MSIG PawEasy is one of the more comprehensive pet insurance plans in Singapore, particularly when it comes to hospitalisation and surgery coverage. Premiums start from $604.26 for dogs and $241.95 for cats, with pets eligible from 16 weeks up to 9 years old.

While dog premiums sit in a similar range to Income’s before discounts, MSIG stands out for offering a notably more affordable entry point for cats. And with a no claim discount of up to 15% for healthy pets, the pricing becomes even more competitive.

Where PawEasy differentiates itself is in its structured, end-to-end approach to medical care—covering pre-surgery consultations, post-surgery treatment, complementary therapy, and even pet mobility aids.

Let’s break down its coverage, costs, add-ons, and whether it’s worth it.

[ms-toc title="MSIG PawEasy pet insurance—MoneySmart review (2026)"]

1. How much does MSIG PawEasy pet insurance cost?

- Premium: Starting from $604.26 (dogs) / $241.95 (cats)

- Eligible age: 16 weeks to 9 years

MSIG PawEasy pet insurance annual premiums | |||

Pet/plan tier | PawPat | PawRun | PawPlay |

Dog | $604.26 (currently $483.42 with 20% off) | $664.03 (currently $531.22 with 20% off) | $996.04 (currently $796.83 with 20% off) |

Cat | $241.95 (currently $193.56 with 20% off) | $265.87 (currently $212.70 with 20% off) | $398.82 (currently $319.05 with 20% off) |

Before discounts, dog pricing is broadly comparable to lower tiers from other insurers, such as Income Happy Tails pet insurance. However, MSIG is noticeably more affordable for cats at entry level.

The current 20% promotion lowers premiums significantly, but remember that renewal pricing may differ.

Looking to get your fur kid protected? Check out our other pet insurance reviews and guides.

