If you’ve already maxed out your UOB One savings account, congratulations—you’ve likely made the most of its high-interest tier. But now what? With interest capped for balances above $150,000 and UOB’s recent rate cuts, any additional savings could end up sitting idle.

Many Singaporeans in the same boat are wondering: what’s the next low-risk, low-effort step?

Redditors recently weighed in on this very question, offering a variety of suggestions from safe, MAS-backed options like SSBs and T-bills to digital platforms and even gold or ETFs. We reviewed the best of their ideas and ranked the options from lowest to highest risk.

Whether you’re looking for guaranteed returns or exploring ways to grow your money modestly, this guide helps you choose your next move after UOB One.

8 investment options after you’ve maxed out UOB One

- CPF top-ups

- Singapore Savings Bonds (SSBs) and T-bills

- Mari Invest (SavePlus and Income)

- High-interest savings accounts: OCBC 360, UOB Stash, and UOB Privilege

- Cash management accounts

- Money market funds (especially in foreign currencies)

- Physical gold or digital gold accounts

- Global ETFs with dollar-cost averaging

- Bonus: Non-interest alternatives still worth considering

- Conclusion

1. CPF top-ups

Image: Reddit

If you’re looking for one of the safest ways to grow your money, CPF top-ups are worth considering. Topping up your Special Account (SA) (if you're below 55) or Retirement Account (RA) (if you're 55 and above) helps you earn a stable 4% per annum, with bonus interest on the first $60,000 of your combined CPF balances. That’s a much higher rate than most savings accounts, and it's guaranteed by the government.

You can also consider topping up your MediSave Account, which earns the same 4% p.a. rate and helps you reach your Basic Healthcare Sum (BHS) for future medical expenses.

The key trade-off is that CPF top-ups are not liquid—you won’t be able to access the money until age 55 (or for specific uses like housing or healthcare). But if your short-term needs are covered, CPF offers risk-free, compounding growth.

Risk level: ★☆☆☆☆ (1/5)

Effort level: ★☆☆☆☆ (1/5)

ALSO READ: CPF Retirement Planning 2025: How to Maximise Your Retirement Income

2. Singapore Savings Bonds (SSBs) and T-bills

Image: Reddit

Image: Reddit

If you're after peace of mind and predictable returns, Singapore Savings Bonds (SSBs) and T-bills are 2 of the safest places to park your excess cash. Both are capital-guaranteed, meaning your principal is fully protected. You’ll never get back less than what you put in, regardless of market conditions, because both products are backed by the Singapore government.

Here’s a quick breakdown of how they differ:

- SSBs: Long-term, flexible savings bonds that allow early redemption without penalty.

- T-bills: Short-term government debt instruments with fixed returns and locked-in tenures.

Feature | SSBs | T-bills |

Tenure | Up to 10 years | 6 or 12 months |

Withdrawal flexibility | Redeem anytime | Locked until maturity |

Interest payout | Every 6 months | Paid upfront (discounted price) |

Current indicative rates | 2.29% p.a. (Jul 2025 SSB) | 1.79% p.a. (17 Jul 2025 T-bill) |

Minimum investment | $500 | $1,000 |

Capital guaranteed | Yes | Yes |

The current SSB and T-bill rates aren’t very high, but we were looking at rates of over 4% just 3 years ago.

You’ll need a CDP (Central Depository) account linked to your bank account to apply, which is why the effort level is slightly higher than something like CPF top-ups. But once that’s set up, buying and tracking your investments is fairly straightforward.

Risk level: ★☆☆☆☆ (1/5)

Effort level: ★★☆☆☆ (2/5)

3. Mari Invest (SavePlus and Income)

Image: Reddit

Mari Invest is MariBank’s investment platform offering 2 interest-earning products: Mari Invest SavePlus and Mari Invest Income. Both are easy to access, with no minimum lock-in, but they differ in risk and liquidity.

Mari Invest SavePlus

Mari Invest SavePlus is a low-risk, high-liquidity alternative to traditional savings accounts. You can start with just $1, withdraw funds instantly, and pay no transaction fees. It invests in the Lion-MariBank SavePlus fund, which delivered 3.16% (1-year return) and 3.33% annualised since launch (as at 31 May 2025, per MariBank). It’s ideal for parking cash you may need to tap into anytime.

Mari Invest Income

Mari Invest Income distributes the PIMCO GIS Income Fund Admin SGD Hedged – Inc, a global bond fund aiming for higher and more consistent payouts over the long term. However, this fund does not allow instant withdrawal, as it involves longer-duration bonds and market-linked risks.

