In Singapore, cards clearly rule the payments scene. According to the FIS Global Payments Report 2023 by Worldpay, credit cards made up 36% of all point-of-sale (POS) transactions in 2022, with debit cards coming in second at 21%—edging out even cash, which accounted for 19%.

While credit cards tend to steal the spotlight with flashy sign-up bonuses and air miles, debit cards are quietly stepping up their game. Many now offer cashback, lifestyle perks, and even overseas spending features—without the pressure of minimum income requirements or the risk of snowballing interest charges. Whether you're a student, a budget-conscious spender, or simply prefer using your own money over borrowed credit, a smart debit card can go a long way.

In this guide, we’ll walk you through the best debit cards in Singapore, comparing their cashback structures, lifestyle perks, and hidden fine print—so you can pick one that actually fits how (and where) you spend.

Top debit cards in Singapore for 2025

- Summary: Comparison of debit cards in Singapore

- DBS Visa Debit Card—best for urbanites with diverse online + offline spend

- PAssion POSB Debit Card—best for yuu ecosystem users

- UOB One Debit Card—best for daily spenders with UOB savings

- OCBC Debit Card—best for cashback fans who want no limits

- Citibank Debit Mastercard—best for frequent travellers & online shoppers

- Standard Chartered XtraSaver Debit Card—best for drivers with high account balances

- HSBC Debit Card—best for HSBC users who travel often

- Maybank Platinum Debit Card—best for Singaporeans who shop across the border

- Debit cards 101: What is a debit card?

- Debit card vs credit card—what’s the difference?

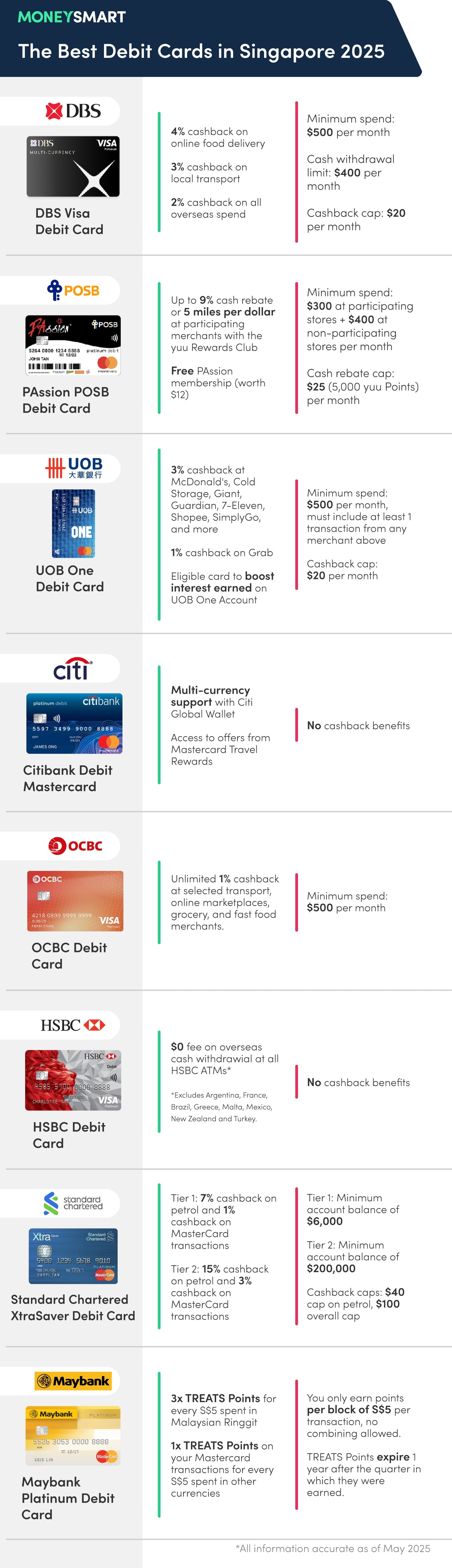

1. Summary: Comparison of debit cards in Singapore

Here’s a side-by-side look at the best debit cards in Singapore right now—so you can quickly compare what works best for your lifestyle.

