The UOB PRVI Miles Card has the highest base miles earn rates among entry-level miles cards in Singapore. Impressive, no? But don’t forget that it comes with a conversion fee.

…which the KrisFlyer UOB Credit Card does not. This heavyweight lets you earn KrisFlyer miles directly without any conversion fees. You can even earn up to 3 KrisFlyer Miles on your everyday dining, shopping, and transport spending.

Which UOB card deserves a spot in your wallet? In this article, we’ll break down the fees, miles earning potential, and unique benefits of each card to see how the UOB PRVI Miles Card stacks up against the KrisFlyer UOB Credit Card.

Review: UOB PRVI Miles Card vs Krisflyer UOB Credit Card (2024)

- The vital stats

- Earning miles

- Earning 6 miles per S$1

- Miles renewal bonus

- Airport privileges

- Miles expiry

- Which card is better?

1. UOB PRVI Miles vs KrisFlyer UOB: The vital stats

The most straightforward things to compare between these 2 cards are fees, rates, and income requirements. In the table below, I bolded the areas in which they differ.

UOB PRVI Miles Card | KrisFlyer UOB Credit Card | |

Annual fee & waiver | $261.60 including GST (waived for 1 year) | $196.20 including GST (waived for 1 year) |

Supplementary annual fee | 1st Supplementary Card free, $130.80 for subsequent Supplementary Cards | 1st Supplementary Card free, $98.10 for subsequent Supplementary Cards |

Interest free period | 21 days | 21 days |

Annual interest rate | 27.80% | 27.80% |

Late payment fee | $100 | $100 |

Minimum monthly repayment | 3% or $50, whichever is higher | 3% or $50, whichever is higher |

Foreign currency transaction fee | 3.25% | 3.25% |

Cash advance transaction fee | 8% | 8% |

Overlimit fee | $40 | $40 |

Minimum income | $30,000 (Singaporean/PR) / $40,000 (non-Singaporean) | $30,000 (Singaporean/PR) / $40,000 (non-Singaporean) |

Card association | Visa / Mastercard / American Express | Mastercard |

Wireless payment | Visa Contactless, UOB Mighty Pay | Apple Pay, Samsung Pay, UOB Mighty Pay, Mastercard Contactless |

There are 2 important differences between the UOB PRVI Miles Card and the Krisflyer UOB Credit Card.

Firstly, the former has a higher annual fee for both the primary and supplementary cards. Luckily, this higher fee doesn’t also come with higher income requirements like I’ve noticed is the case for other cards with elevated annual fees. The UOB PRVI Miles Card’s higher annual fees also aren’t that important when you consider the fact that you can always get your annual fee waived.

The second difference is that the KrisFlyer UOB Credit Card’s card association is fixed as Mastercard, while you get to choose Mastercard, Visa, or American Express for the UOB PRVI Miles Card. If you’re considering ease of payment, the former 2 are your best bets.

As far as card benefits go, your card association affects what kind of card privileges you can enjoy with your UOB PRVI Miles Card. As of 2 Sep 2024, the Visa and Amex variants come with more privileges than the Mastercard one.

ALSO READ: UOB PRVI Miles vs DBS Altitude: Which Travel Card Wins in 2026?

2. UOB PRVI Miles vs KrisFlyer UOB: Earning miles

Both the UOB PRVI Miles and KrisFlyer UOB Credit Cards earn you miles, but differ in how and how many miles they earn. Here’s a quick look:

UOB PRVI Miles Card | Krisflyer UOB Credit Card | |

Miles earned in the form of | UNI$ (UNI$1 = 2 miles) | KrisFlyer miles |

Base miles earn rate | S$1 = 1.4 Miles (local spend) | S$1 = 1.2 KrisFlyer miles |

Bonus miles earn rate | S$1 = 6 Miles on selected online hotel and flight bookings via Expedia | S$1 = 3 KrisFlyer miles (Singapore Airlines, Scoot, KrisShop and Kris+ purchases) |

Cap on miles to be earned | No cap | No cap |

Minimum annual/monthly spend required for bonus miles | No minimum spend | S$800 per year on Singapore Airlines, Scoot and KrisShop |

Spend blocks with which you earn miles | Per S$5. | Per S$5. |

With the comparison points above in mind, here are some important questions to ask yourself if you’re trying to decide between the 2 cards.

