Finding the best savings account in Singapore isn’t just about rates—it’s about what fits your life. With banks changing interest rates and requirements every few months, it can be tricky to spot the real winners.

And as we approach May, 2 nerfs are headed our way: the OCBC 360 and Standard Chartered BonusSaver accounts are both set to see rate cuts, making it even more important to know where your money is best parked.

Whether you're saving for your first big goal, growing your nest egg, or just want a hassle-free place for your cash, this guide to the best savings accounts in Singapore will help you find your match. We've done the legwork by comparing all the top savings accounts in Singapore, so you can easily see which ones offer the best rates, perks, and flexibility right now.

How we compare and update these rankings Each month, we review and update the best savings accounts in Singapore, looking beyond just the headline interest rates. We check the fine print, perks, requirements, and latest promotions to make sure our information is accurate and useful. All rates and details are current as of 28 Apr 2026. |

[ms-toc title="What are the best savings accounts in Singapore with the highest interest rates in 2026?"]

At a glance: Best savings accounts in Singapore with highest interest rates (Apr 2026)

Savings account | Effective interest rates (p.a.) | Best for |

Up to 5.85% (on first $100,000, fulfil 4 criteria) | High spenders | |

Up to 4.45% (on first $100,000, fulfil 5 criteria) | Lower income earners ($1,800 min. salary) | |

Up to 7.51% (on first $50,000 – $500,000, fulfil 5 criteria) | Those with other Citibank products | |

Up to 4.60% (on first $100,000, fulfil 4 criteria) | High spenders | |

Up to 1.90% (on first $150,000, fulfil 2 criteria) | Freelancers & self-employed | |

Up to 3.33% (on first $75,000, fulfil 3 criteria) | Home, education, car loan users | |

Up to 4.10% (on first $50,000 – $100,000, fulfil 3 criteria) | Salaried workers | |

1.85% p.a. (on first $75,000, fulfil 3 criteria) | Young adults starting their careers | |

3.50% (just deposit and maintain money, no criteria to fulfil!) | Students or first-jobbers | |

Up to 2.85% (register and qualify for the HSBC Everyday+ Rewards Programme) | HSBC Everyday+ Rewards Programme, HSBC Everyday Global Debit Card users |

Most savings accounts require you to jump through a whole bunch of hoops to enjoy their best rates. But let’s be realistic here. Most of us aren’t going to be taking a home loan, buying insurance from the bank, and investing with the bank—and certainly not all at the same time. What will you earn if you only fulfil 2 or 3 criteria? For example, perhaps you only credit your salary and spend on your credit card. If that sounds like you, here’s our realistic summary for you if you have $50,000 or $100,000 to stash away:

Savings account and the 2-3 easiest requirements to fulfil | Effective interest rate and earnings on first $50,000 | Effective interest rate and earnings on first $100,000 |

Citi Wealth First Account Save $3,000/month + Spend $250/month | 3.01% (up to first $50,000) | 1.53% p.a. (for regular Citibanking customers, 3.01% only applies to the first $50,000) You earn: $1,530 per year ($128 per month) |

Standard Chartered BonusSaver Credit min. $3,000 salary + Spend $1,000/month | 1.85% p.a. (up to first $100,000) | 1.85% p.a. (up to first $100,000) You earn: $1,850 (~$154 per month) |

UOB One | 1.00% p.a. (up to first $75,000) You earn: $500 per year (~$42 per month) | 1.38% p.a. (EIR on first $100,000) You earn: $1,375 per year (~$115 per month) |

OCBC 360 | 1.70% p.a. (up to first $75,000) You earn: $850 per year (~$71 per month) | 1.95% p.a. (EIR on first $100,000) You earn: $1,950 ($163 per month) |

Bank of China SmartSaver | 1.20% p.a. (up to first $100,000) You earn: $600 per year (~$50 per month) | 1.20% p.a. (up to first $100,000) You earn:$1,200 per year (~$100 per month) |

Maybank Save Up Programme | 1.24% p.a. (up to first $50,000) You earn: $619 per year (~$52 per month) | 1.12% p.a. (EIR on first $100,000, since bonus interest only applies to the first $75,000) You earn: $1,121.50 per year (~$93 per month) |

DBS Multiplier | 1.80% p.a. (up to first $50,000) You earn: $900 per year (~$75 per month) | 0.925% p.a. (since 1.80% p.a. only applies up to first $50,000) You earn: $927 per year (~$77 per month) |

CIMB FastSaver | 1.84% p.a. (up to first $50,000) You earn: $920 per year (~$77 per month) | 1.59% p.a. (EIR on first $100,000) You earn: $1,590 per year (~$133 per month) |

POSB SAYE (Save As You Earn) | 3.50% p.a. You earn: $1,750 per year (~$146 per month) | 3.50% p.a. You earn: $3,500 per year (~$292 per month) |

HSBC Everyday+ Rewards Programme Deposit min. $2,000 and make 5 transactions | Up to 1.85% p.a. interest + 1% cashback (capped at $300 a month) You earn: $925 per year (~$77 per month) (excludes cashback) | Up to 1.85% p.a. interest + 1% cashback (capped at $300 a month) You earn: $1,850 per year (~$154 per month) (excludes cashback) |

Note: The table above assumes you have a regular banking relationship. If you earn more, spend more, or are a premier or private banking client, you may enjoy better rates. Read the individual sections on each savings account below to find out more.

Best savings account for…

Not every saver has the same needs. Here’s our quick guide to the best savings accounts in Singapore for different life stages and banking habits:

High savers (large balances)

If you consistently keep a high balance (above $100,000), look for accounts that offer elevated rates on larger sums and don’t cap bonus interest too soon. The UOB One Account is a standout here, as it offers a flat effective interest rate on balances up to $150,000, making it one of the best options for those who want their full nest egg to earn more. Alternatively, the Citi Wealth First Account may suit those able to meet higher eligibility criteria for even bigger balances.

Students

Students often want accounts with minimal hoops and no penalties for lower balances. The POSB SAYE Account is popular for its zero-fuss, “set and forget” savings—just make regular deposits and leave your savings to grow. If liquidity is more important, CIMB FastSaver has no complex requirements, no fall-below fee, and a low minimum balance, making it an easy starting point for younger savers.

Freelancers and those with no salary credit

If your income doesn’t arrive in predictable monthly GIRO credits, you’ll want an account that doesn’t penalise you for missing a salary requirement. CIMB FastSaver is flexible and doesn’t demand a salary credit to unlock its highest rates. DBS Multiplier is also worth a look—its bonus interest can be unlocked through various transaction categories, including investments and PayLah! spending, rather than just salary.

No-fuss users

If you prefer to keep things simple—minimal paperwork, few conditions, and reliable interest—the UOB One Account is one of the easiest to manage: just credit your salary and spend $500 on a UOB card to qualify for bonus rates. The POSB SAYE Account is another strong contender for hands-off savers who just want to “set and forget” for steady returns.