Between the 2, Mari Invest SavePlus is lower risk, due to its money market-style portfolio and daily liquidity.

Risk level: ★★☆☆☆ (2/5) – Invest SavePlus is lower risk than Invest Income

Effort level: ★★☆☆☆ (2/5) — Easy to start; Income requires longer holding period

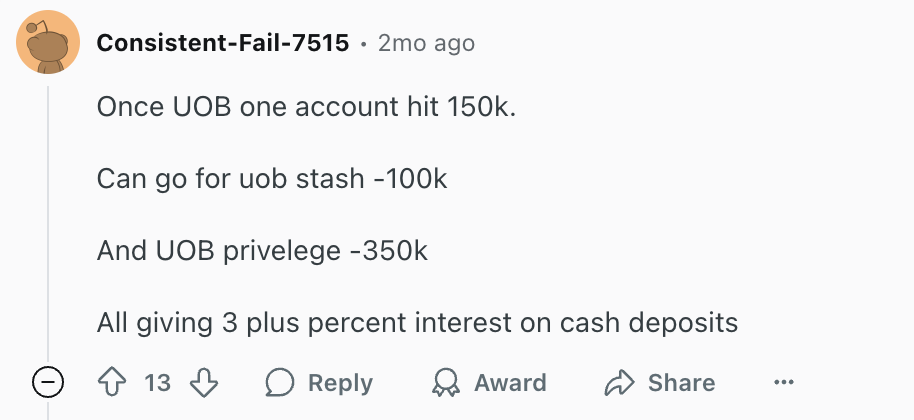

4. High-interest savings accounts: OCBC 360, UOB Stash, and UOB Privilege

Image: Reddit

Traditional high-interest savings accounts remain a popular option after maxing out UOB One—but not all are created equal. These accounts offer decent returns, but you’ll need to meet specific conditions like salary crediting, card spend, and consistent deposits to qualify for the top rates.

OCBC 360

Currently neck and neck with UOB One, OCBC 360 offers up to 3.30% p.a. on the first $100,000—provided you credit at least $1,800 in salary, spend $500/month on an OCBC card, and save $500/month. However, this is changing: from 1 Aug 2025, the effective interest rate will drop to 2.45% p.a., which significantly narrows its edge.

UOB Stash

UOB Stash uses a tiered interest system based on how much you save and whether your monthly average balance (MAB) grows or holds steady. On a $100,000 deposit, the maximum EIR is 2.04% p.a., assuming your balance increases or remains unchanged each month. While it doesn’t require card spending, it does demand consistent savings behaviour.

UOB Privilege

Designed for high-net-worth individuals, UOB Privilege only becomes relevant with deposits of at least $350,000. A current promotion offers up to 2.05% p.a. on fresh funds for 3 months (valid through Jul 2025), but longer-term rates may vary. You’ll likely need to negotiate better rates through a relationship manager.

Risk level: ★☆☆☆☆ (1/5)

Effort level: ★★★☆☆ (3/5) — Higher if you need to track criteria or qualify for promotions

5. Cash management accounts

Image: Reddit

If you're looking for a place to park your money with higher returns than a traditional savings account—without locking it up—a cash management account (CMA) could be the sweet spot.

A CMA is a type of low-risk investment account that puts your money into short-term, highly liquid instruments like money market funds, government bonds, or high-quality corporate debt. Unlike regular savings accounts, CMAs aren’t bank deposits and aren’t SDIC-insured, but they are managed by licensed financial institutions regulated by MAS.

Popular CMA platforms in Singapore include:

- Syfe Cash+ Flexi: Your money is invested in low-risk, high-liquidity funds, with projected net returns of 2.4%–2.5% p.a. (after all fees, as of 30 June 2025).

- Endowus Cash Smart: Offers a mix of conservative and balanced portfolios (Secure, Enhanced, Ultra), yielding ~2%–3.1% p.a.

- StashAway Simple Plus: A low-risk option with no minimum lock-in (although StashAway recommends parking your cash in there for at least 12 months) and a current yield to maturity of 3.1% p.a.

Withdrawals can take anywhere from 1 to 6 business days, but there’s no lock-in period.

