This post was written in collaboration with Great Eastern. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best information in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

Cancer, heart attack and stroke are the “Terrible Three”: That is, they’re the 3 leading critical illnesses that account for more than 90% of critical illness diagnoses. To put things into perspective, the risk of developing either in one’s lifetime are as such: 1 in 4 Singaporeans are at risk of developing cancer; 31 people are diagnosed daily with heart attack; and 26 people diagnosed daily with stroke in Singapore.

That said, survival rates for these conditions are also quite good if detected and treated early, boosted by the fact that more people these days are going for regular health screenings. According to the Health Promotion Board Singapore Cancer Registry Annual Report 2018, the 5-year survival rate for cancer in 2014 to 2018 was 61.1% for females and 52.1% for males.

One way to ensure that you seek timely treatment and have the financial means to pay for it and the time to recover is to ensure you have a good critical illness insurance policy.

But don’t wait until your health fails to buy insurance. It’s key to get insurance before you fall ill, as once you’re diagnosed with a critical illness, it is almost impossible to be accepted for a new insurance policy, whether it offers life or critical illness coverage. A critical illness (CI) plan can safeguard you from the “what ifs” and it is a bonus if the plan provides continued coverage even after the first claim (many insurance policies terminate and stop any payouts or coverage upon this event).

Look for a CI plan that’ll cover you in times of need, by providing a lump sum payout where you can choose how you wish to spend it. Be it for treatments or other expenses including transportation to and fro.

It’s key to get critical illness coverage ASAP, as those diagnosed with their first CI have to go through the additional steps of re-insuring and underwriting (if eligible) when applying for a new insurance plan.

Looking at statistics, it is important to get critical illness coverage for the top three critical illnesses.

According to an annual report published by the Singapore Cancer Registry, which presented trends from 1968 to 2019, those under 39 years old historically make up less than 10 per cent of all cancer diagnoses per year.

However, one concern is that the number of cancer cases in adolescents and young adults (16 to 45 years old) is on the rise.NCCS said it sees between 450 and 550 new adolescent and young adult cancer cases each year; but between 2016 and 2021, NCCS saw more than 6,000 new and existing patients in that age range — or about 1,000 annually. Various reasons for the uptick could be due to better and earlier diagnostic rates, higher exposure to harmful toxins such as alcohol and smoking.

Great Eastern’s GREAT Critical Cover pays up to 3X

Great Eastern’s GREAT Critical Cover: Top 3 CIs is a critical illness plan that covers the “higher risk” top 3 critical illnesses — cancer, heart attack and stroke — as its name suggests.

The plan, when supplemented with the Protect Me Again rider, offers continued coverage when you need it most — even after a critical illness diagnosis when it becomes harder to be accepted for another insurance plan. You get 100% payouts at all stages: early, intermediate and critical for cancer, heart attack or stroke for up to three CI episodes.

Best of all, these benefits come at an affordable price, with premiums starting from as low as $0.80 a day (for a 30-year-old male with a 30% first-year discount). Signing up is easy — you can do it online within 10 minutes.

