Topping up your parents’ CPF Retirement Account has long been a way to offer financial support to family members. Now, you might be able to get money from the government when you do it.

The CPF Matched Retirement Savings Scheme (MRSS) is a new scheme that will run for five years from 2021 to 2025.

Under the scheme, the government will match contributions dollar-for-dollar made to eligible CPF accounts that fall short of the Basic Retirement Sum ($93,000 in 2021).

In light of the COVID-19 pandemic and the huge dent it’s going to make in many of our wallets for years to come, this is the government’s “no handouts” way of ensuring retirement readiness without completely removing personal responsibility.

Here's a quick guide to the Matched Retirement Savings Scheme and how you can benefit.

CORRECTION: An earlier edition of this article stated that you can use cash or CPF under this scheme. This is incorrect. Only cash top-ups are eligible.

What is the Matched Retirement Savings Scheme?

Under CPF's Matched Retirement Savings Scheme, the government will match dollar-for-dollar any contributions made to eligible seniors’ CPF accounts under the Retirement Sum Topping-Up Scheme from 2021 to 2025.

It's meant to help senior Singaporeans who do not have enough retirement savings to meet the Basic Retirement Sum ($93,000 in 2021).

For more on the Basic Retirement Sum, read: CPF Retirement Sum: How Does It Work and How Much Do You Need?

The cap for dollar-to-dollar matching is $600 per year. So, you can receive a maximum of $3,000 free from the government over 5 years.

This being a "Retirement" savings scheme, it applies only to Singaporeans aged 55 to 70. Not 55 yet? That's OK — you can still get this free money by topping up your family members' accounts.

Matched Retirement Savings Scheme eligibility criteria

But before you run off and deposit wads of cash into your parents’ CPF, you must first make sure that your recipients are eligible for the MRSS in the first place.

Age | 55 to 70 (both inclusive) |

Retirement Account (RA) Savings | Below the Basic Retirement Sum ($93,000 in 2021) |

Average Monthly Income | Not more than $4,000 |

Annual Value of Residence | Not more than $13,000 — covers most HDB flats |

Property Ownership | Own not more than one property |

Under the Retirement Sum Topping-Up Scheme, you can transfer money to the CPF account of one of the following people:

- Yourself

- Your parents

- Your parents-in-law

- Your grandparents-in-law

- Your spouse

- Your sibling

As you can see, if you are aged over 55 and satisfy all of the above criteria, you can even make MRSS top-ups to yourself and benefit from the government’s dollar-for-dollar matching.

How does the Matched Retirement Savings Scheme work?

First, check if you/your recipient is eligible for the dollar-for-dollar matching scheme above. Make sure to check if the recipient's CPF balance is below the Basic Retirement Sum of $93,000.

Next, top up your recipients’ CPF accounts with cash. The matching grant will be automatically credited into the recipient’s Retirement Account by the first quarter of the following year.

So, let’s say you deposit $600 into your mother’s CPF Retirement Account in 2021. The government will pay an additional $600 into your mother’s CPF Retirement Account by the first quarter of 2022.

You can repeat this every year up to 2025 to get the maximum $3,000 from the government.

What are the other benefits of topping up?

Other than the government’s dollar-for-dollar matching of transfers, here are some additional benefits you get:

- Contributions earn high CPF interest rates (4% or more)

- Runs alongside CPF LIFE scheme for retirement payouts

- Tax reliefs up to $14,000 a year if you top up in cash

Although the Matched Retirement Savings Scheme is capped at $600 a year, you might want to consider topping up more anyway given the poor interest rates that banks are offering.

Your contributions will enjoy CPF interest rates, which are more attractive than ever. The Retirement Account interest rate for those aged 55 and above is a sweet 4% per annum + an additional 1% on the first $60,000. For an older person with presumably a lower risk tolerance, that is about as high as it gets.

Matched Retirement Savings Scheme & CPF LIFE

The Matched Retirement Savings Scheme is compatible with and runs alongside the existing CPF LIFE scheme, which offers lifelong payouts for the rest of your life.

Seniors born in 1958 or after, who have at least $40,000 or $60,000 (depending on age) in their Retirement Account, will be auto-enrolled in CPF LIFE. If your parents are not auto-enrolled, they can opt into the scheme anytime before the age of 80.

