Remember those Phua Chu Kang jingles that used to assault your ears every time you popped into Giant or Cold Storage? Thankfully, the DBS yuu Card has come a long way since then.

From its cheesy beginnings to its glow-up in October 2024, when it added KrisFlyer miles conversions and finally earned the approval of miles chasers, the yuu Card has been busy evolving. And the changes didn't stop there—DBS has tweaked how much you need to spend (and where) to unlock its full rewards potential, and as of mid-2026, added a second miles transfer partner to boot.

Still, despite the fine print getting a little stricter, the DBS yuu Card remains a heavyweight among credit cards in everyday spending with its 18% cashback or 10 miles per dollar offers. If you’re a regular at its partner merchants, you just might find yourself wanting nobody, nobody but yuu.

Find out if the DBS yuu Card still deserves a spot in your wallet in our updated review.

[ms-toc title="DBS yuu Card review (MoneySmart Review 2026)"]

DBS yuu Card—Is it MoneySmart? | |||||

Image: DBS Overall: ★★★☆☆ (3.3/5) Best for: Honestly, almost anyone. With your choice of up to 18% cash rebate or 10 miles per dollar on everyday local spending, the DBS yuu Card ticks most people’s boxes so long as you frequent the stores on their list. Not hard, since they are everyday merchants. The catch: You do need to spend at least $800 a month to qualify for the bonus yuu Points that bring the cash rebate and miles earn rate up to 18% and 10 miles per dollar respectively. | |||||

Pros—What we like | Cons—What we don’t like | ||||

|

| ||||

DBS yuu Card at a glance | |||||

Category | Our rating | The deets | |||

Earn rates: yuu Points | ★★★★★ |

| |||

Earn categories | ★★★★☆ | ||||

Annual fees and charges | ★★★★☆ |

| |||

Accessibility | ★★★★☆ |

| |||

Extras/periphery rewards | ★☆☆☆☆ | Deals at merchants like Foodpanda, Guardian, and 7-Eleven | |||

Sign-up bonus | ★★☆☆☆ | Choose between:

Eligibility: Spend a minimum of $800 within 60 days of card approval, plus have a valid DBS PayLah! account by the end of the qualifying spend period. | |||

See our credit card ranking rubric to find out how we rank credit cards.

1. DBS yuu Card: Quick facts

- at participating merchants with no min. spend

- 5% Cash Rebates

- spend min. S$800 & at 4 participating merchants per calendar month

- Up to 18% Cash Rebates

- on all other spend

- 0.25% Cash Rebates

- at participating merchants with no min. spend

- 5% cash rebates

- spend min. S$800 & at 4 participating merchants per calendar month

- Up to 18% cash rebates

- on all other spend

- 0.25% cash rebates

Fun fact: the DBS yuu Card is actually what the DBS Black Card got rebranded as. The once dark, shiny, and sleek Black Card was reborn with a tacky makeover and a Phua Chu Kang jingle that haunted every Giant and Cold Storage aisle.

DBS yuu Card, circa 2024 (Image: DBS)

Thankfully, the yuu Card has since had another glow-up—the new design brings back the sleek, black, and sexy vibe it probably should’ve kept all along.

Image: DBS

More importantly, the DBS yuu Card packs a punch. It's a rewards card that offers up to 18% cash rebate or 10 miles per dollar in the form of yuu Points. You earn the highest rates at selected stores, such as Cold Storage, foodpanda, Gojek, and more.

It comes in 2 versions: the DBS yuu Visa Card and the DBS yuu American Express® Card. If you’re trying to decide between the Visa or Amex versions, Visa generally has a higher acceptance rate.