Card | Key benefits | Spend requirement | Cashback / points cap | Other perks |

DBS Visa Debit Card | - 4% online food delivery | $500/month | $20/month | No FX fee when linked to My Account |

PAssion POSB Debit Card | - Up to 9% yuu rebate / 5 miles | $300 (yuu) + $400 (non-yuu) | $25/month (5,000 yuu Points) | 50% off Mandai Wildlife Reserve till 31 Dec 2025 |

UOB One Debit Card | - 3% at listed brands (McD’s, Shopee etc.) | $500/month + 1 qualifying merchant | $20/month | $3 McDonald’s coupon weekly via UOB TMRW |

OCBC Debit Card | - Unlimited 1% cashback at essentials (transport, grocery, food, online) | $500/month | No cap | Free OCBC ATM withdrawals overseas |

Citibank Debit Mastercard | - Citi Global Wallet | None | None | Multi-currency support |

SC XtraSaver Debit Card | - Up to 15% petrol cashback | Tier 1: $6,000 balance | $100/month (incl. $40 on petrol) | Free islandwide ATM withdrawals |

HSBC Debit Card | - Free HSBC ATM withdrawals overseas | None | None | Excludes some countries (e.g. FR, BR) |

Maybank Platinum Debit Card | - 3X TREATS Points for MYR spend | S$5 blocks (per transaction) | Overall account cap: 5,000,000 TREATS Points | Best value in Malaysian Ringgit (Excess points may be forfeited) |

2. DBS Visa Debit Card—best for urbanites with diverse online + offline spend

Image: DBS

The DBS Visa Debit Card offers one of the most versatile cashback schemes for everyday spenders, especially those who frequently shop online or commute via public transport. Its tiered cashback system rewards:

- 4% on online food delivery

- 3% on local transport

- 2% on overseas spend

To enjoy these perks, you'll need to hit a minimum spend of $500/month, and your cashback is capped at $20/month—so it’s best for consistent, moderate spenders. Also, you’ll need to stay under a $400 monthly cash withdrawal limit to qualify.

A major plus is its no foreign exchange fee feature when linked to a DBS My Account. This makes the card great for overseas travel or online shopping in foreign currencies.

If you’re looking for a straightforward card that rewards lifestyle spending across both local and overseas channels, this one checks a lot of boxes.

Best for: Digital natives who spend across ride-hailing, delivery, and overseas merchants.

3. PAssion POSB Debit Card—best for yuu ecosystem users

Image: POSB

The PAssion POSB Debit Card does more than just rack up points—it gives back in the form of lifestyle perks and community tie-ins. If you tie your card with the yuu Rewards Club ecosystem, you get:

- Up to 9% rebate (or 5 miles per $1) at participating yuu merchants

- Free PAssion membership (worth $12)

To maximise this card’s benefits, you need to spend $300 at yuu merchants and $400 elsewhere monthly. Your rewards are capped at $25 (5,000 yuu Points) each month—not massive, but decent for regular users.

Wondering which merchants are yuu merchants? These include BreadTalk, Cold Storage, Giant, foodpanda, Gejek, Guardian, 7-Eleven, and Toast Box.

Aside from rebates, this debit card also comes with a lifestyle perk—a 50% discount on Mandai Wildlife Reserve admission, valid till 31 Dec 2025. It’s a thoughtful extra that adds lifestyle value, especially for families.

This isn’t a catch-all cashback card, but for those who already shop within the yuu merchant network, it’s a solid pick with unique perks.

Best for: Families or regular FairPrice/Watsons/Daiso shoppers who want practical rebates and lifestyle extras.

