Who knew that Singapore’s highest-earning unlimited cashback card would come from…Shopee?

Image: Steady Compounding/gif.com

The Mari Credit Card is named after MariBank, Shopee’s digital bank. With this card, you can earn 5% unlimited Shopee Coins on your Shopee spending. Considering that Shopee is the biggest e-commerce platform in Singapore and people order anything from groceries to home furniture on it, those rebates could really add up.

But that’s not all. The Mari Credit Card will also earn you an unlimited1.7% cashback on your other card spending, which Shopee claims is the highest unlimited cashback rate in Singapore. They’re not lying—the 1.7% puts them in first place, albeit tied with the UOB Absolute Cashback Card.

5% unlimited Shopee coins, 1.7% unlimited cashback, and no annual fee. Is the Mari Credit Card too good to be true? Let’s take a look.

Mari Credit Card—Is it MoneySmart? | |||||

| |||||

Pros—What we like | Cons—What we don’t like | ||||

– 5% Shopee Coins on Shopee spend (from now to 30 Sep 2024) | – You must have a Mari Credit Account and link it to your Shopee account to earn your 5% Shopee Coins. | ||||

Mari Credit Card at a glance | |||||

Category | Our rating | The deets | |||

Earn rates: Cashback | ★★☆☆☆ | –5% Shopee Coins on Shopee spend (from now to 30 Sep 2024) | |||

Earn categories | ★★★★★ | ||||

Annual fees and charges | ★★★★★ | No annual fee | |||

Accessibility | ★★★★☆ | Minimum income requirement: $30,000 (Singaporeans and PRs) | |||

Extras/periphery rewards | ☆☆☆☆☆ | Unlike credit cards from banks that offer things like dining privileges and complimentary travel insurance, this card just does its one job of earning you cashback or Shopee Coins. | |||

Sign-up bonus | ★☆☆☆☆ | Currently no welcome bonus aside from the 5% Shopee Coins rebate ongoing till 30 Sep 2024. | |||

See our credit card ranking rubric to find out how we rank credit cards.

Mari Credit Card—MoneySmart Review (2024)

- Mari Credit Card: Cashback earn rates and categories

- Mari Credit Card: Do the cashback and Shopee Coins earnings stack?

- Mari Credit Card: Is the 5% Shopee Coins rebate good?

- Mari Credit Card fees and charges

- Should I get the Mari Credit Card?

- How do I apply for the Mari Credit Card?

- Alternatives to the Mari Credit Card

1. Mari Credit Card: Cashback earn rates and categories

There are 2 ways you can earn with the Mari Credit Card:

- Shopee Coins credited to your Shopee account (from now to 30 Sep 2024)

- Cashback credited to your card account

How do I earn 5% Shopee Coins with the Mari Credit Card?

From now to 30 Sep 2024, pay for your Shopee purchases using Mari Credit Card Instant Checkout to earn an unlimited 5% Shopee Coins rebate. The Shopee Coins will appear in your Shopee account on your Shopee app.

To pay using Mari Credit Card Instant Checkout, you must:

- Have a Mari Credit Account

- Link your Mari Credit Account with your Shopee account via the MariBank App

- Keep these 2 accounts linked until you get your Shopee Coins reward

To earn Shopee Coins via this method, you must select “Pay In Full” as the payment option on Shopee. These payment methods will not earn you the 5% Shopee Coins:

- Instalments

- Credit Card/Debit Card option (when you manually input your Mari Credit Card details)

- Google Pay

- Apple Pay

If you pay using any of the last 3 options, Shopee will classify your purchase as a card transaction instead, for which you’ll earn 1.7% cashback.

Read more about the terms and conditions for the Mari Credit Card Shopee Coins Promotion.

How do I earn 1.7% cashback with the Mari Credit Card?

Outside of Shopee, you'll earn 1.7% cashback on eligible purchases.

On the Shopee app, if you aren’t paying by Mari Credit Card Instant Checkout, you’ll also earn 1.7% unlimited cashback.

Either way, this 1.7% cashback will be credited to your card account and be used to offset your next Mari Credit Card statement.

As always, exclusions like utilities, medical bills, education, and taxes do not earn you the 1.7% cashback. Read more about the terms and conditions for the Mari Credit Card’s cashback.

