With plan names like Adogable, Ameowing, Furtastic, Ultipaw, and Pawsh, Liberty PetCare doesn’t exactly shy away from purr-sonality. But more importantly, beyond the themed tiers sits one of the more comprehensive pet insurance offerings in Singapore.

Premiums start from $392.40 per year for both dogs and cats, and pets can enrol from as young as 8 weeks old up to below 9 years—making it one of the more flexible options age-wise. At the top end, the Pawsh Plan costs $1,471.50, though Liberty offers no-claim discounts of up to 15%, which can reduce long-term costs.

Where Liberty truly differentiates itself is in its accident coverage, accidental death benefits, and wellness care perks—areas that many competitors either limit or exclude entirely.

So how does Liberty stack up against Income, MSIG, and others? Let’s break down its coverage, costs, fine print, and who it’s best suited for.

[ms-toc title="Liberty PetCare pet insurance—MoneySmart review (2026)"]

1. How much does Liberty PetCare pet insurance cost?

- Premium: Starting from $392.40 (dogs and cats)

- Eligible age: 8 weeks to below 9 years

Liberty sits comfortably in the mid-to-premium range. It’s not the cheapest option, but it also isn’t priced at the very top of the market unless you opt for the highest Pawsh tier.

Here’s how the tiers break down annually:

Plan tier | Adogable Plan | Ameowing Plan | Furtastic Plan | Ultipaw Plan | Pawsh Plan |

Annual premium | $392.40 | $504.67 | $840.39 | $1,016.97 | $1,471.50 |

Prices above are flat rates and exclude no-claim discounts of 5%, 10% and 15% in the event no claim is made under the policy in the preceding 1, 2 and 3 consecutive years respectively.

As you move up the tiers, you’re mainly paying for higher medical limits and additional benefits like wellness care.

One thing worth noting is Liberty’s no-claim discount, which rewards you for claim-free years:

- 5% after 1 year

- 10% after 2 consecutive years

- 15% after 3 consecutive years

If your pet stays healthy, that discount can meaningfully lower your long-term cost.

Looking to get your fur kid protected? Check out our other pet insurance reviews and guides.

|

2. What does Liberty PetCare pet insurance cover?

Image: Liberty Insurance

Liberty’s strength lies in breadth. It doesn’t just focus on surgery or illness—it tries to offer protection across accidents, death, liability, and even routine care.

Let’s break it down.

