Trying to understand all the acronyms that the CPF board in Singapore likes to throw at us can feel like juggling 10 balls while riding a unicycle (i.e. impossible).

But understanding the importance of these CPF terms is going to turn you into a retirement pro. Fine, it might not give you bragging rights with your friends but you can flex in other ways outside CPF too!

By getting down with the CPF terms, and understanding what each can do for you, you’re going to set yourself up early for success with retirement investing.

That’s because whether you’re saving through your CPF Special Account (CPF SA) or thinking about CPF LIFE payments in retirement, you need to know your lingo.

So, here’s a breakdown—an Ultimate Shiok Dummies Guide, if you will—of everything CPF-related in Singapore.

Basic CPF Terms

Before we get into the weeds, we need to settle down and get the foundations right first. That means understanding what CPF actually is.

The CPF stands for “Central Provident Fund” and is Singapore’s mandatory social security savings scheme that applies to all Singapore Citizens and Permanent Residents (PRs).

Yes, yes, they make us put money away every month but it’s for a good cause – our own retirement! So, what are the different CPF accounts we need to be aware of? It comes down to basically four accounts.

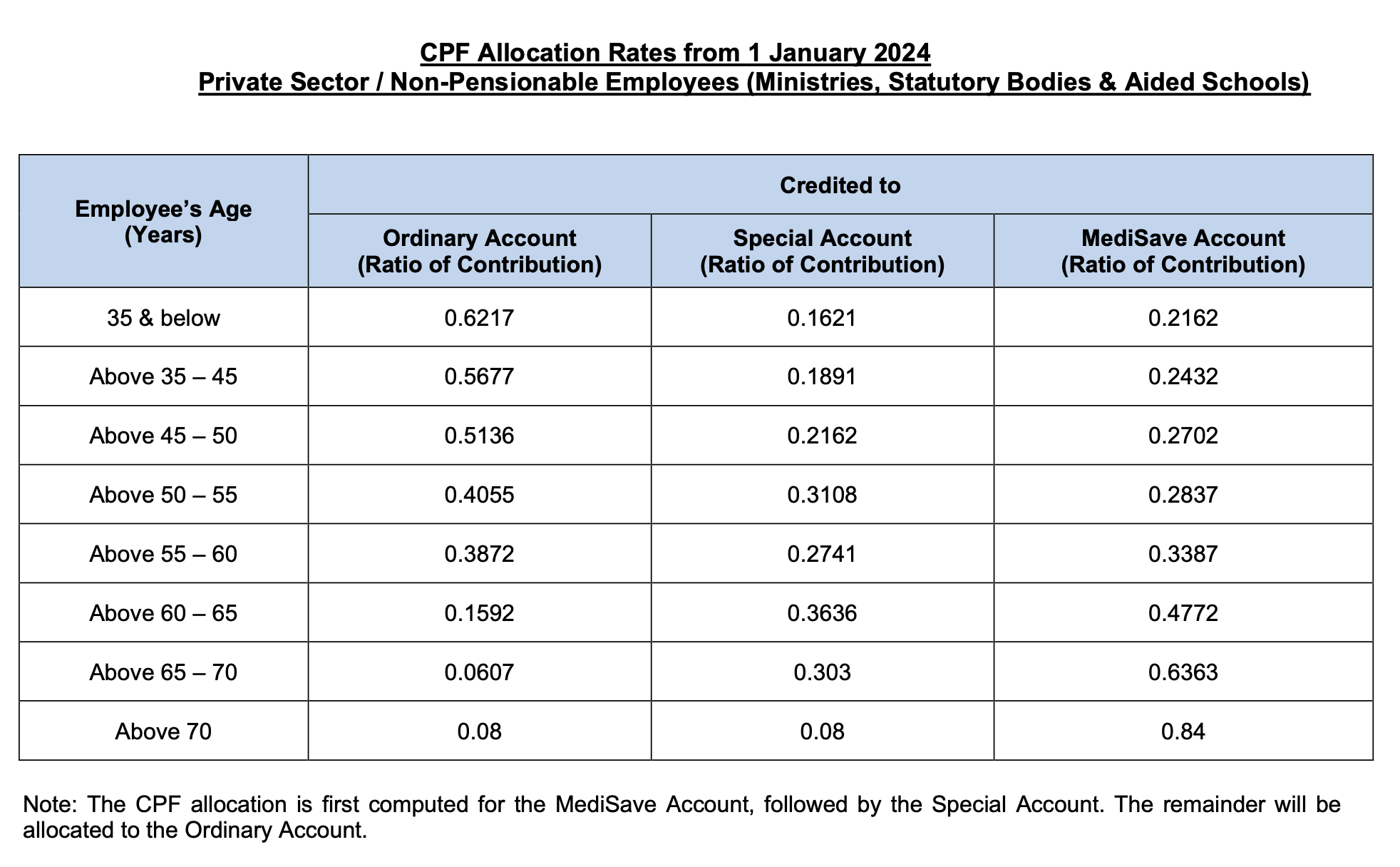

CPF Ordinary Account

The CPF Ordinary Account (CPF OA) is actually pretty ordinary and not that exciting. Funds in this account only earn interest of 2.5% per annum (p.a.) and your money here is meant for housing costs, not building wealth for retirement. As a result, more of your CPF contributions go here in your earlier working years to support that home purchase.