2. Mari Credit Card: Do the cashback and Shopee Coins earnings stack?

If only they did! But no:

- If you use Mari Credit Card Instant Checkout, you’ll earn 5% Shopee Coins.

- If you don’t use Mari Credit Card Instant Checkout, you’ll earn 1.7% cashback.

Unfortunately, these are mutually exclusive and don’t stack.

On the plus side, at least both are unlimited.

3. Mari Credit Card: Is the 5% Shopee Coins rebate good?

By itself, a 5% Shopee Coins rebate isn't very impressive—not when the cashback vouchers you can claim in the Shopee app range from 10% to 80% (via Shopee Live).

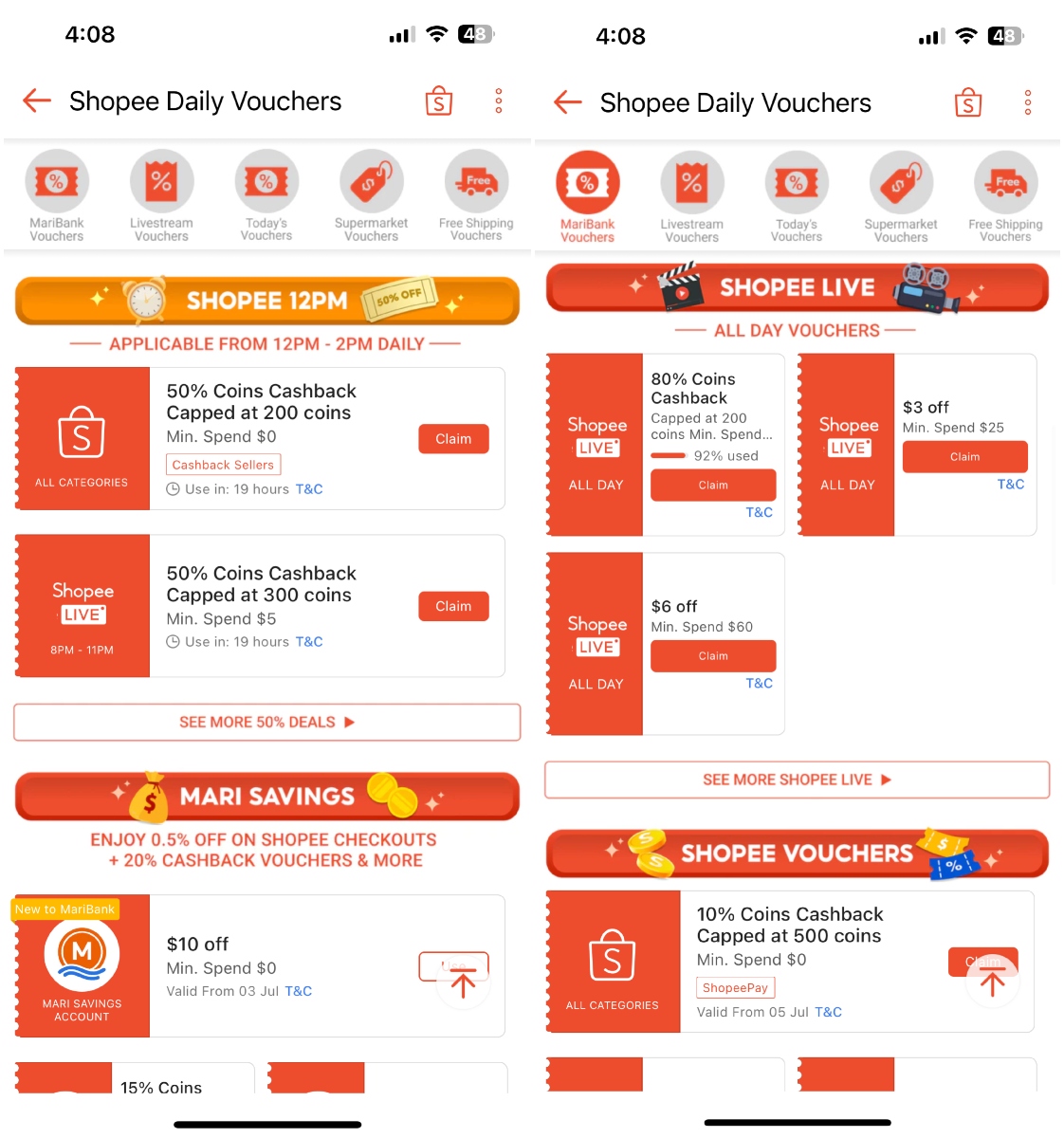

Image: Shopee. Navigate to “Daily Vouchers” under the first tab, “Daily Discover”, to claim your platform vouchers.