Both have the same benefits (that we’ll get into later) and the same fees:

DBS yuu Card fees and charges | |

Annual card fee | Principal card: $196.20 (1 year fee waiver) |

Annual interest rate | 27.80% per annum, charged daily, subject to compounding |

Late fee | $100 (for outstanding balance above $200) |

Minimum monthly repayment | 3% of statement balance or $50 (whichever is greater) |

Foreign currency transaction fee | 3.25%, on top of the prevailing foreign exchange rate determined by Visa |

Cash advance transaction fee | 8% of the amount withdrawn per transaction or $15 (whichever is greater) |

Overlimit fee | $40 |

2. DBS yuu Card: Earning yuu Points

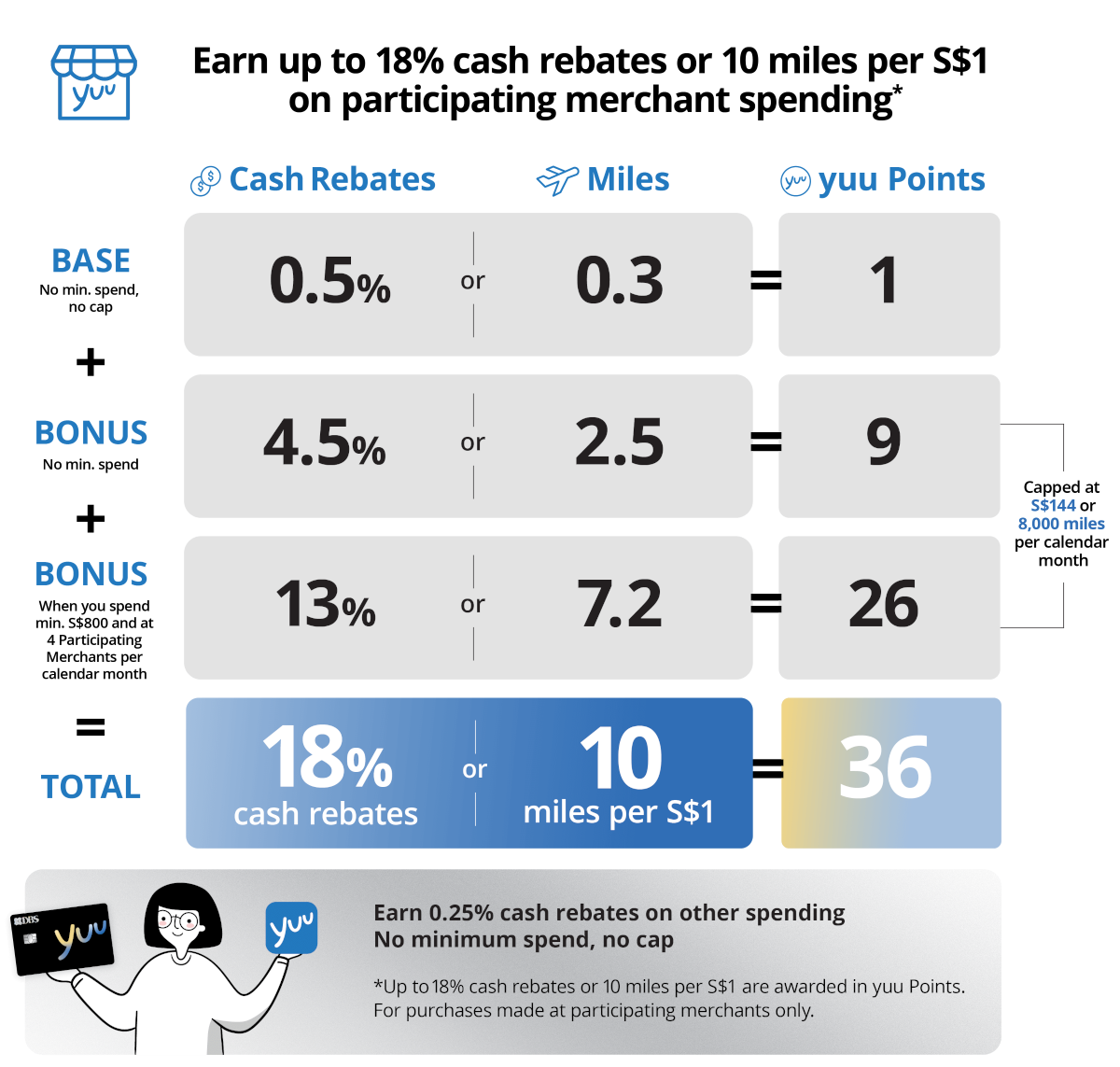

Now for the juicy bit—how do you actually earn those much-hyped 18% cashback or 10 miles per dollar on the DBS yuu Card?