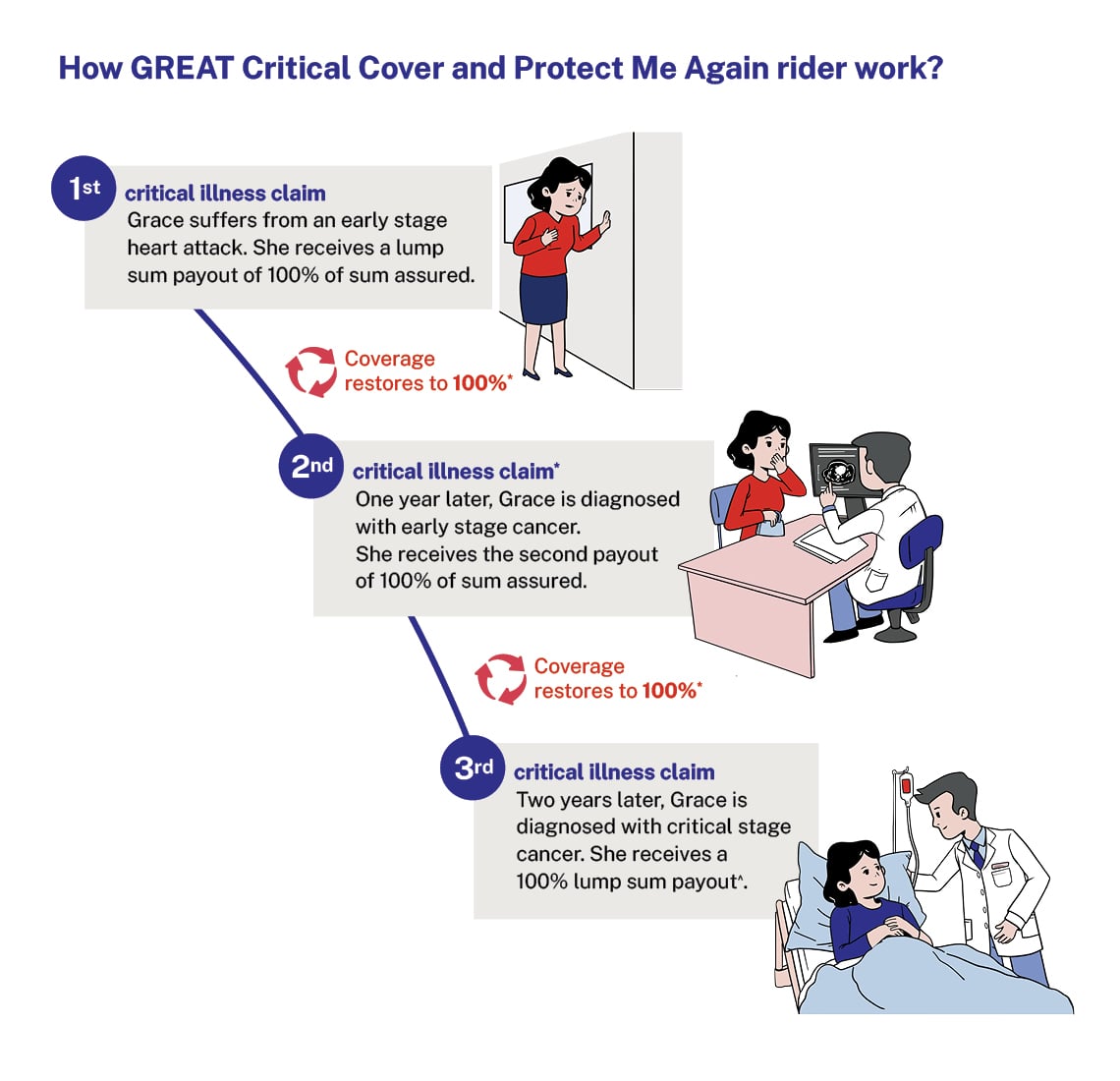

Let’s see how the plan could play out in real life.

1. Here’s a closer look at this new plan

Now that screening technology is more advanced and people are more aware of the need to go for regular screening, there’s a much higher chance of getting an early cancer diagnosis. That in itself is also a blessing in disguise as the person diagnosed can seek treatment early when survival rates are higher. Likewise, it’s also possible to suffer an early stroke but survive at a young age.

GREAT Critical Cover: Top 3 CIs offers coverage for cancer, heart attack and stroke at the early, intermediate and critical stages. So you don’t have to worry that you won’t qualify for coverage due to the stage of disease it is at.

As you get older, the risk of critical illnesses happening rises, and the possibility of developing conditions like heart attack or serious stroke are higher. There is also the chance of recurrence if you survive. According to research published in BMC Neurology, among stroke patients, 59.3% survived for 5 years; and 18.4% were re-hospitalised due to a recurrence within 5 years.

In such situations, you can rest assured that GREAT Critical Cover: Top 3 CIs with the Protect Me Again rider will offer you continued coverage for the second and even third CI occurrence, even after the first critical illness diagnosis.

