This post was written in collaboration with NTUC Income. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best recommendations and advice in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

CareShield Life, our government’s new national long-term care insurance scheme, was launched on 1 October 2020.

This is not to be confused with ElderShield, by the way.

Some differences between CareShield Life and ElderShield:

CareShield Life | ElderShield | |

Age eligible | From 30 years old | From 40 years old |

Payout amount | From $612/month in 2021 (increases annually until age 67 or when a claim is made) | Up to $400/month |

Payout duration | Lifetime | Up to 72 months per lifetime |

Criteria | Unable to perform 3 out of 6 Activities of Daily Living (ADLs) | |

*Note: Those on ElderShield may have the option to switch to CareShield Life from 2021, but will need to pay higher premiums

Most importantly, CareShield Life provides universal long-term care coverage for all Singapore Residents (Singaporean Citizens and Permanent Residents) born in 1980 or later, including those with pre-existing medical conditions and disability.

According to the Ministry of Health: “1 in 2 healthy Singaporeans aged 65 could become severely disabled in their lifetime, and may need long-term care. Severe disability may arise due to a sudden disabling event (e.g. stroke and spinal cord injuries), the worsening of chronic conditions and diseases (e.g. diabetes), or the progression of illnesses as we age (e.g. dementia).” (Source)

The cost of long-term care is no joke also. According to the Agency for Integrated Care, the basic cost of staying in a nursing home varies between $2,000 and $3,600 a month (before MOH subsidy), depending on the level of care required. (Source)

Even if you’re single and wealthy, being severely disabled (unable to perform 3 out of 6 ADLs) would likely mean that you’re unable to earn a salary and will need to enroll in a nursing home or employ a live-in caregiver. We’re not even counting the medical supplies, equipment (bed, wheelchair, walker, etc) and daily expenses. The payout of $612/month (as of 2021) provided by CareShield Life alone may not be enough to fully cover all these expenses.

Related article: How Does CareShield Life Help Singaporeans?

And what happens if due to an accident or an illness (sudden or chronic — the latter likely brought about due to lifestyle risk factors such as stress, obesity, an unhealthy diet, sedentary lifestyle, smoking, etc — which may not always happen due to old age), a person is temporarily disabled and unable to work but not to the extent of being unable to perform 3 ADLs? Jialat liao…

How CareShield Life supplements help

But that’s where CareShield Life supplements come into play — currently, there are only 3 private insurers in Singapore offering this, one of which is NTUC Income. These CareShield Life supplements help to close the gap by providing coverage from 2 ADLs and above, offering monthly payouts (yes, also for life) and other payments that can help your caregivers and even your dependants.

Let’s take a closer look at what additional benefits CareShield Life supplements may offer.