The good news is that the 5% Shopee Coins rebate promised by the Mari Credit Card doesn't replace your platform vouchers, but adds to them.

As of 16 Jul 2024, MariBank has updated their terms and conditions to allow the 5% unlimited Shopee Coins rebate to stack with other in-app platform vouchers. For example, that means if I apply a 10% cashback voucher on my Shopee app and pay using Mari Credit Card Instant Checkout, I'll earn 10% + 5% Shopee Coins from my purchase. That's 15% cashback in the form of Shopee Coins.

This stacking is explained in clause 2.7 of the Mari Credit Card Shopee Coins Promotion’s updated terms and conditions.

Clause 2.7 before 16 Jul 2024 | Clause 2.7 from 16 Jul 2024 | ||||

“For the avoidance of doubt, Orders eligible to earn Cashback under the Promotion will not be eligible to earn any additional Cashback (including in the form of Shopee Coins) under any other Cashback or rewards program offered by Us, unless otherwise specified.” | "For the avoidance of doubt, Orders eligible to earn Cashback under the Promotion can be stacked with other promotions offered by our Affiliates and/or Marketing Partners (including but not limited to rewards granted in Shopee Vouchers), depending on their respective terms and conditions. |

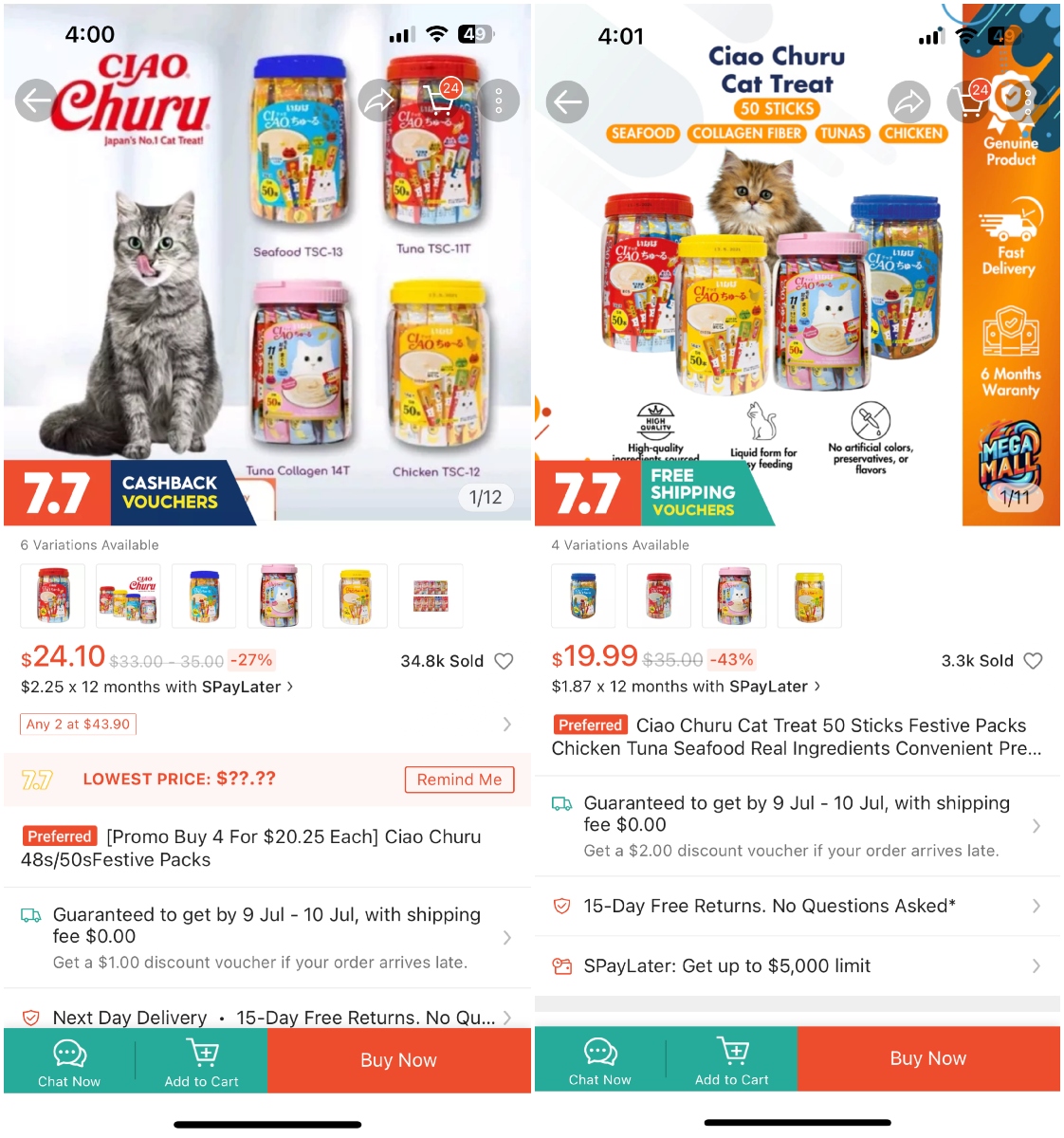

Friendly reminder if you plan on stacking cashback vouchers with the Mari Credit Card's 5% Shopee Coins offer: Shopee’s in-app cashback vouchers only apply to items with Shopee’s dark blue cashback label, like the product listing on the left:

Image: Shopee

Without the cashback label, Shopee cashback vouchers will not earn you any Shopee Coins from your purchase of that item.

Regardless of how you earn them, Shopee Coins expire at the end of the third month from when they were awarded. If you don’t use Shopee enough to make use of them within 3 months, these rebates won’t be useful to you.

4. Mari Credit Card fees and charges

The Mari Credit card goes very light on the fees—$0 annual fee!—but heavy on foreign currency charges. Don’t use this card overseas or to buy purchases with foreign currencies!

Here’s a summary of their fees, interest, and other charges:

Mari Credit Card fees and charges | |

Annual Card Fee | None |

Late Fee | None. However, they will charge you late interest—see below. |

Overlimit Fee | None |

Interest-free period | Up to 51 calendar days from statement date (inclusive), if there is no balance carried forward from previous statement. |

Minimum Payment Due | 3% of the Statement Due (or S$30, whichever is greater) plus any amount that is overdue and/or exceeds your credit limit. |

Interest on outstanding balances | 27.99% per annum, if the Statement Due is not paid in full by Due Date. |

Late Interest on outstanding balances | 30.99% per annum, if the Minimum Payment Due is not paid in full by Due Date. |

Foreign Currency Transactions | 3.77% (includes the 1% charge imposed by MasterCard) |

ALSO READ: 3 Best Credit Card Pairings for Maximising Cashback, Miles, and Rewards

5. Should I get the Mari Credit Card?

Get the Mari Credit Card if you:

- Regularly shop on Shopee (but do note that the 5% Shopee Coins rebate promotion is only valid till 30 Sep 2024!)

- Want an unlimited cashback card—1.7% is the best rate out there. It’s tied with the UOB Absolute Cashback Card, but the Mari Credit Card edges out the competition by being Mastercard. The UOB Absolute Cashback’s card association is Amex, which is not as widely accepted.

- Hate paying annual fees or calling the bank to get them waived.

Don’t get the Mari Credit Card if you:

- Do not have and do not want to have a MariBank account.

- Love credit card privileges like dining discounts and complimentary travel insurance—none here.

- Are expecting a welcome gift—also none here.

6. How do I apply for the Mari Credit Card?

If you’ve been looking for the application page online to no avail, here’s why: the Mari Credit Card is currently on an invite-only basis.

How do you check if you’ve been invited? That depends on whether you’re:

- An existing Mari Credit Account user;

- An existing MariBank customer, but not a Mari Credit Account or Mari Credit Card user yet; or

- Not a MariBank customer yet

For existing Mari Credit Account users

- Log in to your MariBank app.