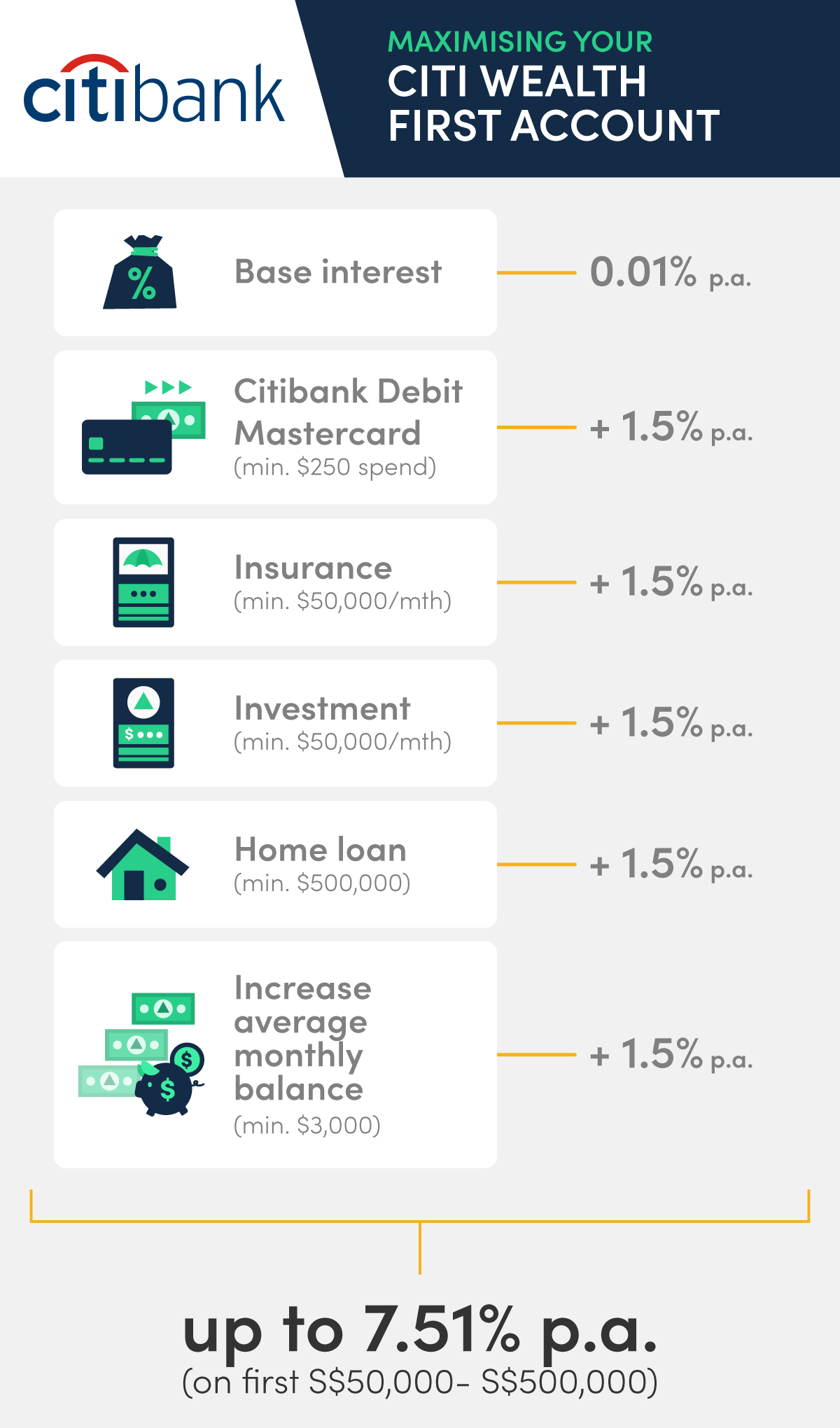

1. Citi Wealth First Account

Citibanking, Citi Priority | Citigold | Citigold Private Client | |

Deposit amount | First $50,000 | First $250,000 | First $500,000 |

Base interest rate | 0.01% p.a. | ||

Spend (min. $250/month on Citibank Debit Mastercard) | 1.5% p.a. | ||

Invest (min. $50,000/month) | 1.5% p.a. | ||

Insure (min. $50,000/month) | 1.5% p.a. | ||

Borrow (min. $500,000 home loan) | 1.5% p.a. | ||

Save (min. $3,000/month) | 1.5% p.a. | ||

TOTAL | 7.51% p.a. | ||

The Citi Wealth First Account has a simple mechanic for calculating its total interest rate: base interest (0.01%) + bonus interest (up to 7.50%).

Its base interest starts at 0.01% for everyone, whether you’re a Citibanking, Citi Priority, Citigold, or Citigold Private Client customer. That’s the lowest base interest rate out of all the savings accounts on this list.

Next, beef up that measly 0.01% up with bonus interest rates. You get different bonus rates depending on which of the following categories you fulfil:

- Spend (+1.5%): Spend at least $250/month on your Citibank Debit Mastercard.

- Invest (+1.5%): Purchase one or more new single lump sum investments totalling at least $50,000/month. Investments can include Unit Trust, Structured Notes and Bonds.

- Insure (+1.5%): Purchase one or more new single premium policies totalling at least $50,000/month. This excludes policies purchased using Central Provident Fund Savings or Supplementary Retirement Schemes.

- Borrow (+1.5%): Take up a new home loan of at least $500,000.

- Save (+1.5%): Deposit more money into your account, increasing your account’s average daily balance by at least $3,000 from the previous month's.

If you fulfil all of the transaction categories above, the maximum interest rate you can get with the Citi Wealth First Account is a generous 7.51%. That's one of the highest rates among the savings accounts this month. Plus, it applies to the first $50,000 to $150,000 in your account, and not just the first $25,000 after the first $100,000 or something like that (looking at you, UOB One). That means 7.51% p.a. is the effective interest rate!

Realistically speaking, most of us can only deposit our salaries in the account, i.e. "Save", and "Spend". If you only fulfil these 2 criteria, you'll earn 3.01% p.a. interest on the Citi Wealth First Account. That's $1,505 earned per year from your first $50,000.

The only advantage to starting a Citigold or Citigold Private Client banking relationship is that the bonus interest rates can apply to a larger sum of money. For Citibanking and Citi Priority customers, bonus interest rates are applied to only the first $50,000, according to the Citi Wealth First T&Cs (Clause 7). This increases to $250,000 for Citigold and $500,000 for Citigold Private Client.

Citi Wealth First Account

- Minimum balance: $15,000

- Fall below fee: $15

- Bonus interest cap: $50,000 – $500,000

- Base Interest Rate p.a.

- 0.01%

- Max. Interest Rate p.a.

- 7.51%

- Total Relationship Balance

- S$350,000

Get S$1,500 Cash or 19,050 SmartPoints (enough to redeem an Apple iPhone 17 Pro Max)

- Sign up as an Accredited Investor

- Deposit S$500,000 AUM in fresh funds within 3 calendar months

OR

- Sign up as an Non-Accredited Investor

- Deposit S$500,000 AUM in fresh funds within 3 calendar months

- Make a new qualified investment of min. S$100,000 within 3 calendar months

Get S$1,200 Cash or 15,970 SmartPoints (enough to redeem an Apple 13-inch MacBook Air)

- Sign up as an Accredited Investor

- Deposit S$350,000 AUM in fresh funds within 3 calendar months

Get S$900 Cash

- Sign up as an Non-Accredited Investor

- Deposit S$350,000 AUM in fresh funds within 3 calendar months

PLUS get an additional S$200 Cash Bonus on top of your gifts if you fund the fresh funds within 2 months! T&Cs apply.

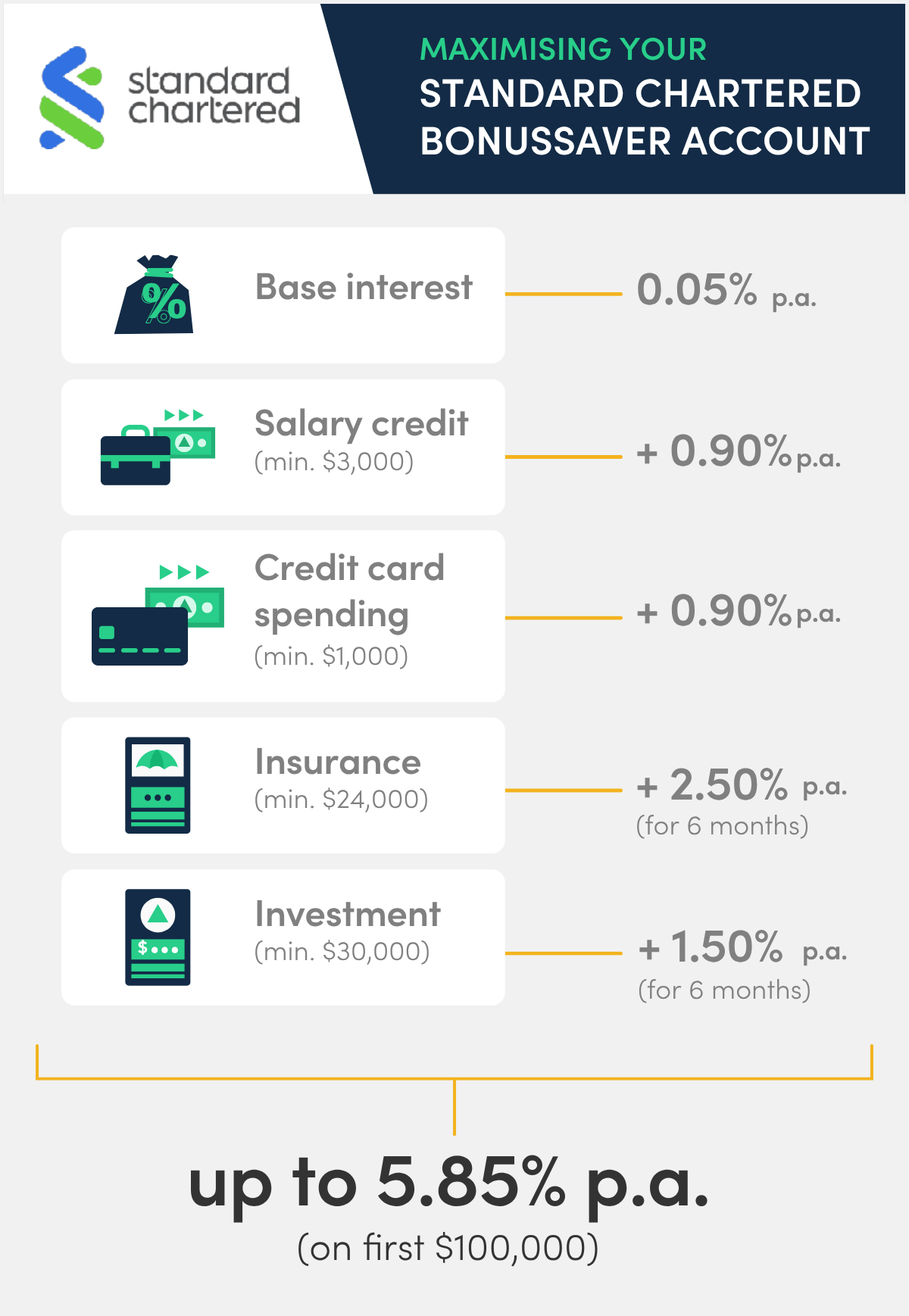

2. Standard Chartered BonusSaver account interest rates

Following changes that took place on 1 Jan 2026, the Standard Chartered BonusSaver savings account is getting nerfed again. From 1 May 2026, here's what will be changing:

Transactions | Interest rates from 1 May 2026 |

None (base interest) | 0.05% |

Salary credit (min. $3,000) |

|

Credit card spending (min. $1,000) |

|

Invest in eligible unit trust (min. |

|

Buy eligible insurance (min. $24,000) | +2.50% for 6 months |

Total interest |

|

- Base Interest Rate

- 0.05% p.a.

- Max. Interest Rate

- Up to 5.85% p.a.

- Min. Balance

- S$3,000

While 5.85% p.a. is pretty high, it isn’t easy to hit this maximum interest rate on the Standard Chartered BonusSaver. You’d need to fulfil all 4 requirements: credit your salary, spend on your credit card, invest, and buy insurance. Tough!

