If life gives you $100,000, can Reddit tell you how to turn it into a money tree?

“Put it in UOB One.”

“All in Bitcoin, thank me later.”

“Use the money to start a side hustle.”

These aren’t our suggestions—they’re suggestions from Redditors from a thread on what to do with a $1000,000 lump sum of cash. Another thread from someone who inherited $100,000 has yet more recommendations.

Would it be totally insane to follow financial advice from Reddit? Are some—or any—of these suggestions sound? Let’s review them, from the safest options like fixed deposits and Singapore Government Securities to more high-risk investments like Bitcoin.

"How Should I Invest $100k?": Rating Advice From Reddit

- Put it in a high-interest savings account

- Buy Singapore Government Securities (T-bills, Singapore Savings Bonds)

- Park it in a fixed deposit

- Tuck it away in an emergency fund

- Pay off your debts and loans

- Have a fun fund…?

- Get health insurance and do a health screening

- Top up your CPF

- Invest in blue chip stocks

- Invest in exchange-traded funds using dollar cost averaging

- Buy property with friends

- Start a side hustle

- Buy into Bitcoin

- Diversify your investments

1. Put it in a high-interest savings account

Source: Reddit

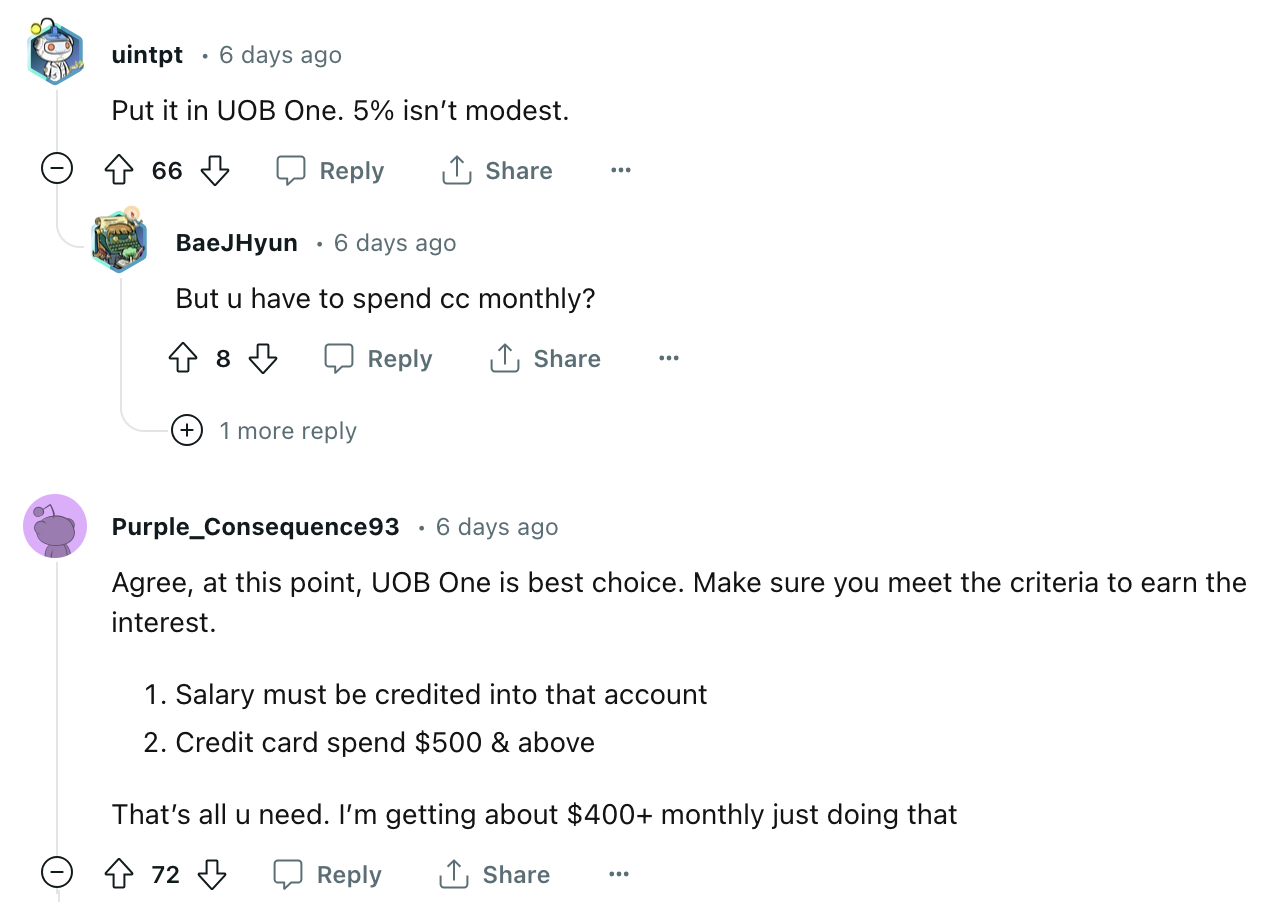

Take a quick look at this Reddit thread, and you’ll notice “UOB One” comes up a lot. But what are these people talking about? What is UOB One?

The UOB One Account is UOB’s flagship savings account. So technically, along this line of logic in the Reddit thread above, any high-interest savings account would work the same way. You put your money into a bank, meet certain criteria, and earn interest.

So why is everyone suggesting the UOB One Account out of all the other savings accounts in Singapore? The UOB One Account’s maximum interest rate is 7.8% p.a.. That’s about as high as it gets on a savings account for simply using your credit card (minimum $500 spend) and crediting your salary (minimum $1,600)—it even made the news in Dec 2022 for this!

Next question: Why were the Redditors mentioning 5% and the corresponding $400 then? The 7.8% rate applies only on the $25,000 that sits between $75,000 and $100,000 in your account. If you look at your $100,000 lump sum as a whole, the effective interest rate (EIR) that applies to it is 5.00% p.a. That earns you $5,000 a year, or $416 a month.

- Base Interest Rate p.a.

- 0.05%

- Max. Interest Rate p.a.

- Up to 3.40%

- Min. Balance

- S$1,000

Is it MoneySmart? | |

Our rating | ★★★★★ |