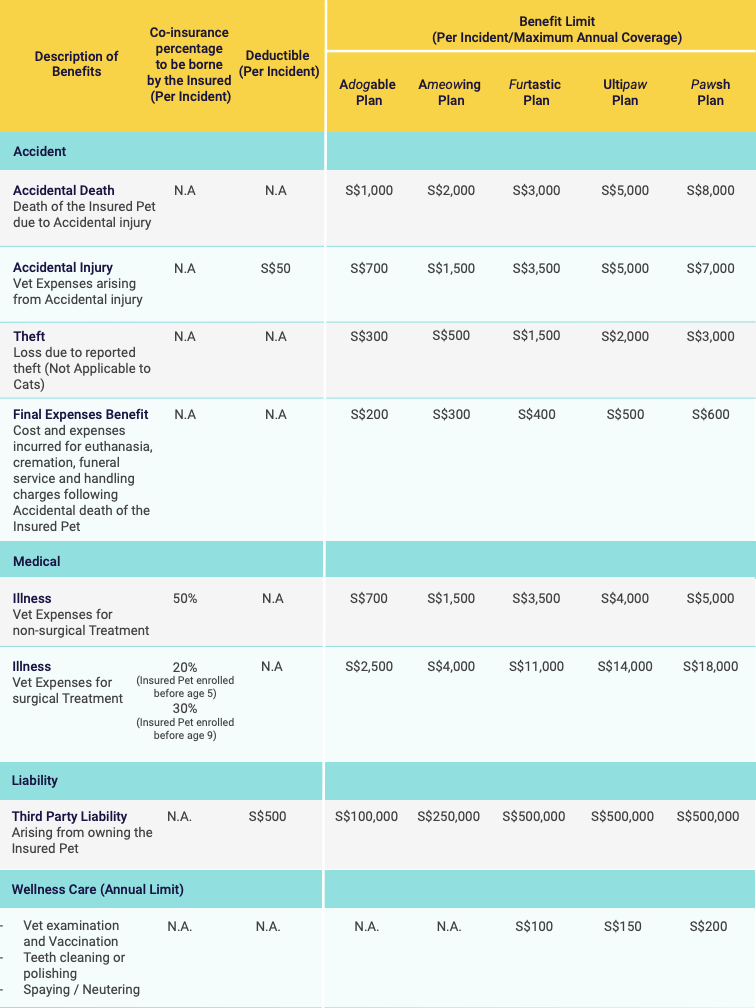

Accidental injury

Accident coverage is included at every plan tier, which already gives Liberty an advantage over some competitors.

- $700 – $7,000 per incident

- $50 deductible per accident claim

- No co-insurance for accident claims

In practical terms, this means if your dog swallows something it shouldn’t and needs emergency treatment costing $2,000, you only pay the $50 deductible, and Liberty covers the rest (up to your plan limit). There’s no percentage-sharing on top of that.

Accidental death

- $1,000 – $8,000

This is a lump-sum payout if your pet passes away due to an accident. Only CIMB and Liberty provide this among the 6 insurers we reviewed.

For pet owners, this benefit can help you with miscellaneous costs during the grieving process or unexpected financial strain during a difficult time.

Theft (dogs only)

- $300 – $3,000

If your dog is stolen and a police report is filed, Liberty provides compensation within your plan limit. Theft cover isn’t common in Singapore pet insurance, so this adds another layer of protection.

Note: This does not apply to cats.

Final expenses

- $200 – $600

This benefit covers costs such as euthanasia, cremation, and related handling charges. While the payout is lower than Income’s final expenses benefit, Liberty also provides a separate accidental death benefit—which together can provide more comprehensive end-of-life financial support.

Illness coverage

Medical illness benefits are split into two categories:

Non-surgical treatment

- $700 – $5,000

- 50% co-insurance

Surgical treatment

- $2,500 – $18,000

- 20% co-insurance (enrolled before age 5)

- 30% co-insurance (enrolled before age 9)

Surgical limits are competitive at higher tiers. However, the 50% co-insurance for non-surgical claims is something to think about—especially if your pet develops a chronic condition requiring ongoing medication.

Third party liability

- $100,000 – $500,000

This protects you if your pet injures someone or damages property and you’re held legally responsible.

However, for certain breeds—including Pit Bull, Akita, Mastiffs, Bull Terrier, Doberman Pinscher, Rottweiler, and German Shepherd—the maximum liability is capped at $100,000 regardless of tier.

Compared to Income’s $1,000,000 maximum, Liberty’s limits are more modest.

Wellness care

This is where Liberty quietly stands out.

Available only on the top 3 tiers, wellness coverage ranges from:

- $100 – $200 per year

It covers:

- Vet examinations

- Vaccinations

- Teeth cleaning or polishing

- Spaying or neutering

While $200 won’t stretch far, it’s still unusual to see preventive care reimbursed at all. If you’re already paying for routine visits, this can offset some of that cost.

ALSO READ: How Does Pet Insurance Work in Singapore? 10 Frequently Asked Questions

3. What will you actually pay when claiming?

Liberty’s cost-sharing depends on the type of claim.

For accident, liability, and wellness claims, there is:

- No co-insurance

- A $50 deductible for accident claims

That makes these claims simple and predictable.

For illness claims, you’ll share more of the bill:

- 50% co-insurance for non-surgical treatment

- 20%–30% co-insurance for surgical treatment

For example, if your non-surgical bill is $1,000, you’ll pay $500 and Liberty pays $500. If your surgical bill is $5,000 and your co-insurance is 20%, you’ll pay $1,000 and Liberty covers $4,000.