What type of miles do you want? Which airlines do you fly with?

The KrisFlyer UOB Card earns you KrisFlyer Miles, which you can use to offset flights on Singapore Airlines, Scoot, and partner airlines like Alaska Airlines, Vistara, Virgin Atlantic, Virgin Australia and Juneyao Airlines.

Comparatively, the UOB PRVI Miles Card earns you UNI$, which you can convert to either KrisFlyer Miles or Asia Miles. Asia Miles are redeemable with airlines like Cathay Pacific, Air China, Alaska Airlines, British Airways, Finnair, Fiji Airways, Japan Airlines, Qantas, Qatar Airways, and more.

If you always fly with airlines under KrisFlyer, both cards are an option to you. But if you’re loyal to airlines like Cathay Pacific, British Airways, Qantas, or Qatar, then you might want to opt for the UOB PRVI Miles Card so that you can choose to convert your points to Asia Miles instead of KrisFlyer Miles.

Is a $25 conversion fee worth it for you?

Since the Krisflyer UOB Credit Card earns you KrisFlyer Miles directly, there is no conversion fee to speak of.

On the other hand, the UOB PRVI Miles Card earns you UNI$ that you need to convert to miles. Each conversion comes with a $25 conversion fee. You can convert your UNI$ to miles in blocks of UNI$5,000 to 10,000 KrisFlyer Miles or Asia Miles.

It can take you anywhere from ~$1,667 (UNI$15 per S$5 spent on Expedia) to ~$7,142 (UNI$3.5 per S$5 spent locally) to earn UNI$5,000. If you factor in the cost of the conversion fee, you’re technically earning 10,000 miles from $1,692 to $$7,167 spend instead. That translates to a slightly lower miles earn rate:

Earn rate | UNI$3.5 per S$5 spent locally | UNI$15 per S$5 spent on Expedia |

Spend amount to earn UNI$5,000 (10,000 Miles) | $7,142 (1.4 miles per S$1) | $1,667 (6 miles per S$1) |

Spend amount to earn UNI$5,000 (10,000 Miles), factoring in $25 conversion fee | $7,142 + $25 = $7,167 (1.39 miles per S$1) | $1,667 + $25 = $1,692 (5.91 miles per S$1) |

If you’re thinking it’s more worth it to convert a larger UNI$ at a time to spread out the conversion fee, you’re right. But don’t wait too long to convert your UNI$. Earned UNI$ expires 2 years from the last day of each periodic quarter in which the UNI$ was earned. So UNI$ earned in Jan, Feb or Mar 2024 will expire on 31 Mar 2026.

What are the best bonus spend categories for you to earn miles?

With credit cards—whether miles or cashback cards—you play the game by spending on your card, earning rebates on your spending, and then using those rebates to offset your future spending. That’s why figuring out what you spend the most on is essential for earning more rewards.

Between the UOB PRVI Miles Card and Krisflyer UOB Credit Card, the choice boils down to 2 main questions.

- Do you often make hotel and flight bookings via Expedia? If you do, the UOB PRVI Miles Card can earn you 6 Miles per S$1 on these transactions when you book on expedia.com.sg/prvimiles.

- Do you often spend on Singapore Airlines, Scoot, KrisShop and Kris+? Bearing in mind that KrisShop retail items include a wide range of lifestyle products that go well beyond travel ones—anything from facial serums to premium tea leaves. If you answered yes, the Krisflyer UOB Credit Card is a good choice.

- Earn 3 KrisFlyer miles per S$1 spent on Singapore Airlines, Scoot, KrisShop and Kris+.

- If you spend at least S$800 annually on Singapore Airlines, Scoot, and KrisShop, you can also enjoy 3 KrisFlyer miles per S$1 spent on these everyday spend categories: dining, food delivery, online shopping, online travel and transport.

For base miles earn rates, the UOB PRVI Miles Card is the winner.