Our verdict | Savings accounts are low-risk ways to grow your money, and you can withdraw your cash anytime. At up to 5.00% p.a. effective interest on your $100,000 lump sum, they’re currently a great investment option if you want to play it safe. |

2. Buy Singapore Government Securities (T-bills, Singapore Savings Bonds)

Source: Reddit

After the UOB One Account, some recommend investing the $100,000 in T-bills or SSB. These refer to, respectively, Treasury Bills and Singapore Savings Bonds. They’re both types of government securities, which basically means that they’re tools the government uses to raise money for its operations and projects, such as infrastructure development. Did you really think Jewel, or even the newly opened T2 for that matter, were funded by taxpayers’ money alone? When you invest in a T-bill or SSB, you’re essentially loaning the government money to fund such developments.

While T-bills and SSBs are similar in some respects, they differ in a few others:

T-bill | SSB | |

Interest payment | You receive the interest you earn from a T-bill at the initial sale in the form of a discount (yeah, we know that sounds confusing. Check out our full T-bill article for the full explanation). | You receive interest every 6 months, and it increases each year you hold on to the SSB. |

Latest rates | 3.95% (cut-off yield for 26 Oct 2023 T-bill) | 3.4% (average return over 10 years) |

Tenor | 6 months or 1 year (must keep your money in there for entire duration) | 10 years (withdraw anytime) |

Minimum investment | $1,000 | $500 |

Maximum investment | None | $20,000 |

Lock-in period/Redemption | You cannot redeem a T-bill early. Any money you invest in a T-bill is not liquid during its tenor. | No lock-in period. Redeem your SSB anytime. |

So, now for the big question:

Is it MoneySmart? | |

Our rating | ★★★★☆ |

Our verdict | Singapore government securities are also low-risk investment tools. Choose SSBs for higher liquidity; otherwise T-bills currently offer higher interest rates for fixed lock-in periods. |

3. Park it in a fixed deposit

Source: Reddit

This Redditor suggests putting the $100,00 into a fixed deposit (FD), which is another low-risk investment option. When you park your money in a fixed deposit with your bank of choice, the bank will reward you with interest simply for putting it in there and not touching it for a couple of months. Exactly how many months? Some banks offer fixed deposits as short as 1 month, while others go up to 24 months. The only thing is that like T-bills, fixed deposits are highly non-liquid. You need to stash your cash into the account for the agreed-upon amount of time.

