In Singapore, choosing the right health insurance plan isn’t just a checkbox—it’s one of the most personal (and costly) financial decisions we make. For years, Integrated Shield Plans (IPs) with private hospital treatment were the gold standard for many. Shorter waits, swankier wards, wider treatment choices—it all made sense.

Until it didn’t.

In 2024, medical inflation hit 10%, outpacing the general hikes of 3-5%, with total healthcare costs rising 55.8% since 2004. As healthcare costs balloon, many are rethinking their plans.

We’ve already seen a 5% dropin the uptake of the highest-tier IPs, and nearly 15,000 seniors have switched from private plans back to MediShield Life. So, what’s behind this shift—and what could it mean for the way we plan—and pay—for healthcare moving forward?

Why more are dropping private hospital coverage

1. How IPs are structured: A quick refresher

2. What's happening to IP premiums, and why?

3. What's driving these changes?

4. How this affects Singaporeans

How IPs are structured: A quick refresher

Integrated Shield Plans (IPs) are private insurance plans that supplement the national MediShield Life scheme. In Singapore, IPs are offered by7 private insurers, each providing different tiers designed to match our preferences for hospital ward classes. They are: AIA, Great Eastern, HSBC Life, Income, Prudential, Raffles Health Insurance, and Singlife.

Private Hospital Plans (Highest Tier)

These plans offer coverage for stays in private hospitals, giving you the widest choice of specialists and typically the shortest waiting times. This is often what people refer to as the "highest” IP tier.

Public Hospital A Ward Plans

These cover stays in Class A wards within restructured (public) hospitals, which are typically single-bedded, air-conditioned rooms.

Public Hospital B1 Ward Plans

These cover stays in Class B1 wards in restructured hospitals, usually offering a 4- to 5-bedded, air-conditioned room.

Standard Integrated Shield Plans (for Public Hospital B1 Ward)

This is a standardised, more basic IP offered by all insurers, providing coverage for Class B1 wards in public hospitals.

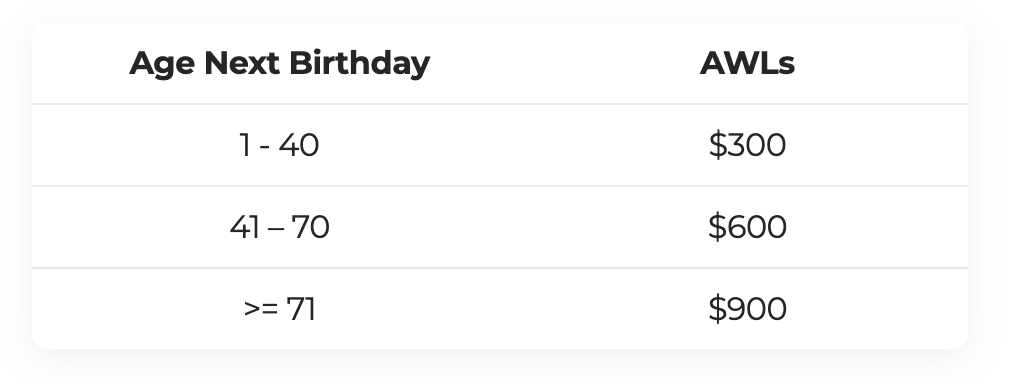

Every IP layer adds coverage on top of MediShield Life. While MediSave can fund part of your premiums (up to certain Additional Withdrawal Limits based on our age), any excess, including riders, must be paid in cash.

Here’s how AWLs are measured on the 3 main age groups’ next birthday:

Image: CPF

What's happening to IP premiums, and why?

It’s more than a price hike. We’re seeing structural changes that affect how IPs work and what they cost.

1. Premium increases by ward class

After the Life Insurance Association’s (LIA) 2-year premium freeze, most insurers revised premiums across all tiers:

- Private Hospital Plans:

The higher-tier plans, which cover stays in private hospitals, have seen the most substantial premium hikes, with average increments of 21% (without riders) and up to 35% (with riders) for certain insurers' private hospital plans – i.e. Great Eastern’s SupremeHealth P Plus and PruShield Premier.

- Public Hospital Plans (A & B1 Wards):

While typically less substantial than adjustments made for private hospital plans, premiums covering Class A/ B1 wards in restructured hospitals have also seen adjustments. Some insurers' restructured hospital-based plans saw increments of 14% (without riders) and 23% (with riders).