If you only catch the lowest hanging fruit, salary credit (0.90% p.a.) and credit card spending (0.90% p.a.), you'll earn 1.85% p.a. inclusive of the base 0.05% p.a. However, if you don't have a problem meeting those 2 requirements, you can also consider these 2 other accounts:

- UOB One Account: Earn 1.90% p.a. on your first $150,000 with credit card spending and salary crediting

- OCBC 360 Account: Earn 1.95% p.a. on your first $100,000 with credit card spending, salary crediting, and saving $500 a month

On the plus side, the juicy 5.85% p.a. is applied to the entire sum of $100,000, whereas accounts like the UOB One savings account are only going to give their highest interest rate to a smaller sum based on a tiered system. (Check our review of the UOB One account to see the effective interest rates on the entire $100,000 sum.)

Do note that you only get the bonus interest for crediting your salary if you're earning at least $3,000 per month. If you earn less, I suggest the OCBC 360 or UOB One savings accounts instead. The former will give you 1.30% p.a. interest on your first $100,000 for crediting a minimum salary of $1,800. UOB has a lower salary requirement of $1,600, but you need to stack the salary crediting with your UOB credit card spend to unlock its rates—1.90% p.a. on your first $150,000.

Standard Chartered Bonus Saver

- Minimum balance: $3,000

- Fall below fee: $5

- Bonus interest cap: $100,000

- on eligible spends

- 1.5% Cashback

- Min Spend

- S$0

- Cashback Cap

- Unlimited

Get S$350 Cash via PayNow or earn 4,000 SmartPoints (worth up to S$469 of Gifts) when you spend min. S$800 in 30 days AND apply to any of the following SCB products through MoneySmart (Bonus$aver Account, CashOne Loan, EasyPay or Funds Transfer). T&Cs apply.

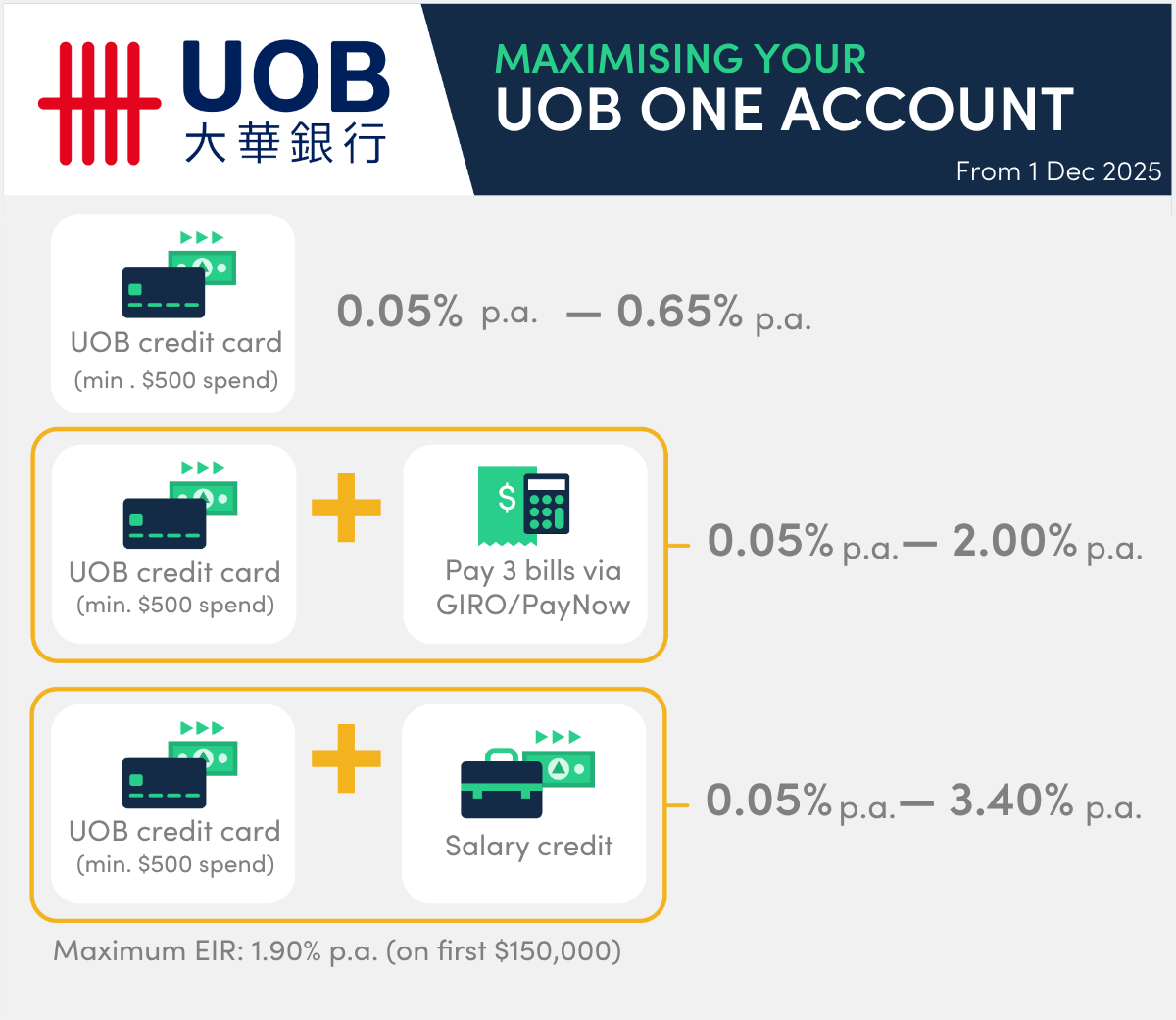

3. UOB One savings account interest rates

The UOB One Account did us all a great service from Dec 2022 to Apr 2024, offering a rate of up to 7.80% (EIR: 5.00% p.a.) back then for simply spending on a UOB credit card and crediting our salaries to the account. Oh, the glory days.

But now, one of Singapore's most popular savings accounts is seeing a maximum EIR of just 1.90% p.a.

UOB One savings account interest rates

Account Monthly Average Balance | $500 spend per month on eligible UOB Card | $500 spend per month on eligible UOB Card + 3 GIRO debit transactions | $500 spend per month on eligible UOB Card + credit salary via GIRO |

First $75,000 | 0.65% | 1.00% | 1.00% |

Next $50,000 | 0.05% | 2.00% | 2.50% |

Next $25,000 | 0.05% | 0.05% | 3.40% |

Above $150,000 | 0.05% | 0.05% | 0.05% |

The highest tiered interest is now 3.4% p.a.

Notice I said "tiered". Meaning, the advertised interest rates above are only applied on specific tiers. For example, the 3.40% only applies to the $25,000 after your first $125,000.

To properly assess your earnings with the UOB One Account, what you need to look at is the effective interest rate—the true interest rate on the full amount you deposit in your UOB One Account.

Effective interest rates on UOB One Account (p.a.) | |||

Account Monthly Average Balance | $500 spend per month on eligible UOB Card | $500 spend per month on eligible UOB Card + 3 GIRO debit transactions | $500 spend per month on eligible UOB Card + credit salary via GIRO |

$75,000 | 0.65% | 1.00% | 1.00% |

$125,000 | 0.41% | 1.40% | 1.60% |

$150,000 | 0.35% | 1.18% | 1.90% |

The maximum EIR you can earn with UOB One is 1.90% on your first $150,000. This assumes you spend on a UOB credit card and credit your salary to the account (we'll get to the mechanics in the sub-section below).

While it isn't exactly sky high, the 1.90% p.a. is at least simple to achieve—just fulfil 2 easy criteria of crediting your salary and spending on a UOB card.

If you want more options, there's also the OCBC 360 savings account to consider, the closest competitor to UOB One. It offers 2.45% p.a. for those who credit their salary, spend on an OCBC credit card, and save at least $500 a month. Although this rate is higher, note that the last criterion of saving money puts some restrictions on your account withdrawals—you have to make sure your average balance increases by $500 each month.

How to maximise interest on the UOB One savings account

The UOB One account's criteria to snag the highest interest rate is easy peasy. You only need to fulfil these 2 requirements:

- Credit your salary to the UOB One account via GIRO

- Spend at least $500 spend per month on an eligible UOB Card

The eligible cards you can hit the $500 spend on are:

- UOB One Card

- UOB Lady’s Card (all card types)

- UOB EVOL Card

- Lazada-UOB Card

- UOB One Debit Visa Card

- UOB One Debit Mastercard

- UOB Lady’s Debit Card

- UOB FX+ Debit Card

Among these cards, the UOB One Card is one of the best cards to pair with the UOB One savings account. Find out why in our full review of the UOB One account.

- cashback on daily spend at McDonald's, Grab, SimplyGo & Shopee

- Up to 10%

- cashback at all grocery spend

- Up to 8%

- cashback cap a year

- Up to S$2,240

Get a SURE-WIN S$30 Cash for New-To-UOB customers who apply and make just one eligible transaction within 30 days from approval. T&Cs apply.

PLUS, enjoy highest cashback of up to 20% on daily spend! T&Cs apply.

If you prefer a card with $0 minimum spend, the recently revamped UOB Lady's Card is right up your alley. And yes, men can apply too!

- Base Earn Rate

- S$5 = 1X UNI$ (0.4 miles per S$1)

- Category of Choice

- S$5 = Up to 25X UNI$ (equivalent to 10 miles per S$1)

- Min. Spend

- S$0

Get a SURE-WIN S$30 Cash for New-To-UOB customers who apply and make just one eligible transaction within 30 days from approval. T&Cs apply.

