This post was written in collaboration with Singtel Dash. While we are financially compensated by them, we nonetheless strive to maintain our editorial integrity and review products with the same objective lens. We are committed to providing the best recommendations and advice in order for you to make personal financial decisions with confidence. You can view our Editorial Guidelines here.

Recently on 5 Jan, one of the core banks in Singapore slashed its interest rates on its flagship savings account, the 4th round of revisions since May 2020. Other major banks had previously also slashed interest rates on their savings accounts from 1 Jan, again this was not the first time since mid-2020.Let’s just say that you’ll be lucky to find a savings account that offers realistic interest rates of 0.5% p.a. to 1% p.a. — unless you have lots of savings and you’re a big spender and/or super-user of the bank’s other services (remember the good old days when realistic interest rates were easily 1.2% p.a. to 1.5% p.a.).Even fixed deposit rates are in a slump right now, with rates as low as 0.2% p.a. and a maximum of 1.3% p.a. — we’re not even going to mention the 3- to 36-month lock-in period.All this slashing makes me feel really sian, especially when my savings account is affected. Perhaps you, like me, feel hesitant about doing anything to your savings in this uncertain climate (who knows when they will slash again?). I know I am, so my additional savings are just sitting stagnant in my bank account, collecting dust and cobwebs, and basically not growing well.I know, I know. This defeatist mindset is very bad to have. But wait...

Enter Singtel Dash’s latest product, Dash PET by Etiqa Insurance

Isn’t it timely that a new insurance savings plan from Singtel Dash with no lock-in period and capital guaranteed (up to 1.3%* p.a.) has emerged? Those who are with good numbers will know that the difference between 0.5% p.a. and 1.3% p.a. on $10,000 is $130 minus $50 equals $80 a year!If you benefitted from Singtel Dash’s popular Dash EasyEarn product; yes, this is similar (but improved!) and Singtel is teaming up again with Etiqa Insurance to roll out this exclusive new product, aptly named Dash PET (Protect, Earn, Transact).It’s easy to get started with Dash PET, especially if you already have the Singtel Dash app and you’re at least 17 years old. There’s also a low barrier to entry as you only need to put in and maintain at least $50 to reap the rewards — top up any time via your Dash wallet, eNETs or PayNow.Read on to find out more about what Dash PET offers.

PROTECT

Dash PET offers an insurance component of up to 105% of your policy value for death. This means, if you put $10,000 in your PET account, the total payout is $10,000 plus 5% of that, which is an additional $500.This is pretty standard for most insurance savings plans, which brings us to the next protective feature — the Covid-19 Financial Assistance Benefit, provided free to all Etiqa Insurance life insured. Upon diagnosis, this includes a hospitalisation benefit up to $1,000, intensive care unit benefit up to $1,000, and a lump sum death benefit of $50,000.We also heard that there could be additional coverage for yourself and your lifestyle coming later this year, where you can add on protection riders and be rewarded with additional returns on your first $10,000 of your Dash PET account value. Stay tuned for more updates when it launches!

EARN (the biggest draw of Dash PET plan for now)

The earn rate is the crux of any insurance savings plan. As we highlighted above, savings interest rates are rather dismal at the moment. Taking advantage of Dash PET’s up to 1.3%* p.a. return is a shining beacon of hope for our stagnant savings.

- Minimum account value: $50

- Maximum account value: $30,000

- Attractive 1.3%* p.a. returns for the first $10,000

- 0.3%* p.a. returns for account value above the first S$10,000

- Capital guaranteed

- No lock-in period: Top-up or withdraw anytime, from just $1 (min. S$50 for eNETS top-up)

- Top-up easily done via Dash wallet, eNETS, PayNow

- Withdraw funds easily using Dash wallet (free) or PayNow ($0.70 admin fee applies per withdrawal via PayNow)

Scenario 1 — you have $30,000 spare cash

If you top up $30,000 as a lump sum amount, that’s the best case scenario as you can maximise your returns.