|

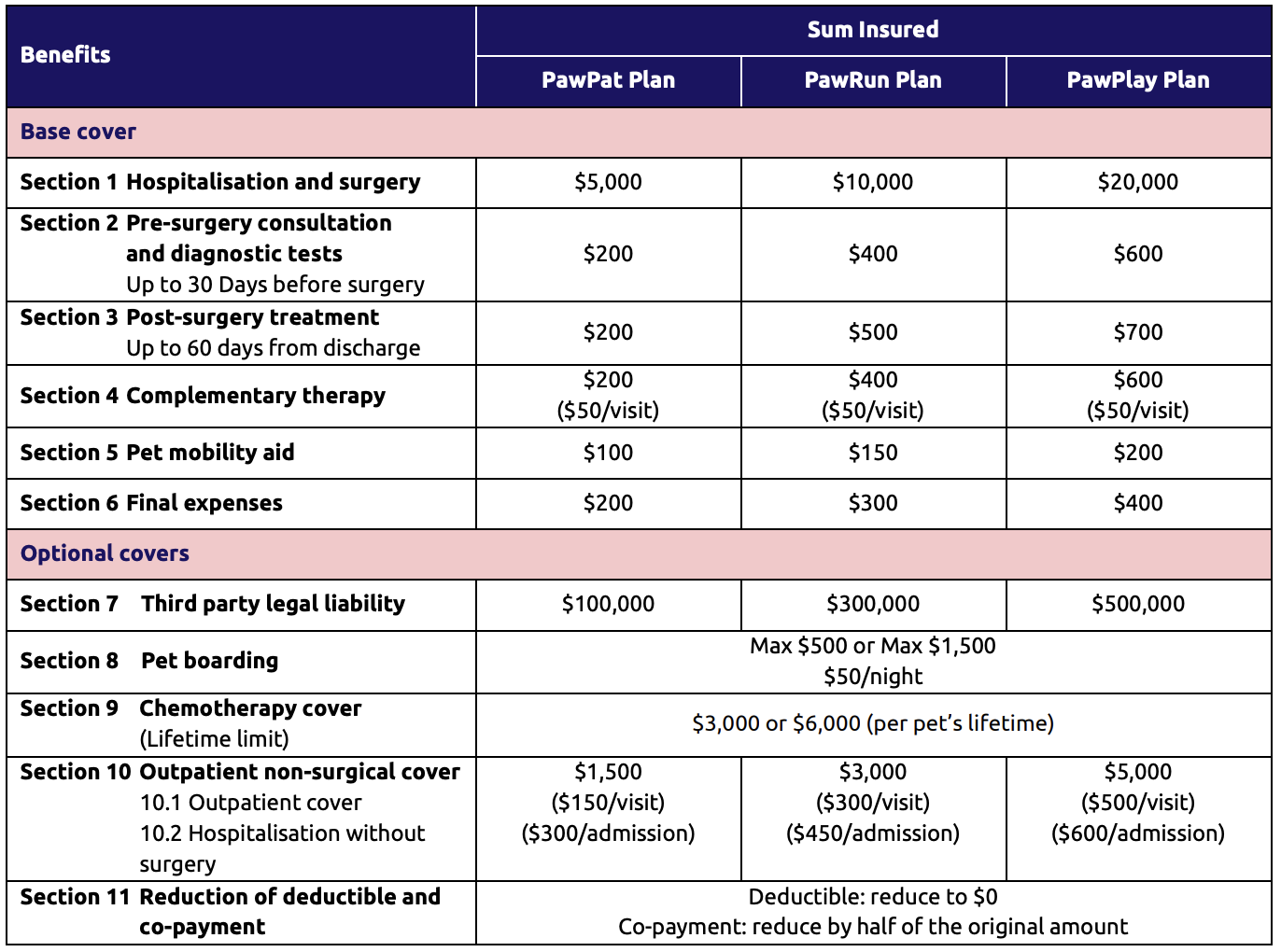

2. What does MSIG PawEasy pet insurance cover?

Image: MSIG

MSIG structures its coverage thoughtfully, with strong core medical benefits and several less common extras.

Hospitalisation and surgery

Hospitalisation and surgery are the foundation of MSIG PawEasy, coming in strong with high annual base coverage:

- $5,000 – $20,000 (depending on tier)

The top-tier PawPlay plan offers up to $20,000 in hospitalisation and surgery coverage per policy year.

What’s particularly strong is that MSIG separates out:

- Pre-surgery consultation and diagnostics: up to $600

- Post-surgery treatment: up to $700

This means your pet is covered before, during, and after major surgery—not just for the operation itself.

Complementary therapy

- $200 – $600

- $50 per visit

Covers treatments such as acupuncture, chiropractic care, and physiotherapy. These therapies are increasingly common in recovery plans but aren’t widely covered by insurers.

Pet mobility aid

- $100 – $200

This covers assistive devices like wheelchairs or mobility supports if your pet needs help after injury or surgery. It’s a niche benefit, but a thoughtful one.

Final expenses

- $200 – $400

This helps cover euthanasia, cremation, or related handling costs. The limits are around average compared to the market.

However, unlike Liberty or CIMB, MSIG does not offer an accidental death benefit or theft coverage. While this isn’t uncommon, it does reduce MSIG’s overall strength for end of life-related coverage.

3. Optional add-ons

MSIG keeps several key benefits as optional covers. This gives you flexibility—but it also means the base plan may feel lighter compared to some competitors.

Here’s how the add-ons stack up.

Third party liability (optional)

- $100,000 – $500,000

This covers legal liability if your pet injures someone or damages property. Some insurers—like Income—include liability in their base plans. With MSIG, you must opt in. The upside is flexibility; the downside is extra cost if liability coverage is important to you.

Chemotherapy cover (optional)

- Lifetime limit of $3,000 or $6,000 per pet

Many lower-cost plans don’t cover chemotherapy at all. Income includes it as a standard annual benefit, while MSIG offers it as an add-on—but importantly, it’s structured as a lifetime limit, not an annual one. That can be helpful for long-term cancer treatment planning, though you’ll need to decide if the additional premium makes sense for your pet’s risk profile.

Outpatient non-surgical cover (optional)

- Up to $5,000

- Per-visit and per-admission sub-limits apply

Some insurers bundle outpatient care into core coverage, while others exclude it entirely. MSIG places it behind an add-on. If your pet develops a chronic condition requiring regular medication or check-ups, this rider becomes more valuable. Without it, coverage focuses mainly on surgery-based treatment.