At its core, the card rewards you in yuu Points for every $1 you spend. These Points can then be redeemed as cashback, converted to KrisFlyer miles, or—as of June 2026—converted to HeyMax Max Miles. How many Points you earn depends on where you spend, and whether you meet the monthly minimum spend requirement.

Spend type | Base rewards | Bonus (no min. spend) | Bonus (with min. spend) | Total (with min. spend) |

|---|---|---|---|---|

yuu Merchant Spend | 1 yuu Point (0.5%) | +9 yuu Points (4.5%) | +26 yuu Points (13%) | 36 yuu Points = 18% cashback or 10 miles per $1 |

SimplyGo (bus & train rides) | 0.5 yuu Point (0.25%) | +9.5 yuu Points (4.75%) | +26 yuu Points (13%) | 36 yuu Points = 18% cashback or 10 miles per $1 |

Non-yuu Merchant Spend | 0.5 yuu Point (0.25%) | — | — | 0.5 yuu Point = 0.25% cashback |

To unlock the full 36x earn rate, you’ll need to:

- Spend at least $800 per month, and

- Make purchases at 4 participating merchants.

Otherwise, you’ll still earn respectable returns—10x Points (5% cashback) at yuu merchants or on SimplyGo rides, no minimum spend required.

Reward cap: Bonus yuu Points are capped at 28,800 Points per calendar month (≈ $144 cashback or 8,000 miles). There’s no cap on base rewards.

Principal and supplementary cardholders pool their spend toward the same bonus rewards calculation—all spend on supplementary cards is included when working out whether the principal card has hit the minimum spend, and all yuu Points earned (on either card) are credited to the principal cardmember's yuu account.

TL;DR:

- Spend S$800 and hit 4 merchants → 18% cashback or 10 miles per $1.

- Spend less → 5% cashback or 2.8 miles per $1.

- Everything else → a token 0.25% cashback, but hey, it’s still something.

3. DBS yuu Card: Redeeming yuu points

If you’re interested in using your yuu Points to reduce your next bill at participating stores, you can offset $1 for every 200 yuu Points. In other words, 1 yuu Point is equivalent to a 0.5% cash rebate.

Are you a miles chaser? You have 2 conversion options now:

- KrisFlyer: convert 3.6 yuu Points to 1 KrisFlyer mile.

- HeyMax Max Miles: convert 3.6 yuu Points to 1 Max Mile—the same ratio as KrisFlyer. Max Miles can then be transferred to over 20 airline and hotel loyalty programmes (most at a 1:1 ratio), giving you a lot more redemption flexibility beyond Singapore Airlines and Scoot. Conversions are currently capped while HeyMax builds out its API, so check the yuu App for the latest limits before you convert a large balance.

Assuming you earned Bonus yuu Points with the 36x multiplier, either conversion route works out to be 10 miles per $1 spent.

So if we crunch the numbers: $100 spend at participating stores = 3,600 yuu Points = $18 cash rebate, OR 1,000 miles (KrisFlyer or Max Miles).

Here’s an infographic from DBS to illustrate the above:

Image: DBS

ALSO READ: How to Stretch Your KrisFlyer Miles with Spontaneous Escapes: Tips and Best Credit Cards to Use

Scenario 1: How to earn 10 miles per $1 or 18% cashback with $800 monthly spend

Let’s put this into a simple example. Say you spend $300 each on foodpanda deliveries and groceries at Cold Storage, and another $200 at non-participating merchants in a month. That’s a total spend of $800, just enough to hit the new minimum spend requirement.