Unlike T-bills, you’ll know how much interest you’ll earn from your fixed deposit upfront. For example, if the fixed deposit rate is 3% p.a. and you invest $10,000 for 6 months, you’ll earn (3% x $10,000) / 2 = $150.

Is it MoneySmart? | |

Our rating | ★★★★☆ |

Our verdict | While low-risk, fixed deposits have low liquidity and interest rates can vary greatly across banks. Do your research before you lock your money away— or actually, let us do the research for you. |

4. Tuck it away in an emergency fund

Source: Reddit

We’ve talked about investing our $100,000 into savings accounts, government securities, and fixed deposits. Before we go into investments with higher risk, let’s hit pause and consider this Redditor’s advice—put some money away into an emergency fund.

Emergency funds are your financial safety net, designed to catch you when life throws its curveballs. Think of it as the fiscal equivalent of an airbag, cushioning the blow from unforeseen expenses like medical emergencies, sudden job loss, or urgent car repairs. Everyone of any income level needs one because—let’s face it—surprises come in all sizes, and not all are pleasant.

So, how much should you stash in this safety stash? The golden rule is to tuck away enough to cover 3 to 6 months' worth of living expenses. That’s enough to give you breathing room to find a new job or handle a crisis without the added stress of living on the financial edge. If your income is less stable or you’re self-employed, you might want to aim for a 9 to 12-month buffer instead. Probably better to have too much saved up than too little.

Is it MoneySmart? | |

Our rating | ★★★★★ |

Our verdict | We love that people brought this up on Reddit. You’re not technically earning anything, but an emergency fund is a must to have. |

5. Pay off your debts and loans

Sort of on a related note, while you’re setting aside money to put into an emergency fund, you should also take stock of any debts and loans you might have. No one suggested this on the Reddit threads we poked around in, but it’s worth mentioning. There’s no point investing your money to earn 3% interest when your outstanding debt is eating away 5% interest.

Paying off debts and loans is nothing short of liberating. If you think about it, freeing yourself from the shackles of compounded interest actually boosts your net worth—not to mention your peace of mind knowing you don’t owe anyone anything anymore.

What if you have more than one debt? How do you prioritise which loans to pay off first? An easy answer is to prioritise high-interest debts first—they’re the silent wealth eaters. This strategy, known as the avalanche method, minimises the amount you'll pay in interest over time.

Alternatively, you could try the snowball method—targeting the smallest debts for quick wins. This works well if you have a number of small loans or debts owed, and can be a motivational boost for you to give you a sense of progress.

Is it MoneySmart? | |

Our rating | ★★★★★ |

Our verdict | No point earning money through investments while your outstanding debts eat away so much more. One step at a time! |