Pet boarding (optional)

- Up to $1,500

- $50 per night

This covers boarding costs if you’re hospitalised and unable to care for your pet. Very few insurers in Singapore include boarding benefits, making this a relatively uncommon feature. It won’t apply to most claims—but when needed, it can be practical.

Reduction of deductible and co-payment (optional)

This rider:

- Reduces deductible to $0

- Cuts co-payment by half

Not all insurers offer a way to reduce cost-sharing. With MSIG, you can effectively “buy down” your out-of-pocket exposure. For owners concerned about large surgical bills, this can meaningfully change the financial equation.

The downside to these add-ons is that your premium will increase accordingly. When I tried adding all optional covers, my quote for the top-tier PawPat plan for my cat went from $241.95 to $426.14 before discounts.

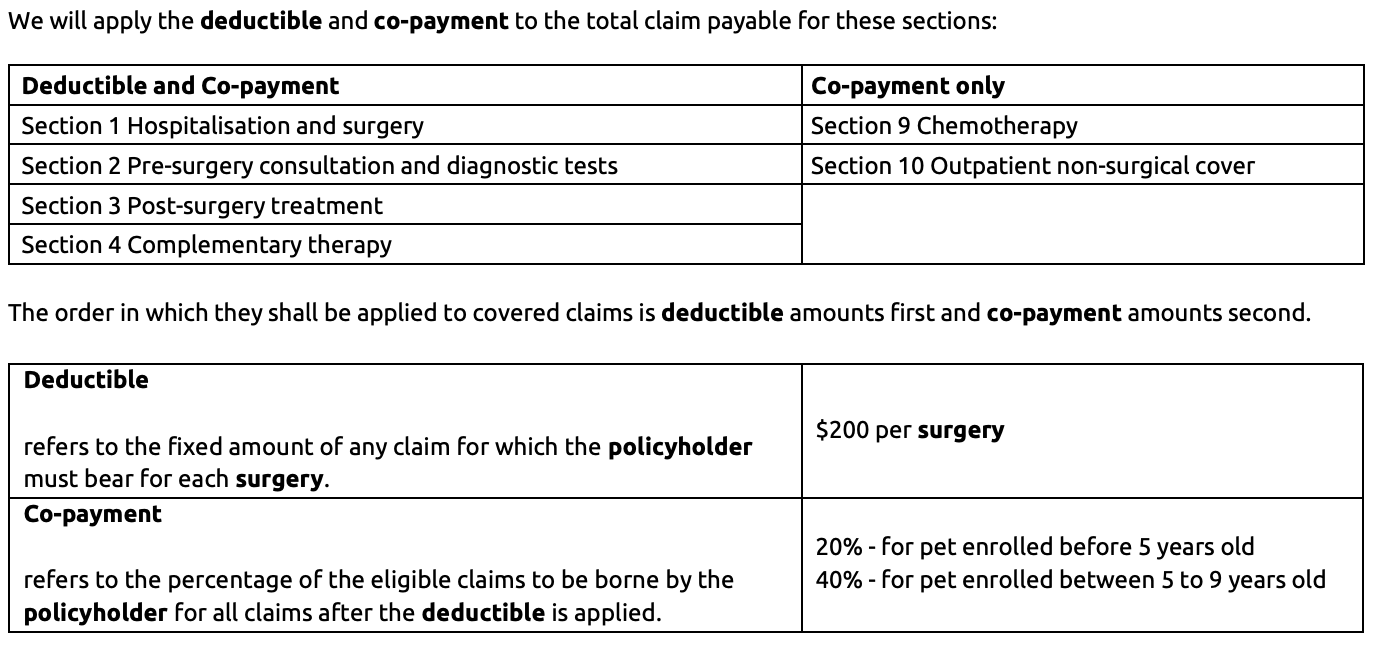

4. What will you actually pay when claiming from MSIG PawEasy pet insurance?

Image: MSIG

If you do not purchase the deductible reduction rider, you’ll pay:

- $200 deductible per surgery

- Co-payment:

- 20% if enrolled before age 5

- 40% if enrolled between age 5 and 9

Here’s what that looks like in practice:

If your pet’s surgery costs $2,000:

- You first pay $200 (deductible)

- Remaining amount: $1,800

- If co-payment is 20%, you pay $360

- Total out-of-pocket: $200+ $360 = $560

If your pet is older and your co-payment is 40%, you pay $720 instead—bringing your total to $920.