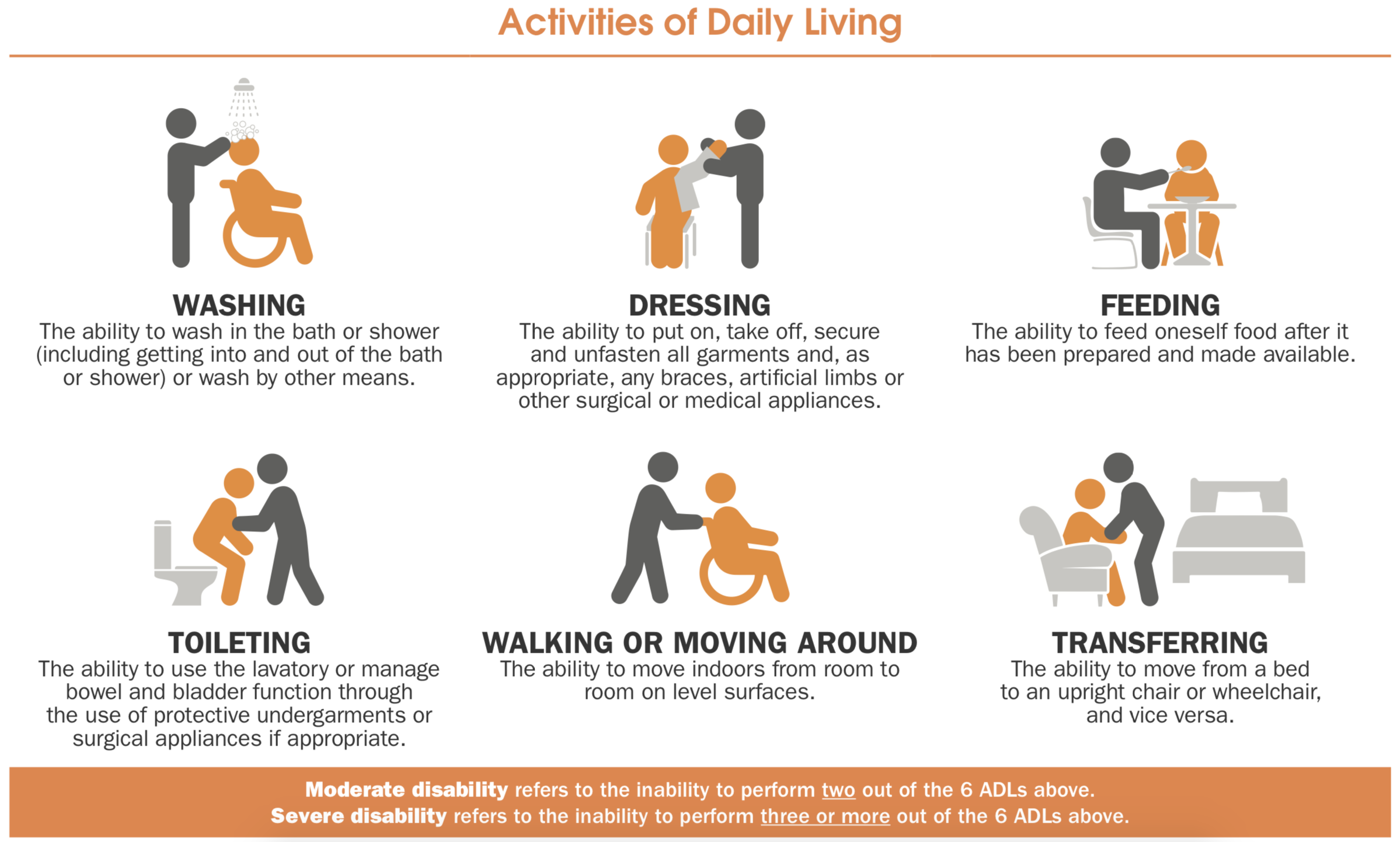

Coverage for 2 ADLs or more

Recap: The government’s basic CareShield Life will only kick in when a person is assessed by a MOH-accredited severe disability assessor to be unable to independently perform at least 3 out of 6 ADLs.

Here are the 6 ADLs for easy reference:

(Image source: Income)

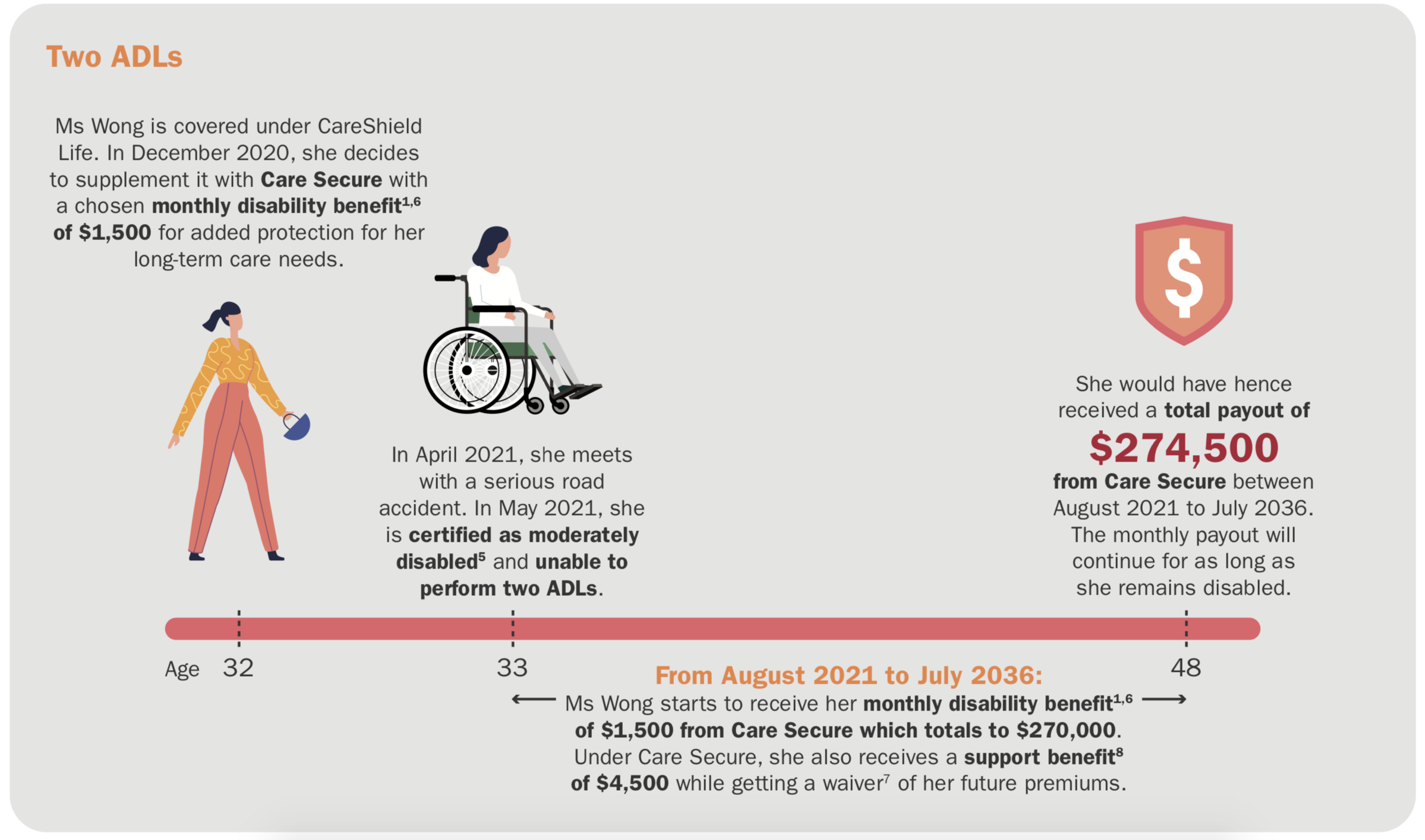

Income’s Care Secure (a CareShield Life supplement) closes the gap as it provides coverage for 2 ADLs or more. This means an individual will be covered from an earlier stage of disability (and we know every little bit of extra financial support helps, right?).