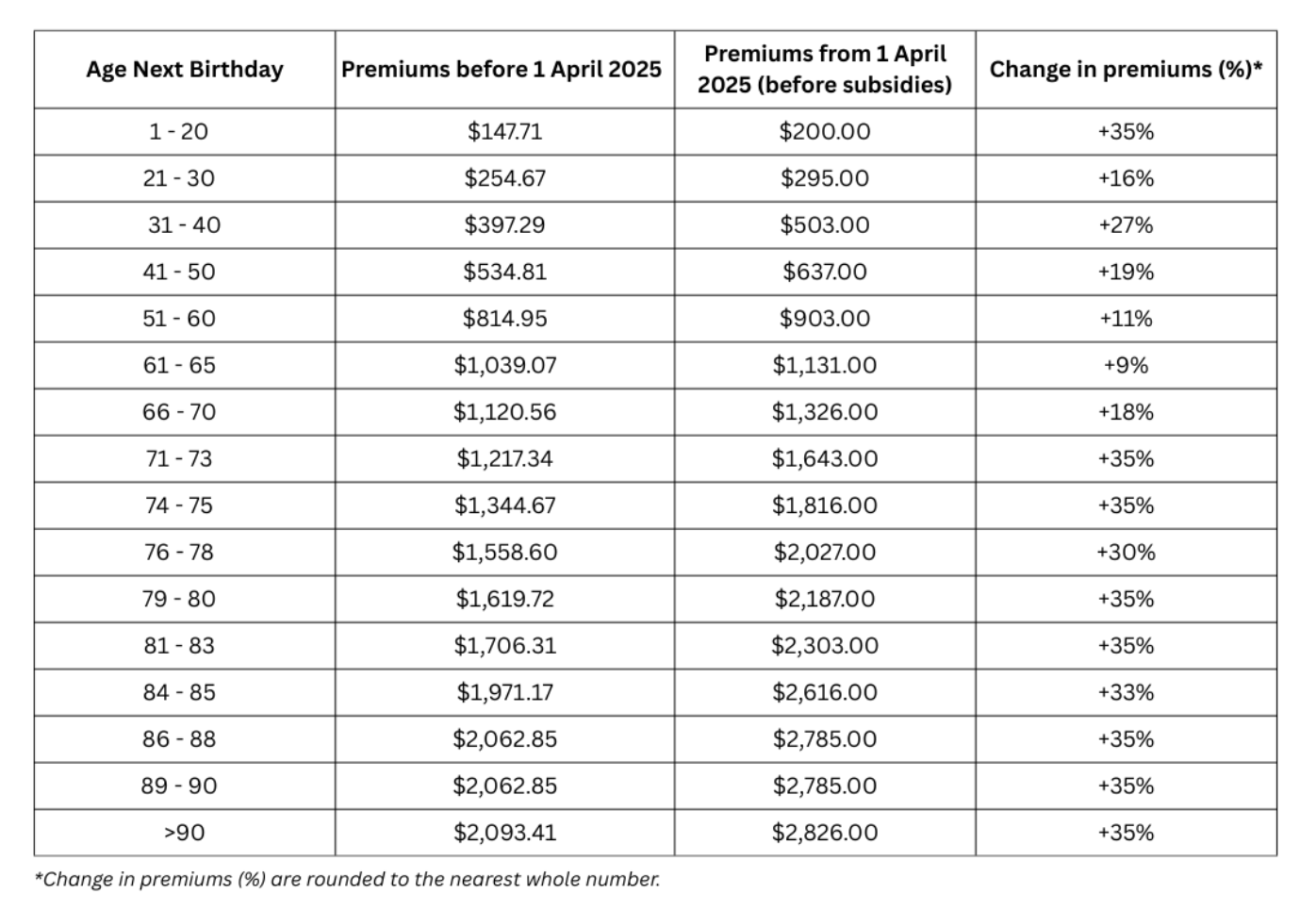

2. Age-related premium jumps

What's more, age-based premium increments are now a much bigger factor. Here’s a breakdown:

Image: MediShield Life

Effective from1 Apr 2025, premiums for the base component of our health coverage will see a substantial 35% increase for those aged 1-20, and a similar 35% jump for individuals aged 71-73.

Even for those within the 41-50 age bracket, premiums saw a notable 19% rise. These steep jumps often lead to tough decisions for families as they try to sustain coverage for older members.

3. Rider overhaul = more out-of-pocket costs

Perhaps one of the biggest changes affecting out-of-pocket costs and overall premiums involves IP riders.