Risk level: ★★☆☆☆ (2/5) – Underlying funds are low risk

Effort level: ★★☆☆☆ (2/5) — Easy to use, but not quite “set and forget”

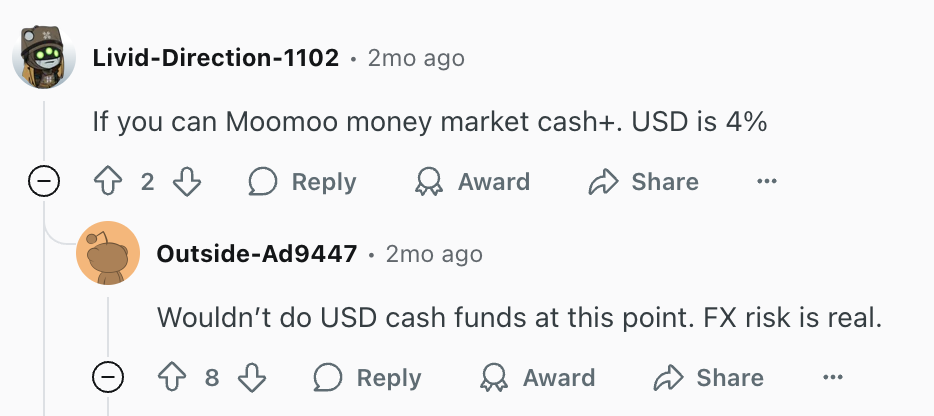

6. Money market funds (especially in foreign currencies)

Image: Reddit

Foreign currency money market funds (MMFs), especially USD-denominated ones, have become increasingly popular among yield-seeking savers. These funds invest in short-term, high-quality debt like US Treasury bills or commercial paper, and they often offer higher interest rates than SGD-based options, sometimes up to 4% p.a. or more, depending on market conditions.

But with higher returns comes foreign exchange (FX) risk. If the USD weakens against the SGD by the time you withdraw, any gains could be eroded or even reversed when converting back to SGD. These products are also not capital-guaranteed and not SDIC-insured, since they are classified as investment products.

Additionally, you’ll need access to a broker platform or a digital investment app to purchase these funds, which involves a bit more setup compared to standard savings products.

Pros of money market funds

- Higher returns – Especially compared to SGD MMFs or bank savings accounts

- Liquid – Usually redeemable within 1–3 business days

- Diversified holdings – Typically spread across multiple issuers and instruments

Cons of money market funds

- FX risk – Currency fluctuations may reduce or wipe out gains

- Not guaranteed and not SDIC-insured – Principal is exposed to market risks

- Requires broker setup – More effort than opening a bank account

Risk level: ★★★☆☆ (3/5) — FX volatility adds risk on top of market exposure

Effort level: ★★★☆☆ (3/5) — Requires brokerage access and understanding currency conversion

7. Physical gold or digital gold accounts

Image: Reddit

Gold is often viewed as a store of value rather than an income-generating asset. While it doesn’t earn interest, many investors use gold to hedge against inflation, economic instability, or market volatility.

In fact, on 22 Jul 2025, gold prices climbed to a 5-week high of $3,428.84 per ounce, driven by growing trade tensions and falling U.S. bond yields. When bond yields fall, non-yielding assets like gold become more attractive, especially in times of uncertainty. U.S. gold futures also jumped, reaching $3,443.70—signalling continued interest from institutional investors.

You can gain exposure through:

- Physical gold (e.g., bullion or jewellery)

- Digital gold platforms (which allow you to buy and store fractional gold)

- Gold ETFs or unit trusts

That said, gold prices can fluctuate sharply. It’s generally recommended to allocate only a small portion (think 5–10%) of your portfolio to gold as part of a broader diversification strategy, not as a main cash parking tool.

Risk level: ★★★☆☆ (3/5) — Prices can swing; no income generated

Effort level: ★★☆☆☆ (2/5) — Easy to buy digitally, but storage/logistics add effort for physical gold