Premium | Crediting rate | Total Earned interest after 1 year |

First $10,000 | 1.3%* p.a. | $190 |

Above $10,000 | 0.3%* p.a. | |

Total interest earned | ||

Scenario 2 — you’re a student/first-jobber who makes regular, small top-ups

Don’t currently have $30,000? You can always get started with $50, then make small $100 top-ups to the account value at the start of each month — it’s super-flexible as there are no fees payable; while you won’t achieve the maximum returns possible, you will STILL reap the returns nonetheless.

Month | Total top-up amount | Crediting rate | Earned interest |

1 | $50 (minimum to start) | 1.3%* p.a. | $0.05 |

2 (assume 28 days) | $150 | $0.16 | |

3 | $250 | $0.27 | |

4 | $350 | $0.38 | |

5 | $450 | $0.49 | |

6 | $550 | $0.60 | |

… | (Continue to add $100 per month) | … | |

12 | $1,150 | $1.25 | |

Total interest earned | $7.83 | ||

*Interest is calculated on a daily basis and credited into the account every month. The rate of return also applies to earned interests. By following the latter route, you can use Dash PET as a savings account to hive off (and grow) your additional cash each month. i.e. You can transfer the balance money saved into your Dash PET account instead of leaving it in your main savings account and “accidentally” spending it. This could help you practise better financial habits in 2021.

TRANSACT

If you don’t already have the Singtel Dash app, get it! Beyond products like Dash PET, it’s an everyday, all-in-one mobile app that can be used for daily payments (i.e. shopping at literally any shop that accepts Dash, Fave and even PayNow, unlimited online merchants via Dash’s Virtual Visa, commuting) and even remittance services.There’s also a robust Dash Rewards feature within the Singtel Dash app, where you can redeem rewards ranging from Singtel mobile services, grocery, dining, retail and lifestyle vouchers at popular brands.It makes sense that you can seamlessly (and instantly) withdraw the money you’ve grown in your Singtel Dash PET account (from $1) into your Dash wallet and use it immediately to earn even more rewards in your Singtel Dash app.There’s also the option to withdraw money in your linked PayNow account, but there will be a small fee of 70 cents since this is not within the Singtel Dash ecosystem.Remember, we said there’s no lock-in period for Dash PET (just need to maintain the $50 daily average balance in your account value for the calendar month) and capital is guaranteed. And don’t worry about missing out on growing your account value in Dash PET — you can easily do a quick top-up (from $1) once you’ve gotten your salary etc via the Dash wallet or PayNow. Top up in multiples of S$50 applies for eNETS.