CPF Special Account

The CPF Special Account (CPF SA) is meant more for retirement expenses so, in that sense, it is slightly more special than the OA. But that “special” quality comes down to higher interest rate that CPF SA funds earn – at 4.08% p.a. it’s much higher than what you can get in your CPF OA.

Your funds in here get turned into a Retirement Account (RA) upon reaching 55 and you can’t withdraw any CPF SA funds before you reach the retirement age.

CPF MediSave Account

The CPF MediSave Account (CPF MA) is for – you guessed it! – medical expenses as well as future medical expenses in retirement. Similar to the CPF SA, any funds in the CPF MA earns interest at 4.08% p.a. The great thing about this account is you can use it to help not only yourself but also family members too, including your spouse, children, parents, grandparents, and siblings.

CPF Retirement Account

So, when you turn 55 your CPF SA actually turns into a CPF Retirement Account (CPF RA). This is where you have your CPF SA funds, followed by CPF OA funds, transferred to. It basically goes towards 3 retirement sums, which we’ll touch on later. To cut a long story short, your CPF savings in your RA will basically determine your future monthly payouts in retirement.

Source: CPF

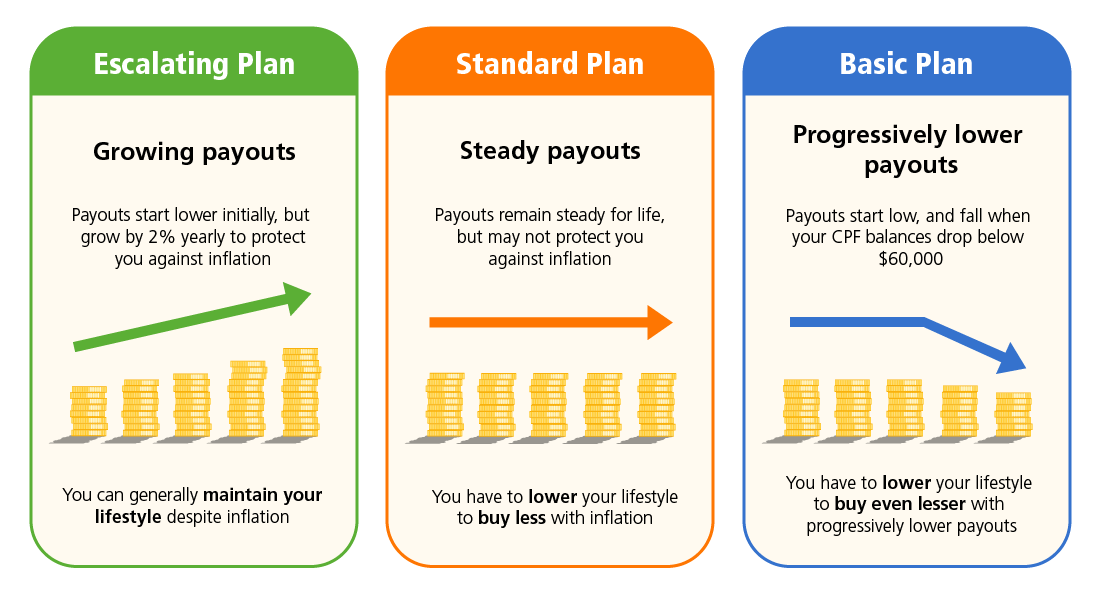

CPF LIFE

When you hit 65 you can actually receive CPF Lifelong Income For the Elderly (CPF LIFE) payouts.