Here’s how your yuu Points add up:

What I spent | yuu Points I earn | Equivalent in cash rebate (200 yuu Points = $1) | Equivalent in miles (3.6 yuu Points = 1 KrisFlyer mile) |

|---|---|---|---|

$300 at foodpanda | 10,800 yuu Points (36 yuu Points per $1) | $54 | 3,000 miles |

$300 at Cold Storage | 10,800 yuu Points (36 yuu Points per $1) | $54 | 3,000 miles |

$200 on other purchases | 100 yuu Points (0.5 yuu Point per $1) | $1 | 28 miles |

TOTAL: $800 | 21,700 yuu Points | $109 | 6,028 miles |

Based on the example above, you’re earning roughly $108 in cashback (or 6,000+ KrisFlyer miles or Max Miles) from $600 worth of spending at participating yuu merchants. That’s the equivalent of 18% cashback or 10 miles per dollar, still among the most generous everyday earn rates around.

If spending $800 a month across a few yuu merchants isn’t a stretch for you, the DBS yuu Card remains a no-brainer for groceries, rides, and takeaway life.

Scenario 2: How to earn 2.8 miles per $1 or 5% cash rebates with no minimum spend

Now let’s say I spent $200 on foodpanda deliveries, $100 on groceries at Cold Storage, and $200 on other purchases. If you add that up, you’ll find I didn’t hit the $800 monthly spend to qualify for the 36x Bonus yuu points. However, my spending at Cold Storage and foodpanda still lets me earn the 10x base yuu Points that have no minimum spend required.

In this scenario, here’s how much I’ll be able to redeem in cash rebates or miles.

What I spent | yuu Points I earn | Equivalent in cash rebate (200 yuu Points = $1 rebate) | Equivalent in miles (3.6 yuu Points to 1 KrisFlyer mile) |

$200 at foodpanda | 2,000 yuu Points (10 yuu Points per $1) | $10 | 556 miles |

$100 at Cold Storage | 1,000 yuu Points (10 yuu Points per $1) | $5 | 278 miles |

$200 on other purchases | 200 yuu Points (1 yuu Point per $1) | $1 | 56 miles |

TOTAL: $500 | 3,200 yuu Points | $16 | 890 miles |

As you can see when you compare the 2 scenarios, hitting that $800 monthly spend makes a big difference. Thankfully, it isn’t too high a minimum spend to hit.

4. DBS yuu Card: How to redeem or convert yuu Points

All your yuu Point conversions and redemptions take place on the yuu app, so go get it if you haven’t already. You can also use the app even without the DBS yuu Card, and the app is free, so there’s no reason not to get it and chalk up some points (in this case, $1 spend = 1 yuu Point earned).

How to redeem yuu Points as cash rebate:

Just tell the cashier you want to use your yuu Points, and let them scan your yuu ID. The redemption rate: offset $1 for every 200 yuu Points.