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 3.40%

- Min. Balance

- S$1,000

UOB One savings account

- Minimum balance: $1,000

- Fall below fee: $5 (Waived for first 6 months for accounts opened online)

- Bonus interest cap: $100,000

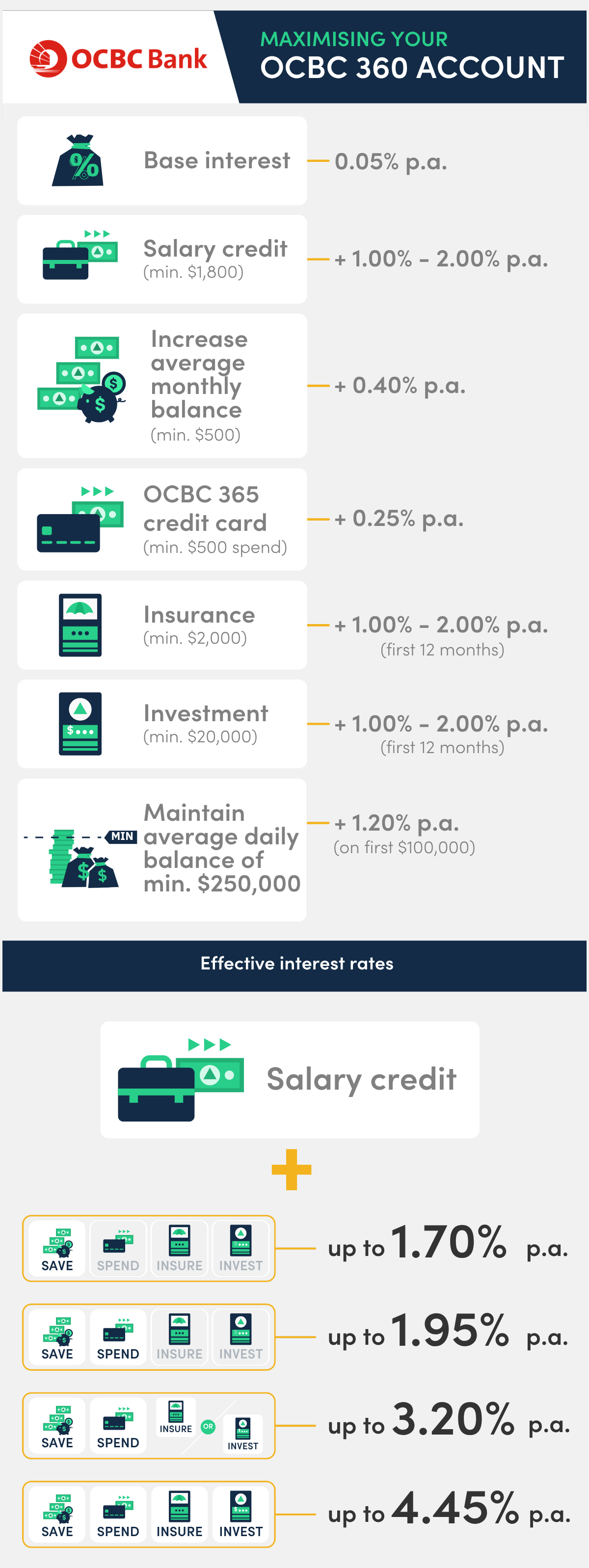

4. OCBC 360 savings account interest rates

Like Standard Chartered, the OCBC 360 savings account is getting nerfed from 1 May 2026. Here are the changes:

Transactions | Interest rate (first $75,000) | Interest rate (next $25,000) |

None (base interest) | 0.05% p.a. | 0.05% p.a. |

Salary credit (min. $1,800, GIRO/FAST/PayNow) |

|

|

Increase average monthly balance (min. $500) | + 0.40% p.a. |

|

Spend (min. $500 on selected OCBC credit cards) |

| |

Insure in selected products (min $2,000) |

|

|

Invest in selected products (min. $20,000) |

|

|

Maintain average daily balance of min. $250,000 |

| |

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 5.45%

- Min. Balance

- S$3,000

The OCBC 360 savings account starts at a base interest of 0.05% p.a. You get this on any amount you put in the account.

From there, the OCBC 360 savings account then gives you varying bonus rates for crediting your salary, spending on your credit card (minimum of $500/month), growing your balance, insuring and investing. You can mix and match the criteria you want to fulfil to unlock different interest rates. However, these bonus rates apply only to the first $100,000 in your account, and OCBC tiers the first $75,000 differently from the next $25,000 for several components.

Depending on the combination of criteria you fulfil, this is what your maximum Effective Interest Rate (EIR) will be on your first $100,000 from 1 May 2026:

Criteria met | Effective interest rate | Interest earned (on $100,000) |

|---|---|---|

Salary + Save | 1.70% p.a. | $1,700 |

Salary + Save + Spend | 1.95% p.a. | $1,950 |

Salary + Save + Spend + Insure or Invest | 3.20% p.a. | $3,200 |

Salary + Save + Spend + Insure + Invest | 4.45% p.a. | $4,450 |

Note: The Insure and Invest bonuses are capped at 12 months from each qualifying purchase, so the higher tiers above only apply for that window.

Realistically, most of us will likely only fulfil 3 criteria: Salary, Save, and Spend. Once you fulfil these 3 criteria, the maximum EIR you can enjoy is 1.95% p.a.

To recap, the OCBC 360's closest competitor, the UOB One account, currently gives you an EIR of 1.90% p.a., making the 2 pretty even. So, how do you decide between the 2?

OCBC 360 vs UOB One savings account

In absolute terms, you currently earn 0.05% more with the OCBC 360 one (1.95% p.a.) than the UOB One savings account (1.90% p.a.).

Other plus points in favour of OCBC 360 include:

- With the OCBC 360 account, there is no one mandatory requirement to hit. Mix and match as you please. The UOB One account requires that you spend on a UOB credit card as a baseline enjoy its bonus interest rates.

- With the OCBC 360 account, you earn bonus interest for crediting your salary through GIRO, FAST, or PayNow. With the UOB One account, it only counts if you credit your salary via GIRO.

You might notice that UOB One's 1.90% p.a. applies to the first $150,000, whereas OCBC 360's 2.45% applies to the first $100,000. If you have $125,000, which account is better?

Here’s a breakdown based on current structures:

Deposit balance | UOB One Account | OCBC 360 Account | Winner (higher interest) |

|---|---|---|---|

$75,000 | $750.00 | $1,275.00 | OCBC 360 (by $525) |

$100,000 | $1,375.00 | $1,950.00 | OCBC 360 (by $575) |

$125,000 | $2,000.00 | $1,962.50 | UOB One (by $37.50) |

$150,000 | $2,850.00 | $1,975.00 | UOB One (by $875) |

Calculations are based on annualised rates, before compounding.

In summary:

- At smaller balances (up to ~$100,000): OCBC 360 comes out ahead, with bonus rates of 1.70% on the first $75,000 and 2.70% on the next $25,000—well above UOB's 1.00% first tier.

- At $125,000 and above: UOB One pulls ahead, thanks to its juicier tranche rates of 2.50% on the next $50,000 and 3.40% on the next $25,000, compared with OCBC's drop-off to 0.05% on anything above $100,000.

- Ease of qualifying: UOB's requirements (salary credit via GIRO + $500 card spend) remain simpler than OCBC's multi-category conditions.

If you typically keep $125,000 or more in savings and can meet UOB's salary credit + card spend criteria, UOB One gives you the higher overall return. Otherwise, OCBC 360 is the better bet for smaller balances or if you're already crediting your salary there.

Recommended cards for the OCBC 360 savings account

The bonus 0.25% p.a. interest for credit card spending is an easy one to hit, but do note that the $500 monthly spend applies only to selected OCBC credit cards:

- OCBC 365 Credit Card

- OCBC INFINITY Cashback Card

- OCBC NXT Credit Card

- OCBC 90°N (available in both Visa and Mastercard versions)

- OCBC Rewards Card

My top pick is the OCBC 365 Credit Card for its high cashback rates, subject to a minimum monthly spend of $800:

- 5% cashback on everyday dining (including local, overseas and online food delivery)

- 6% cashback on fuel spend at all petrol service stations locally and overseas

- 3% cashback on groceries, land transport, online travel, recurring telco and electricity bills

- Cashback on Fuel Spends

- 6%

- Cashback on Everyday Dining

- 5%

- with min. spend of $1,600 per month

- Unlock up to $160 Cashback

Get $250 Cash or 3,900 SmartPoints (enough to redeem an Apple AirPods Pro 3 worth S$349) when you apply and spend a min. of S$400 within 30 days! T&Cs apply.

But if you've jumped through enough hoops for your savings account and just want a blanket 1.6% cashback rate from your credit card, the OCBC INFINITY Cashback Card is a better fit.

- on eligible transactions

- Earn 1.6% Cashback

- Min. Spend

- S$0

- Cashback Cap

- Unlimited

Get $250 Cash or 3,900 SmartPoints (enough to redeem an Apple AirPods Pro 3 worth S$349) when you apply and spend a min. of S$400 within 30 days! T&Cs apply.

OCBC 360

- Minimum balance: $1,000

- Fall below fee: $2. Waived for first year.

