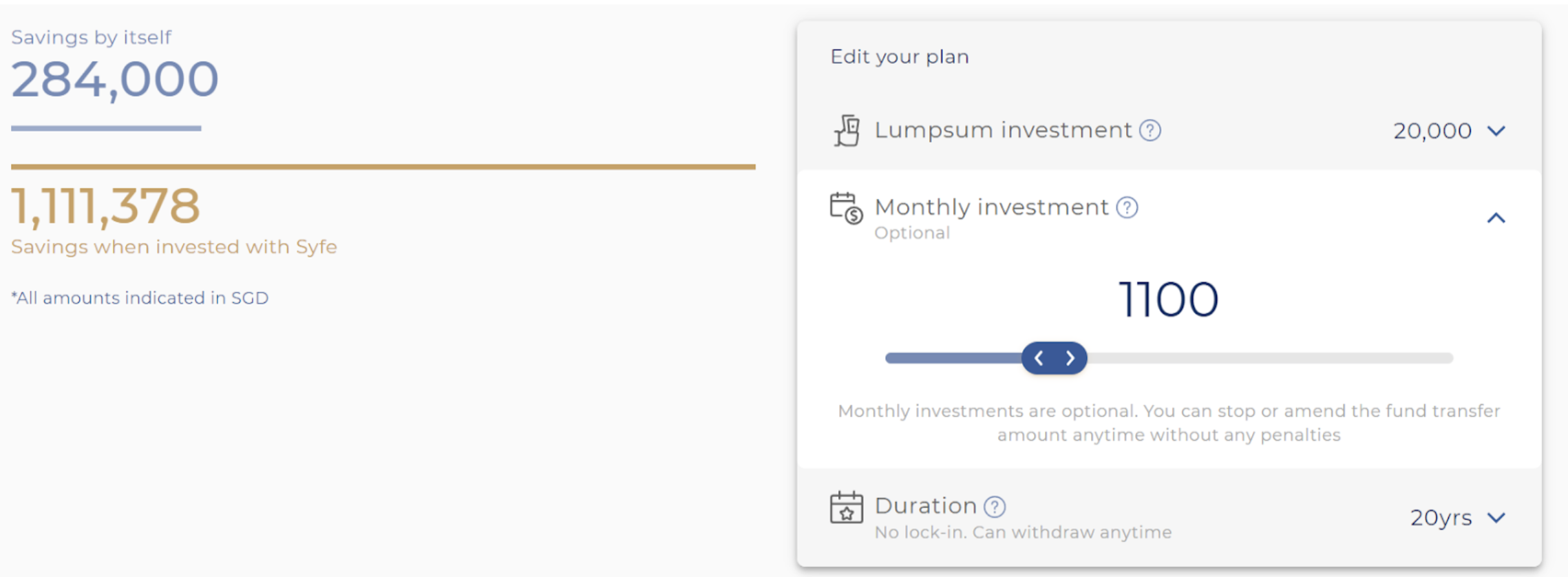

If FIRE by 50 is something she really wants to strive for, increasing her monthly investment amount to $1,100 could help her get there.

For illustration purposes only. Create your own forecast using Syfe’s projection here

Abby chooses Syfe Core Growth as the high exposure to equity ETFs provides greater return potential while her bond and gold ETFs cushion against volatility.

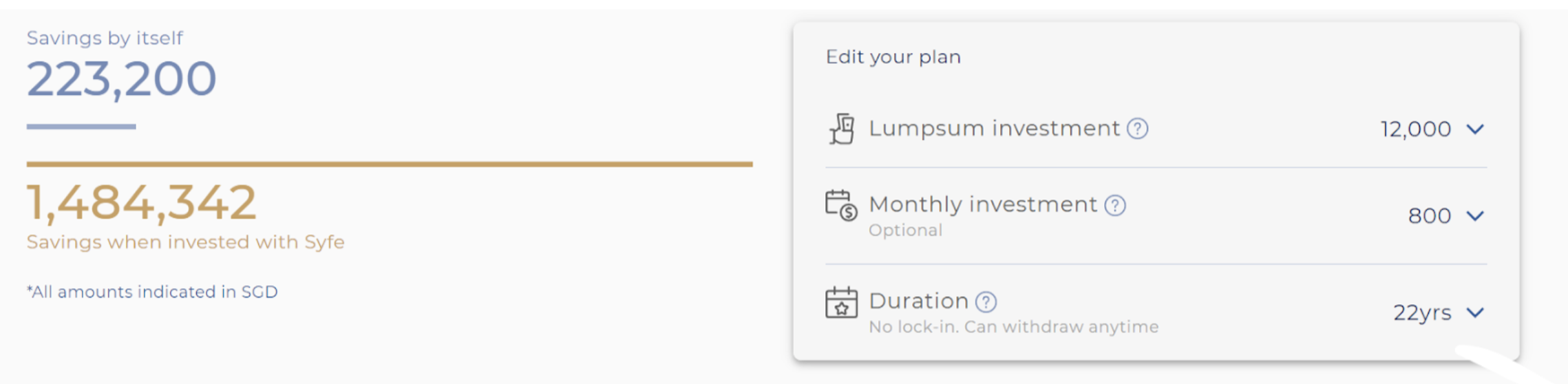

Scenario 2: Brandon, 28, working dad

FIRE number: $1.5 million

Brandon aims to send his child to an overseas university (about $450,000) and he also wants to accumulate $1 million by age 50. Thus, he targets a FIRE number of about $1.5 million to achieve both financial goals concurrently.