What if you answered no to both questions in the previous section? In this case, we turn our attention to the base miles earn rates (the rates above are for bonus categories only). While the Krisflyer UOB Credit Card earns you 1.2 KrisFlyer miles per S$1 spend in both SGD and foreign currency, the UOB PRVI Miles Card beats it in both categories:

- S$1 = 1.4 Miles (local spend)

- S$1 = 2.4 Miles (foreign spend)

So as far as base earn rates go, the UOB PRVI Miles Card is the better choice. In fact, it has the highest base miles earn rates among all the entry-level miles cards in Singapore!

Do those high base miles rates make up for the fact that its bonus miles category is limited to just Expedia bookings? That depends on your spending habits and is something you have to figure out for yourself.

I do want to point out that the bonus miles rate you get with the UOB PRVI Miles Card is twice the bonus rate you’ll get with the KrisFlyer UOB Credit Card. In this sense, spending $400 on Expedia bookings with the UOB PRVI Miles Card and $800 on Singapore Airlines/Scoot/KrisShop purchases with the KrisFlyer UOB Card will earn you the same number of miles.

Will you spend at least S$800 a year on Singapore Airlines, Scoot, and/or KrisShop?

This is relevant to the Krisflyer UOB Credit Card, which offers 3 KrisFlyer Miles per S$1 spent on dining, online shopping, transport, and other spend. It’s worth considering, especially since one flight on Singapore Airlines can easily already put you over that sum.

You’ll then earn 3 miles per S$1 on these everyday spend categories, which is over twice as much as the 1.4 miles per S$1 local spend you’d earn with the UOB PRVI Miles Card.

3. The KrisFlyer UOB Credit Card can match the UOB PRVI’s 6 miles per S$1…but don’t do it!

The KrisFlyer UOB Credit Card offers up to 6 Bonus KrisFlyer Miles per S$1 spend if you open a KrisFlyer UOB Account and credit your salary to it. That sounds great at first; and at 6 miles per dollar, that even puts the KrisFlyer UOB’s highest bonus mile earn rate level with that for the UOB PRVI Miles Card. But there are 2 big problems I have with this offer.