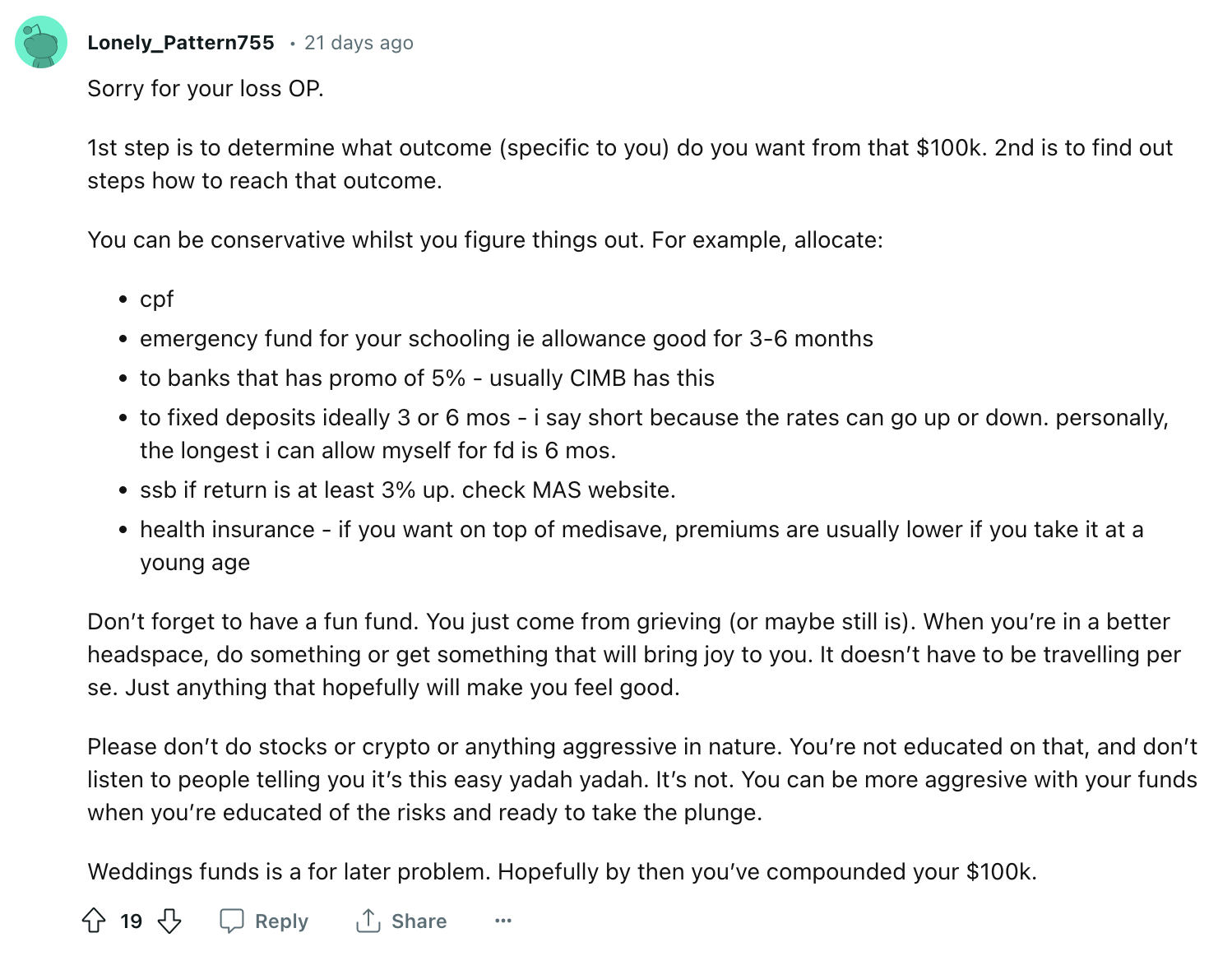

6. Have a fun fund…?

Source: Reddit

This Redditor gave a plethora of suggestions. We’ve covered fixed deposits, savings accounts, SSBs, and emergency funds, but there are 3 new things mentioned in this comment: health insurance, CPF, and a “fun fund”. Let’s discuss each of these one by one.

The “fun fund” first. No, this isn’t a legit financial strategy. But in this case, the OP mentioned that they received a lump sum of $100,000 following a bereavement. Lonely_Pattern755 is trying to add a more human, more sensitive touch to the flood of financial advice the OP received. We don’t disagree, but would add a word of caution to not overdo it. Additionally, in cases like these where one is working through a difficult situation, perhaps counselling services might be helpful. Not exactly “fun”, but certainly a good investment.

Is it MoneySmart? | |

Our rating | ★★☆☆☆ |

Our verdict | Money is great to grow, but eventually meant to be spent. Just don’t overdo it, and put your money to meaningful use. |

7. Get health insurance and do a health screening

Health insurance should be a no-brainer if you don’t already have it, or if your coverage is insufficient. All Singaporeans are covered by MediShield Life, but supplementing that with an Integrated Shield Plan is a good idea for additional coverage. These can come with benefits like better wards in public hospitals, the option of staying in a private hospital, higher claim limits, and shorter waiting times.