- Bonus interest cap: $100,000

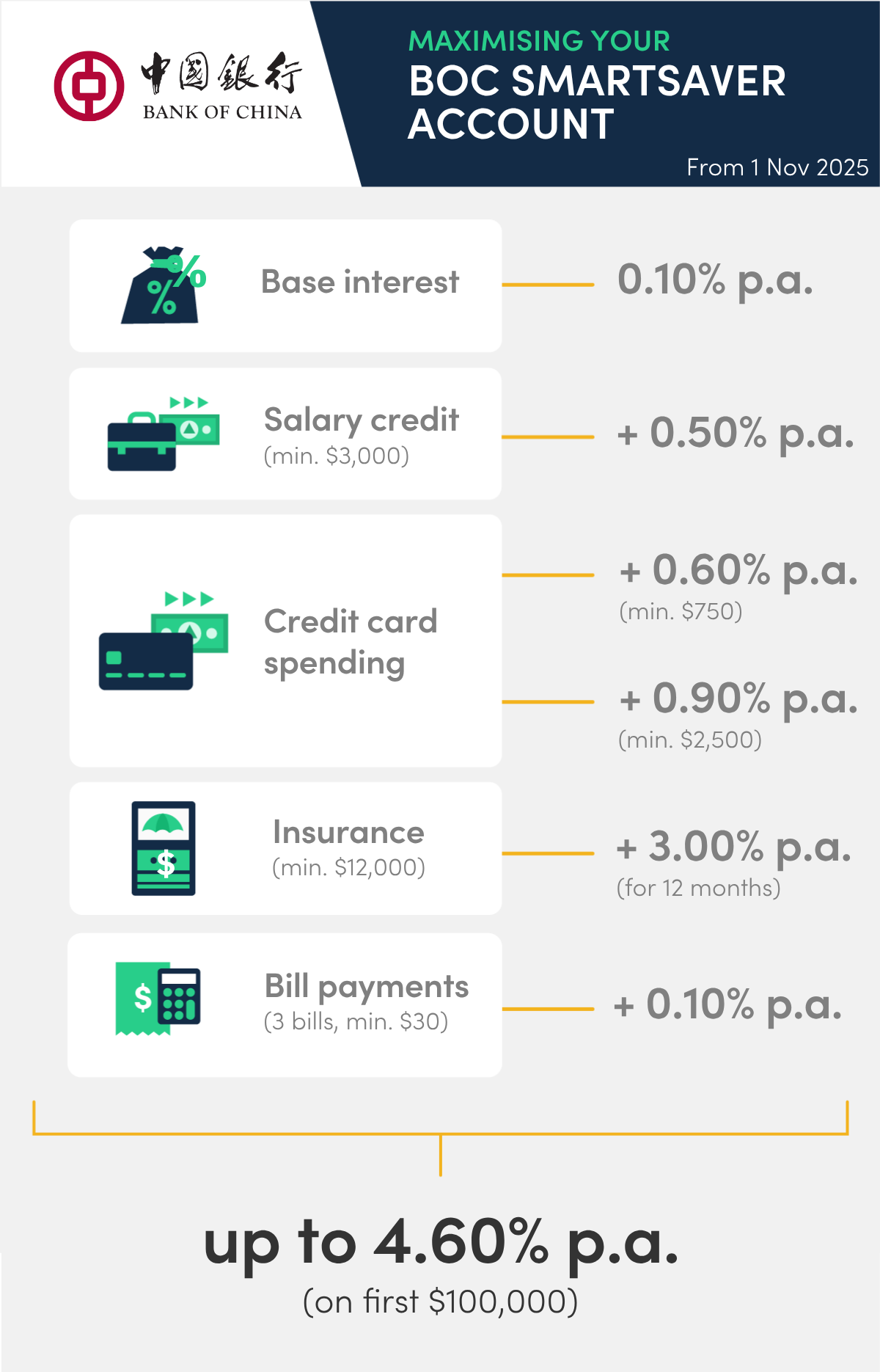

5. Bank of China SmartSaver account interest rates

Transactions | Interest rate |

None (base interest) |

|

Insurance plan spending | + 3.00% p.a. for 12 consecutive months |

Salary credit (minimum $2,000 before 1 Nov 2025, increased to $3,000 from 1 Nov 2025) | + |

Credit card spending | + |

3x bill payments of at least $30 each (GIRO or internet/mobile banking) | 0.1% p.a. |

(For account balance above $100,000) Extra bonus interest when you fulfil any one of the requirements for Card Spend, Salary Crediting or Payment bonus interest |

|

Source: Bank of China

With the Bank of China SmartSaver account, you now get 0.60% p.a. just for opening the account and crediting your salary to it.

The Bank of China SmartSaver account also awards a wealth bonus of 3.00% per annum for 12 consecutive months. However, to qualify, you’ll have to put down a pretty hefty sum on their insurance products. These are your options:

- $12,000 in annual premiums with a 10-year premium term

- $24,000 in annual premiums with a 5-year premium term

- $150,000 Single Premium Insurance Plan

If you max out the bonus interest in all categories, you can currently enjoy a rate of up to 5.35% p.a. on your first $100,000 saved with the Bank of China. After the 1 Nov 2025 nerf, the maximum interest rate on your first $100,000 will drop to 4.60% p.a.

On the other hand, let's say you only credit your salary and spend ($750 a month). You'll earn an interest rate of 0.1% (base) + 0.50% (salary) + 0.60% (credit card) = 1.20% p.a. on your first $100,000. You're better off with OCBC 360 or UOB One.

Bank of China SmartSaver

- Minimum balance: $200 (Maintain at least $1,500 to enjoy bonus interests)

- Fall below fee: $3

- Bonus interest cap: $100,000

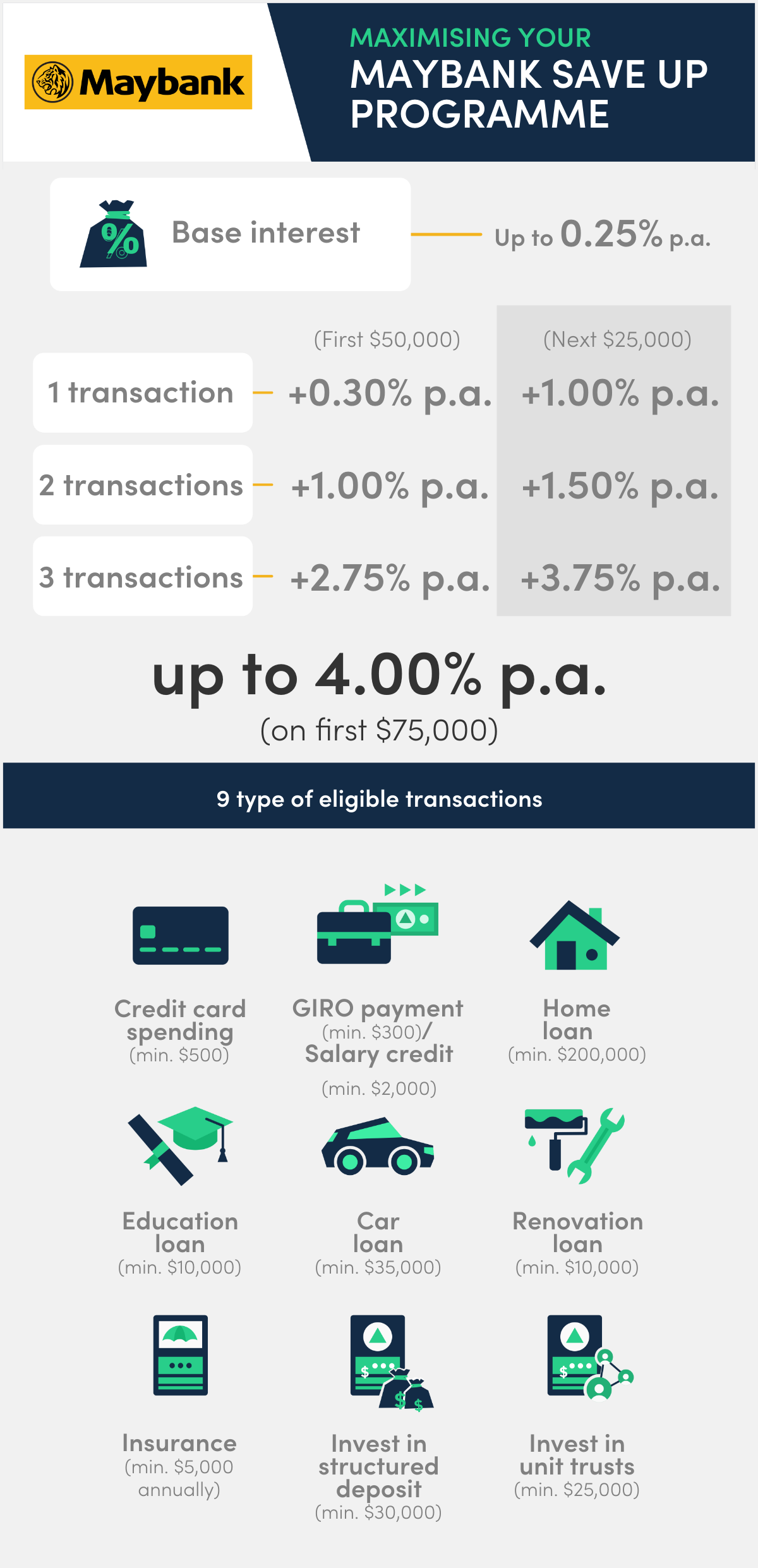

6. Maybank Save Up Programme interest rates

Interest rates | |||

Transactions | First $50,000 | Next $25,000 | Maximum Effective Interest Rate |

None (base interest) | Up to 0.25% p.a. | Up to 0.25% p.a. | |

1 x transaction | + 0.30% p.a. | + 1.00% p.a. | 0.53% p.a. (excludes base interest) |

2 x transactions | + 1.00% p.a. | + 1.50% p.a. | 1.17% p.a. (excludes base interest) |

3 x transactions | + 2.75% p.a. | + 3.75% p.a. | 3.08% p.a. (excludes base interest) |

Base interest

The Maybank Save Up Programme starts with a higher base interest rate than most other savings accounts... sorta. The base interest is actually tiered:

- First $3,000: 0.05% p.a.