The important thing to understand about this scheme is that it’s an longevity annuity insurance scheme and not an investment product. There are three levels of payouts that you can get, determined by how much you’re willing to dish out in premiums.

- Escalating Plan: These payouts grow by 2% per year to protect you against rising costs

- Steady Plan: This is a standard monthly payout and they won’t grow every year

- Basic Plan: This is the bare bones plan and you’ll receive progressively lower payouts in the future

Image: CPF

Don't stop now! The gold is just a scroll ahead...

CPF Schemes

Majulah Package

While you may be chanting “Majulah Singapore!” with gusto at the NDP, the Majulah Package is more likely to get only older Singaporeans excited about their retirement savings.

That’s because this scheme is only for Singaporeans who were born in 1973 or earlier (sorry all you Millennials and Gen Z-ers).

There are three components to the package:

- Earn and Save Bonus: From March 2025, there’ll be a S$400 to S$1,000 annual bonus to CPF RAs or CPF SAs for Singaporeans who work and earn up to S$6,000 per month

- Retirement Savings Bonus: From December 2024, there’s a S$1,000 to S$1,500 one-off bonus to CPF RAs or CPF SAs for Singaporeans with CPF retirement savings that are less than the 2023 Basic Retirement Sum (BRS) of S$99,400

- MediSave Bonus: A $750 to S$1,500 one-off bonus to CPF MediSave Account

Singapore’s Ministry of Finance says the package will benefit around 1.6 million Singaporeans and every Singaporean born in 1973 or earlier will get to enjoy at least one of the components of the Majulah Package.

Matched Retirement Savings Scheme (MRSS)

The CPF love for acronyms doesn’t stop at the account levels. The MRSS was launched fairly recently (in 2021) and is aimed at helping senior citizens in Singapore—with low retirement savings—save more by matching top-ups to their CPF RA, up to S$600 per year.

So, Singaporeans aged 55 to 70 years old (although this will be 55 and above from 1 January 2025) are eligible but they must also meet certain requirements, namely:

- Have CPF RA savings less than the 2024 BRS of S$102,900

- Average monthly income of not more than S$4,000

- Annual value of residence of not more than S$21,000

- Not own more than one property

Workfare Income Supplement (WIS)

The WIS is a scheme that helps top up the salaries of lower-income workers to help them meet save sufficiently for retirement.

It’s mainly for Singaporean workers who are in the bottom 20% of earners, with some support for those slightly above this level.

As of February 2024, over S$10.5 billion has been disbursed through the WIS to over 1 million lower-income workers.

While there are obviously criteria to meet eligibility, the current annual maximum WIS payouts range from S$2,100 for those aged 30-34 all the way up to S$4,200 for those aged 60 and above.

Not all of this goes to CPF, with around 40% allocated in cash while the remaining 60% goes towards CPF contributions.

Healthcare terms

MediShield Life

Think of MediShield Life as your basic health insurance plan. It’s administered by the CPF Board and helps you pay for those large hospital bills and select pricey outpatient treatments, like kidney dialysis or chemotherapy for cancer.

It’s designed to help you pay less and not completely drain your MediSave should a large hospital bill be forthcoming.

The plan typically allows you to stay in public hospitals at a subsidized rate but you’re going to be restricted to the B2/C-type wards so if you want a bit more privacy (and comfort) through A/B1-typ wards or even going private, you’ll have to stump up more of the moolah yourself.

All Singaporean Citizens and Permanent Residents are covered by MediShield Life and MediSave.

Integrated Shield Plan (IP)

Ok, so you want to have a bit more protection and coverage beyond the basic MediShield Life plan. That’s where the Integrated Shield Plan (IP) comes in.

This is an extra layer of private insurance coverage that has a higher allowance for stays at private hospitals or Class B1/A wards in public hospitals.

There are loads of different plans to choose from, so you need to be aware of what you’re purchasing. However, if you have an Integrated Shield Plan, you already have MediShield Life.

There is no duplicate coverage and you won’t have to pay two separate premiums.

MediSave Contribution Ceiling

While you might think you can go and save as much as you want in your CPF MA, you can’t. There’s actually a limit, believe it or not.

This is referred to as the Basic Healthcare Sum (BHS) and you can save up to the prevailing BHS if you haven’t turned 65 yet.

Currently, the BHS in 2024 is set at S$71,500 and it’s adjusted yearly to account for longer life expectancy and higher healthcare costs.