On the topic of health, when was the last time you had a full health screening? This is going to be worth your while, especially if you manage to detect any health conditions and seek the appropriate treatment early. You’ll end up paying less in the long run—think about it as saving future you a bunch of medical bills!

Is it MoneySmart? | |

Our rating | ★★★★☆ |

Our verdict | Hefty medical bills without insurance are decidedly not MoneySmart. If you don’t already have health insurance or lack sufficient coverage, now’s the time! |

8. Top up your CPF

Wait, isn’t CPF just the thing that eats up a chunk of my salary each month, money that I never see again? Why would I put even more money into that black hole? There are actually several reasons why you’d want to park money into your CPF. For one thing, you earn 4% interest on money in your CPF Special Account (SA)—that’s higher than most fixed deposits, SSBs, and T-bills. Interest aside, you’ll also earn up to $16,000 in tax relief for making CPF top-ups, plus enjoy higher CPF monthly payouts when you retire.

One word of warning: any money you put into your CPF SA can’t be taken out until you retire. So be sure that’s where you want your cash to be stashed before you make the top-up.

By the way, don’t mix up what we just talked about above with the CPF Investment Scheme (CPFIS). The CPFIS lets you invest the money in your Ordinary Account (OA) and SA savings in anything from SSB unit trusts. You can even put the OA money into gold, shares, and property funds. Just note that since the government always wants to enhance your retirement savings, any money you earn will go right back into your CPF, not into your bank account.

Is it MoneySmart? | |

Our rating | ★★★☆☆ |

Our verdict | Safe and with a decent interest rate of 4% p.a. in your CPF SA. Just be aware it’s a one-way street, and money you put into your SA can’t come out till you’re ready to retire. |

9. Invest in blue chip stocks

Source: Reddit

InternationalWait212 is all about the waiting game. They say, put your $100,000 in stocks and wait 10 years or so—stocks might go up/down today, next month, and even next year, but they’ll be on the upward trend in the long run. Is this true?

Well, historically, stock markets generally exhibit an upward trajectory with economic expansion and innovation putting wind in their sails. Individual stocks, however, can vary greatly and are not guaranteed to rise. Downturns and volatility are part of the market's nature. For a steadier path to potential long-term growth, investors often turn to blue chip stocks.

Blue chip stocks are the all-stars of the stock market—reputable, well-established companies known for their financial stability and solid track records. In Singapore, these market stalwarts often include household names like DBS Group, Singtel, and CapitaLand.

Okay, so these guys are famous and established and all that jazz. But what does it mean to invest in them? Investing in blue chip stocks is like placing your money on these proven performers. They work by offering investors a share in their profits, often paying dividends consistently.

While they're generally considered safer than newer or smaller companies because of their established business models and consistent performance, no stock is entirely risk-free. Market conditions, economic shifts, or company-specific setbacks can affect their performance. However, if you look at the grand scheme of things in the world of investments, blue chip stocks are often seen as reliable and hold strong even when the market gets rough.

Do you know what’s even safer than a blue chip stock? Several blue chip stocks. You might get that in an exchange-traded fund, which we’ll discuss next.

Is it MoneySmart? | |

Our rating | ★★★☆☆ |

Our verdict | As far as investing in stocks goes, blue chip stocks are one of your lower risk options. |

10. Invest in exchange-traded funds using dollar cost averaging

Source: Reddit

Lots of acronyms in this thread, but don’t be intimidated. We’ve actually covered SSB and CPFSA already, so the only new terms are DCA and ETF.

DCA = Dollar cost averaging. This is a strategy where you invest the same amount of money at regular intervals, spreading the purchase of investments over time. The idea is to smooth out the average price you pay in fluctuating markets and reduce the risk of investing a lump sum at the wrong time. It’s also the investment method used in regular savings plans.