4. UOB One Debit Card—best for daily spenders with UOB savings

Image: UOB

UOB’s One Debit Card doesn’t try to be everything to everyone—it’s sharply focused on rewarding high-frequency, small-ticket spending. Think fast food, supermarkets, and online orders:

- 3% cashback at McDonald’s, Guardian, Shopee, SimplyGo, and more

- 1% cashback on Grab

- Eligible to boost UOB One Account interest

With a $500 monthly spend requirement and $20 cashback cap, this card works best when you’re already using these brands regularly. Importantly, at least 1 qualifying transaction must be from a UOB-listed merchant to unlock the cashback. Plus, if you are already ordering McDonald’s regularly, don’t overlook the ongoing $3 McDonald’s coupon offer every Friday (via UOB TMRW).

- cashback on daily spend at McDonald's, Grab, SimplyGo & Shopee

- Up to 10%

- cashback at all grocery spend

- Up to 8%

- cashback cap a year

- Up to S$2,240

You might be wondering how the UOB One Debit Card is related to the infamous UOB One Account or the UOB One Card, its credit card cousin. While most pair the UOB One Account with the credit card to unlock higher interest rates on their savings, the UOB One Debit Card is also eligible to earn you extra interest on the high-yield savings account. Read more in our review of the UOB One account.

All in all, this card isn’t for big spenders or jetsetters, but it nails the day-to-day value proposition.

Best for: Daily spenders who rely on UOB One Account and want cashback on routine purchases.

5. OCBC Debit Card—best for cashback fans who want no limits

Image: OCBC

If you hate fiddling with complex tiers and hidden restrictions, the OCBC Debit Card’s flat cashback model is refreshingly simple. Spend $500 a month and you’ll earn unlimited 1% cashback at useful merchants:

- Transport: Grab, ComfortDelGro, GoJek, SimplyGo

- Online: Lazada, Shopee

- Groceries: NTUC FairPrice and FairPrice Online

- Fast food: McDonald’s, Subway, Toast Box, etc.

There's no cashback cap, which makes it one of the most fuss-free rewards systems among debit cards in Singapore. You’ll get reliable returns on essentials without having to jump through hoops.

The one qualifier I want to add is that if you meet the minimum income requirement for credit cards instead, there are better unlimited, no minimum spend cashback credit card options out there. These will earn you limitless cashback on almost everything—not just your daily essentials. For example, OCBC has its own OCBC INFINITY Cashback Card, and Citi has the Citi Cash Back+ Card, both of which earn you 1.6% cashback.

- on eligible transactions

- Earn 1.6% Cashback

- Min. Spend

- S$0

- Cashback Cap

- Unlimited

Get $250 Cash or 3,900 SmartPoints (enough to redeem an Apple AirPods Pro 3 worth S$349) when you apply and spend a min. of S$400 within 30 days! T&Cs apply.

- Cash Back on Eligible Spend

- 1.6%

- Min. Spend per month

- S$0

- Cash Back Cap per month

- Unlimited

Apply and spend S$500 within 30 days to choose your reward: UPSIZED S$400 Cash Reward or 6,140 SmartPoints (worth up to S$499 of Gifts) and receive them as quickly as 5 weeks after meeting the spend criteria!

PLUS, double your excitement with a chance to win the ultimate S$15,000 getaway to your dream destination in our exclusive lucky draw! T&Cs apply.

But back to the OCBC Debit Card, which is great for those who aren’t eligible for credit cards or don’t want the fuss of paying credit card bills. With the OCBC Debit Card, OCBC also throws in free cash withdrawals at overseas OCBC ATMs, which is a useful perk for occasional travellers.

If you prefer predictability and shop frequently across household brands, this card offers great long-term utility with minimal upkeep.

Best for: No-frills users who want steady cashback on groceries, transport, and food—without limits.

6. Citibank Debit Mastercard—best for frequent travellers & online shoppers

The Citibank Debit Mastercard doesn’t offer cashback—but that’s not its value proposition. What it lacks in rebates, it makes up for in cross-border utility and travel perks.