With the help of Syfe Core Equity100...

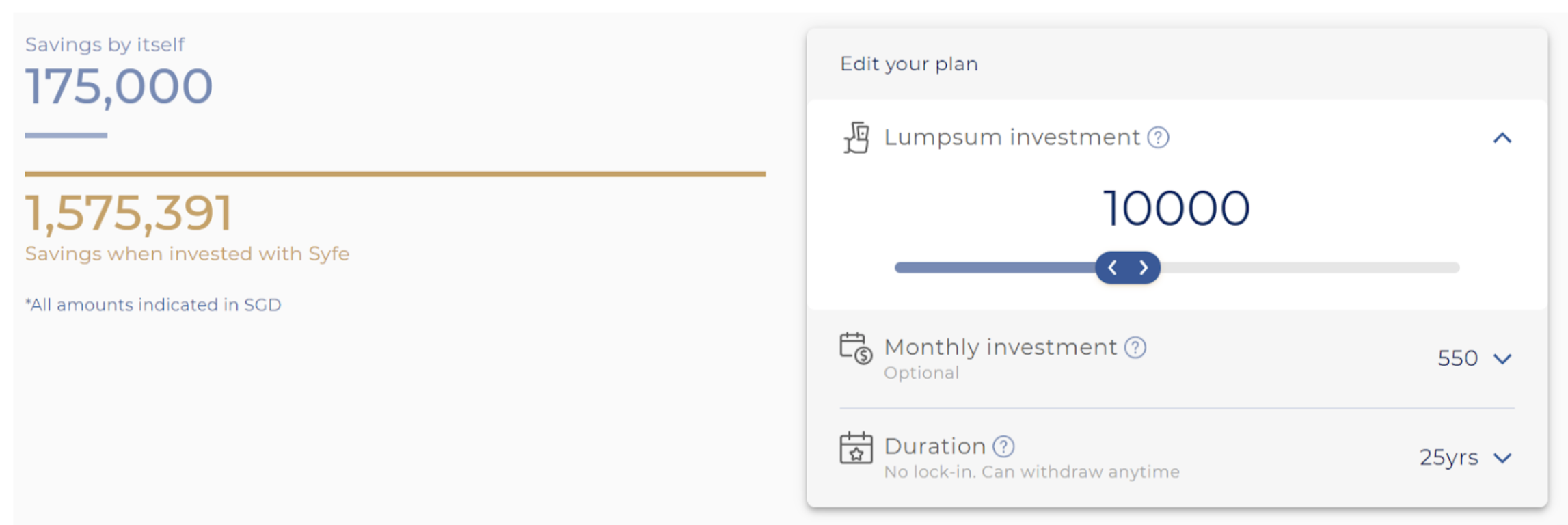

Brandon’s investment with Syfe Core Equity100; for illustration purposes only.

Brandon invests in Syfe Core Equity100 as the 100% exposure to equities allows him to maximise his long-term potential returns. As he has time on his side (and a hearty risk appetite to boot), he’s comfortable taking on a higher level of risk. However, not forgetting his commitments and child, he sets aside other cash in his bank account for emergencies (6 months of expenses) and ensures he has robust protection plans in place.

As his kid is still a wee tot, he can still afford to cut himself some slack and extend his time horizon to 25 years. This will make his monthly investment lower. With a lumpsum investment of $10,000 and monthly investments of $550, he’ll still be able to grow his Syfe Core Equity100 portfolio to $1,575,391.

For illustration purposes only. Create your own forecast using Syfe’s projection here

Live your life and let time do its thing

Give yourself a pat on the back for making it this far. You’ve conducted a financial audit, worked hard to reduce your expenses and maybe even increase your income, and you’ve set up your investment plan.

Now all that’s left is to sit back and let time do its thing. With your regular contributions and the magic of compounding, your goal should materialise without requiring consistent hard work. You don’t even need to actively manage your portfolio — Syfe will help you reinvest your dividends (for free) and take care of any portfolio rebalancing that needs to be done.

While that sounds easy enough, Syfe doesn’t lock in our funds, so it’s mighty easy to be tempted to withdraw all of your hard-earned investments on a whim. STOP. The key to achieving FIRE is to remain consistent and dedicated.

From the very beginning of your FIRE journey, you need to determine if FIRE by 50 is a goal you want to hit — no matter what. Well, even if it isn’t, just getting started thinking about the possibility of FIRE by 50 is a helpful motivator for you to save and invest for your future, while thinking more holistically about your financial plan.

Note: Many factors like your current salary and savings rate, how the market performs, how much you need to live on each year in early retirement, your withdrawal rate, the size of your family, your goals, unexpected expenses etc can influence your FIRE number and decision to FIRE by a certain age.

Keep calm and Syfe on

Rest easy when investing with Syfe for the long term, as it is fully regulated by the Monetary Authority of Singapore. All of your wealth is held in a custodian bank account managed by DBS, while all investment holdings are held with Danish investment brokerage Saxo.

With no minimum funding and no lock-ins, it’s simple enough to try out the Syfe platform to get familiar with its offerings.

Take the first step towards achieving FIRE by age 50, all while raising a family.

Signing up for a Syfe account through MoneySmart is quick and easy and can be done with SingPass. Still thinking about it? Learn about different financial profiles and find the one that resonates best with you.