Credit cards are an ubiquitous part of our lives, and still remarkably relevant in Singapore, even amidst the rise of e-wallets and other digital payment methods. It's not uncommon to find Singaporeans carrying as many as 6 cards, drawn by the speed and ease of transactions.

Before you go on swiping (or tapping), it's good to remember the fundamental difference. Unlike debit cards—where funds are taken directly from your bank account—credit card charges are essentially short-term loans extended by card issuers. As with any loan, these are subject to hefty interests, - going as high as 18-27%+.

If you find yourself unable to repay the debts and accrued interest, you risk having your balances rolled over month after month (a trend that contributed to a $8.3B in unpaid credit card debt across Singapore), while slowly digging into a deeper financial hole.

Paying the minimum on credit cards—what's the long-term impact?

- How do minimum payments for credit cards work?

- The pitfalls of paying the minimum of your credit card bill

- How to break free from minimum payments

- In conclusion

1. How do minimum payments for credit cards work?

So when you get your credit card bill and can't (or just don't want to) pay the full amount, what looks like the easiest way out on paper? This is when 'paying the minimum’ comes into play.

Imagine you owe $1,000. On your bill, you'll see a much smaller number called the "Minimum Payment Due." Most banks in Singapore like CitiBank, DBS and HSBC usually calculate this in one of two ways:

- A small percentage of your balance—for example, 2% of $1,000, which is $20.

- A fixed amount—like $25, as long as your total balance is above that amount.

Paying $20-$25 might seem like a relief on the wallet, while avoiding late fees. It might even suggest that you have more money to spend. However, minimum payments might cause you further problems in the long run.

2. The pitfalls of paying the minimum of your credit card bill

First, you’ll get stuck in the interest trap

The reality is, with those high interest rates (18-27% p.a.), a significant portion of your minimum payment will go to covering the interest that has accrued since your last statement,and not the original amount you borrowed (the principal).

- To illustrate—If you carry a $5,000 balance at an 18% rate and only pay the minimum, it will take you over 30 years to pay off that debt. Not only that, you'll pay more than double the original sum in interest (>$10,000).

Even if you're paying on time, you're barely making a dent in what you owe, while interest just keeps piling up on the remaining owed.

Another factor is the generous credit limits often offered by card issuers, frequently reaching3-4 times an individual's monthly income. This can make you overestimate your spending power:

- For example—if you earn $3,000 a month, you can have a credit card that lets you spend up to $12,000. Even if you already owe $5,000, that extra $7,000 might make it seem acceptable to just pay the minimum amount due.

This perceived financial cushion then tempts you to spend further on things you don’t really need, or even consider larger expenses like a vacation or a down payment.

Without realising the slow progress of your debt reduction, and how interest builds up due to overspending, that balance can increase rapidly—especially if you're managing several credit cards.

Second, it’ll impact negatively on your credit score and financial goals

Aside from compounding interest, paying the minimum can impact yourcredit score. As your outstanding credit balance increases, so does your credit utilisation ratio—the proportion of your available credit that you’re currently using.

In Singapore, it's crucial to maintain a healthy credit utilisation ratio, generally considered to be below 30%.

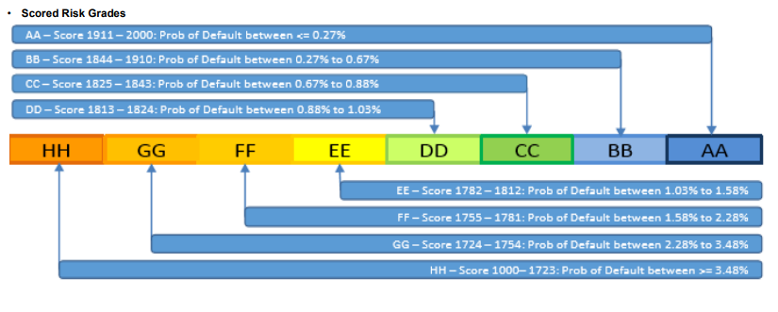

Most lenders, including DBS, OCBC and UOB, rely on credit scores provided by the Credit Bureau Singapore (CBS) to evaluate your creditworthiness. A credit utilisation ratio above that 30% will lower your CBS score. If your score falls below the 'BB' range of 1844-1910, lenders will perceive as a higher risk in managing financial obligations.

Here’s how the CBS Risk Grade are calculated

Image: CBS

A less stellar credit score will also affect your future endeavours—like the ability to secure loans for expensive purchases (think property or vehicles) and may influence aspects like rental applications or insurance premiums.

Consider these scenarios:

- If you want to buy an HDB:

Say you've saved up $700,000 for an HDB loan.

A good credit score could mean a downpayment of just 20%($140,000). But with a lower score, banks might demand 25% upfront ($175,000). That extra $35,000 could take longer to save & delay your homeownership by several years.

- If you’re in your 50s yet stuck with high-interest debt:

With a low credit score, you might face a 25% interest on a $15,000 credit card due to minimum payments.