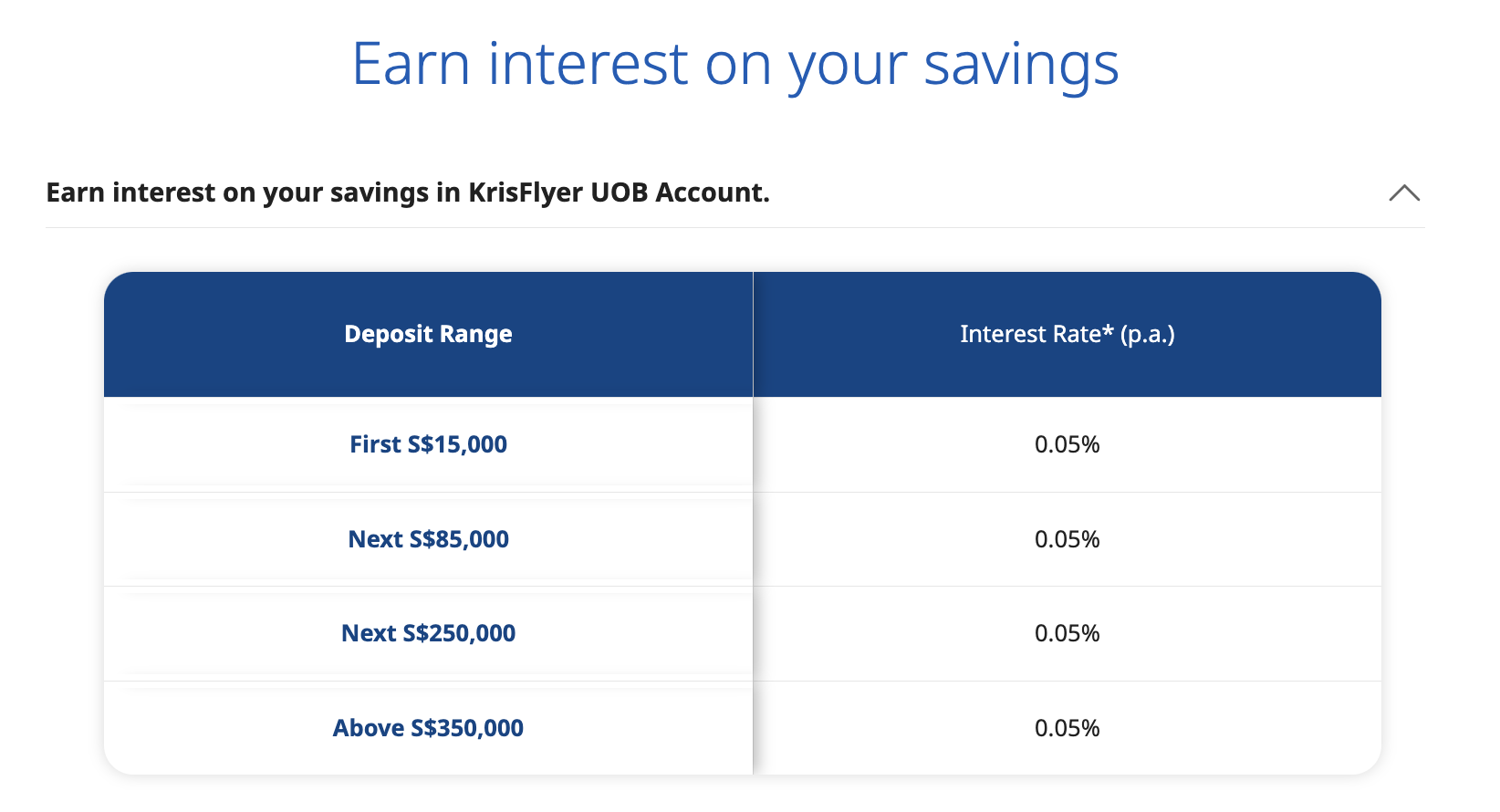

Firstly, opportunity cost. Even if you only put in the minimum $1,000 in your UOB KrisFlyer Account, that’s $1,000 you could have invested elsewhere. T-bills, Singapore Savings Bonds, or fixed deposits would probably get you 3 – 3.5% right now. That’s 60 to 70 times more interest than you’ll get with the KrisFlyer UOB Account, which earns you a dismal 0.05%.

Image: UOB

By the way, speaking of crediting your salary into an account, there are lots better savings accounts you could credit your salary to to earn higher interest.