ALSO READ: CPF Guide Singapore: CPF Contribution Rates, Ceilings, Retirement Sum and More (2024)

Contribution terms

CPF contribution rates

Ok, so you’re actually bringing in CPF money – that’s great! But where is it coming from? Well, 17% of it comes from your employer up to you working until you’re 55 years old.

Another 20% comes from you, which means you’re getting a solid 37% in CPF contributions per month! After the age of 55, the contribution rates from both the employee and employer start to come down. Of course, there is the issue of the wage ceiling that everyone has to contend with.

That means you’re capped at how much you can get from CPF depending on how much you earn. So, say—hypothetically speaking—you’re balling out and earning S$50,000 per month, you will NOT be getting 37% of that (or S$18,500) per month in CPF contributions.

In fact, the wage ceiling means anything earned beyond a certain amount per month isn’t contributed towards CPF.

As a result, the current CPF wage ceiling is S$6,800 per month. So, the maximum that you can have in CPF contributions is capped at 37% of that, or S$2,516 per month. This wage ceiling will gradually increase to S$8,000 by 1 January 2026 so that monthly maximum will also increase.

Withdrawal and Retirement terms

CPF withdrawal rules

While you may think you can only withdraw CPF funds when you hit the retirement age, the reality is that you can withdraw some funds when you reach 55 years old.

There are three tiers for withdrawals. First off, if you haven’t met the Full Retirement Sum (FRS) (currently S$205,800) then you’re severely limited in terms of what you can withdraw at age 55 (sad face, I know). But there’s some good news in the other two options.

Second, if you have met the FRS in your CPF savings you can withdraw any amount above this from your CPF OA and CPF SA. Of course, the CPF Board does encourage you to consider making those withdrawals in your retirement years and not immediately after you turn 55.

And finally, the third tier is if you’re a property owner with a lease that lasts up to at least age 95 then you can set aside your FRS with a mixture of property and cash, and withdraw part of your CPF RA savings.

Retirement Sums

When we turn 55, we get given a CPF Retirement Account (RA) and this is where our CPF OA and CPF SA savings are transferred to.

Currently, there are three retirement sums that will allow us to get paid when we do eventually retire. As of 2024, these retirement sums are:

- Basic Retirement Sum (BRS) – S$102,900

- Full Retirement Sum (FRS) – S$205,800 (BRS x 2)

- Enhanced Retirement Sum (ERS) – S$308,700 (BRS x 3)

While the ERS is currently 3 times the BRS, from 1 January 2025, that will be raised to 4 times the BRS. All three of these retirement sums are increased by just over 3% per year to keep pace with inflation so don’t worry, they won’t be the same every year!

Investment-related terms

CPF Investment Scheme (CPFIS)

Some of us have probably used the CPFIS and (if we haven’t) then we should! That’s because the CPFIS allows us to invest a portion of our CPF OA and CPF SA savings to grow our wealth.

Remember that global stocks are the best long-term wealth creators—think decades rather than months/years—so it makes complete sense to make use of the CPFIS.

Luckily for us, the CPF Board makes it easy. There are a couple of requirements though. You have to have minimum balances of S$20,000 in your CPF OA and S$40,000 in your CPF SA as well as completing a CPFIS Self-Awareness Questionnaire (yes, apparently we have to be aware of ourselves and our investments)!

Any CPF funds in those accounts beyond that can be invested via the CPFIS. It’s also broken up into separate schemes so you have the CPFIS-OA (for funds from your OA) and the CPFIS-SA (for funds from your SA).

While the CPFIS-OA places percentage limits on stocks (35%) and gold (10%) of your investible savings, you are able to purchase individual stocks or REITs as well as a wide range of ETFs and bonds.

That’s not an option for the CPFIS-SA, where buying individual stocks, REITs, and gold isn’t permitted while higher-risk ETFs and corporate bonds aren’t options for individuals either.

In that sense, the CPF Board is pushing us to invest more via our CPF OA to generate better long-term returns, which is logical given the lower annual interest rate on that account versus the CPF SA.

Conclusion

There you have it, peeps—a complete guide for total beginners to the wonderful (and scary!) world of the CPF.

It is uber complicated, I agree, but once you find your feet and get used to understanding the ins and outs of the scheme, it’s a great tool to help us reach our retirement goals.

Remember, the first step is equipping ourselves with the knowledge so we can best take advantage of what the CPF has to offer. Best of luck on your retirement journey!

Found this article useful? Share it with your family and friends!

Related Articles