Mandatory co-payment is here to stay

The days of 'as charged' or 'full coverage' riders, where we paid little to nothing out-of-pocket, have ended.

This means that your riders come with a mandatory 5% co-payment for medical bills, typically capped at $3,000 per policy year. This move also signifies we're more directly exposed and liable to directly pay for a portion of our medical bills.

Claims-based pricing will further drive up premiums

You might also notice that many insurers have introduced claims-based pricing for riders.

Just like car insurance, making a claim may raise your premiums. This comes with the aim to encourage consumers to be prudent in making healthcare claims while ensuring these plans remain viable and sustainable.

Several private insurers, like AIA, are now putting their own spin on the claims-based pricing to keep premiums somewhat affordable. Max VitalCare offers up to a 25% discount if no claims are made on the policy!

Still, considering the broader healthcare trends, the reality is that our premiums are likely to continue their upward climb for the foreseeable future

What's driving these changes?

Several key trends fuel this:

Reason #1: Singapore’s rapidly ageing population

By 2030, a quarter of Singaporeans (1 in 4) will be aged 65 and above. This fast-growing population inevitably means more frequent visits, complex treatments, and longer hospital stays, directly putting further strains on resources and drumming up costs across the board.

Reason #2: Advancements in medical technology

While we're grateful for breakthroughs, newer, more effective treatments, sophisticated diagnostic tools, and innovative drugs often come with a hefty price tag. From advanced surgeries like minimally invasive robotic procedures to cancer treatments like immunotherapies, these improvements, while life-saving, contribute to rising medical bills.

Reason #3: Rising manpower costs

Healthcare is (and has always been) a highly people-centric industry. To attract and retain dedicated doctors, nurses, and allied health professionals, their wages and benefits must remain competitive.

These increasing manpower costs, which form a substantial part of our healthcare expenditure, naturally filter down into the overall cost of services. Manpower costs alone can account for over 60% of a hospital's operating expenses, and with a tight labour market, these costs will continue to climb.

Reason #4: The buffet syndrome

Another significant (but perhaps hidden) factor is the 'buffet syndrome'. When insurance covered everything, some people overused it—opting for more tests or treatments than necessary. That drove up claims and forced insurers to increase premiums across the board.

In fact, people on full coverage riders often racked up bills up to 60% more, higher than those with co-payment riders. Without some skin in the game, healthcare spending spirals.

Just like any other business, insurers must ensure their plans remain financially viable long-term. This is why the LIA's premium freeze ended, prompting them to adjust rates to cover the increasing claims they've been paying out.

How this affects Singaporeans

So what does all this mean in practical terms?

We’re paying more out of pocket

Let's start with what hits closest to home – our wallets. Base premiums for ages 71-73 have jumped a substantial 35%. Coupled with a mandatory 5% co-payment, out-of-pocket expenses are significantly higher.

This will most affect seniors due to steeper age-based increases and less financial stability, and strainfamilies supporting elderly parents. The 5% co-payment also comes as a surprise to those accustomed to the old 'as charged' mode.

More are downgrading their plans (especially seniors)

Cost-conscious individuals, especially older adults, are stepping down to basic MediShield Life. While it keeps premiums low, the trade-off is reduced flexibility and higher out-of-pocket expenses for certain treatments.

For example, a $10,000 private hospital bill could become a $5,000 one in a public B1 ward. But that comes with longer waits and fewer provider choices.

Access to private care may shrink

If fewer people are using private IPs, access to private specialists and faster treatment could become more limited. This might drive more people into the public system—and possibly lead to longer wait times for non-urgent specialist visits or elective surgeries.

More uncertainty in healthcare planning

Claims-based pricing introduces more unpredictability. It’s no longer just about your age—your claims history now plays a role. That makes it harder to plan and budget for healthcare expenses long-term.

Are there any upsides?

Fortunately, there is—especially when it comes to MediShield Life improvements and government support.