- Next $47,000: 0.25% p.a.

- Remaining balance above $50,000: 0.25% p.a.

Your base interest's effective interest rates are hence:

- First $50,000: 0.238% p.a.

- First $75,000: 0.242% p.a.

- First $100,000: 0.244% p.a.

Bonus interest

Next, the Maybank Save Up Programme then lets you choose from 9 different Maybank products/services to get bonus interest:

- GIRO payment (min. $300) OR salary credit (min. $2,000)

- Credit card spending (min. $500) on Maybank Platinum Visa Card and/or Horizon Visa Signature Card

- Invest in structured deposit (min. $30,000)

- Invest in unit trust (min. $25,000)

- Buy insurance (min. $5,000 annually)

- Home loan (min. $200,000)

- Renovation loan (min. $10,000)

- Car loan (min. $35,000)

- Education loan (min. $10,000)

The bonus interest rates aren’t competitive unless you fulfil 3 transactions. Assuming you hit 3 transactions and start with a bonus interest rate of 0.25%, you’ll get an EIR of around 2.99% p.a. on your first $50,000 and 4.00% p.a. on the next $25,000. Together, you're looking at 3.33% p.a. EIR on the first $75,000, inclusive of base interest.

For comparison, the OCBC 360 account will give you an EIR of 2.45% p.a. on $100,000 for hitting 3 categories—crediting your salary, saving, and spending on your credit card. UOB One is handing out an EIR of 2.50% p.a. on the first $150,000 if you spend on a card and credit your salary via GIRO. These are lower rates but on a larger sum—and, for the UOB One account, simpler mechanics.

Speaking of credit card spending, do note that Maybank only considers credit card spending on the Maybank Platinum Visa Card and Horizon Visa Signature Card. Spending on other Maybank credit cards doesn't count. On the plus side, these cards give you good cash rebates both locally and overseas.

(1) (1).jpg)

- Cashback on Local & Foreign Spend

- Up to 3.33%

- Min. Spend per month

- S$300

- Cashback Cap per quarter when you spend S$300 per month

- S$30

- on Air Tickets and Foreign Currency Spend

- S$1 = 7X Points

- on local Shopping, Groceries, Dining, Hotel Bookings

- S$1 = 3X Points

- Rewards to Miles Conversion for Selected Airline Partners

- 1 Point = 0.4 Miles

Maybank Save Up Programme

- Minimum balance: $1,000

- Fall below fee: $2. Waived for individuals below age 25.

- Bonus interest cap: $50,000

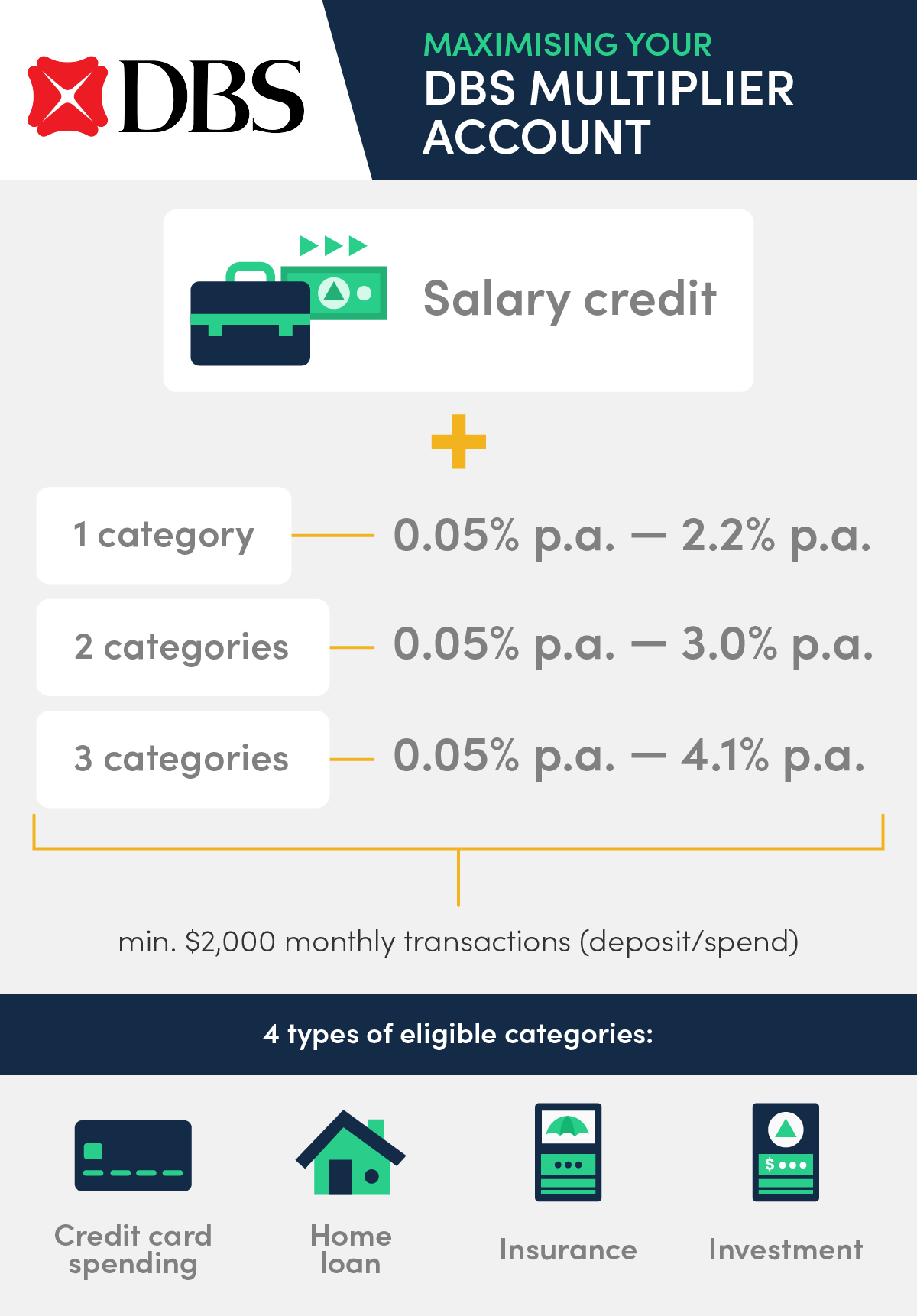

7. DBS Multiplier savings account interest rates

The DBS Multiplier account's interest rates are only competitive if you hit 3 categories across credit card spending, home loan, insurance, and investment.

Total monthly transactions | Income + 1 category | Income + 2 categories | Income + 3 categories |

First $50,000 | First $100,000 | First $100,000 | |

$500 to $14,999 | 1.80% | 2.10% | 2.40% |

$15,000 to $29,999 | 1.90% | 2.20% | 2.50% |

$30,000 and up | 2.20% | 3.00% | 4.10% |

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 4.10%

- Min. Balance

- S$3,000

The rates in the table above apply to you if you credit your salary/dividends/SGFinDex to any DBS or POSB account (yes, it doesn’t need to be your DBS Multiplier account!). You need to have at least $500 worth of transactions from 1 or more of the following categories:

- Credit card or PayLah spending (no minimum)

- Home loan (cash + CPF components counted)

- Selected insurance policies (life insurance, critical illness, endowment plans and selected single premium policies)

- Selected investments (regular savings plan, unit trust, online equities trade, digiPortfolio or bonds, and structured products)

The more categories you hit, the higher bonus interest rates you get.

One thing I really like about the DBS Multiplier is that there is no minimum amount required for the credit card or DBS PayLah! spend. You can also choose either, although I would recommend the credit card route for extra cashback or miles. You can earn up to 10 miles per dollar with the DBS Altitude Visa Signature Card on your travel spend at Expedia and Kaligo, and 2.2 miles per dollar on other overseas spend.

- Local Spend

- S$1 = 1.3 miles

- Overseas Spend (made in foreign currency)

- S$1 = Up to 2.2 miles

- on DBS Points earned

- No Expiry

The DBS Vantage Visa Infinite Card comes with an even bigger welcome miles bonus, although it isn't the most accessible credit card due to its high minimum income requirement.

AA.png)

- Local Spend

- S$1 = 1.5 miles or 1.5% cashback

- Overseas Spend

- S$1 = 2.2 miles or 2.2% cashback

- when you pay the Card's Annual Fee

- 25,000 Bonus Miles

What if you don’t have any DBS credit card, insurance, or investments? If you're 29 years old or below, you can still earn 1.5% p.a. on the first $50,000. You don't need to credit your salary to a DBS/POSB account, but DBS will still require you to at least use PayLah!. The good news is that there isn’t a minimum amount for PayLah! spend. Just use it to pay for anything, even if it’s a $1+ cup of kopi at your local coffeeshop. Easy!

Overall, the DBS Multiplier account makes it easy to earn bonus interest with its zero minimum spend transaction categories and the flexibility to credit your salary into any DBS account, not necessarily the DBS Multiplier.

However, DBS Multiplier account interest rates start pretty low, especially if you don’t credit your salary to a DBS/POSB account. Comparatively, CIMB FastSaver’s interest rates start at 1.50% p.a. for just opening the account and depositing a minimum of $1,000.

DBS Multiplier

- Minimum balance: $3,000

- Fall below fee: $5. Waived for first-time customers & those up to age 29.

- Bonus interest cap: $100,000

8. CIMB FastSaver savings account interest rates

The CIMB FastSaver account stands out because of its lack of insurance and investment components to access higher interest rates. It does have the usual suspects—salary and credit card spend requirements. With these, you get to unlock the highest interest rate (currently 2.30% p.a.) on the first $25,000.