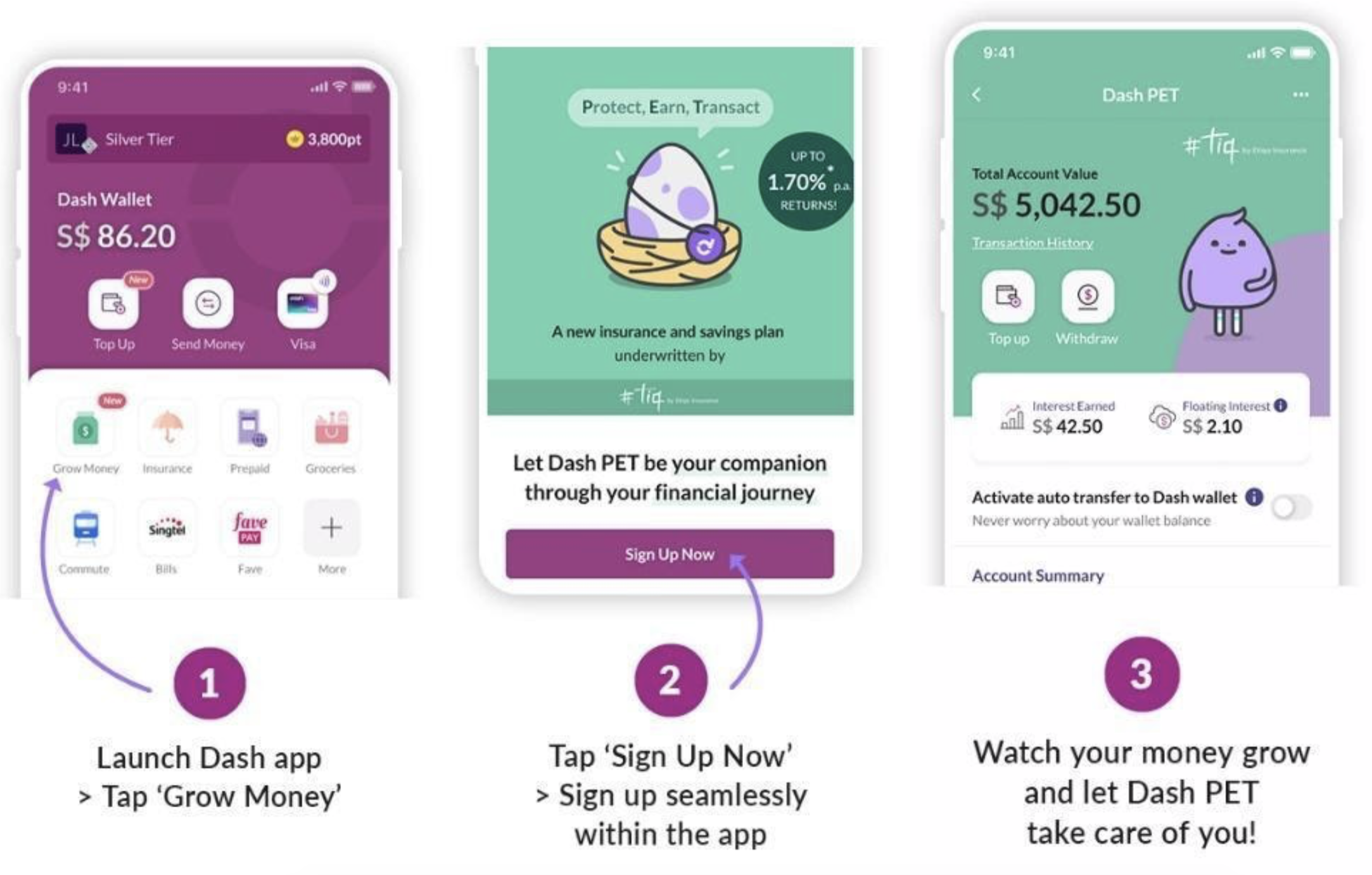

How to get started with Dash PET

To begin your insurance savings journey with Singtel Dash PET, it only takes 3 steps after you download and open the Dash app on your mobile phone. Click here to find out more and to get started with Singtel Dash PET, or head here to download the Singtel Dash app for free.Disclaimer:

Click here to find out more and to get started with Singtel Dash PET, or head here to download the Singtel Dash app for free.Disclaimer:

- The information is meant purely for informational purposes and should not be relied upon as financial advice.

- Dash PET is not a bank account or a fixed deposit. It is an insurance savings plan that earns a crediting interest rate.

- *For the first S$10,000 Account Value: Guaranteed 1.3% p.a. for the first policy year. For above first S$10,000 Account Value: Guaranteed 0.3% p.a. bonus for the first policy year

This policy is underwritten by Etiqa Insurance Pte. Ltd. (Company Reg. No. 201331905K). This advertisement is for general information only. Full details of the policy terms and conditions can be found in the policy contract on dash.com.sg/dashpet. Protected up to specified limits by SDIC. As buying a life insurance policy is a long-term commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid. You should seek advice from a financial adviser before deciding to purchase the policy. If you choose not to seek advice, you should consider if the policy is suitable for you. This advertisement has not been reviewed by the Monetary Authority of Singapore. Information is accurate as at 1 February 2021.

Related Articles