This structure means Liberty works best for high-cost, one-off events rather than frequent smaller illness treatments.

4. What is not covered in Liberty PetCare pet insurance?

Like all pet insurance policies in Singapore, Liberty PetCare has exclusions you should understand before signing up.

Liberty does not cover:

- Pre-existing conditions — any illness or injury diagnosed before your policy starts will not be claimable. This makes early enrolment important, especially for breeds prone to hereditary issues.

- Routine care beyond the wellness limits — while Liberty uniquely includes wellness benefits in its higher tiers, once you exceed the $100–$200 annual cap, additional routine costs (like vaccinations or dental cleaning) come out of pocket.

- Theft for cats — theft coverage applies only to dogs.

- Working, racing, or commercial pets — pets used for guarding, breeding, or other commercial activities are excluded.

Liberty also does not provide unlimited third party liability coverage. Limits range from $100,000 to $500,000, and for certain breeds—such as Pit Bull, Akita, Mastiffs, Bull Terrier, Doberman Pinscher, Rottweiler, and German Shepherd—the cap is reduced to $100,000 regardless of plan tier.

If liability protection is your main concern, particularly if you own a larger or “iffy” breed, it’s worth comparing this carefully against insurers offering higher maximum limits.

5. Eligibility: Which pets can apply for Liberty PetCare pet insurance?

To qualify for Liberty PetCare, both the pet and the owner must meet specific requirements.

The insured pet must:

- Be at least 8 weeks old and below 9 years old at the start of the first policy period

- Be microchipped and licensed

- Be residing regularly at the same premises as the insured in Singapore

- Have completed all required vaccinations

- Not be a working pet (e.g. guide dog, hunting dog, guard dog) or racing dog

- Not be used for breeding purposes

The minimum entry age of 8 weeks makes Liberty one of the few insurers that allows very early enrolment—ideal for new puppy or kitten owners looking to secure coverage before medical issues arise.

The insured (policyholder) must:

- Be the registered owner of the pet and the named policyholder

- Be a Singapore Citizen, Permanent Resident, or a foreigner holding a valid Work Permit, Employment Pass, Dependant’s Pass, Student Pass, or Long-Term Visit Pass

Overall, Liberty’s eligibility criteria are straightforward and in line with industry norms, with the added advantage of early enrolment from just 8 weeks old.

6. Pros and cons of Liberty PetCare pet insurance

When you step back, Liberty offers a broad mix of benefits—but with some clear trade-offs.

Pros

- Accident coverage at every tier

- Strong accidental death benefit

- Theft cover for dogs

- Wellness care benefit

- No co-insurance for accident or liability claims

- No-claim discounts up to 15%

Cons

- 50% co-insurance for non-surgical illness

- Liability limits lower than some competitors

- Breed-specific liability cap

- Wellness limits relatively modest

7. Who should buy Liberty PetCare pet insurance?

Liberty may be a good fit if you:

- Want strong accident protection without complex cost-sharing

- Value theft and accidental death benefits

- Like having some support for routine care

- Are enrolling a young pet from 8 weeks old

It works especially well for owners who want practical, wide-ranging coverage beyond just surgery. However, if your biggest concern is reducing out-of-pocket illness expenses, you’ll want to factor in the co-insurance carefully.

8. Final verdict: Is Liberty PetCare pet insurance good value?

Liberty PetCare strikes a balance between breadth and practicality. Its accident structure is refreshingly straightforward, and features like theft and wellness care give it a wider safety net than many competitors.

However, illness claims can involve meaningful cost-sharing, and liability limits are not the highest in the market.

If you want broad protection—including accidents, death benefits, and preventive care—Liberty is one of the more well-rounded options available.

MoneySmart verdict: Liberty PetCare offers strong accident and everyday protection with clear claims structure, but illness co-insurance and moderate liability limits mean it’s best for owners comfortable sharing medical costs. |

For more information, view Liberty PetCare brochure and policy wording.

This article was first drafted with the help of AI and later reviewed and refined by the author.

Found this article useful? Share it with your fellow pawrents!

Related Articles