- Multi-currency wallet via Citi Global Wallet

- Exclusive deals through Mastercard Travel Rewards

This card is useful for those who spend in foreign currencies or hop countries regularly. By letting you hold and pay in multiple currencies, it helps dodge unnecessary conversion fees and fluctuations.

The lack of cashback may be a deal-breaker for some, but if you’re simply looking for seamless travel functionality and access to Mastercard’s perks, it delivers.

Otherwise, you can always check out multi-currency cards to avoid foreign currency fees.

Best for: Frequent travellers or digital nomads who want hassle-free multi-currency support.

7. Standard Chartered XtraSaver Debit Card—best for drivers with high account balances

The XtraSaver Debit Card offers high cashback potential, especially if you own a car. Its 2-tier system rewards account holders based on their savings:

Account balance requirement | Petrol cashback | Other Mastercard spend cashback | Monthly cashback cap |

Minimum $6,000 | 7% | 1% | Up to $100, with $40 petrol sub-limit |

Minimum $200,000 | 15% | 3% |

Beyond that, you get free ATM withdrawals islandwide, thanks to access to atm5 machines.

The higher tier may be out of reach for most, but even the base tier offers good returns for drivers—especially given petrol prices. The Mastercard cashback sweetens the deal if you use the card for regular transactions.

This card won’t appeal to low spenders or those without vehicles, but for motorists, the rewards stack up nicely.

Best for: Drivers with higher account balances who want strong cashback on petrol and daily spend.

8. HSBC Debit Card—best for HSBC users who travel often

Like the Citibank Debit Mastercard, there are no flashy rebates here—but the HSBC Debit Card prioritises global ATM access over cashback. Key features include:

- Free withdrawals at HSBC ATMs worldwide

- Access to over 2.3 million Visa/Plus ATMs globally

It's worth noting that some countries are excluded from the free withdrawal benefit, so always check the fine print. These countries include: Argentina, France, Brazil, Greece, Malta, Mexico, New Zealand and Turkey.

Still, the card offers peace of mind for travellers. You won’t have to worry about ATM fees sneaking up on you during overseas trips, and it’s super convenient to just whip out your regular debit card and tap to pay. However, if you’re a cashback hunter or local spender, this won’t offer much.

Best for: HSBC customers who travel regularly and want fee-free global ATM access.

9. Maybank Platinum Debit Card—best for Singaporeans who shop across the border

Image: Maybank

Maybank’s Platinum Debit Card is a quiet player in the market, but it offers decent cross-border rewards—especially if you shop across the Causeway.

- Earn 3X TREATS Points per S$5 spent in Malaysian Ringgit

- 1X TREATS Point per S$5 in other currencies

The biggest drawback? You only earn in blocks of S$5, and there’s no rounding up—so micro-transactions don’t count. You also can’t combine transactions to form $5 blocks. This makes the card less friendly for digital wallets or splitting bills.

Still, if you spend in Malaysia regularly—say, for shopping, dining, or petrol—this can help you accumulate rewards faster than typical SG-based cards.

While Maybank doesn’t state a monthly cap for their TREATS Points on the Maybank Platinum Debit Card, there is an overall accumulation limit of 5,000,000 TREATS Points. Redeem your TREATS Points before you hit this ceiling, because Maybank will forfeit any points earned in excess of this amount.

You also want to redeem your TREATS Points before they expire. This is 1 year from the quarterly period in which they were earned for most Maybank customers. But for Visa Infinite, World Mastercard Cardmembers enrolled into the Rewards Infinite programme, TREATS Points never expire.

Best for: Singaporeans who frequently shop or travel in Malaysia and want to earn loyalty points on every trip.

10. Debit cards 101: What is a debit card?

These days, banks simply eschew the traditional ATM card (the one you use to withdraw cash) and just issue account-linked debit cards to bank account holders. Generally, debit cards are accepted wherever credit cards are. They work on the same credit card networks, either Visa or Mastercard.

When you charge a purchase to your debit card on Visa or Mastercard, the funds are deducted directly from your bank account. This process might take a few days (so you might not see a dent in your bank balance immediately after making a purchase) but it will happen automatically.