2. 100% payout of up to 3x claims for any stage (early, intermediate or critical) of these critical illnesses

GREAT Critical Cover: Top 3 CIs when added with the Protect Me Again rider, gives you a 100% payout each time you make a claim. So, if you are diagnosed with a first critical illness, you get 100% payout of your sum assured. Subsequently, if you receive a second and third recurring or new CI diagnosis , you once again get 100% payout of your sum assured*.

There are also some critical illness plans that appear to let you make multiple claims but are actually just accelerating your payouts against your total sum assured. So, you might only receive a small portion of your sum assured for an early cancer claim, rather than the full 100%.

3. Flexible use of lump sum cash payouts

Hospitalisation insurance such as Integrated Shield plans (IPs) are beneficial but it only pays for most of your hospital bills and some hospitalisation charges. The funds will be paid directly to the hospital or reimbursed to your account if you have already paid the bill yourself. While Integrated shield plans cover a large part of medical expenses, there are certain cancer drugs not covered by Integrated shield plans. These drugs can be costly and would require the patient to bear the full cost of it.

Thus, hospitalisation insurance alone may not be sufficient if you are diagnosed with a critical illness; in addition, your recovery may take longer and you may need to take a break from work. The question is, can you afford to take time off work and who will bear the responsibility of your daily expenses and recovery cost?

This is where GREAT Critical Cover: Top 3 CIs plan helps you cope better by offering a lump sum payout that can be used to support yourself during recovery without the need to dip into your savings. This means you can be financially supported to focus wholly on resting and regaining full health.

Being a standalone plan, GREAT Critical Cover: Top 3 CIs doesn’t take the payouts from your existing life/term life insurance plan. As a critical illness insurance plan, it provides coverage against the top three critical illnesses, making a 100% payout upon diagnosis of a covered illness.

4. Covering your varying needs

GREAT Critical Cover: Top 3 CIs can provide additional coverage for anyone with an existing whole life or critical illness insurance plan who would like to boost their protection against the top three critical illnesses. This may work for you if you have started on a basic CI coverage in earlier years and prefer to get a larger sum assured just focused on the major CI killers in Singapore.

Younger people with less disposable income can also benefit from the plan. Due to their young age and their budget commitment, it might be better off for them to start off with a critical illness starter plan for the top three critical illnesses instead of having zero critical illness coverage.

5. There’s even a compassionate benefit portion

In the unfortunate event of death, your loved ones will receive a lump sum payout of S$25,000 for all causes of death.

Enjoy continued coverage against top 3 CIs and get 10% perpetual discount off your premiums!

Get a quote online or speak to a Great Eastern Financial Representative today!

Note: Depending on your medical history, you may need a medical checkup for GREAT Critical Cover: Top 3 CIs.

1 Annual premiums of S$278.30 for the first year after the 30% first-year discount, is based on a male, 30 years old (age next birthday). The daily rate is based on a 30-year-old, non-smoker with the annual premium of GREAT Critical Cover: Top 3 CIs and Protect Me Again rider for a sum assured of S$100,000, divided by 365 days and rounded off to the nearest 1 decimal place. The annual premium will increase based on the attained age of the life assured, as at each policy anniversary.

* Coverage restores to 100% after 12 months from the date of diagnosis for the most recently diagnosed critical illness, for a subsequent claim of a different critical illness. Coverage restores to 100% after 24 months from the date of diagnosis of the immediately preceding applicable critical illness for recurrent critical illness. Please refer to the Product Summary for more details on the benefit term terms and conditions.

^ We will pay the higher of 100% Basic Sum Assured or the Total Premium Paid less all prior CI claims paid.

The information presented is for general information only and does not have regard to the specific investment objectives, financial situation or particular needs of any particular person.

Age stipulated refers to age next birthday (ANB).

As this product has no savings or investment feature, there is no cash value if the policy ends or is terminated prematurely.

You may wish to seek advice from a financial adviser before making a commitment to purchase this product. If you choose not to seek advice from a financial adviser, you should consider whether this product is suitable for you.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The above is for general information only. It is not a contract of insurance. The precise terms and conditions of this insurance plan are specified in the policy contract.

Protected up to specified limits by SDIC.

Information correct as at 26 September 2022.

Disclosure: This article is written in collaboration with MoneySmart.