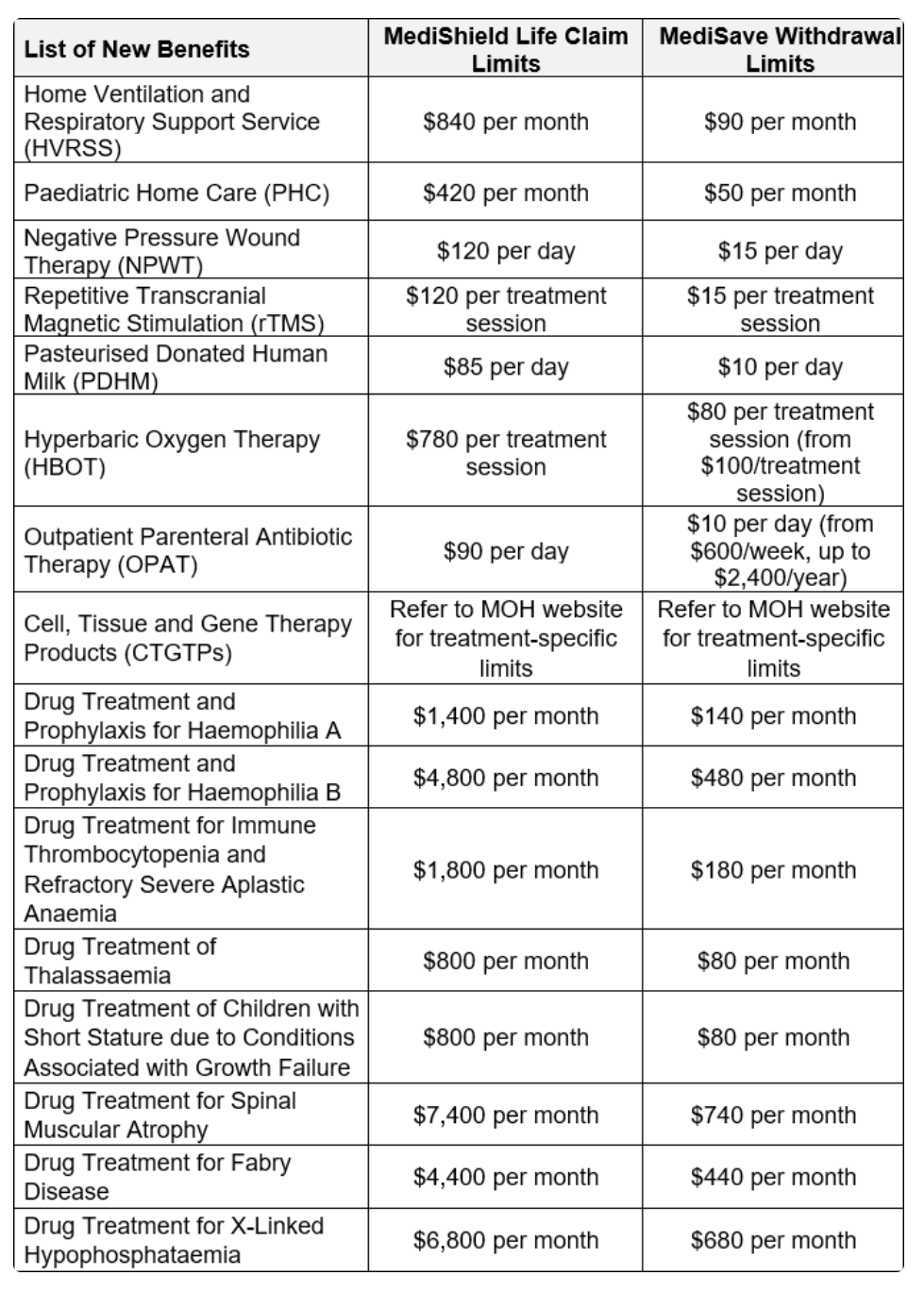

Higher claim limits

One of the biggest wins is the increased coverage limits, which will rise by $50,000 to $200,000 for claims. This means we can sufficiently cover high-cost drug treatments, as well as expensive and advanced treatments like cell tissue or gene therapy products.

Image: MOH

MediShield Life Claim Limits & Withdrawal Limits For New Treatments To Be Covered By MediShield Life.

The Ministry of Health expects 9 out of 10 subsidised bills to be fully covered under these revised limits.

Government support to ease premium hikes

Another reassuring aspect is theadditional $4.1 billion insupport over the next 3 years to cushion higher premiums. This includes $3.4 billion in MediSave top-ups and $700 million in premium subsidies.

For over 90% of Singaporeans, these combined top-ups and subsidies will more than offset the total $1.8 billion in additional premiums.

Final thoughts

Singaporeans are clearly rethinking their health insurance strategies. Private coverage isn’t as accessible or as affordable as it once was, but we’re not without options.

With stronger MediShield Life benefits and significant government support, many can still find ways to maintain coverage without breaking the bank. Now’s a good time to review your IP, understand the changes, and see how they fit into your current financial situation and future needs.

Not sure what’s right for you? Chat with one of our insurance specialists today to make sense of your options.

Related Articles