This forces you to work 2-3 years longer than your planned retirement. That extra interest paid could have been part of your retirement nest.

3. How to break free from minimum payments

Despite these pitfalls, the good news is you can take action. Here are several ways to help you move beyond minimum payments and towards debt freedom:

First off, let’s pay more than minimum (whenever possible)

It's clear that the simplest, most effective way is to pay off more than the minimum due whenever your financial situation allows. Consider these practical approaches:

Round Up Your Payments | Allocate Extra Funds |

If minimum payment is $23, consider paying $30 or $50. Those extra few dollars can make a difference over time. | If you receive a bonus, a tax refund, or any unexpected income, consider putting a portion of it towards your credit card debt. |

Set a Fixed Payment Amount | Cut Unnecessary Expenses |

Instead of paying the minimum plus a little extra, aim for a specific, higher payment amount each month that fits your budget | Take a look at your spending—cutting back on things like eating out or entertainment can free up cash to pay down faster |

Next, applying the debt avalanche/ debt snowball method

If you're juggling debts across different credit cards, here's another smart move—consider the Debt Avalanche or Debt Snowball method. Think of them as structured gameplans to help you tackle those balances one at a time. They're both popular, yet work in slightly different ways:

Debt Avalanche

This method prioritises paying off your debts with the highest interest rates first, regardless of the balance. The idea is to minimise the total amount of interest you pay over time. Mathematically, it’s the most efficient way to save money on interest and pay off your overall debt faster.

How it works:

- Start by creating a clear list of all your debts, paying close attention to the interest rate attached to each one.

- Direct any extra funds you have towards the debt carrying the highest interest rate.

- Once that debt is gone, channel all money you were putting towards it (minimum payment + extra) to the debt with the next highest interest rate.

Debt Snowball

Meanwhile, Debt Snowball focuses on paying off your debts with the smallest balances first, regardless of the interest rate. The idea here is to gain quick wins and boost your morale as you see debts start to disappear.

How it works:

- Begin by making a list of all debts, this time focusing on the total amount you owe on each (smallest balance first).

- Make the minimum payment on all debts.

- Direct any extra money you have towards the debt with the smallest balance.

- Once debt is paid off, take the entire payment you were making on it and add to the minimum payment of the next smallest debt (creating a "snowball" of payment towards larger debts).

Or, start exploring balance transfers/ debt consolidation options

Balance transfer

In Singapore, a balance transfer involves moving the outstanding balance from one or more of your credit cards to a new credit card that offers a promotional period with a0% or very low interest rate.

Unlike minimum payments where much goes to interest, a balance transfer directsmore (if not all) of your payment towards the debt, leading to faster paydown. Furthermore, consolidating multiple card balances onto a single, low-rate card helps simplify your debt management.

However, there are a few things to consider:

- There's a small fee involved—a one-time charge, around 1%-5% of what you're moving over. Do a quick calculation to make sure the interest savings outweigh this cost.

- That super-low rate won't last forever—aim to pay off the balance during the promotional period (usually 3-18 months). This period offers the lowest possible rate, before reverting to the much higher usual rate (19%-26% p.a.) kicks into action.

Note: Balance transfers can also incur late payment penalties—sometimes as high as $60 to $125. Be sure to meet your set repayment sum to avoid these high fees!

When in doubt, check out our list of the Best Balance Transfer Rates in Singapore (2025).

Debt consolidation (through personal loans)

If you're looking at a more substantial overall debt, or find that the 3 to 18-month promotional periods wouldn't realistically allow you to clear your balance, another good option is debt consolidation via a personal loan.

Unlike a balance transfer, debt consolidation involves taking out a separate loan to pay off all your existing credit card debts. The key advantage here is the potential to secure a lower/ fixed interest rate (~3.5%-10.8% p.a.) over an extended and predictable repayment period of 1 to 5 years.

This fixed installment structure makes budgeting far easier and provides a clearer path to becoming debt-free, versus the time-sensitive nature and 'rate shock' that follows a balance transfer's promotional period.

To help you decide, here's a comparison of the two:

Balance Transfer | Personal Loan | |

|---|---|---|

Interest rate | 0% p.a. | 3.5% to 10.8% p.a. |

Processing fee | 1.5% to 5.5% | 1% to 2% |

Repayment period | 3 months to 18 months | 1 to 5 years |

Repayment amount | Varies, but minimum 1% to 3% of outstanding amount per month | Fixed amount per month throughout the term |

Early repayment penalty | No | Yes |

Source: MoneySmart

Check out our list of the Best Personal Loans with Lower Rates & Fast Approval in 2025

4. In Conclusion

Credit cards are super handy in Singapore’s hustle—but don’t let minimum payments quietly drain your wallet. The good news? With a game plan—like paying a bit more each month, using balance transfers, or exploring debt consolidation in Singapore—you can take back control.

Still stuck? Give your card issuer a ring and ask about debt management programs. Pick your path, stick to it, and future-you will thank you.

Found this article useful? Share it with someone who might need it.

Related Articles