That’s a meaningful difference, especially for large surgical bills.

This cost-sharing is important to factor in when comparing MSIG to plans with lower or no co-insurance on certain claims.

ALSO READ: How Does Pet Insurance Work in Singapore? 10 Frequently Asked Questions

5. What is not covered in MSIG PawEasy pet insurance?

Like most insurers, MSIG excludes:

- Pre-existing conditions

- Routine care (unless wellness add-ons are purchased elsewhere)

- Theft

- Accidental death benefit

Unlike Liberty or CIMB, there is no accidental death or theft coverage, even at higher tiers. If those risks are important to you, MSIG may feel narrower in scope unless supplemented elsewhere.

It’s also worth noting that several meaningful benefits—such as third party liability, chemotherapy, and outpatient non-surgical treatment—are not included by default. While this gives you flexibility to customise your coverage, it does mean the base plan focuses heavily on surgery and hospitalisation rather than broad, all-in protection.

In other words, MSIG’s core strength is structured medical care—but you’ll need to opt in if you want wider lifestyle or liability coverage.

6. Eligibility: Which pets can apply for MSIG PawEasy pet insurance?

To enrol in MSIG PawEasy, your pet must meet the following criteria:

- Age: 16 weeks to 9 years at policy start

- Must be microchipped and licensed (for dogs)

- Must reside in Singapore

- Must complete required vaccinations

- Not used for racing, breeding, or commercial purposes

The maximum entry age of 9 years is in line with most major insurers, which means you don’t necessarily need to rush into purchasing coverage when your pet is very young—though earlier enrolment typically results in lower co-payment rates.

MSIG does not advertise a mandatory pre-enrolment medical examination in the same way Income does, which makes sign-up comparatively straightforward. That said, like all insurers, any pre-existing condition diagnosed before coverage starts will not be covered—so applying while your pet is healthy can make a meaningful difference to long-term protection.

7. Pros and cons of MSIG PawEasy pet insurance

Before deciding if MSIG PawEasy pet insurance is worth it for you and your pet(s), here’s a look at how it balances out.

Pros

- Strong hospitalisation and surgery limits (up to $20,000)

- Separate pre- and post-surgery coverage

- Complementary therapy included

- Pet mobility aid benefit

- More affordable for cats

- Flexible optional add-ons

Cons

- $200 deductible per surgery

- 20%–40% co-payment

- No accidental death or theft benefit

- Key benefits like liability and chemotherapy are add-ons

MSIG’s strength lies in its structured, medical-first design—particularly the way it separates pre- and post-surgery care rather than bundling everything into a single cap. However, because many meaningful benefits sit behind optional riders, the plan’s overall value depends heavily on how much customisation you’re prepared to pay for.

8. Who should buy MSIG PawEasy pet insurance?

MSIG PawEasy may suit you if:

- You want strong surgical coverage

- You value structured, comprehensive medical care

- You own a cat and want a competitively priced plan

- You prefer customising coverage via add-ons

It’s especially attractive for owners who want thoughtful extras like complementary therapy or mobility aids.

However, if minimising out-of-pocket surgical costs is your top priority, you’ll want to carefully consider the deductible and co-payment structure.

9. Final verdict: Is MSIG PawEasy pet insurance good value?

MSIG PawEasy offers strong all-round medical protection with well-designed surgical benefits and thoughtful extras like complementary therapy and mobility aid coverage. It’s particularly competitive for cats and for owners who want customisable add-ons.

That said, deductibles and co-payments can significantly increase out-of-pocket costs—especially for major surgeries—and some key protections require additional riders.

If you value structured, comprehensive coverage and don’t mind some cost-sharing, MSIG is a solid contender.

MoneySmart verdict: MoneySmart verdict: Strong surgical coverage and thoughtful extras, but deductibles and co-payments mean it’s best for owners prepared to share medical costs—and to pay more if opting for add-ons. |

For more information, view MSIG PawEasy benefit summary and policy wording.

This article was first drafted with the help of AI and later reviewed and refined by the author.

Found this article useful? Share it with your fellow pawrents!

Related Articles