It’s not always easy to make sense of why certain trends go viral (anyone else as confused as I am on the “very demure, very mindful” trend?) yet they do.

Unlike the viral nature of social media, though, making sense of income tax breaks and investing in Singapore is relatively straightforward…although not as entertaining!

Free money, y’all

One of the biggest income tax relief programmes here is the Supplementary Retirement Scheme (SRS). It’s generously given out by the Inland Revenue Authority of Singapore (IRAS), who normally like to take our money in taxes rather than give us that cheddar back in tax breaks.

But hey, we should take what we can when any government department offers us, what’s effectively, a tax rebate!

If you’re looking for an in-depth and comprehensive guide to understanding the many ins and outs of the SRS, then check out our guide on everything you need to know about the SRS.

But what about making sense of whether it’s worth contributing to the SRS in the first place? We need to be super analytical about this and also understand whether it makes sense given our income bracket.

So, here’s what you should be pulling in before you even think about contributing to the SRS for those tax breaks and why there are actually two annual wage numbers to think about.

The supposedly big number for SRS investing

The best way to think about putting money into your SRS is being able to reach “critical mass”. That effectively means earning enough money so that your contributions actually make sense in terms of the tax breaks from the IRAS.

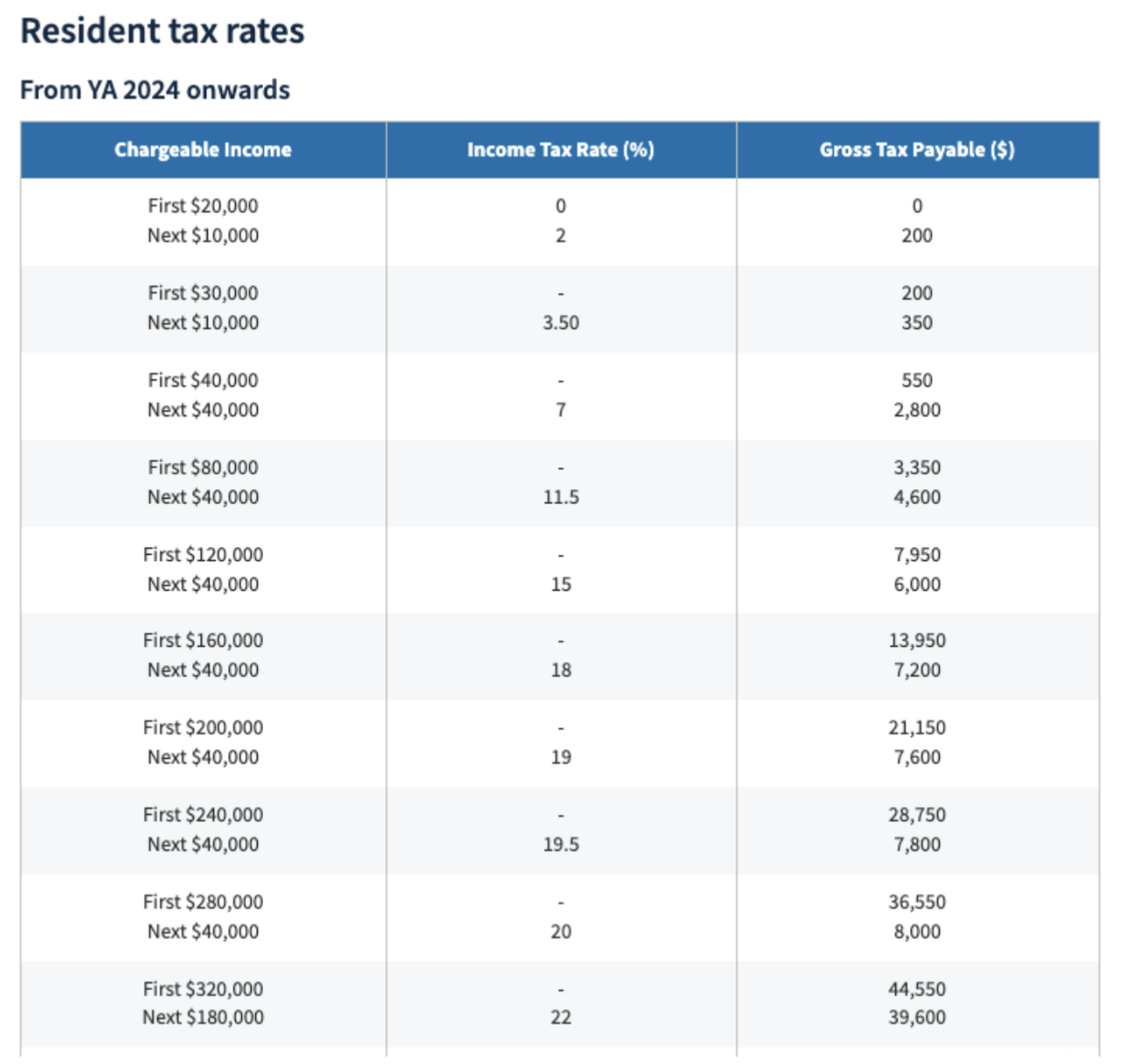

At what point does this effect start to kick in? Simply put, it starts making sense to contribute (small) amounts when you earn above $40,000 per annum (p.a.).

If you look at the below, you can see that your tax bill on the next $40,000 you earn (after your first $40,000) adds an extra $2,250 to your annual tax bill.

Source: IRAS

Source: IRAS.gov.sg

Let’s break that down into some numbers we can easily grasp. Remember that our annual contribution caps to the SRS are $15,300 for Singaporeans/Permanent Residents (PRs) and $35,700 for Foreigners.

Say you’re earning $60,000 p.a. as a Singaporean/PR and you contribute the whole $15,300 for the year to your SRS. That’ll save you $1,071 in taxes (15,300 x 7%). So, for clarity’s sake, for every $100 you contribute to the SRS, you’d save $7 in taxes – not a huge amount yet as our parents would always say “every little counts”.

How to think about analysing the SRS

Ok, that’s great but let’s actually be realistic. You’re not going to be contributing just over 25% of your annual pay to the SRS given you’ve got to live day to day and enjoy life. Plus that 20% from your CPF per month is going to already burn a hole in your pocket.

So, it’s more of an additional avenue for you to save rather than a “must have” tax break when you’re earning that much.