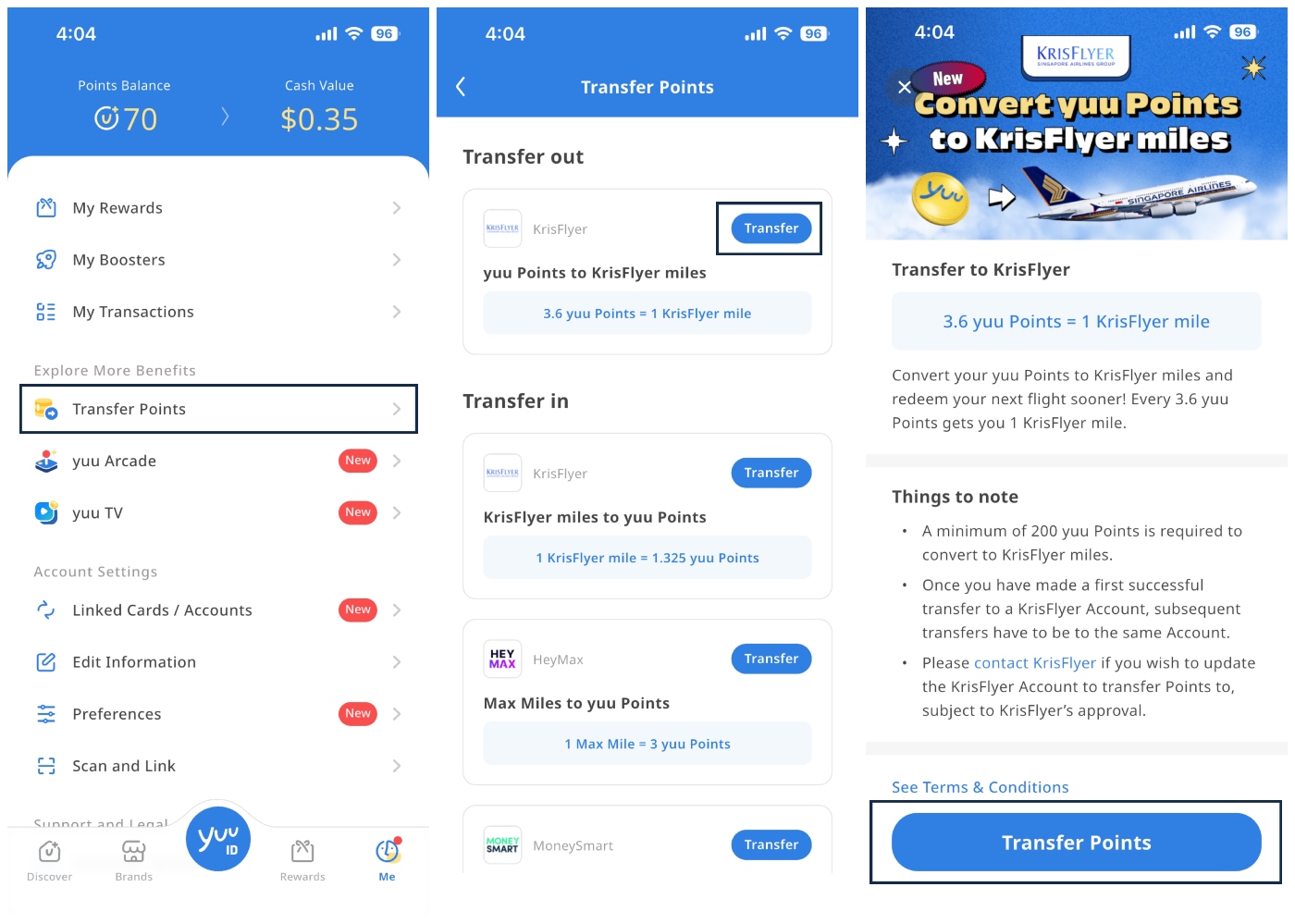

How to convert yuu Points to KrisFlyer miles:

On the yuu app, go to the Me tab on the bottom right > select Transfer Points. 3.6 yuu Points converts to 1 KrisFlyer mile, but you need a minimum of 200 yuu Points for one conversion. There’s no conversion fee.

Screenshots from my own yuu app as of 30 Oct 2025

5. DBS yuu Card: Which are the participating merchants?

You can find the full list of participating merchants in the DBS yuu Card terms and conditions, clause 8:

Participating merchant | Defined as transactions made in Singapore at: |

|---|---|

Cold Storage | Cold Storage, CS Fresh, Jasons Deli |

Giant | Giant, Giant Hypermart, Giant Express |

Guardian | Guardian |

7-Eleven | 7-Eleven |

foodpanda | foodpanda food delivery, panda mart, panda shops |

Gojek | Gojek Singapore |

SimplyGo | Bus and train rides via SimplyGo |

Charge+ | Charge+ Singapore |

CHAGEE | Orders placed via CHAGEE App |

Singtel | Singtel Shop, Singtel Exclusive Retailers |

6. Should I get the DBS yuu Card?

If you live in Singapore and spend most of your week toggling between grocery runs, Chagee breaks, and public transport rides, then yes—the DBS yuu Card still makes a strong case for itself. Between up to 18% cashback or 10 miles per dollar, it remains one of the most rewarding cards for everyday local spending.