How CPF LIFE works is:

- When you turn 55, your Special and Ordinary Accounts will merge to form a Retirement Account

- You can withdraw Retirement Account above the Basic or Full Retirement Sum

- From age 65 to 70, you can start your CPF LIFE plan

- At this point, the remaining RA balance will be used to pay a lump sum premium for CPF LIFE

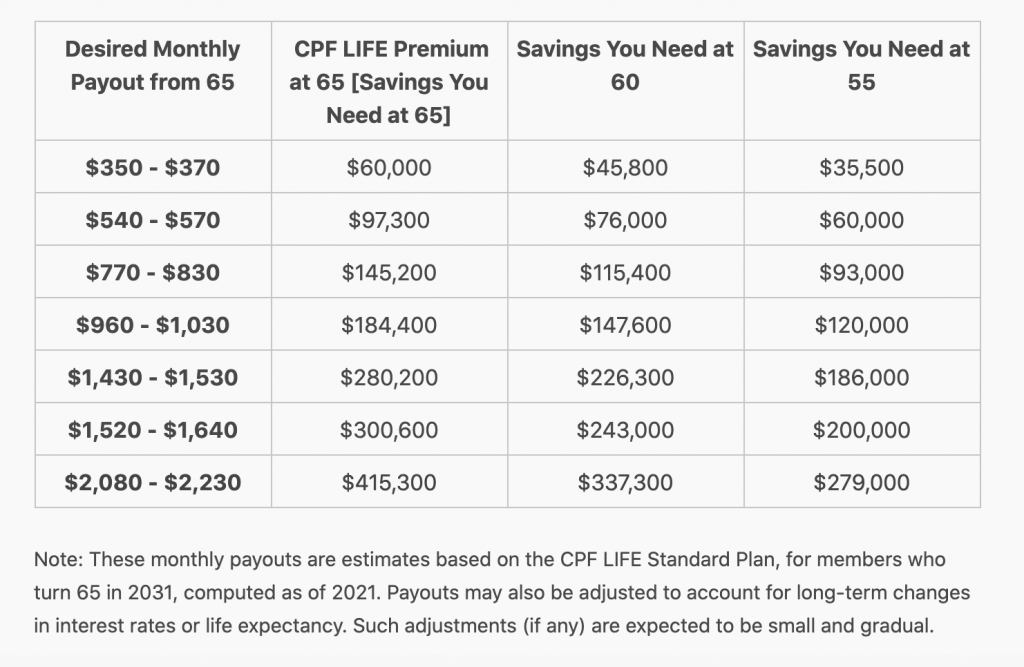

For those who are enrolled in CPF LIFE, the amount of money you have in your Retirement Account will determine the payouts you receive.

Although you can join the CPF LIFE scheme with less than the Basic Retirement Sum in your RA, your monthly payouts will be correspondingly low, as this screenshot from CPF shows.

Screenshot from CPF website

To increase your retirement payouts and live more comfortably in expensive Singapore, you should aim to save at least the Basic Retirement Sum or more, if possible.

What if my parents aren't on CPF LIFE?

If your parents were born before 1958 and have not opted in to CPF LIFE, they are on the old Retirement Sum scheme.

That means their payouts are tiered depending on whether they have reached the:

- Basic Retirement Sum: $93,000 for those turning 55 in 2021

- Full Retirement Sum: $186,000 for those turning 55 in 2021

- Enhanced Retirement Sum: $279,000 for those turning 55 in 2021

(The Enhanced Retirement Sum is the maximum you can keep in your Retirement Account; any amounts in excess can be withdrawn freely or left in the account to earn interest.)

So in order to maximise your CPF account’s potential as a source of retirement income, you have to make sure you meet certain balance thresholds.

Note that the old Retirement Sum Scheme pays out only until age 90, whereas CPF LIFE pays out for life no matter how old you get. It's definitely worthwhile to consider switching out, which you can up to age 80.

Bonus: Up to $14,000 tax relief under the Retirement Sum Topping-Up Scheme

One final benefit is that you get to enjoy tax relief for your MRSS contributions.

The person making MRSS top-ups can enjoy up to $14,000 worth of tax relief under the Retirement Sum Topping-Up Scheme category.

The maximum of $14,000 tax relief is allocated as follows:

- $7,000 for top-ups made to yourself or by your employer on your behalf

- $7,000 for top-ups made to your parents or other family members (top-ups to spouses or siblings do not qualify for tax relief, unless their income from all sources was not more than $4,000 in the preceding year, or they are physically or mentally handicapped)

In all, if you or your parents qualify for the Matched Retirement Savings Scheme, now is an excellent time to do some strategic top-ups.

Know someone who might benefit from the Matched Retirement Savings Scheme? Share this article with them.

Related Articles