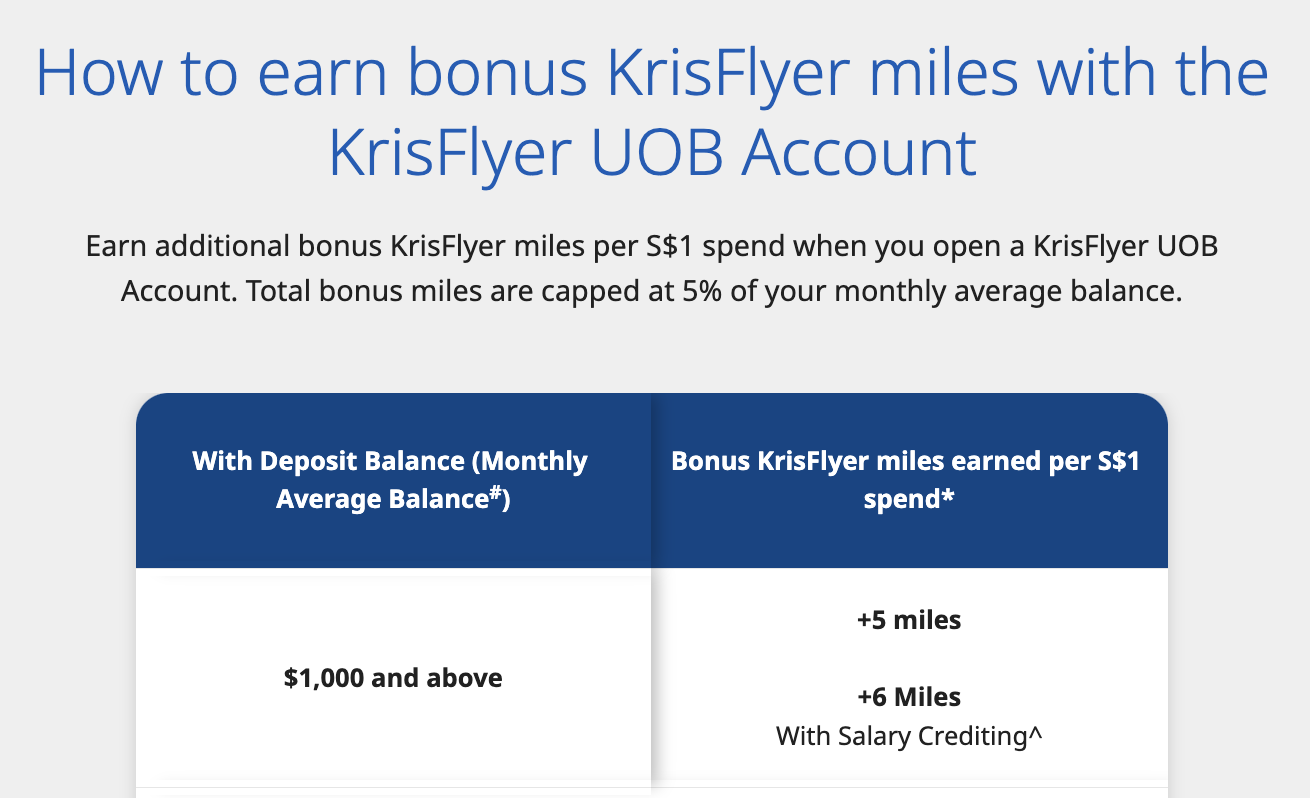

The second reason I advise against the KrisFlyer UOB Account is the low cap on the bonus miles you can earn. Your bonus miles are capped at just 5% of your monthly average balance in your KrisFlyer UOB Account.

Let’s say you have $10,000 in there (which, going back to the first point, represents too high an opportunity cost in my opinion). Your bonus miles are capped at just 500 KrisFlyer Miles, which you’ll earn from spending just $100 (without salary credit) on your KrisFlyer UOB Credit Card.

Image: UOB

ALSO READ: Citi PremierMiles vs DBS Altitude: Quick Feature & Reward Comparison

4. UOB PRVI Miles vs KrisFlyer UOB: Miles renewal bonus

Unlike the UOB PRVI, the KrisFlyer UOB Credit Card offers a miles renewal bonus—10,000 KrisFlyer Miles if you renew your annual membership and pay the Principal Cardmember annual fee of S$196.20 in full. That’s essentially buying miles at about 1.96 cents each.

What can you do with 10,000 miles? To give you an idea, here are the KrisFlyer Miles you’d need to redeem an Economy flight on Singapore Airlines:

- Singapore to Denpasar, Bali: 17,000 miles

- Singapore to Bangkok, Thailand: 27,000 miles

- Singapore to Tokyo: 54,000 miles

At the time of writing, a return trip to Bali from Singapore costs about $600+ to $700+ on SQ. Considering your S$196.20 annual fee payment will earn you 10,000 miles to take you more than halfway there to redeem a flight to Bali, that’s a good deal.

The UOB PRVI Miles Card doesn’t have a renewal bonus, but the American Express iteration offers 20,000 loyalty miles when you spend at least S$50,000 in a membership year based on a 12-month statement period. That’s an average of $4,167 per month! If you’re already spending this much, the 20,000 miles will be a nice-to-have. Otherwise, they aren’t something to aim for given the high spend amount required.

5. UOB PRVI Miles vs KrisFlyer UOB: Airport privileges

The UOB PRVI Miles American Express Card gets you 2 complimentary airport transfers per quarter, subject to a minimum S$1,000 overseas spend within the same quarter. Unfortunately, the Visa and Mastercard versions don’t come with this benefit.

The KrisFlyer UOB Credit Card doesn’t grant you airport transfers or lounge access, but you do get S$15 off Grab rides to or from Singapore Changi Airport with the promo code KFUOBCC. This is capped to once per half yearly (i.e. Jan to Jun and Jul to Dec), and is limited to the first 1,000 redemptions per month.

If you ask me, neither card comes out very strong in terms of its airport benefits. And being entry-level cards is no excuse—entry-level miles cards with lounge access include the Citibank PremierMiles Card and the DBS Altitude Visa Signature Card.