ETF = Exchange-traded funds. An ETF is like a basket of various investments, including things like stocks and shares, that you can buy and sell easily. It's a simple way to invest in lots of different things at once, without having to pick each one individually. Since they offer diversified holdings, they’re less risky than individual stocks. However, potential returns and risks are gonna vary depending on the assets and the market conditions they mirror.

ETFs typically track indexes, perhaps the most famous of which is the S&P 500, which tracks the 500 biggest companies on the US stock exchange. Closer to home, the Straits Times Index tracks the top 30 companies in the Singapore stock market.

To apply the DCA strategy to an ETF, you would invest a fixed amount of money into that ETF at regular intervals, say monthly or quarterly, regardless of the ETF’s price at each interval. While this isn’t as safe or guaranteed as say a fixed deposit account or SSB, it’s not terribly risky either compared to things like bitcoin or crypto. That’s because you’re getting the best of both worlds—you’re mitigating market fluctuations with DCA while getting a diverse portfolio of different assets with an ETF.

Is it MoneySmart? | |

Our rating | ★★★★☆ |

Our verdict | ETF + DCA = a pretty darn solid investment strategy in the stock market. Note that with DCA, you’re thinking long term—don’t expect huge returns overnight. |

11. Buy property with friends

Source: Reddit

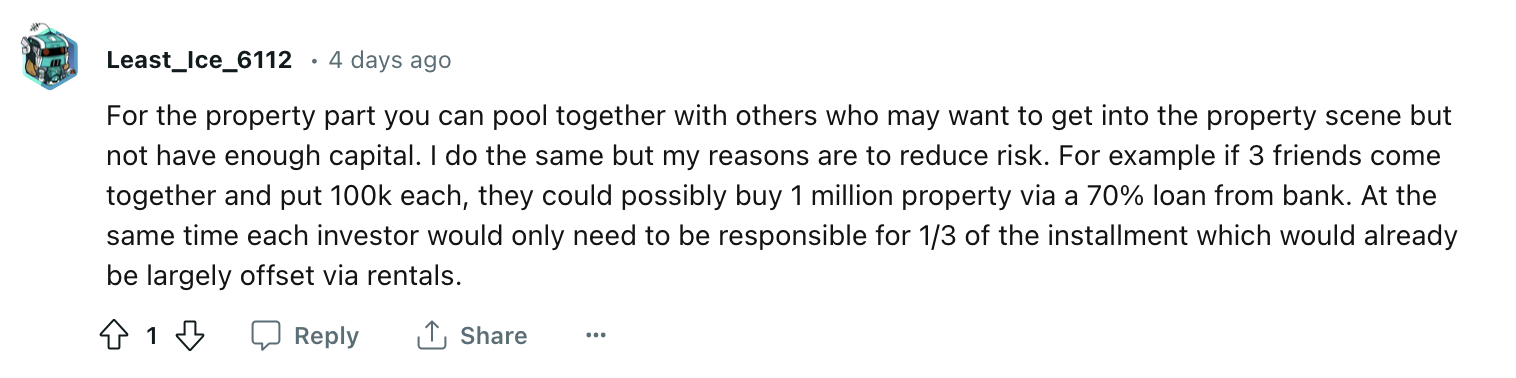

I did a double take when I read this suggestion because pooling money with friends to buy a property together didn’t even cross my mind. Least_Ice_6112, I don’t mean to sound cold, but this suggestion just doesn’t hold water for me due to the risks involved (or maybe I just don’t trust my friends enough). I’ll go into the risks later.

First, let’s talk about the benefits and how this property “group buy” would work first. Pooling money with friends means you can afford to buy a larger property than you’d be able to buy as a single. For HDB flats and executive condos, you can purchase your property under the Joint Singles Scheme, meaning all your names are tied to the property. This option comes with some restrictions—for example, you can only apply for 2-room BTO flats.

For private property like condos and landed homes, you’d need to work out how the property share should be split under the Tenancy-In-Common ownership scheme. If you split the costs equally, it’s fair to split the share equally too. So far, so good.