After you meet those requirements for the initial $25,000 balance, you can enjoy up to 1.58% p.a. Yup, no conditions to buy insurance, sign up for an investment, or any other hoops to jump through.

Account balance | Prevailing interest rate | Bonus interest (Top up your account by at least $10,000) | Additional interest (credit salary or schedule a recurring GIRO transfer of at least $1,000) | Additional interest (spend on CIMB Visa Signature Credit Card) | Total interest rate |

First $25,000 | 0.50% p.a. | 0.30% p.a. (Personal Banking) / 0.40% p.a. (Preferred Banking) | + 0.50% p.a. | + 1.00% (min. $800 monthly eligible spend) | 2.30% |

Next $25,000 | 1.08% p.a. | 0.30% p.a. (Personal Banking) / 0.40% p.a. (Preferred Banking) | – | – | 1.38% p.a. |

Next $25,000 | 1.58% p.a. | 0.30% p.a. (Personal Banking) / 0.40% p.a. (Preferred Banking) | – | – | 1.88% p.a. |

Above $75,000 | 0.50% p.a. | 0.30% p.a. (Personal Banking) / 0.40% p.a. (Preferred Banking) | – | – | 0.80% p.a. |

If we assume you hit the requirements to earn 2.30% on your first $25,000, your effective interest rates are:

Balance | EIR |

|---|---|

First $25,000 | 2.30% p.a. |

First $50,000 | 1.84% p.a. |

First $75,000 | 1.85% p.a. |

First $100,000 | 1.59% p.a. |

If you only have $25,000 to park in a savings account, CIMB FastSaver is a good choice. You're not going to get rates like this on such small amounts with other savings accounts, where the highest rates are unlocked at higher balances only.

This account is also perfect for most young adults starting out their career, because of the very low minimum balance of $1,000 and no fall below fee.

CIMB FastSaver

- Minimum balance: $1,000

- Fall below fee: None!

- Bonus interest cap: $75,000

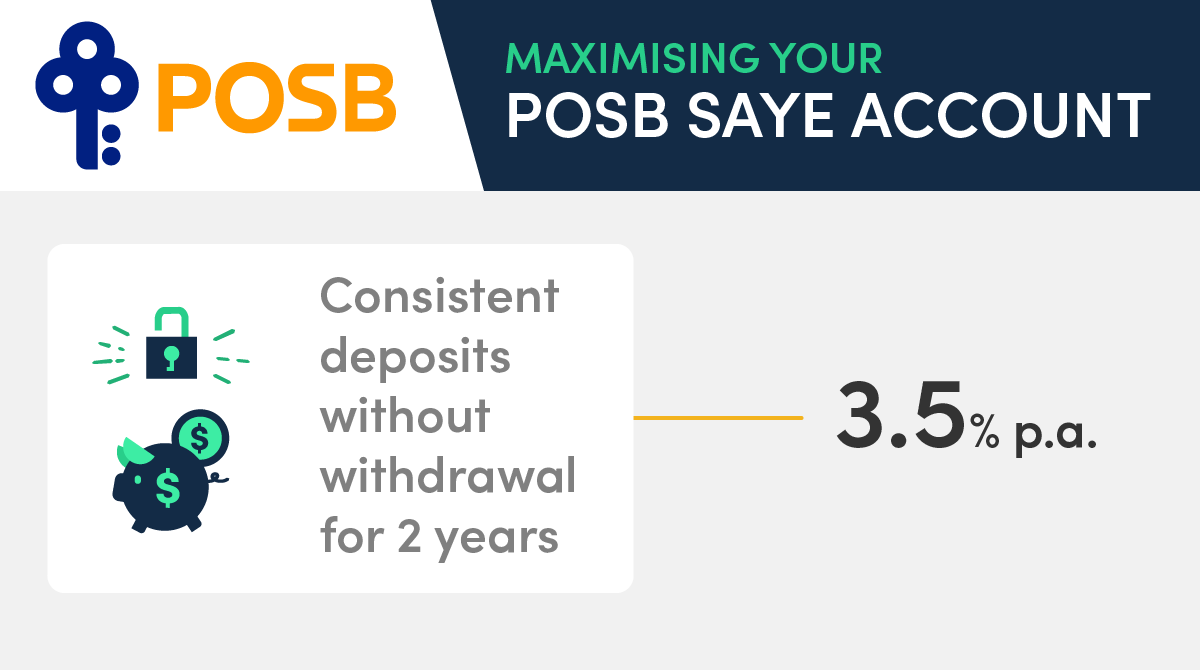

9. POSB SAYE savings account interest rates

What if you want to open a savings account, but don’t want to do anything but credit money into it? The best zero-effort contender is the POSB SAYE (Save As You Earn) account.

You need to set up a standing order to credit a fixed amount every month (anything from $50 to $3,000) into your SAYE account, then resist the urge to touch it for 2 years. As a reward for your restraint, you earn 3.5% p.a.

Note that it’s a whole lot less liquid than any other savings account, so for the love of God, please don’t put your emergency stash in here.

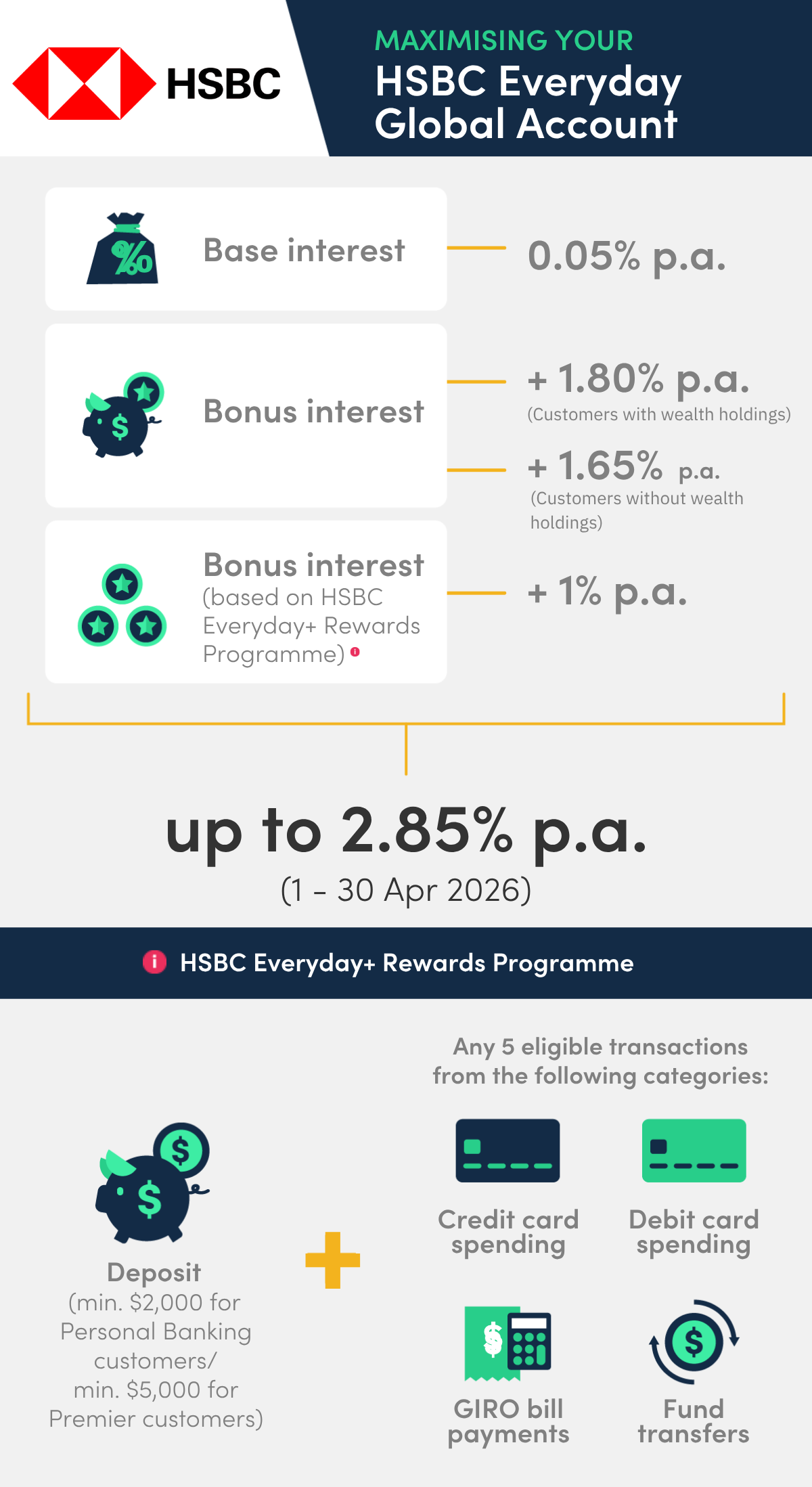

10. HSBC Everyday Global Account

- Min. Annual Interest

- 0.05%

- Max. Annual Interest

- Up to 1.05%

- Min. Initial Deposit

- S$2,000

Our last savings account on this list is the most headache-inducing. The HSBC Everyday Global Account is a multi-currency account that also doubles up as a savings account...masquerading as an interest/cashback-earning hybrid. Yikes. Let me explain.

The HSBC Everyday Global Account lets you transact in 11 different currencies, but that's probably not the reason why you're reading this article. More importantly for our purposes today, it also functions as a savings account.

Unlike the others on this list, the HSBC Everyday Global Account doesn't stack bonus interest the more you spend/save/borrow/invest/insure. Instead, the account works hand in hand with the HSBC Everyday+ Rewards Programme to, collectively between the account and the programme, earn you an extra 1% bonus interest and 1% cashback per year.