The difference between debit and credit card is that when you use a debit card, the money is directly debited from your savings account. When paying via a credit card, you are using credit, or "future money", as you will only pay for the purchases at the end of your billing cycle month, when a consolidated credit card monthly statement is sent.

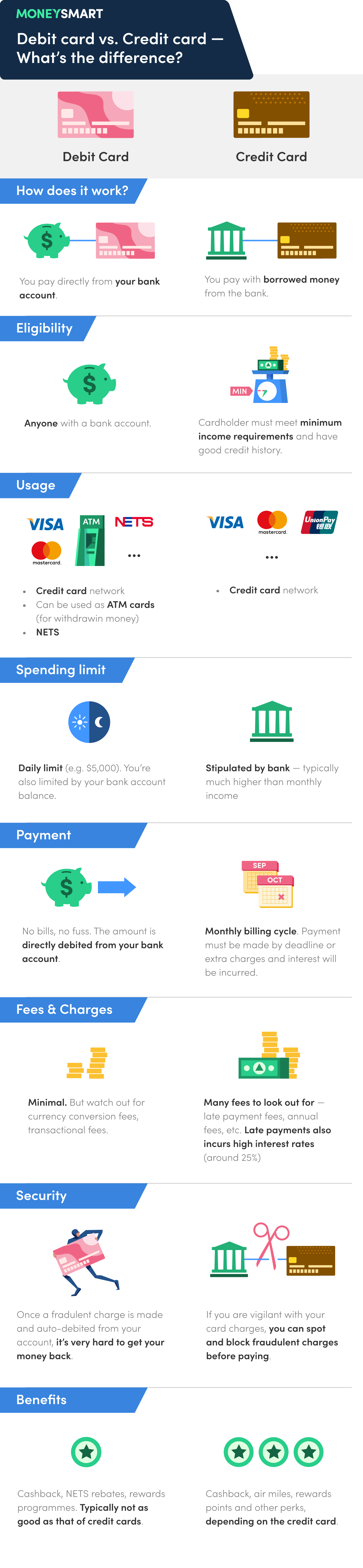

11. Debit card vs credit card—what’s the difference?

Here’s a quick cheat sheet to the difference between credit cards and debit cards:

Debit Card | Credit Card | |

Mechanics | Pay directly from bank account | Pay with borrowed money from bank |

Eligibility | Anyone with a bank account | Cardholder must meet minimum income requirements and have good credit history |

Usage | Accepted on credit card network. Many debit cards can also be used as ATM cards (to withdraw cash) and for NETS | Accepted on credit card network |

Spending limit | Daily limit (e.g. $5,000). You’re also limited by your bank account balance | Stipulated by bank - typically much higher than monthly income |

Payment | No bills, no fuss. The amount is directly debited from bank account | Monthly billing cycle. Payment must be made by deadline or extra charges and interest will be incurred |

Fees & charges | Minimal. But watch out for currency conversion fees, transaction fees | Many fees to look out for - late payment fees, annual fees, etc. Late payment also incurs high interest rates (around 25%) |

Security | Once a fraudulent charge is made and auto-debited from your account, it’s very hard to get your money back | If you are vigilant with your card charges, you can spot and block fraudulent charges before paying |

Benefits | Cashback, NETS rebates, rewards programmes. Typically not as good as that of credit cards | Cashback, air miles, rewards points and other perks, depending on the credit card |

You can pay for the same pair of shoes using a debit card or a credit card. In both cases, you key in the card number and security details (e.g. a CVV2 number). The key difference lies in what happens after that charge is made.

When you use a credit card, you pay with borrowed money from the bank. The bank pays the merchant for your shoes. At the end of the month, the bank will ask you to return the money.

That’s why it’s harder to get a credit card than a debit card - the former usually has some sort of minimum income requirement. The banks want to make sure that you actually have the means to pay them back.

Found this article useful? Share it with your family and friends!

Related Articles