Now, the risks. What if one of your pals suddenly has a change of heart—or, worse, a change of cash flow? Missed payments could turn friends into enemies faster than you can say "foreclosure." And what about the legalities? Sharing a deed isn't as simple as splitting a pizza. If your friend group suddenly turns toxic and forces you to give up your new home, it’s going to look something like breaking up after a BTO or breaking up after buying an EC. The latter’s going to come with greater costs, of course, and the private property equivalent will come with even more severe losses.

What if things get super messy? What if it becomes a legal battle? For this reason, no matter how close you are to your friend(s), I would never recommend splitting the property share equally if you don’t fork out the same amount every month. Touch wood, but if you end up going to court to facilitate the liquidation of the property (following the liquidation of your friendship), the monetary contributions are going to matter. Don’t just take my word for it—an LGBTQ+ real estate expert told me so.

Is it MoneySmart? | |

Our rating | ★☆☆☆☆ |

Our verdict | Do you really trust your friends that much? Unpopular opinion: Don’t. |

12. Start a side hustle

Source: Reddit

It sounds almost idyllic—take your spare cash, invest it into something you love, and you’ll end up with an extra source of income while pursuing your passion. *chef’s kiss*

Reality check: Starting a side hustle isn't as risky as, say, betting it all on black at the roulette wheel, but it's not without its dice rolls. You could be pouring cash into a blog, a crafty Etsy store, or even a pop-up ramen joint. Whatever it is, you'll need to spend money to make money that you can’t guarantee you’ll rake in. Think about the costs of materials, marketing, or even a website to make your handmade creations look more like a legitimate business and less like a casual hobby.

Of course, there are success stories of side hustlers. We’ve got an educator turned jewellery designer, a marketing executive turned fitness coach, and an accounting professional turned baker. But not all side hustles will have you rolling in dough—in fact, we daresay more fail than succeed. It takes time, effort, and a bit of business savvy. So, if you're ready to hustle, make sure you're also ready for a little tussle with the realities of entrepreneurship.

Is it MoneySmart? | |

Our rating | ★★☆☆☆ |

Our verdict | Be ready to tussle if you want to hustle—and actually profit from it. |

13. Buy into Bitcoin

Source: Reddit

Source: Reddit

Ahh, bitcoin. The digital age's gold rush—but instead of pickaxes, you're wielding powerful computers, a digital wallet, and an understanding of blockchain technology.

Bitcoin is a type of cryptocurrency, which is like virtual cash that lives online and champions the idea of financial transactions without middlemen like banks.