Get the DBS yuu Card if you:

- Spend regularly at Cold Storage, Giant, CS Fresh, Guardian, 7-Eleven, foodpanda, Gojek, or SimplyGo for your daily commute.

- Can comfortably hit $800 a month in spending and make purchases at 4 different participating merchants each month to unlock the maximum rewards.

- Like flexibility—you can redeem yuu Points as cash rebates, KrisFlyer miles, or even merchant rewards via the yuu app.

Don’t get the DBS yuu Card if you:

- Struggle to hit $800 across multiple merchants. The top earn rate only kicks in once you meet both the spend and merchant conditions.

- Plan to spend well above $800 monthly expecting higher returns—the bonus rewards are capped at 28,800 yuu Points per month, which is equivalent to about $800 of spending (worth up to $144 cashback or 8,000 miles).

- Prefer straightforward cashback that’s instantly offset against your bill—this card’s reward system involves some app wrangling and conversions.

- Used to rely on BreadTalk, Toast Box, Thye Moh Chan, or Mandai Wildlife Group for bonus rewards—these no longer qualify.

Bottom line: If your day-to-day life revolves around yuu partner merchants, the DBS yuu Card still packs heavyweight value. But if you’d rather not think about spending thresholds and caps, there are simpler cashback cards out there.

7. DBS yuu Card promotion

- at participating merchants with no min. spend

- 5% Cash Rebates

- spend min. S$800 & at 4 participating merchants per calendar month

- Up to 18% Cash Rebates

- on all other spend

- 0.25% Cash Rebates

- at participating merchants with no min. spend

- 5% cash rebates

- spend min. S$800 & at 4 participating merchants per calendar month

- Up to 18% cash rebates

- on all other spend

- 0.25% cash rebates

Convinced the DBS yuu Card deserves a spot in your wallet? These welcome gifts will make the deal even sweeter.

New cardmembers can choose between a Samsonite FLATFORM Spinner 28" with Foldable Duffle Bag (worth $740, promo code SAMDBS) or $288 cashback (promo code CASH288).

To qualify:

- Apply with your chosen promo code.

- Charge a minimum spend of $800 to your card within 60 days of card approval.

- Have a valid DBS PayLah! account by the end of the qualifying spend period.

- Apply during the promotion period (1 March 2026–30 June 2026) and be approved by 14 July 2026.

View the DBS yuu Visa Card and DBS yuu American Express® Card pages for the latest promotions.

8. Is the DBS yuu Card really that good?

The DBS yuu Card still earns its place among the best cards for everyday local spending in Singapore—the addition of HeyMax as a miles partner only sweetens the deal, even as the merchant list has tightened slightly. If your spending naturally falls within the yuu ecosystem, it remains hard to beat. I mean, 18% cash rebate and 10 miles per dollar are extremely good rates. You do need to spend $800 a month to unlock these rates, but a lot of adults in Singapore would hit this anyway (have you seen our cost of living these days? Sob.)

Even if you don’t, you’d still be earning fair rates at the participating stores—5% cash rebate or 2.8 miles per dollar. These are very decent rates especially when you consider that you’re earning them with no minimum spend required.

Let’s talk cash rebate first. Most of the time, $0 minimum spend cashback cards fall into the category of unlimited cashback cards and earn you between 1.5% to 1.7% cashback (Standard Chartered Simply Cash Credit Card, Citi Cash Back+ Card, UOB Absolute Cashback Card).