6. UOB PRVI Miles vs KrisFlyer UOB: Miles expiry

Applicable to | |||

Miles/points | Expiry | UOB PRVI Miles | KrisFlyer UOB |

UNI$ | Earned UNI$ expires 2 years from the last day of each periodic quarter in which the UNI$ was earned. | ✓ | |

Asia Miles | Asia Miles don’t expire as long as you earn or redeem them at least once every 18 months. The expiry date is extended by 18 months from the date the miles are credited or debited, not from the activity date (such as spending on your credit card). | ✓ | |

KrisFlyer Miles | KrisFlyer miles will expire after 3 years at the end of the equivalent month in which they were earned. | ✓ | ✓ |

When you consider when your miles expire, you’ll notice something curious about the UOB PRVI Miles Card—because you first earn UNI$ to be converted to miles, the total length of time you have to convert and redeem your miles is longer. You can keep your UNI$ for 2 years before converting them to KrisFlyer Miles, from which they’ll be valid for 3 years. If you choose to convert them to Asia Miles instead, you can keep them forever as long as you earn or redeem your Asia Miles once every 18 months.

With the KrisFlyer UOB Credit Card, your KrisFlyer miles are credited directly to your KrisFlyer account. The 3-year timer starts on them immediately.

In this respect, the UOB PRVI Miles Card is the better choice.

7. UOB PRVI Miles vs KrisFlyer UOB: Which card is better?

Winner: UOB PRVI Miles Card

Let me preface this by saying that the UOB PRVI Miles Card is better for me. It’s almost unfair to compare the 2 cards because they serve 2 different kinds of travellers.

The KrisFlyer UOB Credit Card is a fantastic choice for someone who regularly flies on Singapore Airlines and Scoot. Once you spend S$800 in a year on your flights with these airlines, you can start racking up 3 KrisFlyer Miles per S$1 spend on everyday spend categories like dining, online shopping, and transport. Even if you don’t hit this annual spend, you’ll earn 3 KrisFlyer Miles per S$1 spend on these airlines and on KrisShop.

Assuming you’re already loyal to SQ or Scoot, you’ll also love that you earn KrisFlyer Miles directly with no conversion fees needed. Just remember not to go for the KrisFlyer UOB Account because of the low interest rates, opportunity cost, and low cap on the bonus miles you can earn.

I would love the KrisFlyer UOB Credit Card…if I were that kind of person I just described. But I’m not. The biggest issue is that I’m not a KrisFlyer loyalist. I’m always changing airlines depending on which fits my budget and has flights that leave at the right time I’m looking for. I’ve flown with SQ maybe only twice in my life, and only because my university paid for the flight (SQ is expensive!). Yes, I have flown with Scoot more often…but just as often as I’ve flown with other budget airlines like Jetstar.

The UOB PRVI Miles Card makes more sense for me, with greater flexibility to convert my UNI$ to either Asia Miles or KrisFlyer miles. Aside from it having the highest base earn rates among other entry-level miles cards, I like that I can earn 6 miles per S$1 on Expedia bookings without a minimum spend requirement. Although the UOB PRVI Card comes with a conversion fee, I’ll happily pay it to have the choice of which type of miles I want to convert them to, plus an overall longer time horizon to then redeem my miles.

UOB PRVI Miles vs KrisFlyer UOB: The most important question to ask yourself

So between the UOB PRVI Miles Card and the KrisFlyer UOB Credit Card, which is the better option for you? It’s your choice to make based on, first and foremost, the airlines you fly with.

If you always fly SQ, Scoot, or their partner airlines like Alaska Airlines and Virgin Atlantic, the KrisFlyer UOB Credit Card is a strong contender.

On the other hand, if you rarely fly with the aforementioned airlines and have no intention to in the future, the KrisFlyer UOB Credit Card is going to make no sense for you. Choose the UOB PRVI Miles Card for the flexibility to use your UNI$ earned as KrisFlyer Miles or Asia Miles (e.g. Cathay Pacific, British Airways, Finnair, Fiji Airways, Japan Airlines, Qantas, Qatar Airways).

Read on to see how the UOB PRVI Miles Card stacks up against other miles cards, including the DBS Altitude Card.

Found this article useful? Share it with your friends and family who could use the insights.

Related Articles