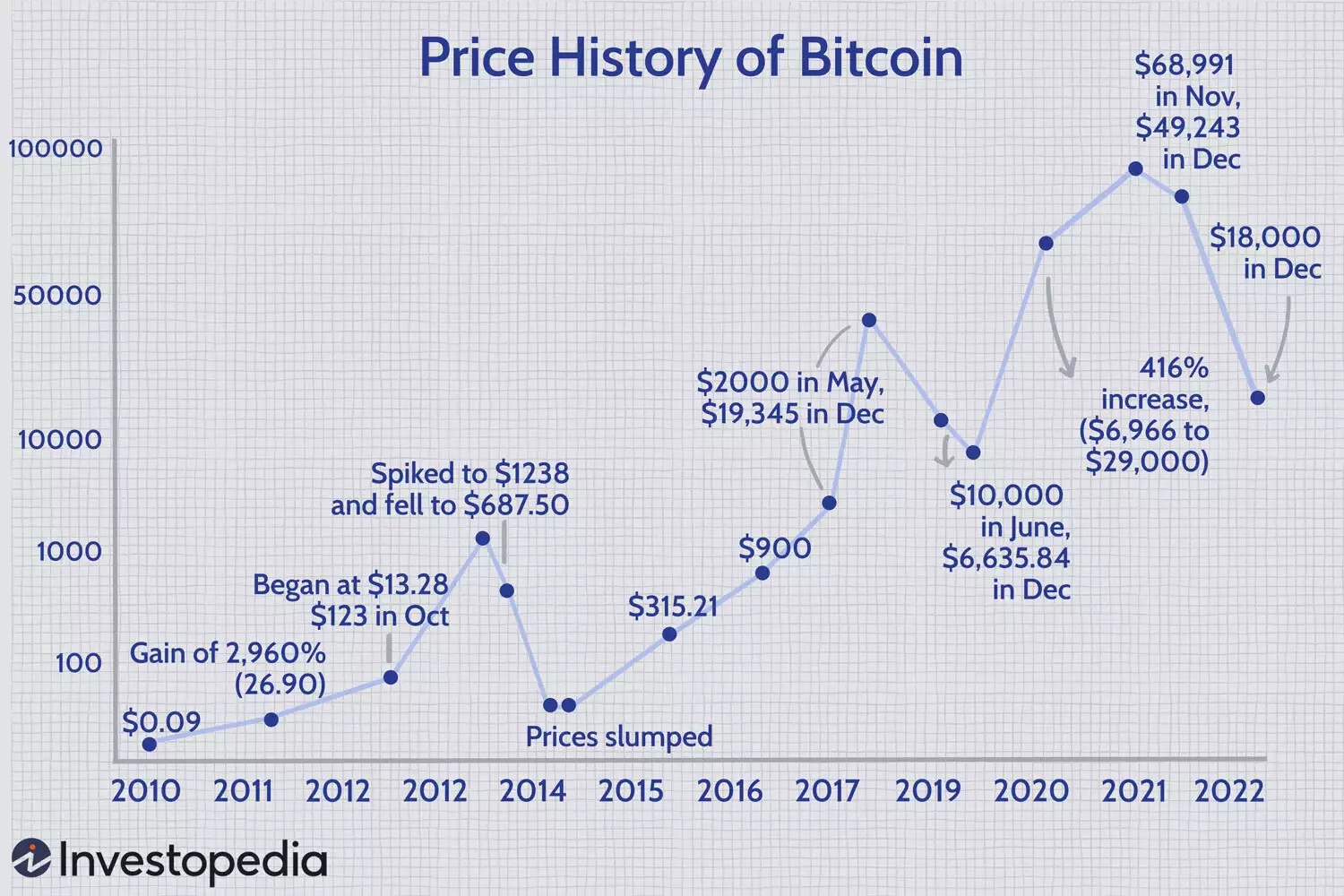

Sounds exciting? Perhaps too exciting. Investing in Bitcoin can be very unpredictable as its value can fluctuate widely thanks to market sentiment, regulatory news, and tech developments. Just last year, Bitcoin plummeted by 64%—only to have its value more than double this year. Here’s a look at how the price of Bitcoin has spiked up and down from 2010 to 2022:

Source: Investopedia

If you want to invest in Bitcoin, be ready for volatility and risks. It's not for the faint-hearted or for the cash you'll need in a pinch. In the world of Bitcoin, potential high rewards come also with high risk.

Is it MoneySmart? | |

Our rating | ★☆☆☆☆ |

Our verdict | If your SSBs and fixed deposits are on 1 end of the investment risk spectrum, Bitcoin is on the other. It’s not for just any beginner-level investor—tread with caution! |

14. Diversify your investments

Source: Reddit

Source: Reddit

Source: Reddit

Finally, I wanted to highlight these comments on Reddit because they all exhibit something I highly recommend—diversification.

You know that saying, don’t put all your eggs in one basket? That’s what diversifying your investments is like. Instead of loading up on just one stock or banking everyone on a property with friends, you spread your money across different assets. This buffet of assets could include a mix of super safe stuff like fixed deposits and SSBs, medium-risk things like stocks and ETFs, and even high-risk investments like Bitcoin.

Why is this safer? By diversifying, you're not just relying on one company or sector's success. When stocks are in a freefall, at least you have your T-bills holding steady, and commodities like gold could add a little sparkle to your portfolio. Diversifying builds a robust investment immune system that can better withstand market ups and downs.

Is it MoneySmart? | |

Our rating | ★★★★★ |

Our verdict | No matter what you choose to invest your money in, diversifying is always a good idea to cushion fluctuations. |

Found this article useful? Share it with your family and friends!

Related Articles