HSBC Everyday Global Account: How much interest can I earn?

When you have an HSBC Everyday Global Account and also qualify for the HSBC Everyday+ Rewards Programme, you can earn up to 2.85% p.a. in the promotion ongoing from now to 30 Apr 2026:

- 0.05% p.a., the Everyday Global Account's prevailing interest rate

- Up to 1.80% p.a. Everyday Global Account Bonus Interest for customers with wealth holdings (e.g. Unit Trusts, Equities, Bonds, Structured Products, Regular Premium insurance policies and Single Premium insurance policies) OR 1.65% p.a. for customers without wealth holdings

- 1.00% p.a. when you qualify for the HSBC Everyday+ Rewards Programme

Combined, these bring your total interest to 2.85% p.a. if you have wealth holdings or 2.70% p.a. if you don't.

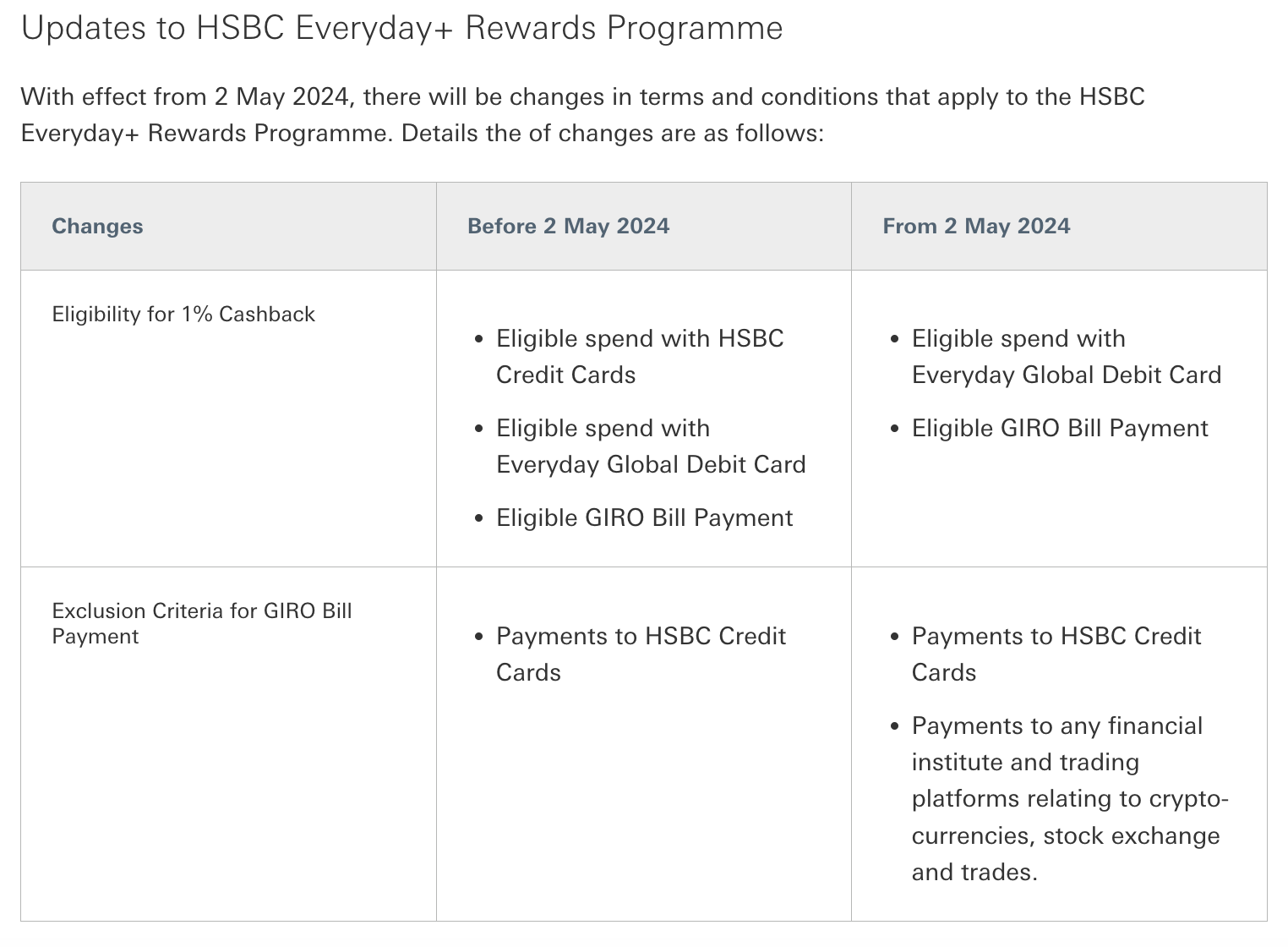

How do I qualify for the HSBC Everyday+ Rewards Programme?

The third component above (1% additional interest) comes from qualifying for the HSBC Everyday+ Rewards Programme. Here are the requirements:

- Deposit at least $2,000 (for Personal Banking customers) or $5,000 (for Premier customers) into the account

- Make 5 eligible transactions, with no minimum amount. These can be any combination of the following types:

- Transactions made with a HSBC personal credit card*

- Transactions made with a HSBC Everyday Global Debit Card

- GIRO bill payments

- Fund transfers to a non-HSBC account

What do I earn from the HSBC Everyday+ Rewards Programme?

Qualifying for the Everyday+ Rewards Programme gets you:

- 1% bonus interest (as we talked about) on the money you top up into your account each month (capped at $300/month)

- 1% cashback on your HSBC Everyday Global Debit Card transactions and GIRO bill payments (capped at $300/month for Personal Banking customers, $500/month for HSBC Premier customers)

* Note that you can use an HSBC credit card to qualify for the HSBC Everyday+ Rewards Programme, but credit card spending won't earn you cashback once you qualify the programme. The 1% cashback you receive is pegged to your spending on your HSBC Everyday Global Debit Card, not your credit card.

This change was implemented by HSBC on 2 May 2024 and is also spelled out in their updated terms and conditions.

Image: HSBC

On the plus side, HSBC doesn't limit you to a select few credit cards for the credit card spending criteria, so take your pick of the HSBC credit cards available. My personal pick is the HSBC Live+ Credit Card, with which you can earn up to 8% cashback (for a limited time) on this card on selected dining, shopping, and entertainment spending.

- on Dining, Shopping and Entertainment

- 8% Cashback*

- on fuel at Caltex and Shell gas stations in Singapore

- 5% Cashback*

- on All Other Spends

- 0.3% Cashback*

Get S$400 Cash or 6,140 SmartPoints (worth up to S$499 of Gifts) when you spend S$500 from Card Account Opening Date to end of the following calendar month!

PLUS, win a S$15,000 Dream Holiday to your preferred destination! T&Cs apply.

On top of the interest and cashback, HSBC will give you one-time cash bonuses of up to $150 (for Personal banking customers) / $300 (Premier customers) when you deposit at least $100,000 (Personal banking) / $200,000 (Premier Banking) and meets the eligibility criteria above for the first 6 months.

How to register for the HSBC Everyday+ Rewards Programme

To register, send an SMS to 74722 with the following format:

EGA<Space>first 9-digit of your Everyday Global Account number (e.g. EGA 123456789)

Drawbacks and pitfalls of savings accounts in Singapore

Before you sign up, be aware of these common savings account pitfalls:

- Bonus interest is easy to lose: Miss a requirement for even one month—like salary credit or card spend—and your rate can drop to the base level.

- Monthly and hidden fees: Many accounts charge fall-below fees, service fees, or penalties if you don’t meet conditions. Always check the fine print.

- Account fit: Irregular income? No plans for a bank credit card? Avoid accounts that require strict salary credits or card spend to earn higher rates.

- Easy mistakes: Using the wrong transfer method or missing a cut-off date can cost you bonus interest. Some banks also require you to opt in for promos.

- Changing rates: Interest rates and requirements can change at any time—today’s top account may not stay competitive for long.

Double-check requirements before committing, and review your account regularly to avoid surprises.

Savings account alternatives in Singapore

If you’re open to earning more or diversifying beyond traditional savings accounts, here are some alternatives worth considering:

Fixed deposits

If you can lock in your money for a few months, short-term fixed deposits (FDs) sometimes offer higher guaranteed rates than savings accounts. Just check the minimum deposit and early withdrawal penalties.

ALSO READ: Best Fixed Deposit Rates in Singapore (Apr 2026)

Digital banks

Digital-only banks such as Trust, GXS, and MariBank offer fuss-free accounts, often with high base rates, no minimum balance, and zero fees. Their rates and features can change quickly, so compare them regularly with traditional options.

Singapore Savings Bonds (SSBs)

SSBs are government-backed, low-risk investments that pay out interest every six months and let you withdraw your money at any time without penalty. They’re ideal for those seeking both safety and flexibility, though returns fluctuate based on prevailing interest rates.

Treasury bills (T-bills)

T-bills are short-term government securities with tenures of 6 or 12 months. They typically offer higher yields than regular savings accounts, but your funds are locked in until maturity. They’re a good fit if you want a guaranteed return over a fixed period.

Money market funds and cash management accounts:

Platforms like Endowus, StashAway, Syfe Cash+, and others invest your cash in diversified, low-risk funds that can yield more than most savings accounts. While returns aren’t guaranteed, your money remains accessible in cash management accounts.

Each of these options has its own pros, cons, and risks, so weigh them carefully alongside your savings needs. For many, a mix of accounts can help balance flexibility, safety, and higher returns.

We've also reviewed the Best Banking Accounts in HK. Check them out!

You may also check the Best Savings Account with Debit Cards in 2026. Read more.

Know someone who needs to switch their savings account? Share this article with them!

Related Articles