- Tap Mari Credit Card on the home screen.

- Tap on Get Card Now.

For existing MariBank customers who are not Mari Credit Account or Mari Credit Card users:

- Log in to your MariBank app.

- Tap Mari Credit Card on the home screen.

- Tap Apply.

- Register for Mari Credit Card digitally with Singpass.

For those who are not MariBank customers yet

- Download the MariBank app from the Apple App Store, Google Play Store, or Huawei AppGallery.

- Register with a valid Singapore mobile number.

- Apply for Mari Credit Card digitally with Singpass.

Source: MariBank

In all cases, you’ll receive a virtual credit card immediately once you apply for the Mari Credit Card.

Mari Credit Card upcoming sign-up promotion: $8 cashback

MariBank is set to launch the Mari Credit Card to the public on 24 Jul 2024. If you're planning on getting it, sign up with the promo code [MCCMONSM] to enjoy $8 cashback when you successfully sign up for the Mari Credit Card and make your first spend.

Disclaimer: We don't get a cut if you use the promo code above. We're just sharing it because why say no to extra cashback?

This promotion will run from 24 Jul 2024 to 31 Aug 2024. T&Cs apply.

7. Alternatives to the Mari Credit Card

To compete with the 5% Shopee Coins rebate

UOB One Card: If you spend $2,000 a month, you can get 10% cashback on Shopee and other merchants like McDonald's (including McDelivery®), DFI Retail Group (Cold Storage, CS Fresh, Giant, Guardian, 7-Eleven and more), Grab (including GrabFood) and SimplyGo (bus and train rides).

- cashback on daily spend at McDonald's, Grab, SimplyGo & Shopee

- Up to 10%

- cashback at all grocery spend

- Up to 8%

- cashback cap a year

- Up to S$2,240

To compete with the no minimum spend 1.7% unlimited cashback

UOB Absolute Cashback Card: Also 1.7% unlimited cashback, but the card association is Amex and so may not be as widely accepted.

- Cash Back on Eligible Spend

- 1.7%

- Min. Spend per month

- S$0

- Cash Back Cap

- Unlimited

Citi Cash Back+ Card: Just 0.1 percentage-point lower cashback, and with Mastercard as the card association. Plus, better welcome offers.

- Cash Back on Eligible Spend

- 1.6%

- Min. Spend per month

- S$0

- Cash Back Cap per month

- Unlimited

Get UPSIZED S$430 Cash Reward or 6,140 SmartPoints (worth up to S$499 of Gifts) —just spend S$500 within 30 days of card approval with your new Citibank Credit Card! Receive them as quickly as 5 weeks after meeting the spend criteria.

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

OCBC INFINITY Cashback Card: This card is very similar to the Citi Cash Back+ Card, with the same cashback rate and card association. Read my review of the OCBC INIFINITY Cashback Card for a thorough comparison of Singapore’s unlimited cashback cards.

- on eligible transactions

- Earn 1.6% Cashback

- Min. Spend

- S$0

- Cashback Cap

- Unlimited

Get $250 Cash or 3,900 SmartPoints (enough to redeem an Apple AirPods Pro 3 worth S$349) when you apply and spend a min. of S$400 within 30 days! T&Cs apply.

P.S. Here’s our MoneySmart credit card ranking rubric

In case you’re wondering, here’s how we decide on our credit card rankings.

Is that credit card MoneySmart? Our MoneySmart credit card ranking rubric | |

Category | Our rating |

Overall | The average rating for the credit card on the whole, calculated from the ratings for the individual categories below. Plus, we’ll give you a one-liner on who we think the credit card is best suited for. |

Earn rates: Air miles / Cashback / Rewards points | Air miles ✈️✈️✈️✈️✈️ / Cashback / Rewards points . This category looks at the depth rather than breadth of earn rates.

|

Earn categories | This category looks at the breadth rather than depth of your earnings.

|

Annual fees and charges |

|

Accessibility | Minimum income requirements:

|

Extras/periphery rewards | These include:

|

Sign-up bonus |

|

Check out our ultimate list of credit card reviews for the low-down on credit cards in Singapore.

Found this article interesting? Share it with your family and friends!

Related Articles