And who says this disability must be permanent? It could be temporary, and the more support/less stress one has, the quicker the recovery might be, right?

Depending on the level of your CareShield Life supplement plan, the monthly disability payout could be as high as $5,000 (for Income’s Care Secure).

Support benefit

Look for a CareShield Life supplement that has a support benefit, sometimes termed a lump sum benefit.

This could greatly aid the insured person, who might need financial help coping with their new situation, getting medical supplies/equipment, rehabilitation, etc.

Income’s Care Secure provides support benefit that pays up to 600% of the disability benefit in a lump sum.

- Unable to perform 2 ADLs: 300% of disability benefit

- Unable to perform 3 ADLs: 600% of disability benefit

If someone is covered by Care Secure, they could receive up to $30,000 as the support benefit payout if they went for the maximum amount of coverage and were unable to perform 3 or more ADLs (up to $5,000 disability benefit/month). Even if they opted for the minimum of $1,200/month disability benefit, that’s still a high amount of $7,200.

Dependant benefit

And what if the insured has young children, a spouse or aged parents who are depending on him/her? It’s even more difficult if the insured is the sole breadwinner.

Income’s Care Secure pays 25% of the disability benefit as the dependant benefit every month for up to 36 months in the insured’s lifetime.

This additional money of up to $1,250/month (if the insured got the maximum of $5,000 disability benefit/month) could greatly help with a kid’s school fees, household maintenance fees, groceries and so on.

That’s helpful, because disability and caregiving not only impacts the affected individual, but those around him/her as well.

Premium rates

In a perfect world, it would be nice to pay nothing and be guaranteed the $5,000/month payout for life should something happen to us. But there’s no free lunch, so we need to weigh our options, do our sums, work out our budget and choose the best plan for our needs.

The good news — you can use up to $600/year from our MediSave to pay for the CareShield Life supplement.

For a 35-year-old, non-smoker, paying up to 67 Age Last Birthday:

Income’s Care Secure

|

*The premium rate is based on the insured’s entry age at last birthday and is non-guaranteed.

As the annual sample premium is less than $600/year, the full amount will be covered by MediSave (you’ll of course need to have sufficient funds in your MediSave).

Here’s how Income’s Care Secure can provide early support for your long-term care needs if you are not able to perform 2 ADLs (p.s. CareShield Life covers you starting from 3 ADLs).

(Source)

*The figures used are for illustrative purposes only and assumes that the payout is not limited or excluded by policy terms and conditions; please also refer to footnotes 1, 5, 6, 7, 8 in Care Secure’s brochurehere.

Other benefits to look out for

Do check all the other benefits/coverage of your CareShield Life supplement, such as:

Premium waiver

What are the terms and conditions, when does it kick in, etc? For example, the premium waiver for Income’s Care Secure kicks in when the insured is unable to perform 2 ADLs and above.

Death benefit

There is also a death benefit available. In the event of the insured’s death, 300% of the disability benefit is paid out on the condition that the insured was already receiving the disability benefit.

Get the financial support for early treatment to avoid/slow down disability deterioration and possibility of making a full recovery. Remember, the government allows you to use up to $600/year of your MediSave for CareShield Life supplements, so why not use it?

Find out more about Income’s Care Secure here.

Important Notes

All opinions expressed in this article are solely those of MoneySmart and do not reflect the opinions of NTUC Income Insurance Co-operative Limited (“Income”). Income is not responsible nor liable to any party in any manner whatsoever for such opinions, and MoneySmart is solely responsible for any opinion and the accuracy and completeness of any information and intellectual property used in this article. The information contained in this article are provided and meant for general information only and do not constitute an offer, recommendation, solicitation or advice by Income or MoneySmart to buy or sell any product(s) or investment product(s). It is not and should not be relied as a financial advice and has no regards to any person’s investment and financial needs. If you are unsure whether this plan is suitable for you, you may seek personalised financial advice from a qualified insurance advisor. Otherwise, you may end up buying a plan that does not meet your expectations or needs. As a result, you may not be able to afford the premiums or get the insurance protection you want. Precise terms, conditions and exclusions of product are found in the policy contract.

For customised advice to suit your specific needs, consult an Income insurance advisor.

Protected up to specified limits by SDIC (applicable for Income products that fall under the Policy Owners’ Protection Scheme).

Information is correct as at 6 May 2021.

Related Articles