If you live like a monk and literally spend next to nothing on food, rental, parental allowance, going out etc. then sure, you’re going to have spare cash lying around to contribute. But that’s not most of us.

Put plainly, we have to take into account what we’re already contributing to the CPF on an annual basis and then think of the SRS as the “gravy” or “sauce” on top.

The real SRS wage number to focus on

So, at what point does the SRS actually become meaningful for you? Well, the ordinary wage (OW) ceiling for the CPF right now is $6,800 per month but let’s be conservative and look out to 1 January 2026 when the OW ceiling will be at $8,000 per month.

That means you’re making $96,000 p.a. but having to contribute 20% of that to the CPF, so you’re contributing $19,200 per year to your CPF. That’s already a pretty hefty sum. Let’s return to the SRS. At that wage level ($96,000 p.a.), every $100 you contribute to your SRS will give you $11.50 in tax savings. Again, that’s good but not “woweeeee” in terms of the amount saved.

Earning above $96,000 per year isn’t going to have you on the hook for any additional mandatory CPF contributions, so you’ve actually got more money at your disposal.

So, in reality, we should be looking to contribute more meaningful amounts (and yield those higher tax savings) when we both get into the higher tax brackets and have more income at our disposal that’s ex-CPF.

Personally, I think anything above the $120,000 p.a. mark will help you save a decent whack on tax while not impinging on your spending habits or existing retirement contributions.

Say you earn $140,000 p.a. and max out the $15,300 contribution cap. At the 15% tax bracket, that gives you an annual tax saving of $2,295. Say you earn $180,000 p.a. and max out the contribution cap – within the 18% tax bracket that saves you $2,754. Now we’re talkin’.

How to think about SRS contributions and where to invest

Finally, it’s useful to think about how much you should contribute on a regular basis. Just because you’re not maxing out the contribution cap, doesn’t mean you can’t contribute even $100 or $200 every so often.

In fact, opening an SRS account early and contributing even $1 can help you lock in the retirement age at contribution and allow you to withdraw your SRS funds earlier upon retirement.

The SRS effect starts to really ramp up and become more of a realistic contributor to your tax savings (and retirement funds) when you earn above $120,000 per year.

Remember, we need to invest our SRS funds and it shouldn’t be sat in cash because that earns just 0.05% p.a. in interest. Even putting into cash-like instruments isn’t worth it given you can get similar yields in your various CPF accounts.

So, your SRS funds should ideally be in low-cost, globally-diversified equity funds that can potentially give you a long-term return that is above what you’d get in your CPF.

To summarise, use the SRS to both save tax and invest…only when it makes sense!

Related Articles