To get >5% cashback, a cashback card will often require you to hit a monthly or quarterly minimum spend. For example the OCBC 365 Credit Card rewards you with 5% cashback on dining, but only if you spend $800 or more per month. So compared to cashback cards, the DBS yuu Card is exceptional.

Now let’s look at miles cards. These typically don’t have minimum spends, but local earn rates are usually around 1.1 or 1.2 miles per dollar for general spending. Because they are miles cards, the bonus miles are often for travel-related categories.

For example, the Citi Premier Miles Card earns you 10 miles per dollar on online travel bookings via Kaligo and Agoda. The KrisFlyer UOB Credit Card gets you 3 KrisFlyer miles per S$1 spend on dining, food delivery, online shopping, online travel and transport spend… but with a minimum spend requirement of $800 annually on Singapore Airlines, Scoot and KrisShop.

Finally, how does the DBS yuu Card compare to its fellow rewards cards? This is a category of card that could give the DBS yuu Card some real competition. I would consider the following cards in the next section as alternatives to the DBS yuu Card.

9. Alternatives to the DBS yuu Card

The UOB Lady's Card comes with a 2 miles per dollar base earn rate and 10 miles per dollar earn rate on a category of your choice. It also has no minimum spend. However, do note that you earn UNI$ (UOB’s rewards points currency) per every $5 spend, not per $1, which means you’re bound to have orphaned spending that you don’t earn points on.

- Base Earn Rate

- S$5 = 1X UNI$ (0.4 miles per S$1)

- Category of Choice

- S$5 = Up to 25X UNI$ (equivalent to 10 miles per S$1)

- Min. Spend

- S$0

The Standard Chartered Rewards+ Credit Card is another contender to the DBS yuu Card, and is probably a better choice if you want to use the card for overseas spending too. It doles out 10X Rewards Points per S$1 spent in foreign currency, including online spends, and 5X Rewards Points per S$1 spent in Singapore Dollars for local dining transactions. For this card, 1 Point = 0.29 miles—comparable to the 1 yuu Point = 0.28 miles of the DBS yuu Card.

- on Foreign Currency Spend

- S$1= 10X Points

- on Local Dining Spend

- S$1= 5X Points

- on All Other Spend

- S$1= 1X Point

UOB One Card: For bigger spenders, the DBS yuu Card is not such a good idea due to the bonus yuu Points cap that’s equivalent to a $800 monthly spend. If you spend $2,000 a month, get the UOB One Card for up to 10% cashback on Shopee, McDonald's (including McDelivery®), DFI Retail Group (Cold Storage, CS Fresh, Giant, Guardian, 7-Eleven and more), Grab (including GrabFood) and SimplyGo (bus and train rides).

- cashback on daily spend at McDonald's, Grab, SimplyGo & Shopee

- Up to 10%

- cashback at all grocery spend

- Up to 8%

- cashback cap a year

- Up to S$2,240

P.S. Here’s our MoneySmart credit card ranking rubric

In case you’re wondering, here’s how we decide on our credit card rankings.

Is that credit card MoneySmart? Our MoneySmart credit card ranking rubric | |

Category | Our rating |

Overall | The average rating for the credit card on the whole, calculated from the ratings for the individual categories below. Plus, we’ll give you a one-liner on who we think the credit card is best suited for. |

Earn rates: Air miles / Cashback / Rewards points | Air miles ✈️✈️✈️✈️✈️ / Cashback / Rewards points . This category looks at the depth rather than breadth of earn rates.

|

Earn categories | This category looks at the breadth rather than depth of your earnings.

|

Annual fees and charges |

|

Accessibility | Minimum income requirements:

|

Extras/periphery rewards | These include:

|

Sign-up bonus |

|

Check out our ultimate list of credit card reviews for the low-down on credit cards in Singapore.

Found this article useful? Share it with your family and friends!

Related Articles