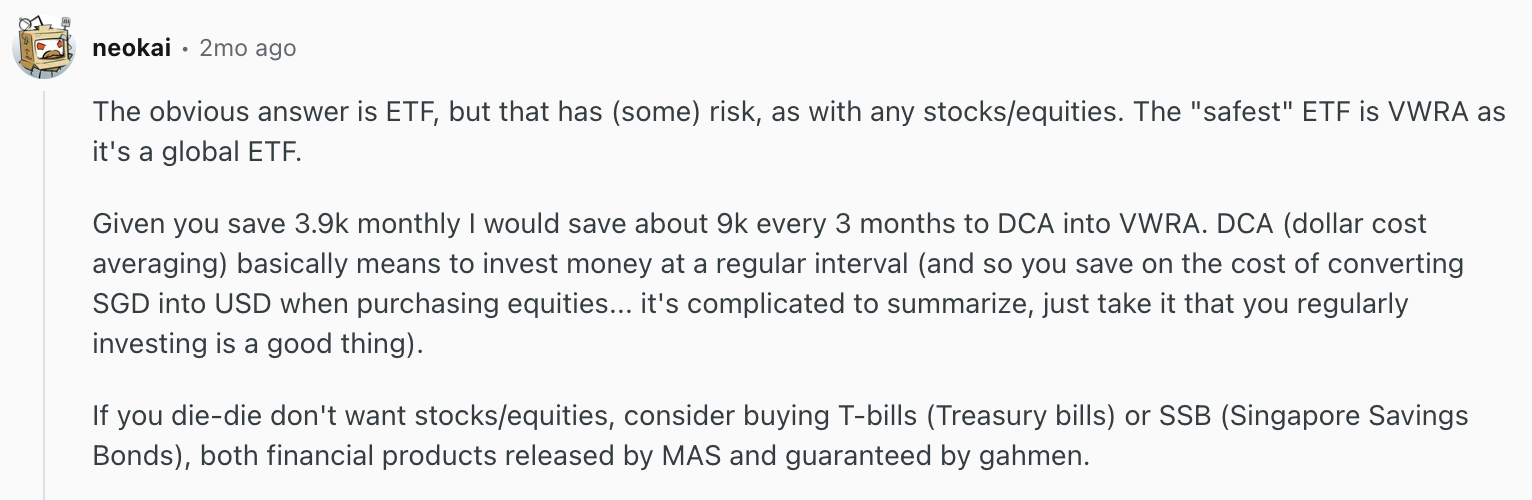

8. Global ETFs with dollar-cost averaging

Image: Reddit

The Redditor above recommended investing in a global ETF like VWRA—and while this route does involve more risk than cash-based products, it also offers higher long-term growth potential.

VWRA (Vanguard FTSE All-World UCITS ETF) gives you exposure to thousands of companies globally, including the US, Europe, and Asia. It’s often considered one of the more diversified and “safer” ETFs within the equity space because it spreads risk across markets and sectors.

The suggestion was to invest $9,000 every 3 months using a strategy called dollar-cost averaging (DCA). This simply means investing a fixed amount regularly instead of trying to time the market, helping smooth out price fluctuations over time.

However, investing in VWRA typically requires:

- A brokerage account

- Currency conversion from SGD to USD

- Comfort with market ups and downs

This strategy is better suited for investors with a long-term horizon, some tolerance for volatility, and money they don’t need immediate access to.

Risk level: ★★★★☆ (4/5) — Exposed to global market movements

Effort level: ★★★☆☆ (3/5) — Setup and currency conversions required

9. Bonus: Non-interest alternatives still worth considering

While not designed to grow your money, these 2 options suggested by Redditors are still worth a look for peace of mind and protection.

Locking your UOB balance (anti-scam feature)

Image: Reddit

UOB offers a Money Lock feature that allows you to protect your funds by preventing unauthorised transfers from your account. Even if your ATM card or banking credentials are compromised, the money can’t be moved unless you unlock it yourself at an ATM.

Best of all, your interest earnings aren’t affected, so you can leave your funds safely untouched while still earning your usual UOB One interest.

Insurance (life, critical illness)

If you haven’t already sorted out your insurance, this is a good time to plug the gaps. Insurance won’t grow your savings, but it can shield you from unexpected costs that would otherwise drain them. Look into term plans for coverage and separate endowment policies if you’re also aiming for stable, lower-risk returns.

Investment-linked policies (ILPs) are multi-layered and often come with a lot to unpack, from high fees to issues of transparency. Like any investment product, don’t sign up for one unless you have a full understanding of how they work and what they entail, and are prepared to navigate their complex structure.

10. Conclusion

Maxing out your UOB One account is a good problem to have. It means you’ve built up substantial savings and are now ready to make your money work a little harder. The good news? There’s no shortage of low-risk or moderate-effort options to grow your cash beyond that $150,000 cap.

Whether you prefer guaranteed instruments like SSBs, flexible tools like cash management accounts, or you're ready to explore ETFs and global markets, there’s a strategy for every comfort level. Just remember that the right option depends not only on returns, but also your timeline, liquidity needs, and risk appetite.

And don’t overlook the value of protecting your savings—through tools like UOB’s Money Lock feature or essential insurance coverage. Earning interest is important, but safeguards and structure matter too.

This article was first drafted with the help of AI and later reviewed and refined by the author.